-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

Journal of Logistics Management

2019; 8(3): 51-60

doi:10.5923/j.logistics.20190803.01

Influence of Valence of Logistic Information Integration Capability on Firm Performance in Kenya

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLEdwin Kimitei, Joel Chepkwony, Charles Lagat, Ronald Bonuke

Department of Marketing & Logistics, Moi University, Eldoret, Kenya

Correspondence to: Edwin Kimitei, Department of Marketing & Logistics, Moi University, Eldoret, Kenya.

| Email: |  |

Copyright © 2019 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Firms may improve their performance by integrating their logistic capabilities in their daily operations. However, the valence/attributes of logistic capabilities used by the firms could potentially affect the overall relationships between logistic capabilities and firm performance. Therefore, this study determined the influence of the valence of logistic information integration capability and firm performance of manufacturing firms in Kenya. The study adopted explanatory research design. The target population comprised of 750 manufacturing firms registered under Kenya Association of Manufacturers from where a sample size of 442 firms were selected using stratified and simple random sampling approaches. The study demonstrated that each valence of logistic information integration capability has a significant effect on performance. Therefore, whenever firms aim at optimizing logistic information integration capabilities, the firms must pay more attention to each valence. Therefore, exploring avenues of improving each valence, logistic information integration capability firms may eventually improve the overall performance of the manufacturing firms.

Keywords: Firm Performance, Logistic Capabilities, Logistic Information Integration Capability, Manufacturing firms, Kenya

Cite this paper: Edwin Kimitei, Joel Chepkwony, Charles Lagat, Ronald Bonuke, Influence of Valence of Logistic Information Integration Capability on Firm Performance in Kenya, Journal of Logistics Management, Vol. 8 No. 3, 2019, pp. 51-60. doi: 10.5923/j.logistics.20190803.01.

Article Outline

1. Introduction

- Business organizations strive to improve their performance through improved profits margins, return on assets (ROA), return on investment (ROI), shareholder returns, market share, customer service, social responsibility, employee stewardship (Kristjansdottir, Shafiee, Bonev, Hvam, Bennick & Andersen, 2016; Torres, Sidorova & Jones, 2018; Owens, Wilson & Abell, 2019). Comprehensively, performance of the business organization can therefore be improved by focusing on these attributes and laying out strategies that may ultimately improve these attributes either independently or concomitance (Yang, Hong & Modi, 2011; Painter, Hibbert & Cooper, 2018; Cegarra-Navarro, Jiménez-Jiménez & Garcia-Perez, 2019; Kolade, Obembe & Salia, 2019). There are numerous strategies that firms can lay to improve their overall performance, of which the key is logistic capability. In business organizations, logistic capability include the firm’s resources (including assets, competencies, processes, firm attributes, information, etc) that permit them to implement plans that improve business efficiency and effectiveness (Najafizadeh & Kazemi, 2019). Firms engage logistic capabilities in supporting production in building company’s effectiveness, and facilitate profitability in the business environment (Durst & Evangelista, 2018) including morbidity from the point of origin to the point of consumption (Zijm & Klumpp, 2016; Fosso Wamba, Gunasekaran, Papadopoulos & Ngai, 2018). The capabilities are unique to each organization and may therefore differentially influence the inclusive performance. They include coordinating assets, competencies, organizational processes, information, knowledge etc (Schönsleben, 2018; Zijm, Klumpp, Heragu & Regattieri, 2019). Many firms prioritize to improve their logistics capabilities by giving more attention to information.Many firms have relied on accuracy of information in a business organization to properly coordinate their activities (Wang, Gosling & Naim, 2019). Therefore, firms that are able to implement proper logistic information integration capability have been established to have better firm performance (Prajogo, Toy, Bhattacharya, Oke & Cheng, 2018; Shou, Li, Park & Kang, 2018). Nevertheless, the operational success of logistic information integration capabilities of firms may be affected by other external factors that merit investigation. There are a number of attributes that define logistic information integration capabilities within the firms, which may differ among across several organizations. The widely reported valence of logistic information integration capabilities include information processing (Kmetz, 2018; Zhu, Song, Hazen, Lee & Cegielski, 2018), information linkages (Maiga, Nilsson & Ax, 2015; Bhattacharya & O'Hara, 2018; Nikolova-Jahn, Demirova & Entchev, 2018), information flexibility (Han, 2016; Chen, Wang, Nevo, Benitez & Kou, 2017; Han, Wang & Naim, 2017), information control systems (Duréndez, Ruíz-Palomo, García-Pérez-de-Lema & Diéguez-Soto, 2016; Esparza-Aguilar, García-Pérez-de-Lema & Duréndez, 2016; Ahmad & Mohamed, 2017), information technology (Cui, Ye, Teo & Li, 2015; Wang, Chen & Benitez-Amado, 2015) among others. Firms intending to improve their overall performance therefore, need to emphasize the role of individual valence and relate them to performance. However, there are currently few studies that have looked at the influence of each of the valence on the overall firm performance. Therefore, the aim of this study was to evaluate influence of the valence of logistic information integration capability on performance of manufacturing firms in Kenya, furthermore, test the following hypothesis: H01: There is an association between valence of firms’ logistic information integration capabilities and firm performance.

2. Literature Review

2.1. Firm Performance

- There is vast amount of literature on firm performance and the extent to which performance allow firms to achieve their set of targets (Wamba, Gunasekaran, Akter, Ren, Dubey & Childe, 2017; Erhardt, 2018; Juhn, McCue, Monti & Pierce, 2018). These targets include both objective (numerical) and subjective (judgmental) indicators. Thus, performance can be construed in the form of quality, flexibility, and on time delivery (Lomberg, Urbig, Stöckmann, Marino & Dickson, 2017). Performance is also examined through service and cost dimensions (Jayaram & Xu, 2016). Costs concerns price related to the firm while service aspect of the performance focuses on flexibility of service delivery and timely delivery of services (Jayaram & Xu, 2016). On the basis of cost, performance may be viewed as financial or non-financial (Oztekin, Delen, Zaim, Turkyilmaz & Zaim, 2015).Firm performance is measured in terms of effectiveness, efficiency, relevance, and financial practicality (Arena, Azzone & Bengo, 2015). Effectiveness measures the degree to which the organization is successful in achieving its internal strategy, efficiency refer to how well the organization utilizes its resources to in pursuit of its goals, relevance measure provides information on the degree to which stakeholders believe that the organization is relevant in meeting its needs. Financial viability measures the financial feasibility the organization in the short and long term. Several financial measures are available to the organizations such as calculation of profits, Return on Assets (ROA), Return on Equity (ROE), Return on Investment (ROI), Return on Sales (ROS), Earning before Interest and Tax (EBIT), Economic Value Added (EVA) etc (Pekkola, Saunila & Rantanen, 2016; Strouhal, Štamfestová, Ključnikov & Vincúrová, 2018; Aydiner, Tatoglu, Bayraktar & Zaim, 2019). The financial returns are easily available in every organizations in forms of regular financial reports thus from research perspective, these measures makes it easy to determine performance (Hope, Thomas & Vyas, 2013; Sunder, 2016). As a routine, organizations are not willing to provide accurate financial performance, while others find do not maintain transparency in financial reporting and thus provide reports that are inaccurate, exaggerated or out rightly false (Barth & Schipper, 2008). In recent times, organizations are attempting to evaluate firms performance using non-financial measures such as market share, innovation rate customer service, customer satisfaction, social responsibility, customer retention or loyalty employee stewardship etc (Goel, 2017; Omran, Khallaf, Gleason & Tahat, 2019), which have been described as subjective (Singh, Darwish & Potočnik, 2016). Other studies have used a combination of both objective and subjective measures (Lomberg et al., 2017). Nevertheless, there is still no consensus among researchers as to which specific variables should be exclusively used as measure of indicators of firm. Regardless of its possible outcome, subjective measures have been widely used to determine performance in business organizations (Vij & Bedi, 2016). Consequently, this study chose to measure firm performance using customer satisfaction, customer retention or loyalty, and sales growth which combines some form of subjective measurement indicators and objective indicators to derive at a more robust performance indicator.

2.2. Valence of Logistics Information Integration Capability

- Logistics capability encompass part of a firm’s resources including assets, competencies, firm attributes, organizational processes, and information that allow for the implementation of strategies intended at improving efficiency and effectiveness (Zawawi, Wahab, Al Mamun, Ahmad & Fazal, 2017; Rajagopal, Krishnamoorthy & Khanapuri, 2018; Wen & Min, 2018). In attempting to achieve effectiveness of the logistics capabilities, firms pay more attention to process capability, learning capability, service reliability capability, flexibility capability and information integration capability (Sandberg & Abrahamsson, 2011; Wilding, Wagner, Gligor & Holcomb, 2012). Firms are aware that information can be lifeblood when it comes to operational success, thus logistic information integration capabilities remains one of the key dimensions of logistic capabilities. Logistic information integration capabilities link different levels in the system such as information sources, such as order information, purchasing in order, production information plan, the packaging information schedule, the transport information, distribution information, financial disbursement information etc (Neubert, Ouzrout & Bouras, 2018). Logistic information integration also foster timely information interchange which is essential in handling changes within the organizational processes to meet up to the customer requirement (Ketikidis, Koh, Dimitriadis, Gunasekaran & Kehajova, 2008; Voronkova, Kurochkina, Firova & Bikezina, 2017). Accordingly, logistic information integration capability plays a crucial role in enhancing morbidity of goods and services, which relies on logistics capability information processing (Zhu et al., 2018), information linkages (Maiga et al., 2015; Bhattacharya & O'Hara, 2018; Nikolova-Jahn et al., 2018), information flexibility (Han, 2016; Chen et al., 2017; Han et al., 2017), information control systems (Esparza-Aguilar et al., 2016; Ahmad & Mohamed, 2017), information technology (Wang et al., 2015). Moreover, information integration capabilities of a firm may ensures unhindered access to documents that can be used to improve operational efficiency of the organization (Gunasekaran, Papadopoulos, Dubey, Wamba, Childe, Hazen & Akter, 2017b). Majority of the firms use logistics information integration capability systems to enhance inventory control, track orders and materials and monitor resource utilization (Neubert et al., 2018; Yu, Luo, Feng & Liu, 2018). Subsequently, well-articulated logistic information integration capability guides the entire organization and helps it to coordinate logistics operations process. Therefore, studies on logistics information integration capabilities remain relevant to date.

2.3. Valence of Logistic Information Integration Capability and Firm Performance

- It has been widely established that timely and accurate information positively impact firm performance (Graca, Doney & Barry, 2017; Kembro, Näslund & Olhager, 2017; Prajogo et al., 2018). Logistic information integration capability satisfies customers perceived information about order status, product availability, delivery schedule and invoices as well as increase the flexibility with regard to methodologies of resources utilization. As such, there are direct effects of logistic information integration capability and overall performance of the firm (Sabherwal & Jeyaraj, 2015; Gu, Jitpaipoon & Yang, 2017). However, there are several contentions about which valence of the logistic information integration capabilities that affect firm performance.Proper communication of information along the supply chain enables the combination of operational and information flow, which provides transparent, networks for suppliers and customers thus creating effective firm management. According to Zhang et al., (2011), logistic information integration capability increases supply chain visibility through collaboration among supply chain members via real-time data sharing and enhance time-based delivery thus increasing firm performance. With sufficient information and with increased visibility and communication between various logistics operations and shareholders, different parties along the supply chain can promptly make appropriate decisions which in turn improve efficiency in logistics management. In fact, the recent advanced in technology have assisted in improving firm performance through improved accuracy in information management (Inkinen, 2016). There are several empirical evidences supporting logistic information integration capability in improving firm performance (Maiga et al., 2015; Wong, Lai & Bernroider, 2015; Singh & Teng, 2016; Gunasekaran, Subramanian & Papadopoulos, 2017a; Kim & Chai, 2017). However, studies relating to the valence of logistic information integration capability affect firm performance are not widely studied in literature. Therefore, aspects of firm’s logistics information integration capability affecting firm performance have remained neglected.

2.4. Theoretical Perspective

- This study used the resource-based view which asserts that firms can gain and sustain competitive advantages which results to superior performance by developing and positioning valuable resources and capabilities or through acquiring and controlling the resources (Barney, 2001; Schroeder, Bates & Junttila, 2002; Kraaijenbrink, Spender & Groen, 2010). In the context of RBV, organizations are viewed on how their assets, systems and capabilities are used in creating value. In most cases, the firms that gain advantage are those capable of accumulating resources and capabilities that are rare, valuable, non-substitutable and difficult to imitate. Capabilities of the firms take diverse forms such as innovation, organizational learning, and stakeholder integration (Siguaw, Simpson & Enz, 2006). Accordingly, the focus has been on those capabilities and resources contained within the organization. Nevertheless, a firm's resources extending beyond their boundaries, is also capable of creating a competitive advantage and should also be considered. There is a relatively large literature in logistics information integration capability considering the realm of RBV. The RBV therefore can present a theoretical foundation for this study to examine the relationships between logistic information integration capability and firm performance.

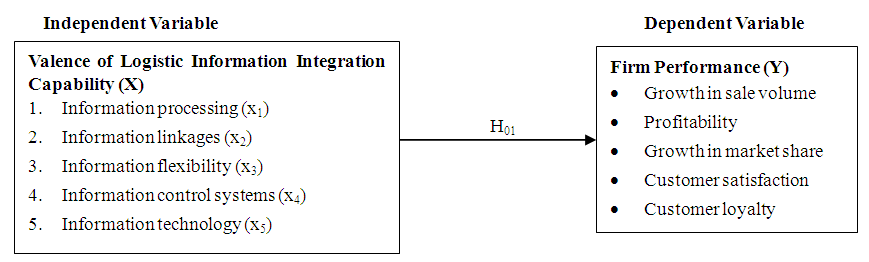

2.5. Conceptual Model of the Study

- Conceptual models show the relationships between the independent and dependent variables. In this study, the conceptual model is shown in Figure 1. In the model the researcher tested the hypothetical relationship between the valence of logistic information integration capability which was determined by information processing (x1), information linkages (x2), information flexibility (x3), information control systems (x4) and information technology (x5). The dependent variable firm performance which was measured by growth in sale volume, profitability, growth in market share, customer satisfaction and customer loyalty.

| Figure 1. Conceptual Framework |

3. Methodology

- This study is in line with positivism approach, which seeks to use existing theory to deduce and formulate variables. The study adopted explanatory research design of a cross sectional nature. Explanatory research design analyses the cause-effect relationship between two or more variables (Leavy, 2017; Rahi, 2017). Hence the design was appropriate to the study because the research sought to establish a cause-effect relationship on the two constraints which is logistic information integration capability and firm performance. The target population were 750 manufacturing firms registered with Kenya Association of Manufacturers (KAM, 2018). The targeted unit of analysis were purchasing and logistic managers. Stratified sampling combined with simple random sampling technique was used to select sample size. Structured questionnaires used to collect data for dependent, mediating and independent variables, where each item was subjected to Five-point Likert was used.The dependent variable was firm performance measured using subjective measures of sales volume, profits, market share, customer satisfaction, customer loyalty and new products over the past three years as described in previous research studies (Farris, Bendle, Pfeifer & Reibstein, 2010; Santos & Brito, 2012; Hill & Alexander, 2017). The independent variable was logistic information integration capability was measured based on literature from previously published methods (Lu & Yang, 2010; Wiengarten, Pagell, Ahmed & Gimenez, 2014). To reduce the effects of confounding variables, the study included two control variables vis: firm size quantified by the number of employees and firm age (number of years in operation). The reliability of the research instrument was tested using the internal consistency technique by employing Cronbach Alpha value of 0.7. Internal and external validity was assessed to establish whether the research instrument truly measures what it is intended to (Patino & Ferreira, 2018). Descriptive statistics used were mean and standard deviation; Pearson correlation coefficient were applied to test the relationship and strength between the variables. Multiple regression models were used to test the hypothesis.

4. Results and Discussion

4.1. Characteristics of the Respondents

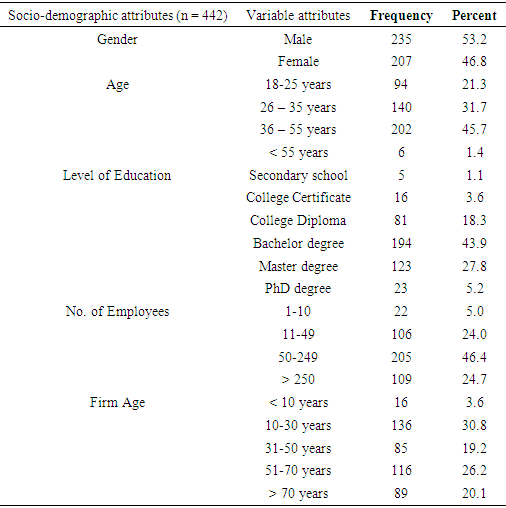

- The overall results of the socio-demographic background of the respondents are presented in Table 1. There were a higher proportion of the males compared with females suggesting more male employees in the firms. Most of the employees (45.7%, n = 202) were aged 36 to 55 years followed by 26–35 years. The least but not last is 21.3% (94) are above 18 to 32 years; lastly, 1.4% (6) is above 63 years. In terms of educational status, 43.9% attained Bachelor degree, 27.9% Master degree, 18.3% Diploma, 3.6% (16) of the respondents have Certificate level of education. Majority of firms employed between 50 and 249 employees (46.4%) followed by > 250 employees (24.7%) while 5% had less than 10 employees. Finally, overall age of the firm indicated that most had been operational operation from 10 to 30 years followed by those operating between 51-70 years. 26.2% had operated for a period ranging from 51 to 70 years while 3.6% (16) were in operation for less than 10 years.

|

4.2. Reliability of Research Instruments

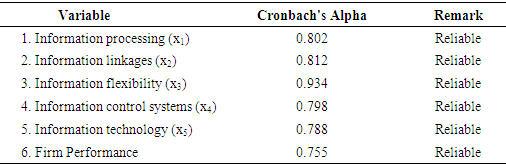

- Since reliability is a measure of how much instruments yield predictable outcomes or data after repeated preliminaries (Heale & Twycross, 2015). The alpha coefficient results of the reliability tests carried out in Table 2 show that Information flexibility yielded the highest reliability (α = 0.934), followed by Information linkages (α = 0.819), Information processing (α = 0.802), Information control systems (α = 0.798), Information technology (α = 0.788), and finally, firm performance had a reliability score of (α = 0.755). Reliability coefficients above 0.7 are considered acceptable and thus in the current study they were all good.

|

4.3. Firm Performance

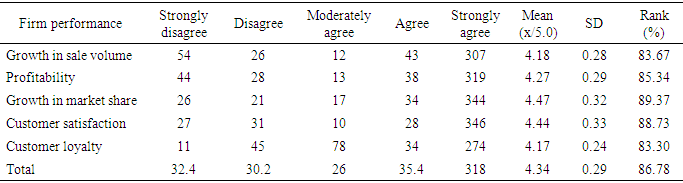

- The dependent variable for this study was firm performance. The metric score for the firm performance is shown in Table 3. Based on five attributes of performance, the overall mean of 4.34/5.00 indicated a good firm performance. Among the attributes, Growth in market share, Customer satisfaction and Profitability were the greatest contributors to firm performance.

|

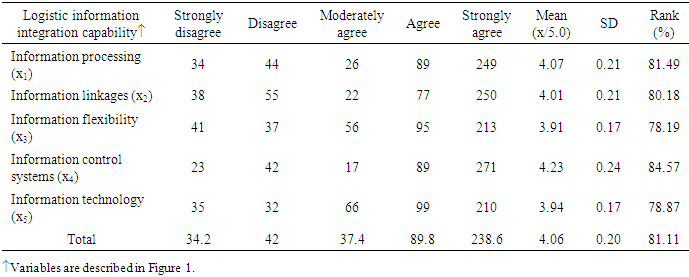

4.4. Valence of Logistic Information Integration Capability

- The metric scores for the Valence of Logistic Information Integration Capability are shown in Table 4. The overall score of the logistic information integration is high (4.06/5.00) among the sampled firms, suggesting that they properly manage their logistic information capability. Among the valence of logistic information integration, Information control systems, Information processing and Information linkages scored the highest ranks of >4/5.00 showing that these valences were the most important in firm as previously established. Information flexibility and Information technology were equally important component of logistic information integration among the firms with overall metric scores above 3.5/5.00 which still ranks as good.

|

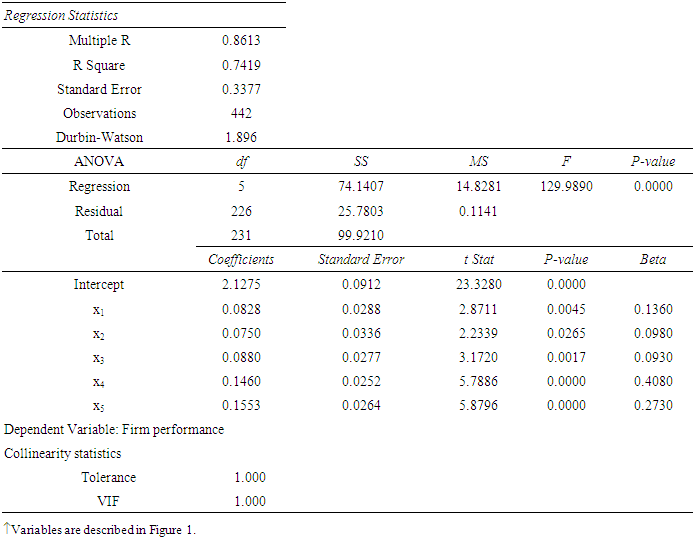

4.5. Test for the Direct Effects of Valence of Logistic Information Integration Capability on Firm Performance

- Multiple regression statistics showing the relationship between valence of logistic information integration capability and firm performance is provided in Table 5. The regression results confirm that the overall valence of logistic information integration capability strongly influenced the firm performance (r = 0.7419, R2 = 0.8613, P < 0.05). Accordingly, Information control systems (β = 0.4080), Information technology (β = 0.2730) and Information processing (β = 0.1360) significantly explained the firm performance. These results concur with several previous studies (Klein & Rai, 2009; Pereira, 2009; Wong, 2013; Huo, Han & Prajogo, 2016) due to the firms capacity to respond to threats and contingencies hence able to improve the positive attributes of firm performance. A critical look of this valence suggest that logistic information integration enabled the firms to coordinate flow of materials along the value chain hence enabling the supply chain entities to prepare well for contingencies. The positive relationships may also be related to proper information flow within the entire supply chain that may improve firm performance (Maiga et al., 2015; Gunasekaran et al., 2017a). The remaining factors including Information linkages (β = 0.0980) and Information flexibility (β = 0.0930) were not strongly significant factors explaining firm performance.

|

5. Conclusions

- This study tested a null hypothesis that there no significant empirical relationship between valence of Logistic information integration capability and firm performance (H01). The study provided evidence that Information control systems, Information technology and Information processing were the most important valence that significantly explained firm performance. For a long-term development, manufacturing firms should clearly delineate the most important valence of logistic information integration capability and enhance them while improving those that are not highly rated in the firm. In highly competitive firm environment where differentiation is the key competitive advantage, strong valence associated with logistic information integration is required to enhance the overall information flow within the supply chain. In addition, coordinated upstream and downstream linkages should consider incorporating the valence of logistic information integration capability. The study findings established that better performing manufacturing firms must employ certain valence of logistic information integration capabilities. Therefore, there is need for manufacturing firms to adopt integrated logistic information capabilities to that enables them to benefit from reliable order cycles and reduce various inventory costs. Besides, exhibiting superior performance, they need to collect and process logistic information and share related logistic information with other departments. This will aid firm in planning and dedicating sufficient resources towards attaining firm effectiveness in terms of operations and improve the overall performance. Manufacturing firms should invest only on those information capabilities that can create a competitive differentiation strategy for sustainable performance. Moreover, managers must not only develop unique capabilities internally, but they must recognize the combined effects of supply chain practices that can generate a total impact on operational capabilities both at upstream and downstream of the supply chain.In emphasizing the importance of Resource Based view theory, firms are should evaluate potential factors that can be deployed to confer to firm performance including using available resources to add value to their products. It also encourages firms to produce their products in a way that they cannot be imitated or substituted to increase their performance. Therefore, the contribution of this theory is validated by this study since it encourages the management of manufacturing firms to invest in improving logistic information integration capability to develop, nurture and maintain key resources and competencies in order to improve the performance of the firm.From a local context, this study extends previous logistic information integration capability and firm performance frameworks in developing countries by considering different key dimensions of valence logistic information integration capability practices in Kenyan manufacturing and performance respectively. Such information is rare in the domains of low developed countries especially in the Sub Saharan Africa where firm performance may be a challenge.

ACKNOWLEDGEMENTS

- I am grateful to Prof. Charles Lagat, Dr. Ronald Bonuke and Dr. Joel Chepkwony for their professional guidance, inspiration, patience, support and advice throughout the entire process of developing this research paper. Our special thanks go to Moi University for their administrative and technical support.