-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Statistics and Applications

p-ISSN: 2168-5193 e-ISSN: 2168-5215

2019; 9(4): 122-127

doi:10.5923/j.statistics.20190904.04

Construction of Bivariate Distribution by Mixing Positively Dependent and Negatively Dependent Distributions

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLMuhammet Bekçi1, Mehmet Yılmaz2

1Sivas Cumhuriyet University, Faculty of Science, Department of Statistics and Computer Sciences, Sivas, Turkey

2Ankara University, Faculty of Science, Department of Statistics, Ankara, Turkey

Correspondence to: Muhammet Bekçi, Sivas Cumhuriyet University, Faculty of Science, Department of Statistics and Computer Sciences, Sivas, Turkey.

| Email: |  |

Copyright © 2019 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

In this paper, a new method for constructing bivariate distributions with given marginals is proposed, based on a mixing two bivariate distributions. A new bivariate distribution family is introduced by adding an appropriate term with independence class of distribution. During this construction process, the model is not complicated. By choosing a base distribution from the same marginals we derive a new distribution around the independent class. We note that the new distribution has additional parameter which would provide additional flexibility in applications. The joint probability density, joint reliability and reversed hazard rate functions of the new bivariate distribution are obtained. Furthermore, it is established that construction of bivariate distributions by this method allows for some flexibility in the values of Spearman’s correlation coefficient.

Keywords: Dependence, Bivariate Distribution, Spearman’s Rho, Fréchet Bounds

Cite this paper: Muhammet Bekçi, Mehmet Yılmaz, Construction of Bivariate Distribution by Mixing Positively Dependent and Negatively Dependent Distributions, International Journal of Statistics and Applications, Vol. 9 No. 4, 2019, pp. 122-127. doi: 10.5923/j.statistics.20190904.04.

Article Outline

1. Introduction

- Univariate models are insufficient to explain random phenomena. Today, data such as drought, wind speed and rainfall are measured together with the variables that may affect them. With the development of technology, the construction of continuous bivariate distribution functions with given marginals has become an importance. When creating new bivariate distributions, models that can express high correlation are generally tried to be obtained. [2] introduced a method which based on the choice of pairs of order statistics of the marginal distributions. [8] studied on construction of continuous bivariate distributions that possesses the Positive Quadrant Dependence property. [13] introduced a generalization of Farlie-Gumbel-Morgentern (FGM) distribution family. They extend the maximal correlation coefficient for FGM family. Furthermore, [14] introduced bivariate and multivariate generalization of quadratic transmutation distribution family. Proposal of [14] draws our attention in particular. Because the transition from univariate case to bivariate or multivariate cases is not so easy. While in univariate case the real line is the complement of the probabilities, at least in the bivariate case these supplements are on the quadrant. There are some issues to overcome for the case of positive values of the transmutation parameter. However, marginals of this model are univariate transmuted distributions and it cannot detect independency. They proposed quadratic rank transmuted bivariate distribution as

, where

, where  . Here, for

. Here, for  gives the base distribution

gives the base distribution  . However, if the base distribution is taken from independency case, i.e.,

. However, if the base distribution is taken from independency case, i.e.,  , then

, then  can be written as in the eq. (2) of [8] follows:

can be written as in the eq. (2) of [8] follows:  . For

. For  ,

,  cannot meet the conditions (4) and (5) proposed by [8]. Inspired by these studies, the contribution of the article is to propose a simpler but more useful model than the model introduced by [14]. Proposed model also includes both positive and negative values of the parameter as in FGM. Thus, the model gains some flexibility in modeling both positive and negative dependence. Furthermore, proposed model can detect independency. After giving the necessary conditions to construct a new distribution, Spearman's rank correlation coefficient is calculated on two illustrative examples and the usefulness of this family is discussed. Furthermore, some reliability properties are studied for this family.Let

cannot meet the conditions (4) and (5) proposed by [8]. Inspired by these studies, the contribution of the article is to propose a simpler but more useful model than the model introduced by [14]. Proposed model also includes both positive and negative values of the parameter as in FGM. Thus, the model gains some flexibility in modeling both positive and negative dependence. Furthermore, proposed model can detect independency. After giving the necessary conditions to construct a new distribution, Spearman's rank correlation coefficient is calculated on two illustrative examples and the usefulness of this family is discussed. Furthermore, some reliability properties are studied for this family.Let  denote the bivariate distribution function of

denote the bivariate distribution function of  having continuous marginal cdfs

having continuous marginal cdfs  and

and  . Also, let

. Also, let  be the distribution family where the respective marginal are F and G. Then, according to the eq. (2) and the condition (3) of [8], we have the function

be the distribution family where the respective marginal are F and G. Then, according to the eq. (2) and the condition (3) of [8], we have the function  where

where  denotes survival function. This function meets the conditions (3)-(5) given by [8]. Hence, first mixture component distribution is

denotes survival function. This function meets the conditions (3)-(5) given by [8]. Hence, first mixture component distribution is  . Similar work of [8] given by [15] introduces some conditions for negatively dependent families. According to the eq. (2.1) and the condition (2.1) of [15], we have

. Similar work of [8] given by [15] introduces some conditions for negatively dependent families. According to the eq. (2.1) and the condition (2.1) of [15], we have  . Except for the condition (2.3) of [15], this function meets the conditions (2.2) and (2.4) given by [15]. Distribution properties for the second mixture component

. Except for the condition (2.3) of [15], this function meets the conditions (2.2) and (2.4) given by [15]. Distribution properties for the second mixture component  have not yet been provided. To overcome this issue, we have the following theorem. Theorem 1. Let

have not yet been provided. To overcome this issue, we have the following theorem. Theorem 1. Let  be a distribution function belongs to the distribution family

be a distribution function belongs to the distribution family  which is differentiable on

which is differentiable on  and

and  denote the joint probability density function. Then (i)

denote the joint probability density function. Then (i)  is a distribution function,(ii)

is a distribution function,(ii)  is a distribution function if

is a distribution function if  ,

,  .Proof. (i) Multivariate distribution function must satisfy following properties: (P1)

.Proof. (i) Multivariate distribution function must satisfy following properties: (P1)  (P2)

(P2)  and

and  . For the simplicity

. For the simplicity  and

and

.Obviously,

.Obviously,  .(P3)

.(P3)  . For the simplicity, let

. For the simplicity, let  and

and  . Then

. Then Now, by noting that positively dependence implies

Now, by noting that positively dependence implies  , then we have

, then we have  . Also, negatively dependence implies both

. Also, negatively dependence implies both  and

and  . Hence, we have

. Hence, we have  (ii) According to [4], Additionally to the properties (P1)-(P3), to determine bivariate distribution uniquely by its marginals bivariate distribution must lie upper and lower Fréchet bounds. Therefore, this idea explains why we need negative dependence for the construction of distribution given in (ii).(P1)

(ii) According to [4], Additionally to the properties (P1)-(P3), to determine bivariate distribution uniquely by its marginals bivariate distribution must lie upper and lower Fréchet bounds. Therefore, this idea explains why we need negative dependence for the construction of distribution given in (ii).(P1)  (P2)

(P2)  and

and  .

.  Obviously,

Obviously,  .(P3)

.(P3)  .

.  Negatively dependence implies

Negatively dependence implies  . Hence, we have

. Hence, we have  However, if X and Y are positively dependent,

However, if X and Y are positively dependent,  can not bigger than Fréchet lower bound. Therefore, the assumption of negative dependence is needed. To show this situation, we assume

can not bigger than Fréchet lower bound. Therefore, the assumption of negative dependence is needed. To show this situation, we assume  . Then we have

. Then we have As it can be seen that positivity of the above statement depends on

As it can be seen that positivity of the above statement depends on  .According to Theorem 1, first mixture component distribution can be positively, negatively dependent or independent. But the second component distribution must be negatively dependent or independent. Thus, for the base distribution

.According to Theorem 1, first mixture component distribution can be positively, negatively dependent or independent. But the second component distribution must be negatively dependent or independent. Thus, for the base distribution  , in order to be same structure for both mixture components, the random variables X and Y must be negatively dependent or independent. After this motivation, we can now propose the mixing of these two distributions as follows: Let T and V be negatively dependent (or independent) continuous random variables. Then their joint distribution function denoted as

, in order to be same structure for both mixture components, the random variables X and Y must be negatively dependent or independent. After this motivation, we can now propose the mixing of these two distributions as follows: Let T and V be negatively dependent (or independent) continuous random variables. Then their joint distribution function denoted as  belongs to the distribution family

belongs to the distribution family  where F and G denote respectively marginals of T and V. Let

where F and G denote respectively marginals of T and V. Let  and

and  respectively denote the distribution functions of

respectively denote the distribution functions of  and

and  having the same marginals as H. The distribution functions of

having the same marginals as H. The distribution functions of  and

and  are respectively defined by

are respectively defined by | (1) |

| (2) |

denotes survival function of

denotes survival function of  i.e.,

i.e.,  . As can be seen immediately from equations (1) and (2),

. As can be seen immediately from equations (1) and (2),  and

and  are positively dependent random pairs, and

are positively dependent random pairs, and  and

and  are negatively dependent random pairs.According to Therorem 1, we can define a new pairs of random variables X and Y as below:

are negatively dependent random pairs.According to Therorem 1, we can define a new pairs of random variables X and Y as below: Hence, the distribution of

Hence, the distribution of  obtained by mixing (1) and (2) which is given by

obtained by mixing (1) and (2) which is given by | (3) |

, where

, where  , eq. (3) can be rewritten as

, eq. (3) can be rewritten as | (4) |

indicates

indicates  i.e., independence of X and Y,

i.e., independence of X and Y,  indicates that X and Y negatively dependent, and

indicates that X and Y negatively dependent, and  indicates positive dependence between X and Y. Note that X and Y are independent from each other, F indicates well-known bivariate distribution which is Farlie-Gumbel-Morgenstern distribution (see, [3] and [5]).We need the survival and probability density function for subsequent discussions. These functions are respectively given by

indicates positive dependence between X and Y. Note that X and Y are independent from each other, F indicates well-known bivariate distribution which is Farlie-Gumbel-Morgenstern distribution (see, [3] and [5]).We need the survival and probability density function for subsequent discussions. These functions are respectively given by and

and where

where  .

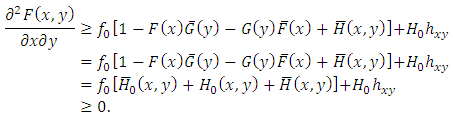

.2. Reversed Hazard Rate of the New Family of Bivariate Distribution

- The bivariate reversed hazard is defined by [1] as

. Analogously to the hazard gradient by [7], [11] defined the bivariate reversed hazard rate as follows:

. Analogously to the hazard gradient by [7], [11] defined the bivariate reversed hazard rate as follows:  , where

, where Reversed hazard rate gradients of

Reversed hazard rate gradients of  given by eq. (4) are as follows:

given by eq. (4) are as follows: Accordingly, after some simplifications, bivariate reversed hazard rate can be given by

Accordingly, after some simplifications, bivariate reversed hazard rate can be given by

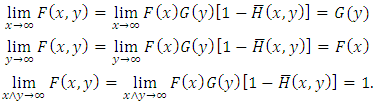

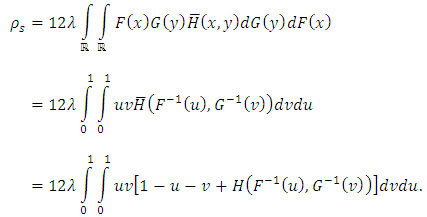

3. Lower and Upper Bounds on Spearman’s Rho Measure for the New Family of Bivariate Distribution

- This section deals with obtaining bounds for the bivariate distribution family given by the eq. (4). According to [6] and [4], for any bivariate distribution belonging to

contains Fréchet a lower bound and an upper bound. These bounds are respectively defined as

contains Fréchet a lower bound and an upper bound. These bounds are respectively defined as  | (5) |

| (6) |

, Spearman’s rho can be expressed as

, Spearman’s rho can be expressed as | (7) |

| (8) |

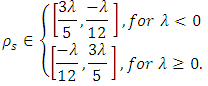

, we have the lower bound as

, we have the lower bound as  To obtain the upper bound, we use the eq. (6), then

To obtain the upper bound, we use the eq. (6), then According to sign of

According to sign of  , we achieve the bounds as below:

, we achieve the bounds as below: We have two example to illustrate this family.Example 1. The Farlie-Gumbel-Morgenstern (FGM) family of bivariate distributions are given by

We have two example to illustrate this family.Example 1. The Farlie-Gumbel-Morgenstern (FGM) family of bivariate distributions are given by  , for

, for  . By taking

. By taking  , the distribution

, the distribution  is given by

is given by  where

where  and

and  . Hence,

. Hence,  . Since

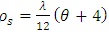

. Since  . One can conclude that this family model weak dependence as FGM does.Example 2. The bivariate Gumbel- Exponential (BGE) distribution is given by

. One can conclude that this family model weak dependence as FGM does.Example 2. The bivariate Gumbel- Exponential (BGE) distribution is given by  , for

, for  . The distribution

. The distribution  is given by

is given by  , where

, where  and

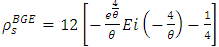

and  . According to [9], the Spearman’s rho coefficient of BGE distribution is

. According to [9], the Spearman’s rho coefficient of BGE distribution is  , where

, where  is the exponential integral function. After some algebraic manipulation,

is the exponential integral function. After some algebraic manipulation,  can be obtained as

can be obtained as

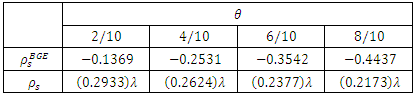

- We calculate approximates values of

and

and  by using Maple with respect to some values of

by using Maple with respect to some values of  . Tabulated values are given as Table 1 below:

. Tabulated values are given as Table 1 below:

|

4. Conclusions

- In this study, we proposed a new bivariate distribution using a base distribution from the negative dependency class which is in

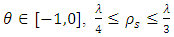

. Thus, this new distribution can reveal both negative dependence, positive dependence and independence between the random variables X and Y. The upper and lower bounds show that the values of the correlation coefficient for this family lies in the interval

. Thus, this new distribution can reveal both negative dependence, positive dependence and independence between the random variables X and Y. The upper and lower bounds show that the values of the correlation coefficient for this family lies in the interval  . Besides, as a result of illustrative examples, it can be said that distributions can be derived for pairs of random variables with higher correlations considering some base distributions. For further discussion, focusing on the negative dependence condition on

. Besides, as a result of illustrative examples, it can be said that distributions can be derived for pairs of random variables with higher correlations considering some base distributions. For further discussion, focusing on the negative dependence condition on  , a new distribution family can be derived with any distribution function from

, a new distribution family can be derived with any distribution function from  .

.ACKNOWLEDGEMENTS

- We thank anonymous referees for their valuable suggestions and constructive comments which helped us in revising the paper in the present form.