-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

Microeconomics and Macroeconomics

p-ISSN: 2168-457X e-ISSN: 2168-4588

2018; 6(2): 33-43

doi:10.5923/j.m2economics.20180602.01

Effect of Morocco’s Basic Medical Coverage on Individual’s Healthcare Expenditures: A Censored Tobit Model

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLJouilil Youness, Lechheb Houda

Department of Economics, Faculty of Law, Economic and Social Sciences, Ibn Tofail University of Kenitra, Morocco

Correspondence to: Jouilil Youness, Department of Economics, Faculty of Law, Economic and Social Sciences, Ibn Tofail University of Kenitra, Morocco.

| Email: |  |

Copyright © 2018 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

The main purpose of this paper is to examine the effect of Basic Medical Coverage (BMC) on the expenditures of Healthcare in Morocco based upon data from the Moroccan Household Panel Survey Data. The Censored Tobit Model (CTM) has been used to estimate the BMC effect on the expenditures of healthcare. For this purpose, we have used a cross-sectional data which came from the Moroccan Household Survey Panel Data (HSPD) particularly from the 3rd wave (2015). Our research revealed that the access to healthcare expenses remain correlated upon the individual’s demographic, social and economic conditions. In fact, our statistical modelling revealed that BMC is significantly correlated with increased of use of healthcare services when they are needed. Indeed, a person in households that had Compulsory Health Insurance (AMO) coverage used health services exactly like those in households that had no insurance coverage. Generally, the findings of the adopted model suggested that RAMed health plan could significantly increase the individual expenditures of healthcare.

Keywords: Morocco’s Basic Medical Coverage, Healthcare expenditures, Censored Tobit Model

Cite this paper: Jouilil Youness, Lechheb Houda, Effect of Morocco’s Basic Medical Coverage on Individual’s Healthcare Expenditures: A Censored Tobit Model, Microeconomics and Macroeconomics, Vol. 6 No. 2, 2018, pp. 33-43. doi: 10.5923/j.m2economics.20180602.01.

Article Outline

1. Introduction

- The Basic Medical Coverage is a device responsible for ensuring individuals face of financial risks in case of illness. In this regard, two schemes have been put in place namely the Compulsory Health Insurance (AMO, Assurance Maladie Obligatoire) and the Medical Assistance Scheme (RAMed, Régime d’Assistance Médicale) (Official Bulletin, Law N° 65-00, 2002). The main goal is to improve accessibility and quality of healthcare especially for low-income population.As a result, what is the real effect of these two schemes on the consumption for healthcare? Is BMC the unique factor that determines access to healthcare?The remainder of this work is organized as follows: the first section is a theoretical framework in which we present the literature review and an overview of the Moroccan Health System. The second presents the econometric framework in which we show that the classical methods of regression are not adapted and we present afterwards an alternative methods namely the Censored Tobit Model. The third estimates the adopted model and discusses the results. In the last one, we conclude.

2. Theoretical Framework

- We proceed as follows. In paragraph 1, we present the literature review and in the second one, we provide an overview of the Moroccan Health System.

2.1. Literature Review

- The main objective of health insurance is to improve access to healthcare and reduce individual expenses, especially for people with limited incomes. The risk pooling of the health insurance mechanism could then reduce healthcare costs and consequently increase the demand of healthcare services. In order to expose the main role of health insurance several theories have been used. Indeed, using a two-part model approach Ekman, B (2007) have proved that medical insurance can improve access to healthcare and reduce out-of-pocket spending. The research works have emphasized the importance of individual and behavioural characteristics in determining the individual’s health status. These models are distinguished according to the importance they attach to each factor (Berkman, 2000). In fact, the behaviour of the individual is perceived as a dual decision process of the demand for healthcare. The first decision is the opportunity to see a healthcare provider and the second is how much care to get.Furthermore, Van Dourslaer (2002) showed that, at the individual level, there is a positive relationship between health status and productivity.Moreover, Arrow, K (1963) revealed that partial or total care allows policyholders access to a large number of health treatments, especially the most expensive ones. Indeed, the abuse of healthcare can be explained not because policyholders are more exposed to the disease but rather because when they were sick it makes more use of morbid care and acts of prevention. This phenomenon is known among specialists in health micro-economy by moral hazard which leads to overconsumption of healthcare and subsequently a loss of social well-being. In other words, a positive correlation should exist between the amount of health expenditures and the level of coverage. In fact, risk coverage implies a reduction in prices in the event of illness, which can encourage insured to consume more care. The purpose of this paper is therefore to test and validate the moral hazard hypothesis, which states that the best insured are those who consume more healthcare.The implementation of an insurance system encourages policyholders to consume more. Moreover, he showed that having a high level of reimbursement can push people to consume more healthcare (Pauly, 1968). To limit over-consumption behaviours Shavell (1979) called for an incomplete coverage. That is, a part of the care load must be borne by the insured in order to moderate their health expenses.Claussat and Glaude (1993), using a simultaneous equations model, concluded that medical coverage has a positive impact on the probability of healthcare utilization. Moreover, they showed that complementary insurance is positively correlated with the demand for care.In addition to the influences of the health coverage, socio-economic and socio-demographic factors also play a determinant role. In fact, Grossman indicated that the age is a major factor in determining the demand for health, since the state of health deteriorates with advancement in the age, individuals consume more care at the elder age. Also, he showed that men consume more care than women. Healthcare spending is higher for the older people than for the younger one (Anderson, 2000). Marital status and number of children are also key determinants of access to healthcare.Also, and according to Grossman model, an increase in the level of education increases the marginal products of medical care. The other important consequence is the effect of income on individual consumption of care. Many empirical studies suggest that when people become richer, they will demand more and better care and more expensive care. Tanti-Hardouin (1994) revealed that the health demand is correlated with income (individual’s income and state income).Additionally, Dong and al. (2002) have shown from an empirical study that household income, the gender of individual and level of study impact significantly health expenses.

2.2. An Overview of the Health System in Morocco

- Moroccan BMC has dual role. Firstly, it provides membership to the insured’s health program and secondly, it reduces the out-of-pocket healthcare costs.

2.2.1. Level of Health Expenditure

- According to the Moroccan Ministry of Health, the national expenditures on health has increased from 30.5 millions MAD on 2010 to 52 millions of MAD on 2013, which represents an increase of 70.49%. In terms of general budget of the state, Morocco devotes around 1.3% of his GDP in health. The single most expensive parts of healthcare are pharmaceuticals, ambulatory and hospital care. (MMS, 2016)For its part, the average annual expenditures on health per capita amounted to about 1,578 MAD in 2013 against 1,000 MAD in 2006, an annual increase of 57.80%. (MMS, 2016)

2.2.2. Characteristics of the Basic Healthcare Offer

- The Moroccan health offer can be divided into two parts:- Public offer: The public sector is the first care provider and the most dominant in the country because it covers almost the entire national territory and constitutes the operational base of all health actions. Nevertheless, it suffers from a lack of coordination and communication with the hospitals, an absence of a health map, an inadequacy of its human, material and financial resources as well as an inefficient and a centralized management.- Private offer: The private medical sector is concentrated mainly in the axis of Casablanca-Rabat. According to the report of the Economic, Social and Environmental Council (ESEC) on 2013 the private sector includes more than half of doctors, 90% of pharmacists and dentists and nearly 10% of paramedics. It is a network in constant and continuous progression.Health infrastructure has grown significantly with just over 2,600 primary healthcare facilities, 144 public hospitals with approximately 22,000 beds and 373 private clinics. (WHO, 2016)Also, the Moroccan health system is distinguished by a deficit in terms of health personnel. In fact, there are 6.2 physicians (all profiles and specialities combined) and 9.7 nurses per 10,000 inhabitants. Also, their distribution throughout the country is unfair. They focus primarily on the two regions of Rabat-Sal´e-Kenitra and Casablanca-Settat.

2.2.3. Coverage of the Moroccan Population

- According to National Agency of Health Insurance (Agence Nationale de l’Assurance Maladie) official publications of 2016, the number of RAMed beneficiaries has significantly increased in recent years to reach almost 10.5 persons, of which almost 88% are vulnerable.Regarding to Compulsory Health Insurance (CHI), the number of beneficiaries is 8.7 millions, of which 65.51% are from the private sector. (NHIA, 2015)In total, the number of people covered by the Basic Medical Coverage (BMC) hardly exceeds 19 millions beneficiaries or almost 56% of the Moroccan population.

2.2.4. Overview of the Health Situation

- According to the Moroccan Ministry of Health, thanks to the efforts undertaken during the last decade, it has been able to eliminate a number of diseases such as malaria, schistosomiasis, leprosy and trachoma. However, the health situation is still characterized by the persistence of communicable diseases such as Human Immunodeficiency Virus (HIV), hepatitis and chronic diseases, in particular cardiovascular diseases, diabetes, cancers and chronic respiratory diseases. In fact, four in ten deaths are due to cardiovascular disease, 28.8 cases of death for every 1,000 births among children under 5 years, two millions Moroccans aged more than 20 years are diabetics,...Etc.

3. Econometric Framework

- This section will try to modelize the effect of health insurance on individual’s healthcare expenditures. For this purpose, we will prove that the classical approach of solving linear equation by OLS method will fail. To overtake this limitation, we will propose an alternative solution namely Censored Tobit Model (CTM).

3.1. Methodology

- Let

be an unobservable underlying process (latent variable), such that:

be an unobservable underlying process (latent variable), such that: | (1) |

a vector of unknown parameters to be estimated;-

a vector of unknown parameters to be estimated;-  random error for each i in 1, 2,.., N;-

random error for each i in 1, 2,.., N;-  (normally distributed) with σ the standard deviation of the normal distribution;-

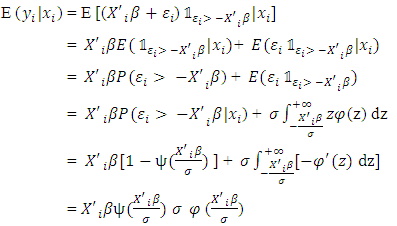

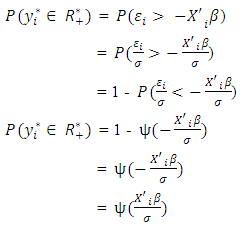

(normally distributed) with σ the standard deviation of the normal distribution;-  Also, let yi denote observed expenditures which is equal to yı if individual i has a health expenditures insurance, and is equal to zero otherwise. Mathematically, our model can be defined by the following function:

Also, let yi denote observed expenditures which is equal to yı if individual i has a health expenditures insurance, and is equal to zero otherwise. Mathematically, our model can be defined by the following function: | (2) |

| (3) |

| (4) |

| (5) |

3.2. Why the Ordinary Least Squares (OLS) Procedures Fail?

- The first idea that comes to mind is to use the ordinary regression to estimate the parameters. Thus, defining:

| (6) |

| (7) |

| (8) |

| (9) |

| (10) |

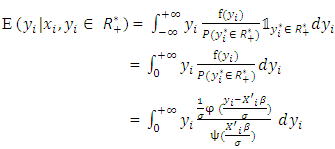

are the standard normal probability density and standard normal cumulative density functions, respectively.Thus, according to equation (9), the estimator is biased. Nevertheless, we can doubt that the bias comes from the censored observations. That why we are going try to apply OLS only for strictly positive observations.However and in the second case (for the strictly positive observations), the density function and the conditional expected value2 are equal to:

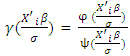

are the standard normal probability density and standard normal cumulative density functions, respectively.Thus, according to equation (9), the estimator is biased. Nevertheless, we can doubt that the bias comes from the censored observations. That why we are going try to apply OLS only for strictly positive observations.However and in the second case (for the strictly positive observations), the density function and the conditional expected value2 are equal to: | (11) |

| (12) |

| (13) |

| (14) |

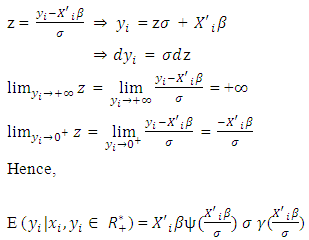

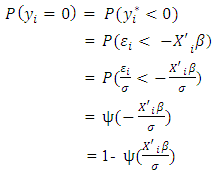

is called the inverse of Mills’ ratio. Thus, according to equation (12), even for only strict positive observations, the OLS estimator stills is biased.Hence, we conclude that, in both cases, applying the OLS method leads to increase the probability of sample selection bias. As a conclusion, the OLS method is not appropriate to estimate the model with censored observations because it gives a biased and inconsistent estimator of parameters β.

is called the inverse of Mills’ ratio. Thus, according to equation (12), even for only strict positive observations, the OLS estimator stills is biased.Hence, we conclude that, in both cases, applying the OLS method leads to increase the probability of sample selection bias. As a conclusion, the OLS method is not appropriate to estimate the model with censored observations because it gives a biased and inconsistent estimator of parameters β.3.3. Censored Tobit Model (CTM)

- In this section, we try to model the eventual relationship between BMC and health expenditures at the individual level.

3.3.1. Presentation

- Because of a large number of zero observations (censored observations), we use Censored Tobit Model (CTM). That means, the Tobit model is appropriate when the endogenous y is limited in some way.Proposed by James Tobin (1958), the Tobit model is commonly used to describe and measure the relationship between a censored (latent) and nonnegative dependent variable with a vector of explanatory variables (quantitative and qualitative). James Tobin proposed it in 1958 hence its name Tobit. (Wooldridge, 2010)

3.3.2. Estimation with ML Methods

- The estimation of a Tobit model can be done by several methods among others the method of Heckman or by the maximum of likelihood. In this article, we will opt for the last one since the obtained estimators are unbiased and asymptotically convergent.The density function3 of yi given xi is:

| (15) |

| (16) |

for the censored normal distribution is:

for the censored normal distribution is: | (17) |

| (18) |

4. Analytic Framework

- This section will present the full specification of the model in which the medical insurance equation will be explained linearly by several variables including health insurance. The objective is to estimate how the effect of insurance on the expended healthcare expenditures. In order to model the conditional expenditures, we use the CTM.In this paragraph, we’ll present the used material, some descriptive statistics of the database, econometric modelling and interpretations of the main results.

4.1. Materials and Methods

4.1.1. Data

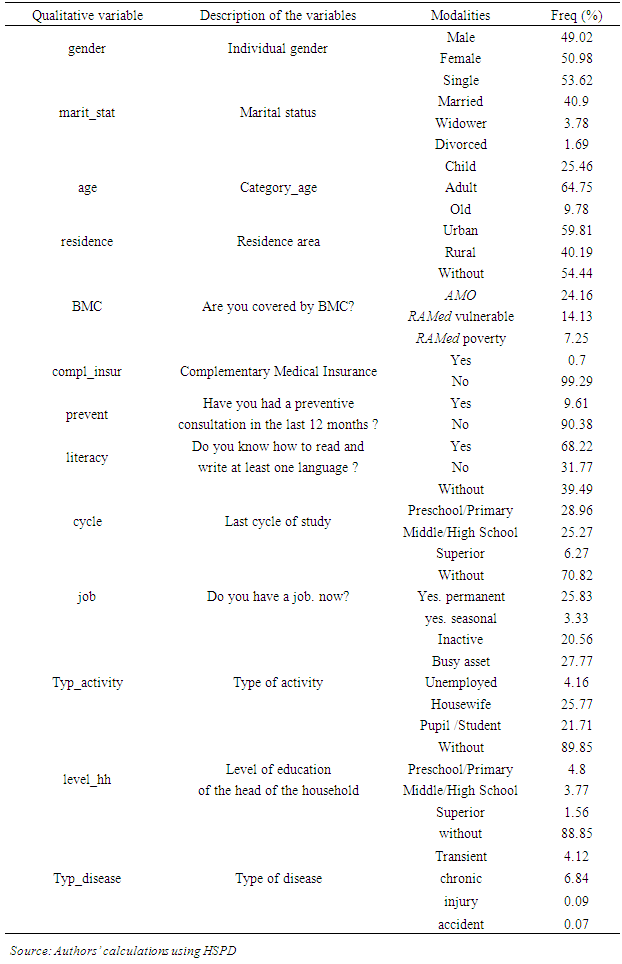

- The cross-sectional data set used in this paper came from National Observatory of Human Development (NOHD) Household Survey Panel Data (HSPD). The survey contained a sample of 8,000 households and obtained information on each individual within in their household (almost 37,234 person).It should be noted that the HSPD is a crosssectional and repeated survey that touches on all aspects of contemporary life and dimensions of human development, namely education, health, demography, housing conditions, and subjective poverty. This survey, the first of its kind in Morocco. The first was launched in 2012 and since then five waves had been completed. The last one ended in 2017.

4.1.2. Methods

- Cross-sectional data from the 3th (2015) Moroccan Household Survey Panel Data (HSPD). The CTM has been used to estimate the BMC effect on the utilization of healthcare expenditures. The data was analysed using STATA software for Windows (version 14).

4.1.3. Assumptions

- Based on the theoretical framework, basic hypotheses were adopted to achieve the main aim of this research project.Hypotheses: Insurance has a negative effect on individual health expenditures.To do so, five assistant hypotheses can be developed;- Female spend more than male on healthcare;- Education has a positive effect on consultation;- Complementary insurance reduces health expenses and increase consultation;- Rural residence influence negatively the number of consultation and increases health expenditures;- Household seize effect positively health expenses.

4.2. Descriptive Statistics

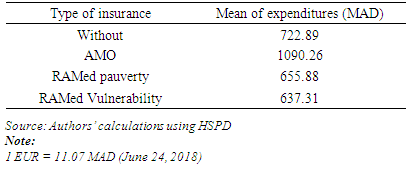

- Descriptive statistics for the main variables are shown in table 1 (appendix 4). During the recall period of one month prior to the survey, only about 4,232 the individuals reported that they made health expenditures, almost 11.37% of respondents. The rest were not sick during that period, or even if they are sick they did not use the healthcare services.According to the same table, in our panel survey there are more males than females among the members. By marital status, 53.62% are single and around 40.90% of the population are married. Children below 15 years of age represent 25.46%. The largest percentage of members was found in the adult age particularly the group between 16 and 60 years.By gender, women spend a little more than men from age 22 to 69 specifically woman age’s 30 to 40 spend on average 10% more than men of the same group.We also observe from the result in table 3 (appendix 4) that our key independent variable (the average expenditures per person) is 812.63 MAD per capita (about 73.40 Euros).By type of insurance, we observe that people who are covered by AMO spend on average 1,090 MAD (about 98.46 Euros) per month. Also, on average, an insured by Ramed spend less than an uninsured counterpart.

4.3. Econometric Modelling

- Following the theoretical framework, we will assume that health expenses (yi) will depend on sociodemographic characteristics, economic status and the household income. Mathematically, we can write that: yi = g (individual’s characteristics, BMC, Household variables)This basic equation examines the direct effect of health insurance on the individual health spending.

4.3.1. Study of the Variables

- - The endogenous variable

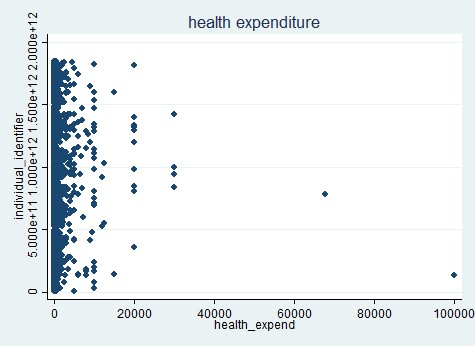

| Figure 1. Health expenditures (Source: Authors’ calculations using HSPD) |

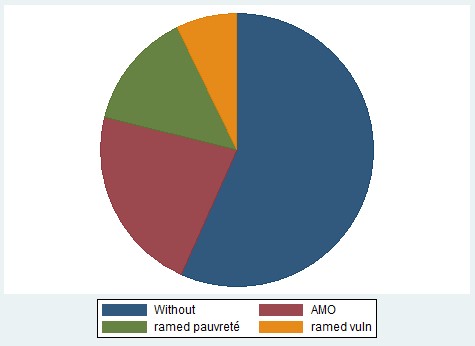

| Figure 2. Beneficiaries of the BMC by insurance types (Source: Authors’ calculations using HSPD) |

4.3.2. Estimation

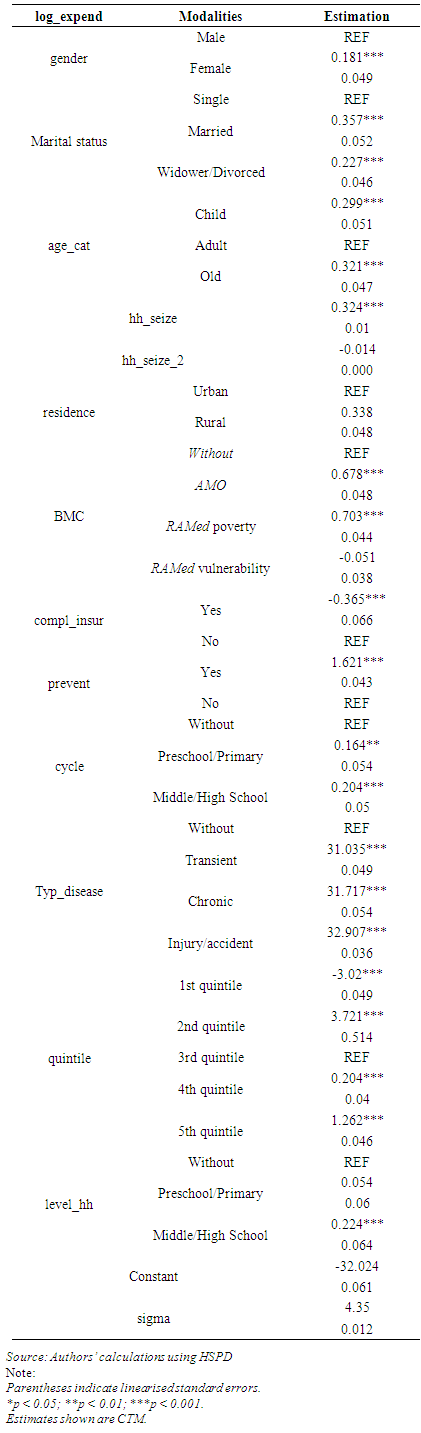

- We used STATA 14 to estimate CTM and to obtain parameters shown in table 4 (appendix 4). The results revealed that the variable of interest and the other endogenous variables generally produce effects in the expected directions.

4.4. Interpretation

- This section presents the interpretation of the finding from econometric analyses. It should be noted that the CTM coefficients are interpreted in the similar manner to OLS regression coefficients (McDonald and Moffitt, 1980). The major findings of our study can be summarized as follows:First, and unlike what was expected, the CTM revealed that acces to BMC is positively associated with health expenditures. In fact, the Compulsory Health Insurance (AMO) is statistically significant at the 0.1 percent level and positively correlated with expenditures. The predicted values of health expenses is 0.678 upper for the person who are covered by AMO than who are compared to those not covered by any insurance, while holding all other variables constant in this model.Second for RAMed program, there are two very different results. The RAMed Vulnerability program is negatively associated with expenses but not significant at the level of 5 percent. That means RAMed Vulnerability doesn’t have any effect on individual healthcare consumption. Whereas for the beneficiaries of the RAMed poverty, is positively correlated and statistically significant (p < 0.005) with the expenditures per capita. That means that, for all things constant, the RAMed poverty had been able to increase the health expenses of the poor population. Quantitatively, the predicted values of expenses is slightly more than 0.7 for people covered by RAMed compared to not covered. This result can be explained that for the beneficiaries of the AMO their expenses have increased because they expect a refund afterwards. While this is not the case for the covered by RAMed. Even though RAMed has facilitated access to care, it has not reduced the healthcare costs of poor people, especially since a large part of the budgets of poor households are devoted to the purchase of medicines. Hence the need to intervene at this level by putting policies and actions that facilitate the acquisition of medicines by the poor.For the other explanatory variables, the gender of the individual, the modelling revealed that the female has a positive relationship with expenses. In fact, being female increase health expenses by about 0.181 higher than it is for male. Also, Concerning the variable category of age is positively related with health expenses and significant at the level 0.001. The predicted value of expenses is slightly more than 0.29 points higher for the child and the old than for the adult.Furthermore, the result of our model demonstrated that large families spend more on healthcare. Indeed, holding all other variables constant in this model, more the size of the family increases the more health expenditures increases, but not necessarily with the same proportion. (p<0.001) Additionally, the variable area of residence is another major explanatory variable used in this analysis. Living in rural area increase significantly health expenditures by about 0.338 point higher than it is for person who live in urban area.In addition to the above demographic variables, another important explanatory variable is education.The estimation results indicated that people who are literate more precisely those who have a high cycle of study spend more healthcare than illiterates one. This relation is statistically significant at the 0.005 level. Education is believed to be an important factor influencing health expenses. Moreover, while the level of education of the head of household increases, while the health expenses increase which shows the breadth of education of the head of the household in the decision to go to consult or not. In other words, the more educated head of the household, the more likely to consult particularly if he had primary or secondary education degree. Moreover and as expected, type of disease is positively related with expenses at the 0.001 significance level which means that sick population spend more than others in healthcare which is quite normal. In fact, the predicted values of expenses is slightly more than 31 points upper for sick person than the non-sick.Finally, the decision of the consultation is strongly influenced by the standard of living of the households. Indeed, as long as the expenditures quantile increases, the probability of going to consult increases as well. This relation is statistically significant at the 0.001 level. The probability of going to consult is strongly correlated with consumer spending; wealthier households are more likely to consult compared to the poor.Also a very interesting result that emerges from this study, it concerns the complementary health insurance. This latter has a negative impact on the dependent variable, which means that supplementary insurance sharply reduces personal expenditures on healthcare.

5. Conclusions and Recommendations

5.1. Conclusions

- As a matter of methodology, the study clearly demonstrated that the CTM specification worked satisfactorily to censored data.In this article, the important effect of BMC on individual healthcare expenditures has been checked and confirmed for Moroccan data. Generally, the key points that can be summarised from this study are:- The estimated model underlines the positive effect of health insurance not only on the decision of access to care, especially for the poor, but also and above all on the cost of care avoided for the poorest populations:- Population insured by the RAMed plan, show a sharp increase in health expenditures compared to uninsured;- This study also showed that insured population by BMC spend more on healthcare compared to uninsured one;- Initial conditions, such as accident and chronic illnesses, seem to influence the decision to consult;- Residence in rural areas pushes households to spend more on healthcare if they made use the healthcare services.

5.2. Recommendations

- It is essential to carry on research works on the explanatory factors of access to care in order to develop appropriate health policies that promote access to care, especially for the poor.We show that the age comes out as an important factor as does income. Higher age leads to more claims as do higher income. Our recommendations can be summarized as follows:- The importance of maintaining a high level of coverage for low-income population;- Allowing free access to medicines for poor people and open private clinics for the person who are covered by RAMed;- Reduce wait times and appointments;- Improve the services offered to the beneficiaries.Lastly, while we think that the results presented in this document are robust, it nevertheless seems opportune to analyse the impact of the BMC using a dynamic approach in particular that of RAMed. Finally, it seems more important evaluate CHI on a large scale than on a small scale. An extension of this work on dynamic analysis (in panel) would be timely insofar as it would make it possible to measure the real impact of health insurance on beneficiaries.

Appendices and Acronyms

- AppendicesAppendix 1: Expected value using OLS method for the whole sample

Appendix 2: Density function for the strictly positive observations

Appendix 2: Density function for the strictly positive observations However,

However,

Because Ψ is an even function on RThus, the conditional expected values is given by:

Because Ψ is an even function on RThus, the conditional expected values is given by: Let z be a real variable such as:

Let z be a real variable such as:

Appendix 3: Density function for the CTM

Appendix 3: Density function for the CTM However,

However, Hence,

Hence, Appendix 4: List of tables

Appendix 4: List of tables

|

|

|

|

| Figure 3. Normality test (Source: Authors’ calculations using HSPD) |

| Figure 4. The log distribution of health (Source: Authors’ calculations using HSPD) |

|

|

|

ACKNOWLEDGEMENTS

- I would like to thank those who provided helpful comments and who have influenced this project especially:EL HASSAN El Mansouri General Secretary of National Observatory of Human Development (NOHD), Morocco. He is also a Doctor in Human Geography and Regional Planning of the Poitiers University.TETO Abdelkader Director of the Survey and Methods Pole at NOHD. He is also a Chief Engineer, Economist Statistician and Ex-director of Observatory of the Living Conditions of the Population in High Commission for Planning (HCP), Morocco. AOMAR Ibourk Professor of quantitative methods and social economics at the Cadi Ayyad University in Marrakech, Morocco. He is also the Director of Economic and Social Research Group at the same university.

Notes

- 1. See the proof in appendix 1.2. See the proof in appendix 2. 3. See the proof in appendix 3.