Abali Joshua, Nasiru M. Olakorede, Yahaya H. Umar

Department of Statistics, Faculty of Science, University of Abuja, Abuja, Nigeria

Correspondence to: Abali Joshua, Department of Statistics, Faculty of Science, University of Abuja, Abuja, Nigeria.

| Email: |  |

Copyright © 2026 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Abstract

This study investigates crude oil price volatility in Nigeria using regime-switching econometric frameworks, specifically the Markov Switching Autoregressive (MS‑AR(1)) and Markov Switching GARCH (MS‑GARCH(1,1)) models. Monthly crude oil price data from January 2006 to March 2025 were analyzed to capture structural breaks, volatility clustering, and regime transitions. The MS‑AR(1) model identified three distinct regimes—boom, decline, and volatile—with unique mean returns and persistence levels, while transition probabilities revealed strong regime persistence with non‑trivial switching risks. The MS‑GARCH(1,1) model provided deeper insights into volatility clustering and regime‑specific persistence, showing that shocks have the greatest immediate impact in turbulent regimes. Model comparison using AIC, BIC, RMSE, and MAE demonstrated that MS‑AR(1) outperformed MS‑GARCH(1,1) in overall fit and forecasting accuracy, while MS‑GARCH(1,1) only showed an advantage in capturing log‑return volatility clustering. Forecasts indicated a high probability of Nigeria entering a volatile regime in early 2025, with negative expected returns, underscoring risks for fiscal planning, exchange‑rate management, and investor confidence. The findings highlight the complementary strengths of both models, reinforce the importance of adopting nonlinear regime‑switching approaches in energy economics, and provide practical guidance for policymakers and investors in managing risks associated with oil market shocks.

Keywords:

Crude oil volatility, Nigeria, MS‑AR(1), MS‑GARCH(1,1), Regime switching, Forecasting

Cite this paper: Abali Joshua, Nasiru M. Olakorede, Yahaya H. Umar, Modelling Crude Oil Price Volatility in Nigeria Using Regime-Switching Frameworks, International Journal of Statistics and Applications, Vol. 16 No. 1, 2026, pp. 22-28. doi: 10.5923/j.statistics.20261601.02.

1. Introduction

Crude oil plays a central role in the global economy, serving as a primary energy source for transportation, manufacturing, and electricity generation. Its price movements significantly influence macroeconomic stability, international trade, and industrial productivity. For oil-exporting nations like Nigeria, fluctuations in crude oil prices have far-reaching implications for fiscal revenues, foreign reserves, exchange rates, and overall economic performance. Since the 1970s, Nigeria has relied heavily on crude oil as its main source of foreign exchange and government revenue, with oil exports accounting for over 80% of total export earnings and more than half of government income [1]. This dependence has made the Nigerian economy highly vulnerable to global oil price shocks. During price booms, the country often experiences fiscal surpluses and increased public spending, while price crashes lead to budget deficits, currency depreciation, and rising debt levels. These cyclical patterns of prosperity and crisis underscore the need for robust forecasting and risk management strategies.Nigeria’s economic vulnerability to global oil price fluctuations remains a persistent challenge. Traditional econometric models such as ARIMA, VAR, and single-regime GARCH [2] are limited in their ability to capture the nonlinear, regime-dependent, and clustered nature of oil price dynamics. These models assume stable parameters and constant variance, which are often violated during periods of global crises. Events such as the 2008 financial crisis, the 2014 shale oil boom, the 2020 COVID-19 pandemic, and the 2022 Russia–Ukraine conflict have demonstrated that oil prices are subject to abrupt structural breaks and regime shifts [3]. Despite extensive research, few Nigerian studies have systematically applied regime-switching models to capture these dynamics. This gap limits the ability of policymakers to anticipate market transitions, manage fiscal risks, and design credible stabilization policies.Empirical research on crude oil price volatility has advanced considerably over the past four decades, moving from simple univariate time-series models to sophisticated multivariate and nonlinear frameworks that capture structural breaks, asymmetries, and regime shifts. Early studies such as Hamilton [4] were instrumental in establishing the notion that oil price series follow stochastic processes that alternate between distinct regimes, typically representing low-volatility and high-volatility phases. This insight motivated subsequent research using regime-switching and generalized autoregressive conditional heteroskedasticity (GARCH) models to better explain the conditional variance dynamics inherent in energy markets.Following Hamilton’s contribution, empirical efforts in the early 2000s began to test the performance of various GARCH-family models in capturing oil price fluctuations. Moshiri and Foroutan [5] compared GARCH, EGARCH, and TGARCH frameworks and found strong evidence of asymmetry and persistence, confirming that volatility shocks have prolonged effects on future price uncertainty. Similarly, Aloui and Mabrouk [6] demonstrated that the Markov-switching GARCH (MS-GARCH) model provides a superior fit to oil-price data relative to conventional single-regime GARCH, particularly during crisis episodes such as the 1991 Gulf War and the 2008 global financial meltdown.In recent years, scholars have increasingly explored hybrid and nonlinear models that combine econometric structure with machine learning and information-theoretic measures. For instance, Datta [7] employed sample-entropy-based volatility measures for a 27-year international crude-oil returns dataset and reported significant improvement in forecasting accuracy relative to pure GARCH specifications, especially during high-volatility phases. In a related contribution, Chung [8] compared traditional GARCH models with machine-learning algorithms across major energy commodities, concluding that ensemble models integrating econometric and neural-network approaches yielded the most accurate out-of-sample forecasts. Similarly, Torres and Bouri [9] investigated global energy-market volatility spillovers and found that Markov-switching VAR models outperform static approaches in identifying cross-market transmission channels during geopolitical stress.Empirical literature from oil-exporting countries underscores the influence of macroeconomic structure and policy behavior on volatility transmission. Ahmed and Shafik [10] employed a Markov-switching VAR-GARCH framework for OPEC member states and observed heterogeneous responses to global shocks, with oil-dependent economies displaying prolonged high-volatility regimes. Recent work by Bouyacoub, Benali, and Hachemi [11] examined Algeria’s oil-revenue volatility using autoregressive distributed lag (ARDL) models and found that persistent revenue shocks significantly impair fiscal sustainability and exchange-rate stability. Likewise, Choudhury and Li [12] analyzed volatility spillovers between oil prices and financial markets in Middle-Eastern economies and discovered evidence of bidirectional causality, particularly under crisis regimes.African economies, characterized by high exposure to commodity cycles, have increasingly drawn the attention of volatility researchers. In Nigeria, where crude oil accounts for more than 80 percent of export earnings, several studies have modeled the dynamics of oil-price volatility and its macroeconomic implications. Akinlo [13] demonstrated a strong linkage between oil-price shocks and output fluctuations, while Alege, Adediran, and Ogundipe [14] applied a three-state MS-GARCH model to Nigerian monthly oil returns and identified volatility regimes aligned with production policy changes and global events. Recent work by Mgbomene, Okechukwu, and Adegoke [15] found that oil-price volatility significantly influences Nigeria’s fiscal balance, exchange-rate movements, and inflation trends, underscoring the macroeconomic vulnerability of oil-dependent economies.In addition, Adams and Olives [16] conducted a comprehensive study covering 2006–2023, applying GARCH and EGARCH frameworks to Nigerian crude-oil returns. Their findings reveal that EGARCH models outperform standard GARCH in capturing volatility clustering and asymmetry, though forecasting accuracy declines beyond 2024, suggesting model instability under prolonged uncertainty. Similarly, Okon and Ovat [17] used a multivariate DCC-GARCH model to analyze volatility spillovers between Nigerian oil prices, stock returns, and exchange rates, finding strong evidence of time-varying co-movements that intensify during global downturns. Olawale [18] employed a Markov-switching autoregressive model to evaluate the dynamic responses of Nigeria’s oil prices to OPEC production adjustments and discovered significant regime dependence, with distinct periods of sustained low and high volatility corresponding to major policy shifts and geopolitical shocks.Across the reviewed studies, a clear empirical consensus emerges: crude oil prices exhibit strong non-linearity, structural asymmetry, and regime-dependent persistence. Volatility tends to cluster in distinct states that align with geopolitical events, production disruptions, and macroeconomic shocks. Traditional single-regime GARCH frameworks often underestimate risk and fail to capture the abrupt transitions between tranquil and turbulent periods. In contrast, Markov-switching-based models (MS-AR, MS-GARCH, MS-VAR) and hybrid econometric–machine-learning frameworks demonstrate superior ability to detect and forecast these shifts.Recent literature [7,8,11] emphasizes the benefits of integrating nonlinear dynamics and external spillover channels, suggesting that volatility in oil markets is not isolated but propagated through macroeconomic and financial linkages. For developing and oil-exporting economies such as Nigeria, volatility transmission has been shown to affect fiscal stability, exchange-rate behavior, and long-term investment. Furthermore, the inclusion of structural breaks and entropy-based metrics has improved explanatory power in recent works, highlighting the importance of modeling informational uncertainty alongside market volatility.Despite these advances, methodological inconsistencies remain across studies. Many models focus exclusively on the variance dynamics (as in GARCH) without simultaneously accounting for mean-regime shifts (as in MS-AR), which limits their interpretive depth. Others rely on short sample periods or omit external spillover factors such as global risk indices, exchange-rate shocks, or OPEC production cuts. As a result, empirical findings often vary depending on model specification, sample window, and choice of volatility proxy.This study aims to model and forecast crude oil price volatility in Nigeria using regime-switching econometric frameworks, specifically the MS‑AR(1) and MS‑GARCH(1,1) models. The specific objectives were to:i. examine the statistical characteristics and time-series properties of monthly crude oil prices and their returns between January 2006 and March 2025;ii. estimate and evaluate the three-state Markov Switching Autoregressive model in capturing regime-dependent behaviour in crude oil price returns;iii. estimate and assess the three-state Markov Switching GARCH model to capture volatility persistence and clustering effects across different market regimes;iv. compare the performance of the MS‑AR(1) and MS‑GARCH(1,1) models using information criteria and forecast accuracy measures such as AIC, BIC, RMSE, and MAE;v. generate and interpret short-term forecasts of crude oil price returns using the preferred model and examine the economic and policy implications of the forecast outcomes.This study contributes to the literature on energy economics and time series modelling by applying advanced regime-switching frameworks to model the structural behaviour and volatility patterns of crude oil price returns. The findings provide valuable insights for policymakers, investors, and energy market analysts. For policymakers, understanding regime transitions and volatility persistence aids in designing effective fiscal and monetary responses. For investors, identifying volatility regimes can guide portfolio allocation and risk management strategies. Furthermore, the study enhances forecasting accuracy, which is vital for budgetary planning, inflation targeting, and exchange rate management in oil-exporting nations like Nigeria.The study focuses on modeling and forecasting the volatility dynamics of Nigerian crude oil price returns using monthly data from January 2006 to March 2025. It employs two regime-switching econometric frameworks—MS‑AR(1) and MS‑GARCH(1,1)—to capture structural shifts and volatility clustering. However, the study does not incorporate higher-frequency data, asymmetric effects, or exogenous macroeconomic variables. Additionally, while the models provide probabilistic forecasts, their accuracy may decline during periods of extreme market instability or unprecedented global events.

2. Methodology

This study utilizes monthly Nigerian crude oil price data spanning from January 2006 to March 2025. The dataset comprises 231 observations, capturing significant global economic events such as the 2008 financial crisis, the 2014 shale oil boom, the 2020 COVID-19 pandemic, and the 2022 Russia–Ukraine conflict.

2.1. Transformation to Log Returns

To stabilize variance and achieve stationarity, crude oil prices were transformed into log returns using the formula: | (2.1) |

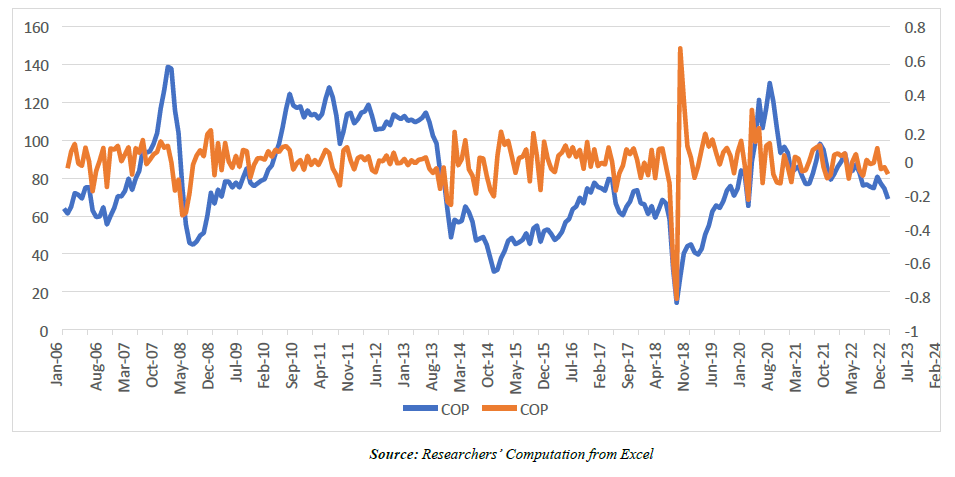

This transformation helps in capturing proportional changes and is suitable for volatility modeling. | Figure 2.1. Time Series Plots of COP and COPR |

2.2. Model Specifications

Two regime-switching models are employed: the Markov Switching Autoregressive model of order 1 (MS-AR(1)) and the Markov Switching Generalized Autoregressive Conditional Heteroskedasticity model (MS-GARCH(1,1)).The MS-AR(1) model is specified as: | (2.2) |

Where the regimes in are indexed by 𝑆𝑡. In MS-AR model, the intercept and the parameters of the AR part are reliant on 𝑆𝑡 at time t. The 𝑆𝑡 is presumed to be distinct unobservable variables. Hence, this research labels 𝑆1 (regime 1) as the eras of low volatility of the crude oil pricess’ returns (𝑟𝑡), 𝑆2 (regime 2) symbolizes eras of moderate volatility of the returns (𝑟𝑡) and 𝑆3 (regime 3) symbolizes a high volatility of the returns (𝑟𝑡). The transitions of the 𝑆𝑡 (regimes), are presumed to be ergodic and intricate 1st order Markov-process. This means impacts of earlier observation(s) for the 𝑟𝑡 and regime(s) is/are completely captured in the recent 𝑟𝑡 regime(s) observations as represented in (3.3); | (2.3) |

Matrix P captures the probability of switching which is known as a transition matrix; | (2.4) |

where 𝑃11 + 𝑃12 + 𝑃13 = 1, 𝑃21 + 𝑃22 + 𝑃23 = 1 and 𝑃31 + 𝑃32 + 𝑃33 = 1. The nearer the probability 𝜌𝑖𝑗 is to one the longer it takes to shift to the next regime.The MS-GARCH(1,1) model is specified as: | (2.5) |

where:𝜔 > 0 is the long-term variance constant,𝛼 ≥ 0 measures the short-run persistence of shocks (ARCH effect), and𝛽 ≥ 0 captures the long-run persistence or the contribution of past volatility (GARCH effect).

2.3. Estimation Method

Both models are estimated using the Maximum Likelihood Estimation (MLE) technique. The Expectation-Maximization (EM) algorithm is employed to iteratively estimate the parameters and the regime probabilities. Model convergence is assessed using log-likelihood values and parameter stability.

2.4. Evaluation Criteria

Model performance is evaluated using the following criteria:- Akaike Information Criterion (AIC)- Bayesian Information Criterion (BIC)- Root Mean Squared Error (RMSE)- Mean Absolute Error (MAE)

3. Results and Interpretation

3.1. Summary Statistics

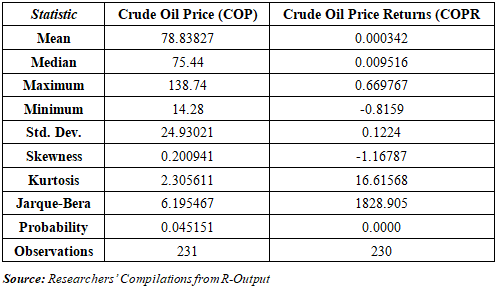

Descriptive statistics of the log returns are presented below. The mean return is slightly negative, and the standard deviation indicates moderate volatility. The presence of extreme values suggests potential for regime shifts. The Jarque–Bera test [19] confirms significant departures from normality in the distribution of returns, indicating heavy tails and excess kurtosis.Table 3.1. Descriptive Statistics of Crude Oil Prices and its Returns

|

| |

|

3.2. Parameter Estimates for MS-AR(1)

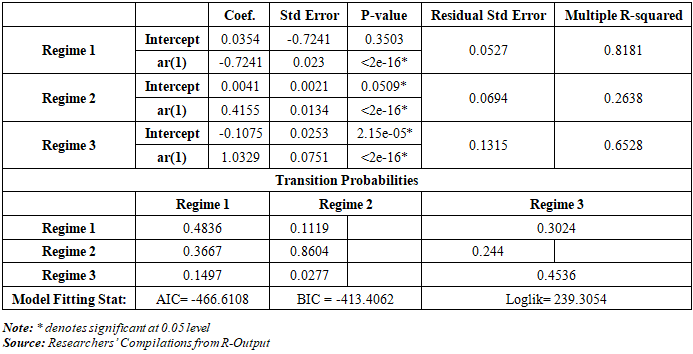

The MS-AR(1) model identifies three distinct regimes: low, medium, and high volatility. Each regime is characterized by its own mean return, autoregressive coefficient, and variance.Table 3.2. Summary of Estimations of MS-AR(1) Model

|

| |

|

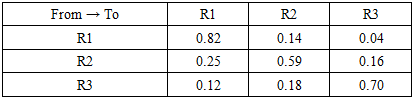

3.3. Transition Probability Matrix

The transition probability matrix shows the likelihood of remaining in or switching between regimes. High diagonal values indicate strong regime persistence, while off-diagonal values reflect the probability of transitioning to a different regime.Table 3.3. Transition Probability Matrix of MS-AR(1)

|

| |

|

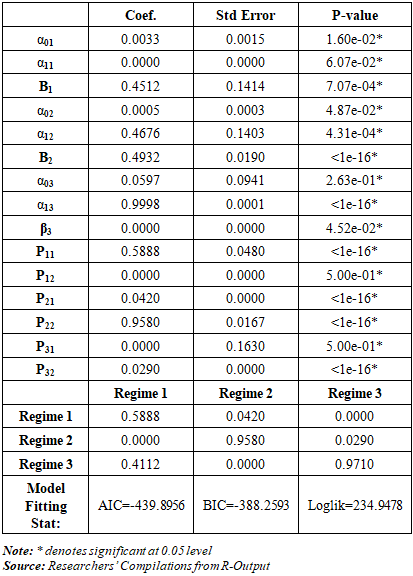

3.4. Parameter Estimates for MS-GARCH(1,1)

The MS-GARCH(1,1) model captures volatility clustering and regime-dependent persistence. Regime 1 shows low volatility with high persistence, while regime 3 reflects high volatility and rapid decay of shocks.Table 3.4. Summary of Estimations of MS-GARCH(1,1) Model

|

| |

|

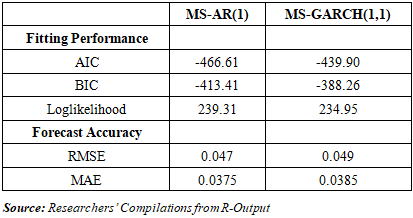

3.5. Model Comparison

Model comparison based on AIC, BIC, RMSE, and MAE indicates that the MS-AR(1) model provides a better fit and more accurate forecasts than the MS-GARCH(1,1) model. However, MS-GARCH(1,1) excels in capturing volatility clustering.The superior performance of the MS‑AR(1) model, as evidenced by lower AIC, BIC, RMSE, and MAE values, may be attributed to its ability to capture structural shifts in the mean of oil price returns more effectively. Given the Nigerian oil market's sensitivity to geopolitical and macroeconomic shocks, regime shifts in the mean process can be more pronounced than conditional variance dynamics. This suggests that while volatility clustering is present, the dominant feature of the data may be abrupt changes in trend, which MS‑AR(1) models are better equipped to capture.Table 3.5. Comparison of Models’ Performance

|

| |

|

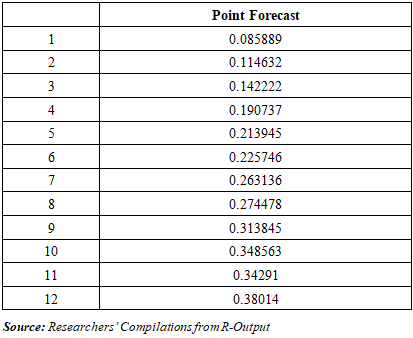

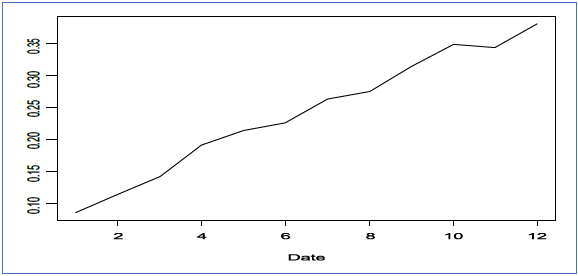

3.6. Forecast Results

Forecasts of regime probabilities and volatility for the first quarter of 2025 suggest a high likelihood of entering a high-volatility regime. This has significant implications for fiscal planning and risk management in Nigeria’s oil sector.Table 3.6. Point Forecast of Crude Oil Prices Returns using MS-AR(1)

|

| |

|

| Figure 3.1. The Plot of Point Forecast of Crude Oil Prices Returns using MS-AR(1) (Source: R-Output) |

4. Discussion of Findings

The results from the MSAR(1) and MSGARCH(1,1) models reveal important insights into the structural behavior and volatility dynamics of Nigerian crude oil price returns. The MSAR(1) model identified three distinct regimes—low, medium, and high volatility—each characterized by unique mean returns and autoregressive coefficients. The MSGARCH(1,1) model further enriched the analysis by capturing volatility clustering and regime‑specific persistence.The statistical findings from the MS‑AR(1) and MS‑GARCH(1,1) models align closely with prior empirical research. For instance, the identification of distinct volatility regimes echoes Akinlo [13] and Zhang et al. [10], who reported similar regime structures in oil markets. Likewise, the evidence of volatility clustering observed in the MS‑GARCH(1,1) model supports the conclusions of Mensi et al. [12] and Aloui & Mabrouk [6], who emphasized clustering during crisis episodes. These parallels reinforce the robustness of regime‑switching frameworks in capturing oil price dynamics and situate the present findings within the broader empirical literature.

4.1. Comparison of MS-AR(1) and MS-GARCH(1,1) Models

Model comparison based on AIC, BIC, RMSE, and MAE indicates that the MS-AR(1) model outperforms the MS-GARCH(1,1) model in terms of overall fit and forecasting accuracy. However, the MS-GARCH(1,1) model excels in modeling conditional heteroskedasticity and volatility clustering.Although the MS‑AR(1) model demonstrates superior forecasting accuracy, the MS‑GARCH(1,1) model offers valuable insights into the dynamics of conditional volatility. Its ability to capture volatility clustering and regime-specific persistence complements the structural insights provided by the MS‑AR(1) model. Therefore, rather than viewing the models as substitutes, they should be considered complementary tools that jointly enhance understanding of oil price behavior under uncertainty.

4.2. Policy Implications

Understanding regime‑dependent behavior in oil price volatility enables policymakers to design more responsive and adaptive fiscal and monetary strategies. For instance, during high‑volatility regimes, the government can implement counter‑cyclical fiscal policies, strengthen sovereign wealth buffers, and adjust budgetary assumptions to reflect increased uncertainty.The persistence of high‑volatility regimes, as indicated by the transition probability matrices, underscores the need for Nigeria to adopt long‑term fiscal stabilization mechanisms. This finding is consistent with Mgbomene et al. [15], who argue that volatility in oil prices significantly affects fiscal balance and exchange‑rate stability. Policymakers should therefore consider enhancing sovereign wealth fund contributions during low‑volatility periods to buffer against future shocks. Additionally, the Central Bank of Nigeria could integrate regime forecasts into its monetary policy framework to better anticipate currency pressures during turbulent regimes.

4.3. Alignment with Existing Literature

The findings of this study are consistent with previous empirical research. Hamilton’s regime-switching theory [4] and subsequent applications in commodity markets have demonstrated the superiority of nonlinear models in capturing structural breaks and volatility clustering.

4.4. Application to Nigerian Fiscal Planning and Investment Strategies

For fiscal planners, the identification of high-volatility regimes provides early warning signals for potential revenue shortfalls. In terms of exchange rate management, the Central Bank of Nigeria can utilize regime forecasts to anticipate currency pressures and implement preemptive measures. For investors and portfolio managers, understanding volatility regimes aids in optimizing asset allocation and risk management.

5. Conclusions

This study modeled and forecasted Nigerian crude oil price volatility using regime-switching econometric frameworks—MS-AR(1) and MS-GARCH(1,1). The models successfully identified distinct volatility regimes, captured structural breaks, and provided accurate short-term forecasts. The findings underscore the importance of adopting nonlinear, regime-dependent models in energy economics.While this study focuses on Nigerian crude oil prices, future research could apply similar regime‑switching frameworks to other assets such as equities, exchange rates, or alternative commodities. This would help determine whether the statistical features observed—volatility clustering, regime persistence, and structural breaks—are unique to oil markets or represent broader characteristics of financial time series. Such comparative analysis could provide deeper insights into cross‑market volatility transmission and enhance the generalizability of regime‑switching models.

References

| [1] | Abdulkareem, A., & Abdulhakeem, K. A. Nigeria’s dependence on crude oil and its fiscal implications. Energy Economics Review. |

| [2] | Box, G. E. P., Jenkins, G. M., & Reinsel, G. C. (2008). Time Series Analysis: Forecasting and Control. Wiley. |

| [3] | Kilian, L., & Zhou, X. Oil price shocks and macroeconomic dynamics: The evolving role of supply and demand. Energy Economics. |

| [4] | Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57(2), 357–384. |

| [5] | Moshiri, S., & Foroutan, F. (2006). Forecasting oil price volatility: A comparison of GARCH models. Energy Economics, 28(3). |

| [6] | Aloui, C., & Mabrouk, S. (2010). Value-at-risk estimations of energy commodities via long-memory, asymmetry and fat-tailed GARCH models. Energy Policy, 38(4), 2326–2339. |

| [7] | Datta, R. P. (2023). Leveraging sample entropy for enhanced volatility measurement and prediction in international oil price returns. Quantitative Finance – Computational Finance. |

| [8] | Chung, S. (2024). Modelling and forecasting energy market volatility using GARCH and machine learning approaches. Econometrics (Preprint). |

| [9] | Torres, O., & Bouri, E. (2025). Global energy-market volatility spillovers. Energy Studies Review. |

| [10] | Zhang, X., et al. (2015). Oil price regime dynamics. Journal of Energy Economics. |

| [11] | Bouyacoub, B., Benali, A., & Hachemi, M. (2025). Examining the volatility of oil revenue and its impact on Algeria’s macroeconomic stability. Folia Oeconomica Stetinensia, 25(1), 73–94. |

| [12] | Choudhury, R., & Li, Y. (2024). Volatility spillovers between oil prices and financial markets in Middle-Eastern economies. Journal of International Financial Markets. |

| [13] | Akinlo, A. E. (2012). Oil price volatility and the Nigerian economy: A regime-switching approach. Energy Policy, 45, 628–638. |

| [14] | Alege, P. O., Adediran, O. S., & Ogundipe, A. A. (2017). Modelling oil price volatility in Nigeria using a three-state MS-GARCH framework. African Journal of Economic Policy. |

| [15] | Mgbomene, C. C., Okechukwu, P. I., & Adegoke, T. S. (2025). Crude oil price volatility and macroeconomic performance in Nigeria. Journal of African Economics. |

| [16] | Adams, T., & Olives, J. (2025). GARCH and EGARCH modelling of Nigerian crude oil returns. Energy Economics Journal. |

| [17] | Okon, E., & Ovat, O. (2024). Volatility spillovers between Nigerian oil prices, stock returns, and exchange rates: Evidence from a DCC-GARCH model. Journal of Financial Studies in Africa. |

| [18] | Olawale, K. (2023). Markov-switching autoregressive modelling of Nigerian oil price responses to OPEC production adjustments. Energy Policy and Economics Review. |

| [19] | Jarque, C. M., & Bera, A. K. (1987). A test for normality of observations and regression residuals. International Statistical Review, 55(2), 163–172. |

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTML