Quang Phung Duy

Department of Mathematics, Foreign Trade University, Ha noi, Viet Nam

Correspondence to: Quang Phung Duy , Department of Mathematics, Foreign Trade University, Ha noi, Viet Nam.

| Email: |  |

Copyright © 2012 Scientific & Academic Publishing. All Rights Reserved.

Abstract

The aim of this paper is to build an exact formula for ruin probability of generalized risk processes under constant interest force with sequences of random variables such that these sequences are usually assumed to be positive integer – valued random variables. An exact formula for finite time ruin (non-ruin) probabilities are derive by using technique of classical probability. A numerical example is given to illustrate results.

Keywords:

Ruin Probability, Non –ruin Probability, Homogeneous Markov Chain

Cite this paper: Quang Phung Duy , Computing Ruin Probability in Generalized Risk Processes under Constant Interest Force, International Journal of Probability and Statistics , Vol. 2 No. 2, 2013, pp. 35-41. doi: 10.5923/j.ijps.20130202.04.

1. Introduction

Claude Lefèvre and Stéphane Loisel[1] studied the problem of ruin in the classical compound binomial and compound Poisson risk models. Their primary purpose is to extend those models which is an exact formula derived by Picard and Lefèvre[9] for the probability of (non-ruin) ruin within finite time. Hong N.T.T. (see [7]) recently built an exact formula for finite time ruin (non-ruin) probability for model:  With

With  are positive integer number.However, Claude Lefèvre and Stéphane Loisel[1] did not provide an exact formula for ruin probability of generalized risk processes under constant interest force with sequences of random variables such that these sequences are usually assumed to be positive integer – valued random variables, with surplus process

are positive integer number.However, Claude Lefèvre and Stéphane Loisel[1] did not provide an exact formula for ruin probability of generalized risk processes under constant interest force with sequences of random variables such that these sequences are usually assumed to be positive integer – valued random variables, with surplus process  written as

written as | (1.1) |

where  is initial surplus (

is initial surplus ( ),

), is constant interest (

is constant interest ( ),

), and

and  are positive integer numbers,

are positive integer numbers,  and

and  take values in a finite set of positive integer numbers;

take values in a finite set of positive integer numbers;  and

and  are assumed to be independent.With these assumptions, the aim of this paper is to build an exact formula for finite time ruin (non-ruin) probability of model (1.1). In our study, we extended the result of Hong N. T. T for model (1.1) with any r > 0. This is the first time that gives an exact formula for ruin (non-ruin) probability for model (1.1) whose exact formula for finite time ruin (non-ruin) probability are derived by using technique of classical probability.The paper is organized as follows; in Section 2, we build an exact formula for ruin (non-ruin) probability for model (1.1) with

are assumed to be independent.With these assumptions, the aim of this paper is to build an exact formula for finite time ruin (non-ruin) probability of model (1.1). In our study, we extended the result of Hong N. T. T for model (1.1) with any r > 0. This is the first time that gives an exact formula for ruin (non-ruin) probability for model (1.1) whose exact formula for finite time ruin (non-ruin) probability are derived by using technique of classical probability.The paper is organized as follows; in Section 2, we build an exact formula for ruin (non-ruin) probability for model (1.1) with  and

and  being independent and identically distributed positive integer – valued random variables,

being independent and identically distributed positive integer – valued random variables,  and

and  are assumed to be independent. An extended result in Section 2 with

are assumed to be independent. An extended result in Section 2 with  and

and  being homogeneous Markov chains is given in Section 3. A numerical example is give to illustrate these results in Section 4. Finally, we conclude our paper in Section 5.

being homogeneous Markov chains is given in Section 3. A numerical example is give to illustrate these results in Section 4. Finally, we conclude our paper in Section 5.

2. Computing Ruin Probability of Generalized Risk Processes under Constant Interest Force with Sequences of Independent and Identically Distributed Random Variables

Let model (1.1). We assume that:Assumption 2.1. u and t are positive integer numbers.Assumption 2.2  is a sequence of independent and identically distributed random variables,

is a sequence of independent and identically distributed random variables,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers with

with  ,

, .Assumption 2.3

.Assumption 2.3  is a sequence of independent and identically distributed random variables,

is a sequence of independent and identically distributed random variables,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers  with

with  ,

, .Assumption 2.4

.Assumption 2.4  and

and  are assumed to be independent.From (1.1), we have:

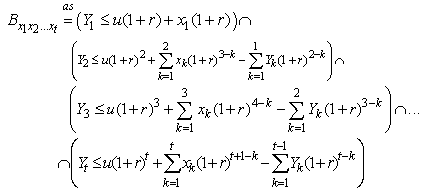

are assumed to be independent.From (1.1), we have: | (2.1) |

Supposing that the ruin time is defined by , where

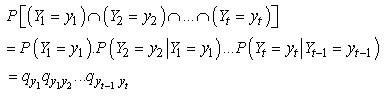

, where  .We define the finite time ruin (non-ruin) probabilities of model (1.1) with Assumption 2.1 to Assumption 2.4, respectively, by

.We define the finite time ruin (non-ruin) probabilities of model (1.1) with Assumption 2.1 to Assumption 2.4, respectively, by | (2.2) |

| (2.3) |

Throughout this paper, we denote  if

if  To establish a formula for

To establish a formula for  , we first proof the following Lemma.Lemma 2.1. Any u and

, we first proof the following Lemma.Lemma 2.1. Any u and  are positive integer numbers.With

are positive integer numbers.With  being a positive integer number and

being a positive integer number and  satisfies:

satisfies: | (2.4) |

then | (2.5) |

Proof.From (2.4), we have Implies

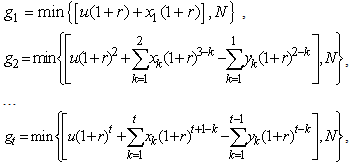

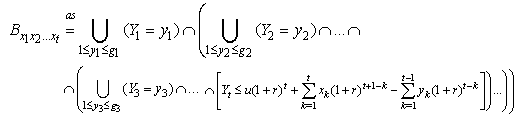

Implies Hence (2.5) holds.This completes the proof.Next, we give an exact formula for finite time non-ruin (ruin) probability of model (1.1).Theorem 2.1. Let model (1.1) satisfy Assumption 2.1 to Assumption 2.4, then finite time non-ruin probability of model (1.1) is defined by

Hence (2.5) holds.This completes the proof.Next, we give an exact formula for finite time non-ruin (ruin) probability of model (1.1).Theorem 2.1. Let model (1.1) satisfy Assumption 2.1 to Assumption 2.4, then finite time non-ruin probability of model (1.1) is defined by | (2.6) |

where ,

, ,…

,… ,In addition,

,In addition,  is integer part of the

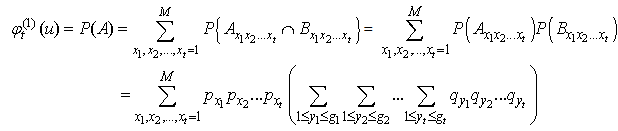

is integer part of the  .Proof.Firstly, we have

.Proof.Firstly, we have

| (2.7) |

By Assumption 2.2, we let  with

with  being positive integer numbers and satisfying:

being positive integer numbers and satisfying:  . Let

. Let .Since

.Since  is a sequence of independent random variables then

is a sequence of independent random variables then | (2.8) |

Hence, (2.7) is given | (2.9) |

where | (2.10) |

By Assumption 2.3, we let  with

with  being positive integer numbers andsatisfying:

being positive integer numbers andsatisfying:  . Let

. Let In addition,

In addition,  is integer part of

is integer part of  ,By using Lemma 2.1,

,By using Lemma 2.1,  ,

,  , …,

, …,  are integer numbers.Thus, (2.10) is written as

are integer numbers.Thus, (2.10) is written as | (2.11) |

As Assumption 2.3, we let  with

with  is positive integer number then

is positive integer number then  . Combining Assumption 2.3, (2.10) and formulas define

. Combining Assumption 2.3, (2.10) and formulas define  , we have

, we have  .Therefore, (2.11) can be rearranged as

.Therefore, (2.11) can be rearranged as | (2.12) |

For the reason that  is a sequence of independent random variables then

is a sequence of independent random variables then In the other hand, system of events

In the other hand, system of events  in (2.12) is incompatible then

in (2.12) is incompatible then | (2.13) |

Next, we consider and

and By using,

By using,  and

and  are independent, if

are independent, if  and

and  hold then

hold then  and

and  are independent events. In addition, system of events

are independent events. In addition, system of events  in (2.9) is incompatible. Therefore, combining (2.8) and (2.13), we have

in (2.9) is incompatible. Therefore, combining (2.8) and (2.13), we have | (2.14) |

This completes the proof.Corollary 2.1. Let model (1.1) satisfy Assumption 2.1 to Assumption 2.4, then finite time ruin probability of model (1.1) is defined by | (2.15) |

Remark 2.1. Formula (2.6) (or (2.15)) gives a method to compute exactly finite time non-ruin (ruin) probability of model (1.1) which  and

and  are sequences of independent and identically distributed random variables, and they take values in a finite set of positive integer numbers.

are sequences of independent and identically distributed random variables, and they take values in a finite set of positive integer numbers.

3. Computing Ruin Probability of Generalized Risk Processes under Constant Interest Force with Homogeneous Markov Chains

Let model (1.1). We assume that:Assumption 3.1.  are positive integer numbers.Assumption 3.2.

are positive integer numbers.Assumption 3.2.  is a homogeneous Markov chain,

is a homogeneous Markov chain,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers  with

with  where

where  . In addition,

. In addition, .Assumption 3.3.

.Assumption 3.3.  is a homogeneous Markov chain,

is a homogeneous Markov chain,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers  with

with  where

where  . In addition,

. In addition,  Assumption 3.4.

Assumption 3.4.  and

and  are assumed to be independent.Supposing that the ruin time is defined by

are assumed to be independent.Supposing that the ruin time is defined by  where

where  .We define the finite time ruin (non-ruin) probability of model (1.1) using Assumption 3.1 to Assumption 3.4, respectively, by

.We define the finite time ruin (non-ruin) probability of model (1.1) using Assumption 3.1 to Assumption 3.4, respectively, by | (3.1) |

| (3.2) |

Similar to Theorem 2.1, we haveTheorem 3.1. Let model (1.1) satisfy Assumption 3.1 to Assumption 3.4, then finite time non-ruin probability of model (1.1) is defined by | (3.3) |

where,  is defined in the same way with Theorem 2.1.Proof.We proof similarly as Theorem 2.1, where, (2.8) replaced by

is defined in the same way with Theorem 2.1.Proof.We proof similarly as Theorem 2.1, where, (2.8) replaced by In the other hand, we have

In the other hand, we have  In addition, (2.13) substituted by

In addition, (2.13) substituted by By using the same method to prove Theorem 2.1, we have formula (3.3).This completes the proof.Corollary 3.1. Let model (1.1) satisfy Assumption 3.1 to Assumption 3.4, then finite time ruin probability of model (1.1) is defined by

By using the same method to prove Theorem 2.1, we have formula (3.3).This completes the proof.Corollary 3.1. Let model (1.1) satisfy Assumption 3.1 to Assumption 3.4, then finite time ruin probability of model (1.1) is defined by | (3.4) |

Remark 3.1. Formula (3.3) (or (3.4)) gives a method to compute exactly finite time non-ruin (ruin) probability of model (1.1) which  and

and  are homogeneous Markov chains and they take values in a finite set of positive integer numbers.

are homogeneous Markov chains and they take values in a finite set of positive integer numbers.

4. Numerical Illustration

4.1. Numerical Illustration for

Let  be a sequence of independent and identically distributed random variables,

be a sequence of independent and identically distributed random variables,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers  with

with  having a distribution:

having a distribution: Let

Let  be a sequence of independent and identically distributed random variables,

be a sequence of independent and identically distributed random variables,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers  with

with  having a distribution:

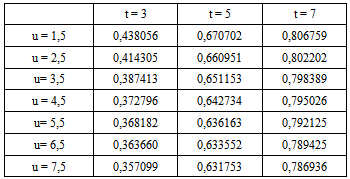

having a distribution: By using the C progaram, the

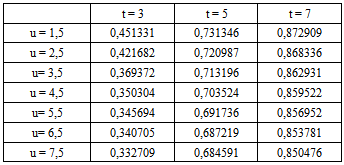

By using the C progaram, the  is calculated with the assumptions above of random variables

is calculated with the assumptions above of random variables  .Table 4.1 shows

.Table 4.1 shows  for a range of value of u.

for a range of value of u.Table 4.1. Ruin probabilities of model (1.1) with Assumption 2.1- 2.4 and r = 0,15

|

| |

|

4.2. Numerical Illustration for

Let be a homogeneous Markov chain,

be a homogeneous Markov chain,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers ,with

,with  having a distribution

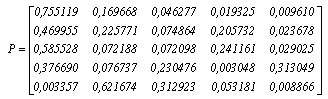

having a distribution In addition, matrix

In addition, matrix  is given by

is given by Let

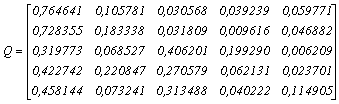

Let  be a homogeneous Markov chain,

be a homogeneous Markov chain,  take values in a finite set of positive integer numbers

take values in a finite set of positive integer numbers , with

, with  having a distribution

having a distribution In addition, matrix

In addition, matrix  is given by

is given by By using the C progaram, the

By using the C progaram, the  is calculated with the assumptions above of random variables

is calculated with the assumptions above of random variables  and matrixs

and matrixs  .Table 4.2 shows

.Table 4.2 shows  for a range of value of u.

for a range of value of u.Table 4.2. Ruin probabilities of model (1.1) with Assumption 3.1-3.4 and r = 0,15

|

| |

|

5. Conclusions

By using technique of classical probability with  , claims, premiums all are positive integer numbers and

, claims, premiums all are positive integer numbers and  is a positive number, this paper constructed an exact formula for ruin (non-ruin) probability of model (1.1), where sequences of claims and premiums are independent and identically distributed random variables or homogeneous Markov chains. Our main results in this paper not only prove Theorem 2.1 and Theorem 3.1 but also give numerical examples to illustrate for Theorem 2.1 and Theorem 3.1. These results proof for the suitability of theoretical results and practical examples. It also mean that:When initial

is a positive number, this paper constructed an exact formula for ruin (non-ruin) probability of model (1.1), where sequences of claims and premiums are independent and identically distributed random variables or homogeneous Markov chains. Our main results in this paper not only prove Theorem 2.1 and Theorem 3.1 but also give numerical examples to illustrate for Theorem 2.1 and Theorem 3.1. These results proof for the suitability of theoretical results and practical examples. It also mean that:When initial  is increasing then

is increasing then  ,

, are decreasing,With

are decreasing,With  being unchanged, when

being unchanged, when  is increasing then

is increasing then  ,

, are increasing.

are increasing.

ACKNOWLEDGMENTS

The authors are thankful to the referee for providing valuable suggestions to improve the quality of the pape.In addition, the author would like to thank my advisor, Professor Bui Khoi Dam for his patient guidance, encouragement and advice.

References

| [1] | Claude Lefèvre, Stéphane Loisel, On finité - time ruina probabilities for classical models, Scandinavian Actuarial Journal, Volume 2008, Issue 1, (2008), 56-68. |

| [2] | De Vylder, F. E., La formule de Picard et Lefèvre pour la probabilité de ruine en temps fini, Bulletin Francais d’Actuariat, 1, (1997), 31-40. |

| [3] | De Vylder, F. E., Numerical finite – time ruin probabilities by the Picard – Lefèvre formula. Scandinavian Actual Journal, 2, (1999), 97-105. |

| [4] | De Vylder, F. E. and Goovaerts, M. J., Recursive calculation of finite – time ruin probabilities, Insurance: Mathematics and Economics, 7, (1998), 1-7. |

| [5] | De Vylder, F. E. an d Goovaerts, M.J., Explicit finite – time and infinite – time ruin probabilities in the continuous case. Insurance: Mathematics and Economics,24, (1999)155-172. |

| [6] | Gerber, H.U., An Introduction to Mathematical Risk Theory. S. S. Huebner Foundation Monograph, University of Philadelphia: Philadelphia. Insurance: Mathematics and Economics, 24, (1979),155-172. |

| [7] | Hong, N.T.T, On finite – time ruin probabilities for general risk models. East-West Journal of Mathematics: Vol.15, No1 (2013), pp.86-101. |

| [8] | Ignatov, Z.G., Kaishev, V. K. and Krachunov, R. S., An improved finite – time ruin probability formula and its Mathematica implementation. Insurance: Mathematics and Economics, 29, (2001), 375-386. |

| [9] | Ignatov, Z.G., Kaishev, V. K., A finite – time ruin probability formula for continuous claim severities. Journal of Applied Probability, 41,(2004), 570-578. |

| [10] | Picard, Ph. and Lefèvre, Cl., The probability of ruin in finite time with discrete claim size distribution. Scandinavian Actuarial, (1997), 58 – 69. |

| [11] | Rullière, D. and Loisel, St., Another look at the Picard – Lefèvre formula for finite – time ruin probabilities. Insurance: Mathematics and Economics,35,(2004),187-203. |

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTML