Khalil Ghazzawi 1, Sam El Nemar 2, Ali Sankari 3, Samer Tout 3, Hassan Dennaoui 4, Radwan el Shoghari 1

1Management Department, Faculty of Business, Lebanese University, Tripoli Branch, Lebanon

2School of Business, Lebanese International University, Lebanon

3Finance Department, Faculty of Business, Lebanese University, Tripoli Branch, Lebanon

4MIS Department, Faculty of Business, University of Nicosia, Nicosia, Cyprus

Correspondence to: Khalil Ghazzawi , Management Department, Faculty of Business, Lebanese University, Tripoli Branch, Lebanon.

| Email: |  |

Copyright © 2016 Scientific & Academic Publishing. All Rights Reserved.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Abstract

CSR is a highly emerging topic around the world, and the debate about CSR raised many questions about the effectiveness of being socially responsible; however, it also motivated many companies around the world to implement CSR strategies. This study will show the evolution of CSR through different points of view over the time that discuss and describe CSR. Moreover, this study described the influence of CSR by discussing the major advantages and disadvantages of being socially responsible; which affect the internal and external environment of the company. However, the influence of CSR is not limited to the people that are related to the company while it social responsibility is highly correlated with the company’s core business, marketing strategy and financial performance. Finally, using SPSS, many variables were identified in order to determine the objective function of this research, and clarify if there is any relation between the effects of CSR and customer’s buying behavior. Consequently, this research resulted in identifying that CSR affects and influences the buying behavior of customers, whereas the results are based on the used frequencies, factor analysis, and regression analysis to the collected data from the distributed questionnaires. The main objective of this research is to highlight the different factors that might influence of corporate social responsibility and social activities on customers, and especially on their buying behavior.

Keywords:

Corporate Social Responsibility, Customer Satisfaction, Customer Behavior

Cite this paper: Khalil Ghazzawi , Sam El Nemar , Ali Sankari , Samer Tout , Hassan Dennaoui , Radwan el Shoghari , The Impact of CSR on Buying Behavior: Building Customer Relationships, Management, Vol. 6 No. 4, 2016, pp. 103-112. doi: 10.5923/j.mm.20160604.02.

1. Introduction

Corporate social responsibility is an emerging topic, especially after globalization which forced companies to deal with different countries, norms, and cultures. All these changes in the business environment directed companies towards CSR; while according to the 2008 KPMG International Survey of CSR, it was claimed that around 80% of the 250 biggest companies around the world issued CSR reports showing the increase of CSR information in the financial reports of these companies. Consequently, the concept of CSR is based on the activities that company chooses to perform and engage in voluntary. Moreover, CSR strategies should cover the social, economic, and environmental dimensions, while it should take into consideration the internal and external environment of the company. However, CSR strategies should find the right balance between shareholders and stakeholders in order to be effective; whereas it should never neglect the main purpose of the company of generating profits. As a result, CSR is considered as long term approach, while companies seek to satisfy the needs of their societies through social activities, especially that “88% of consumers said they were more likely to buy from a company that supports and engages in 2 activities to improve society, as it was reported by Better Business Journey, UK Small Business Consortium. Finally, the dilemma around CSR is not over, while as every arising topic many researchers are questioning its importance; while theories supporting CSR claim that it is very beneficial on all aspects for the company; whereas the other point of view consist of considering CSR as a losing investment and as a strategy that does not fall under business main purpose. As a result the concept of CSR will be discussed in this research. This research will address the concept of CSR through various patterns including its definition and its evolution, its advantages and disadvantages, its relation to the marketing strategy and the financial performance of the company, and how it affects the internal and external environment of the company. As a result this research will address the different points of view concerning CSR in order to identify its effects and determine whether they influence the customers or not, in order to evaluate social activities in consumers’ perceptions. Since CSR is considered to be one of the most important strategies in today’s multinational companies, this research will answer the questions of CSR influence on customers; to what degree consumer’s perception about a certain firm is influenced by social activities?, and how much this influence shape their buying behavior? Finally the objectives of this research will include identifying the buying behavior pattern caused by a certain socially responsible activity, and clarifying the reasons that create this pattern.

2. Literature Review

CSR is a strategy that affects so many aspects of a company’s business, it has been the center of attention of many researchers for a long time in order to define and illustrate its strategies. So in the next section CSR will be defined based on its evolution, structure, and the factors that form CSR.

2.1. Corporate Social Responsibility Evolution

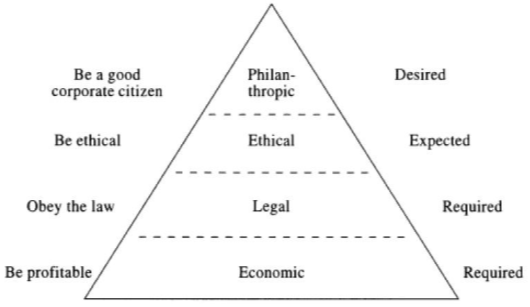

One of the most common ways to define CSR is to review the various definitions of CSR since the topic started to emerge. One of the most important and oldest books that defined CSR was Bowen’s book “Social Responsibilities of the Businessman”. In this book CSR was defined as the obligations that forces business men to take the decisions and execute the actions that are desirable and valued for the society. In addition, according to the same author and according to the survey issued in the Fortunes magazine which implied and proved that 93.5% of the surveyed business men agree that their range of responsibility is wider than their profit or loss, while they are responsible for the consequences of their decisions in front of the society (Bowen, 1953). Another important definition of CSR was issued in the 1960’s by Keith Davis, who stated that CSR is the decisions taken by business men that target what does not directly affect the direct interest of the company. Moreover, Davis argued that CSR is beneficial for the company, whereas the investment for engaging in CSR strategies is paying back for the companies in the long run through their profits. Moreover in the same decade another researcher; Joseph W McGuire altered the definition of CSR in his book “Business and Society”. McGuire’s definition consisted of 4 adding to the economic obligation of the company; another obligation which is the legal one. Besides setting the obligations, McGuire’s claimed that companies do have responsibilities towards the societies while he defined these obligations as the happiness of the employees, taking interest in politics, and the wellbeing of the community and education. Afterwards, in 1967 Clarence C. Walton gave CSR another perspective, while his opinion emphasized that social responsibility is considered as voluntarily work; whereas companies invest its resources and capabilities into social actions without being able to specify and measure their actual return. In addition, as most researchers he stated that there is a relationship between CSR and company’s benefits and revenues; however he considered this relation to be a negative one. The debate about CSR continued and new researchers kept trying to find the most accurate definition of CSR. In the 1970s, Harold Johnson in his article: “Business in Contemporary Society: Framework and issues”, highlighted the stakeholder’s approach claiming that the company is not only responsible for its well-being for generating profits and the satisfaction of its shareholders; whereas it should take into consideration its employees, customers, suppliers, and the whole society. Moreover, Johnson stated his opinion about the correlation between CSR and the economic benefits for the company; while he argued that this correlation is positive. (Johnson, 1971) As the debate continued, in 1971 a committee was formed from business people in order to define CSR. The “Committee for Economic development” which created the experienced point of view, defined CSR in three concentric circles which are: the inner, the intermediate, and the outer circle. • The Inner Circle: It includes the important actions that the company needs to perform in order to carry out its business and generate profits. • The Intermediate Circle: It takes into consideration the social responsibility approach for the firm while performing its activities or the activities of the inner circle. • The Outer Circle: It includes the factors that have an indirect influence on the company and its businesses. However, the company is expected to perform socially responsible activities for new emerging social dilemmas, in order to enhance its business environment if it has the required resources. (Davis, 1960)Although the definition of the committer was considered to be a new one, which is derived from the opinion of experienced businessmen, it wasn’t discussed thoroughly by the researchers. However, another opinion that rose after the committee’s definition is Manne’s, while he reevaluated CSR from the economic perspective and the relation between the financial situation of the company and engaging in CSR strategies. Manne’s opinion is similar in this aspect of CSR to Walton’s point of view while he considers the relation between CSR and the financial performance of the company to be a negative one. In addition, he indicated the most important factor is the shareholders needs and satisfaction, and after ensuring this goal, companies can use a three step approach that he stated to decide whether to engage in social responsibility activities or not. (Walton, 1967). The three steps included in the approach are: • Setting objectives. • Deciding whether to pursue objectives. • Financing objectives. In 1973, Davis updated his definition about CSR, while he stated that: “social responsibility begins where the law ends”, (Davis, 1973). In this definition Davis claimed that companies should not only abide laws, but they should go beyond what is enforced by laws in order to be considered as socially responsible. Whereas CSR was growing, another important approach was presented in 1975 by Sethi, who separated CSR into three categories which are: • Social obligation: It represents the activities of the company that are driven by legal factors or financial and economic goals. • Social Responsibility: It represents the activities that drive the company’s action beyond the law requirements. • Social Responsiveness: It represents the degree of correspondence between the company’s activities and the society’s needs. As the definitions and points of view about CSR varied, one of the most important researchers in the history of CSR, Archie B. Carroll, declared his opinion in 1979. Carroll described CSR as the expectation of the society from the corporations, while they include: economic, legal, ethical, and discretionary expectations that direct organizational activities. However, while many writers interested in CSR agreed with Carroll’s definition as he claimed, the 1980s started with a return towards the stakeholder’s approach by Jones; while he defined CSR as the obligations that go beyond law requirements, and the shareholders needs and satisfaction. However, this point of view limited the organizational responsibility towards the society, by considering that firms are only responsible for the society that it operates in and not for the whole society or nation. (Carroll, 1983) In addition, at early time of this decade Carroll’s updated his definition, to maintain the three first categories (economic, legal, and ethical), and change the fourth one which is discretionary into philanthropic. However, this update wasn’t widely accepted and used in that time, until Carroll’s updated his definition in the 1990s to include only the four new categories (Carroll, 1990).To illustrate his definition Carroll distributed the four categories into a pyramid. First of all, the base of the pyramid is represented by the economic responsibilities which will define and ensure company’s profitability. The second category is, the legal responsibilities, which can be achieved by obeying the law; while taking into consideration that laws define the right and wrong in the society. The next category in the pyramid is the ethical responsibilities, whereas being ethical means having an obligation to do what is right. Finally, at the top of the pyramid, the philanthropic responsibilities while he described it as being a good corporate citizen. Mainly the different views presented in 1990s didn’t give CSR a new perspective while researchers like Wood, Brown and Dacin, Marsden and Andriof and even institutions such as the World Bank, concentrated in their definitions on different presented aspects including: ethics, stakeholder’s needs, and the organizational assistance in the society. For instance, CSR was considered as the “configuration of principles of social responsibility, processes of social responsiveness, and policies, programs, and observable outcomes as they relate to the firm’s societal relationships” (Wood, 1991). Moreover, the World Bank defined CSR as the activities that match organizations with the rest of the society. At the start of the new decade, and with the various definitions of CSR over the years, CSR became a very important topic all around the world for researchers and companies. In 2003 a new definition of CSR came up that heavily disagreed with Carroll’s categories and the use of the pyramid, this new definition was called the three domain approach. Basically, Carroll and Schwartz, in 2003 identified three problems with Carroll’s pyramid approach which include: - Using the pyramid to describe the relation between categories: Carroll, in his model, used the pyramid to identify the four categories of CSR; however this pyramid failed to show the correlation and the overlapping nature between these categories. Generally, it is considered that the items at the top of the pyramid are considered the most important; whereas the items at the bottom are considered with the least priority. This wasn’t the case with Carroll’s pyramid while the philanthropic responsibilities that were on the top of the table didn’t have the high importance status that the reader will get; while Carroll described it as a desired responsibility; whereas he described the two bottom items which can be considered as the least important as the “required” responsibilities; as shown in figure 1 below.  | Figure 1. Pyramid of Corporate Social Responsibility, (Schwartz and Carroll, 2003) |

- Considering philanthropic responsibilities as a separate category: Many researchers disagreed with Carroll’s consideration of the philanthropic responsibilities as an independent category, especially that he described as a voluntary work which is not expected by the society. As a result it was suggested to consider the philanthropic responsibilities as a subcategory for the ethical responsibilities, as it is hard to differentiate between these two categories. Another reason is that the philanthropic responsibilities might only be the result of the economic interests of the company. - The Incomplete development of the economic, legal, and ethical domains: i. Economic Domain: The description that Carroll’s provided in his model failed to address and classify all the economic activities that the company might be engaged in.ii. Legal Domain: Carroll’s defined the legal responsibilities as the action that the company do in order to obey the law; without implying how the legal activities will enhance the corporate social work. iii. Ethical Domain: Carroll’s description of the ethical responsibilities didn’t provide a clear and broad view of these responsibilities; whereas he described the ethical activities as doing what is expected and accepted from the society even if it is not clarified by the law. As a result of the flaws in Carroll’s approach and new model was introduced to define CSR which is was called the “Three Domain Approach” in order to give a broad and a clear view about CSR and its categories.

2.2. The Correlation between CSR and Marketing

Corporate social responsibility and marketing are two related topics based on the simple fact that the two strategies deal with the society. First of all, CSR strategies serve as corrective strategies in order to restore the wellbeing of the society. This is said after acknowledging that firms’ actions do have a negative influence on the society, and without ignoring the fact that firms operate in the societies that form a crucial factor its growth, sustainability, and existence. On the other hand, choosing marketing strategies heavily rely on the societies while they form the environment the companies operate in. These strategies are driven by the societies through many factors including: target market, product line, needs of the customers and many other aspects. In order to understand the relation between these two domains we need have a clear view about their concepts. To begin with, marketing is defined as” the set of processes for creating, communicating, and delivering value for customers and for managing customer relationships in ways that benefit the organization and its stakeholders.” (American Marketing Association, 2004) Consequently, marketing is considered as a type of mutual relation between the organizations and the society; whereas companies try as much as possible to meet and satisfy the needs of customers through designing their product offerings according to their tastes; while they expect a specified number of estimated profits from these customers. On the other and as discussed earlier, CSR is the “management of stakeholder concern for responsible and irresponsible acts related to environmental, ethical and social phenomena in a way that creates corporate benefit.” (Vaaland, Heide, Gronhaug, 2008).

2.3. Factors Affecting the Choice of being Socially Responsible

CSR is considered as one of the most important strategies that companies engage in to compensate of the harm that might be caused by its operations to the society, or to enhance its brand image. However, there are many factors that might affect the choice of the firm to engage in socially responsible activities in order to maximize the benefits of the corporate social responsibilities’ advantages. As explained earlier in this research, there are four main domains that construct social activities which were described as the responsibilities including: the ethical, the economic, the legal, and the philanthropic responsibilities. These categories define several types of actions that the companies could take in order to be socially responsible, whereas the company should take into consideration and balance between the activities they are engaging in, and the strategic objectives of the company. Consequently, while choosing its social strategy companies consider a variety of activities that can be classified according to its relation to: a. Community: The community section provides a wide range of activities that the company could engage in to enhance the wellbeing of the society. In this type of activities organization can help, for instance, in the healthcare sector, educational sector…etc. b. Employees and Labor: In this section firms can cooperate in actions to ensure and enhance the safety and the rights of labors. For example, the firms can help through fighting child labor, improving union relations, decreasing recruitment discrimination, and many other activities. (Skudiene, 2012) c. Environment: Recently, environmental protection has become one of the main concerns for the different components of societies all around the world. Firms can provide its assistance by going beyond the laws and regulations, for instance by using renewable energy, producing environmental friendly products, encouraging recycling and many other activities. d. Ethics: The firms can undertake social practices by emphasizing and encouraging good business standards and fighting corruption. e. Partnerships: Firms can participate in social activities through partnerships with different social organization and nonprofit organizations that that aim to help the society on many social levels. (Jones & al., 2009)Moreover, while being socially responsible companies can participate by donating money, products, time, and many other resources; however they should find the right combination that meets customers’ expectations and their own benefits. In addition, companies can contribute to the wellbeing of the society through their advertising campaigns that can be used to enlighten the audience to the difficulties that are facing the world and the society (McDonald, Rundle-Thiele, 2008).Nevertheless, the motivations that drive companies to undertake actions that can be classified as a part of the four CSR responsibilities differ. In addition to the motive, firms might face several difficulties when choosing the right CSR strategy. First of all, selecting the CSR strategy heavily relies on the perceived goal from this strategy by the managers, whereas these objectives may vary from the listed advantages of CSR strategies discussed earlier. For instance, managers might have an economic goal by creating a new business opportunity or improving the brand image and company’s reputation, while others might seek an ethical goal of decreasing costs and increasing efficiencies. Another important factor that alters CSR strategies is the involved department, while the level of personnel involved in executing and applying the CSR strategy. For example, top management will be liable for the social activities that are related to the community perspective and fall under the philanthropic responsibilities. Consequently, firms need to determine its objectives and the people that are mainly involved in executing CSR strategies during the assessment; however these are not the only requirements. (Holme, 2010) From the other point of view, companies need to determine the real value of being socially responsible; whereas they have to evaluate the expenditures and the resources needed for such activities, after categorizing each activity the company will be engaged in. Another important task that should be done is to edit the activity and the execution process, in order to determine how this activity will benefit the whole organizational structure. In addition, the companies have to quantify the benefits of undertaking such actions, and its impacts internally and externally. However, an important point in this assessment is to really take into considerations all the effects of these activities, evaluate the potential negative influence that it might have, in order to get an accurate estimates of the costs of such actions. As a result, while crafting its CSR strategy companies should seek the right combination that maximizes its benefits from social activities by matching these activities, its benefits, and the main strategic objective of the firm. For instance Tata Steel Tried to engage in CSR long time ago, however not finding the right balance had a negative influence on the company’s core business. This situation forced the company to start cutting its workforce and redesign its CSR strategy in order to refocus on its core business even though that the company gained good reputation through its social responsibility projects. Never the less, CSR is important to almost every company but the most crucial thing in implementing CSR is finding the right balance, especially that the impact of CSR strategies will vary between businesses. There are 2 approaches of CSR: internal and external. The outward-looking approach focuses and the stakeholder’s expectations. On the other hand, the inward-looking approach focuses on internal issues. As a result, in order to succeed in implementing CSR the strategy should focus on both approaches with a priority for the business. (Cinpoieru & Munteanu, 2014)Finally, engaging in social responsibility will enhance the company’s image and reputation, while giving the company a glance about the market. However, to “ignore social issues is to miss strategic opportunities”, (Strategic direction, 2007). Nevertheless, the firm could benefit on many aspects from engaging in such actions, such as creating new opportunities, gaining competitive and sustainable advantage, enhancing it brand image, attracting investors, increasing customers’ loyalty, different types of loyalty, and many other advantages that were discussed earlier in this research. To sum up, CSR is a broad topic that influences the company and its internal and external environments. Therefore, firms should synchronize these actions with its corporate functions, while emphasizing the commitment of all personnel in the company, and the support of top management. However, CSR strategies should be clear and specifically illustrated in order to guide employees in the right direction, and to increase the efficient allocation of resources, especially that CSR might need a lot of investments due to its high connection with the different kinds of corporate actions and strategies. Finally, CSR will influence the company the environment of the company especially the employees and customers. So, how CSR affect company’s stakeholders and environment?

2.4. The Impact of CSR on the Financial Performance

Making the decision to invest in social responsibility is not an easy one, especially that this decision will have wide range of impacts on many business dimensions that will alter company’s performance. CSI requires a considerable amount of resources including money, time, and staff; however, it is expected that this investment will ensure the satisfying payback for the company, with its different benefits, advantages, and impacts that were discussed earlier. Nevertheless, social and intangible effects may be important for the company, but this will not undervalue or ignore the main reason for company’s which can be translated and measured through profits. The relation between CSR and CFP is based on the idea of the positive connection between the impacts of CSR such as consumer’s perception, brand image, and customer satisfaction that will result in an enhanced performance, improved quality products, therefore increased sales and profits. The intensity this relation will vary according to many factors such as the industry, the current market situation, and the efficiency of finding the right balance between the market’s needs, the expectation of customers, and the company’s core business and competencies. On the other hand, there is another point of view when measuring CFP and CSR; while some researchers believe that the amount of social activity that the company engages in is based on the profits this firm makes; which will form a cycle of increasing social activity after increasing profits. However, this point of view did not ignore the fact that CSR benefits are the reason for generating profits. Moreover, measuring CSR impacts may be a hard task since a lot of these effects are based on the change of the perceptions and opinions. However, researchers developed three techniques to measure these impacts. The first one is based on the numbers and auditing numbers; while the other one consists of measuring the modifications in the marketing implications such as sales. Finally, the third technique consists of the combination of the first two. To conclude, even though many researchers didn’t agree on the positive relation between CSR and the financial performance, the majority of CSR experts supported this theory, while emphasizing the importance of CSR benefits on consumer’s behavior and thus financial performance. Accordingly, both concepts are based on the society, but how do they interact? First of all, after analyzing the two topics, we can find similar concepts that highlight the overlapping nature of these two topics such as cause related marketing, and environmental marketing. Moreover, marketing strategies nowadays are starting to consider a wider point of view to take into consideration the stakeholders and not only focus on the customers; which can be considered as one of the main goal of CSR. Another factor that shows the overlapping nature of these two topics away from the theoretical part is the execution. One of the key factors to show this relation is the fit and motivational aspects. Fit is considered as the link between the cause of being socially responsible and the product line of the company. Moreover, fit is considered as a key factor in social marketing since it influences the ideas and perceptions of customers towards organizations, especially if the social initiative is taken according to the company’s core competencies and the society’s expectation. However, fit factor is not enough, whereas the expected change in consumers’ perception is highly relevant to the motivation that they believe it directed the firm towards taking a social initiative. For instance if customers, evaluated that the firm motivation is purely related to its financial benefit the customer’s perception is most likely to be negatively affected, and vice versa. As a result, companies should strive to engage in high fit, proactive actions; while taking into consideration the society’s expectation and the timing of these actions. In addition, we can consider that marketing is controlled by the society, whereas companies need CSR to enhance its brand image in the society. However, marketing play an important role in highlighting the social initiative and the motivation of the company through choosing the right product line, target market, advertising. (Mattila, 2009) Moreover, studies showed that CSR strategies indeed affect consumers but companies are required to increase communication and advertising about the strategies. Consequently companies should follow a more explicit approach that is more compatible with its core business, instead of having a society based approach. This way the company will be able to find the great balance that will enhance the returns of the CSR strategy. To conclude, we can consider that marketing and social responsibility are two correlated topics that highly influence the process of creating a well perceived brand image, while CSR should serve as a reflection of the marketing context of the company. (Rangan & al., 2012)

3. Methodology

3.1. Sample Selection

In this research a survey will be conducted to gather needed information in order to illustrate the importance of the influence of CSR. Using the random sampling technique our survey will target a sample of one hundred and fifty applicants that are familiar with the concept of CSR. The survey was distributed in different region in Lebanon (Tripoli, Beirut and Mont-Lebanon). The data were collected during a period of 6 months between January and June 2016.

3.2. Research Model and Variables

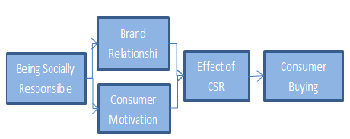

The purpose of this research is to measure the influence of CSR through different variables that were grouped, into three dimensional factors, as follows: Brand Relationships The first factor is the brand relationships in which the following variables were tested: a. Improved brand Image. b. Creating a feeling of loyalty c. Offering better quality Effects of CSR The second factor measures the effects of CSR on the buying behavior through the following variables: a. Buying Decision b. Willingness to pay premium prices c. Increasing purchases Motivations The third factor measures the motivations to buy the products of a socially responsible firm through the following variables: a. Preferring to buy the products of a socially responsible firm. b. Supporting the cause the firm is supporting. c. Supporting the ethical behavior of the company d. Increasing awareness of the cause they are supporting

Brand Relationships The first factor is the brand relationships in which the following variables were tested: a. Improved brand Image. b. Creating a feeling of loyalty c. Offering better quality Effects of CSR The second factor measures the effects of CSR on the buying behavior through the following variables: a. Buying Decision b. Willingness to pay premium prices c. Increasing purchases Motivations The third factor measures the motivations to buy the products of a socially responsible firm through the following variables: a. Preferring to buy the products of a socially responsible firm. b. Supporting the cause the firm is supporting. c. Supporting the ethical behavior of the company d. Increasing awareness of the cause they are supporting

4. Analysis

4.1. Factor Analysis

The second step in analyzing the data is through performing a factor analysis, using SPSS, through dimension reduction; from which the factors of the regression will be identified.As a result the factor analysis was performed while forcing the result of producing three dimensional factors.The results of the test are shown below:Table 1.

|

| |

|

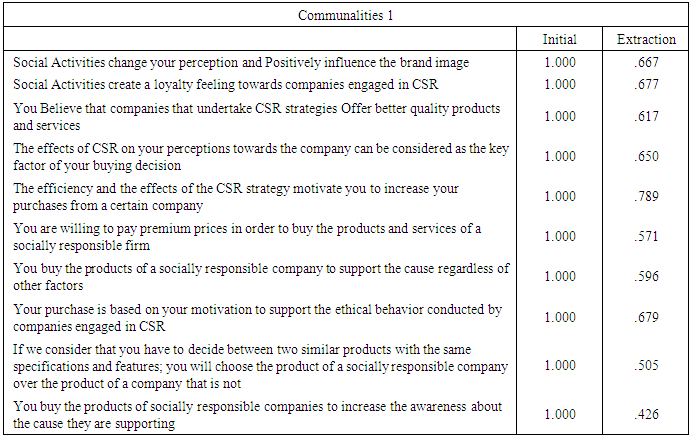

The Table below shows that all the variables have an acceptable extraction values except for the last one (You buy the products of socially responsible companies to increase the awareness about the cause they are supporting) which is lower than 0.5. Another important factor to check after running this test was the total variance explained table.Consequently, another factor analysis has been performed while excluding the insignificant variable and forcing the result of the analysis to three variables only. The results of the third factor analysis showed an improvement which is illustrated in the tables below: First it is important to check the communalities table 2 that is presented belowTable 2.

|

| |

|

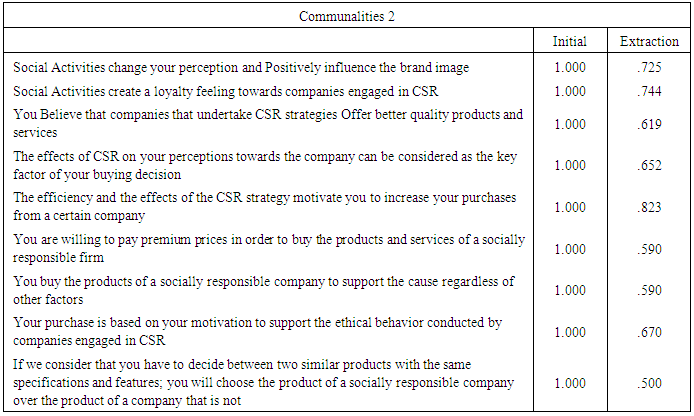

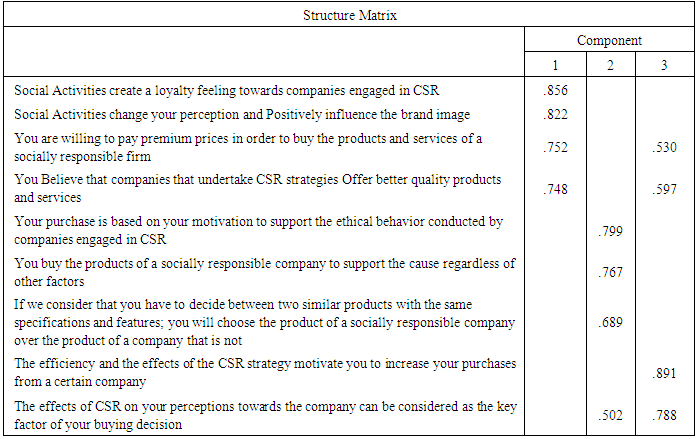

First of all, this communalities table shows an improvement in results whereas it is unlike the results shown in table 1 while in this table all the variables show significant values. Another improvement is shown in the table of the total variance explained below:The result of the cumulative in the second test of factor analysis was 61%; however it is clearly shown that it has enhanced result with 65.700%. Finally, we check structure matrix to determine the correspondence of the variables to the factors.Table 3.

|

| |

|

The above Table shows that the presented nine variables are grouped into three main factors; whereas these results completely correspond to the previously presented model in the methodology section. To sum up these factors are grouped as follows: 1. Brand relationship with the following variables: - Social Activities create a loyalty feeling towards companies engaged in CSR - Social Activities change your perception and Positively influence the brand image - You Believe that companies that undertake CSR strategies Offer better quality products and services 2. Motivations for purchase including the following variables: - Your purchase is based on your motivation to support the ethical behavior - You buy the products of a socially responsible company to support the cause regardless of other factors - If we consider that you have to decide between two similar products with the same specifications and features; you will choose the product of a socially responsible company over the product of a company that is not 3. Buying behavior including the following variables: - The effects of CSR on your perceptions towards the company can be considered as the key factor of your buying decision - The efficiency and the effects of the CSR strategy motivate you to increase your purchases from a certain company - You are willing to pay premium prices in order to buy the products and services of a socially responsible firm.After eliminating the insignificant factors and defining the three dimensions and their variables that resulted from the dimension reduction process, the next step in analysis will be running a regression analysis; which will clarify the relation between the selected dimensions.

4.2. Regression Analysis

In order to complete the analysis of this study, two regression analysis will be performed. The first regression analysis will include factors 1 and 3, while the second regression analysis will include factors 2 and 3. The first regression analysis will be conducted between the first factor (Brand relationship) and the third factor (buying behavior); while considering factor 3 as the dependent variable and factor 1 as the independent. The results of this regression are shown below:Table 4. Model Summary 1

|

| |

|

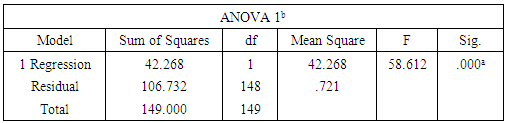

It is shown in table 6 that R is equal to 0.533 (53.3%). This value shows the correlation between the included factors and their variables, indicating in this case a good level of correlation. Another important result is the “R square” showing the level of determination between the two variables, indicating the degree to which the dependent variable (buying, Factor 3) can be determined and explained by the independent variable (Brand Relationship, Factor 1). In this case R square is equal to 0.284 (28.4%). After identifying the correlation between the variables it is important to check the significance of the analysis by checking the Anova table which is presented below:Table 5. Anova 1

|

| |

|

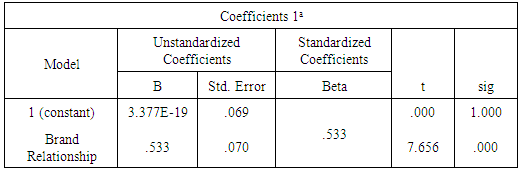

Table 7 shows that the outcome variable is significantly predicted by the regression model. In addition, it is shown that the model is highly significant since the significance value in the regression row and the last column of the table (Sig.) is 0.000, which is less than 0.05. Another important result is F, which is equal to 58.612 indicating the strength of the relation between variables. Finally it is important to check the coefficients table in order to write the regression equation, which is presented below:Table 6. Coefficients 1

|

| |

|

The information provided in table 6, allow us to create the regression equation which will help calculating the change in the “buying behavior” while changing the value of “brand relationship” As a result the regression formula is: Y=b0+b1x1 àY (Buying Behavior) = 3.377^-19+0.533 (Brand Relationship) The second regression analysis will be conducted between the second factor (Motivation) and the third factor (buying behavior); while considering factor 3 as the dependent variable and factor 2 as the independent. The results of this regression are shown below:Table 7. Model Summary 2

|

| |

|

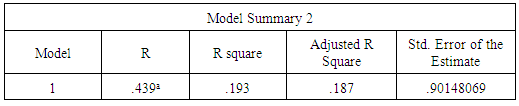

It is shown in the table that R is equal to 0.439 (43.9%). This value shows the correlation between the included factors and their variables, indicating in this case a good level of correlation. Another important result is the “R square” showing the level of determination between the two variables, indicating the degree to which the dependent variable (buying, Factor 3) can be determined and explained by the independent variable (Motivation, Factor 1). In this case R square is equal to 0.193 (19.3%). After identifying the correlation between the variables it is important to check the significance of the analysis by checking the Anova table which is presented below:Table 8. Anova 2

|

| |

|

The above Table shows that the outcome variable is significantly predicted by the regression model. In addition, it is shown that the model is highly significant since the significance value in the regression row and the last column of the table (Sig.) is 0.000, which is less than 0.05. Another important result is F, which is equal to 35.347 indicating the strength of the relation between variables. Finally it is important to check the coefficients table in order to write the regression equation, which is presented below:Table 9. Coefficients 2

|

| |

|

The information provided in table above, allow us to create the regression equation which will help calculating the change in the “buying behavior” while changing the value of “Motivation”.As a result the regression formula is: Y=b0+b1x1 à Y (Buying Behavior) = 3.203^-18+0.439 (Motivation)

5. Discussion

Many conclusions can be drawn from the results of this study. First of all, the results of the surveys validated the idea of the influences of CSR on loyalty, perception, and the belief in offering higher quality on the Lebanese Customer. These factors create the relationship from customers towards the brand; which as shown in the analysis of the results it is related and influences customer’s buying behavior. On the other hand, the results also showed the correlation between factors that motivate Lebanese customers to buy the products of a socially responsible company and their buying behavior. However, the results showed that brand relationship has more on influence on buying behavior than motivating factors. According to this study it is certain that CSR will affect several aspects of consumer’s judgment and feelings towards socially responsible companies, and as result these effects will lead to alter their buying behavior through their buying decisions, willingness to pay premium prices, and increasing purchase. Therefore, Lebanese companies in whatever industry they are working should be responsible toward their society and use this concept to alter the consumer behavior toward their brands and products.

6. Conclusions

The purpose of this study was to identify if there is a relationship between implementing CSR strategies and buying behavior. This study was based on several factors and variables in order to identify if the effects of CSR strategies will lead to a change in the buying behavior. Moreover, the study was based on the results of 150 questionnaires, in order to perform two regression analysis studying the factors of brand relationship towards a socially responsible firm and his buying behavior; whereas, on the other hand the second regression analysis studied the factors that motivates customers and its influence on buying behavior.

References

| [1] | Busaya Virakul, Kalayanee Koonmee, Gary N. McLean, (2009), "CSR activities in award-winning Thai companies", Social Responsibility Journal, Vol. 5 Iss: 2 pp. 178 - 199. |

| [2] | Anna Blombäck, Caroline Wigren, (2009), "Challenging the importance of size as determinant for CSR activities", Management of Environmental Quality: An International Journal, Vol. 20 Iss: 3 pp. 255 - 270. |

| [3] | Gregory Birth, Laura Illia, Francesco Lurati, Alessandra Zamparini, (2008), "Communicating CSR: practices among Switzerland's top 300 companies", Corporate Communications: An International Journal, Vol. 13 Iss: 2 pp. 182 - 196. |

| [4] | Jorge A. Arevalo, Deepa Aravind, (2011), "Corporate social responsibility practices in India: approach, drivers, and barriers", Corporate Governance, Vol. 11 Iss: 4 pp. 399 - 414. |

| [5] | Vida Skudiene, Vilte Auruskeviciene, (2012), "The contribution of corporate social responsibility to internal employee motivation", Baltic Journal of Management, Vol. 7 Iss: 1 pp. 49 - 67. |

| [6] | Charles Holme, (2010), "Corporate social responsibility: a strategic issue or a wasteful distraction?", Industrial and Commercial Training, Vol. 42 Iss: 4 pp. 179 - 185. |

| [7] | Brian Jones, Ryan Bowd, Ralph Tench, (2009), "Corporate irresponsibility and corporate social responsibility: competing realities", Social Responsibility Journal, Vol. 5 Iss: 3 pp. 300 – 310. |

| [8] | Giles Heimann, (2008), ‘Corporate Social Responsibility Global Standards & Policies In Practice’, The Liberian International ship And Corporate Registry. |

| [9] | Mark Schwartz and Archie Carroll, Corporate Social Responsibility: A three Domain Approach, Business Ethics Quarterly, volume 13, issue 4, pp. 503-530. |

| [10] | Som Sekhar Bhattacharyya, (2010), "Exploring the concept of strategic corporate social responsibility for an integrated perspective", European Business Review, Vol. 22 Iss: 1 pp. 82 – 101. |

| [11] | Sophie Van Eupen, Phd Student, A Sensemaking Approach Of Corporate Social Responsibility, Research Proposal Katholieke Universiteit Leuven. |

| [12] | Yongqiang Gao, (2009), "Corporate social responsibility and consumers' response: the missing linkage", Baltic Journal of Management, Vol. 4 Iss: 3 pp. 269 – 287. |

| [13] | Shareholder value or social responsibility?: What should motivate today's CEO?", (2007), Strategic Direction, Vol. 23 Iss: 8 pp. 15 – 18. |

| [14] | Lynette M. McDonald, Sharyn Rundle-Thiele, (2008), "Corporate social responsibility and bank customer satisfaction: A research agenda", International Journal of Bank Marketing, Vol. 26 Iss: 3 pp. 170 - 182. |

| [15] | Merita Mattila, (2009), "Corporate social responsibility and image in organizations: for the insiders or the outsiders?", Social Responsibility Journal, Vol. 5 Iss: 4 pp. 540 - 549. |

| [16] | Kash Rangan, Lisa A. Chase, Sohel Karim, (2012), Why Every Company Needs a CSR Strategy and How to Build It, Working Paper Harvard Business School. |

| [17] | Diana Corina Gligor Cimpoiru, Valentin Partenie Munteanu, (2014), ‘External CSR Communication in a Strategic Approach’, Economia. Seria Management Volume 17, Issue 2. |

| [18] | Harold Johnson, (1971), ‘Business in contemporary society: Framework and issues’, Wadsworth, Belmont, California. |

| [19] | Walton Clarence, (1967), ‘Corporate social responsibilities’, Wadsworth, Belmont, California. |

| [20] | Bowen Howard Rothmann, (1953), Social responsibilities of the businessman, New York: Harper & Row. |

| [21] | Davis Kenis, (1960), ‘Can business afford to ignore social responsibilities?’, Spring, California. |

| [22] | Carroll Archie, (1983), ‘corporate social responsibility: Will industry respond to cutbacks in social program funding? Vital Speeches of the Day’, vol. 49, pp. 604-608. |

| [23] | Carroll Archie, (1990), ‘Principles of Business Ethics: Their Role in Decision Making and an Initial Consensus’, Management Decision, Vol. 28 Issue: 8. |

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTML