| [1] | Adeyemi, S.L. and Salami, A.O. 2010. Inventory management: A tool of optimizing resources in a manufacturing industry a case study of Coca-Cola bottling company, Ilorin Plant. Journal of social science. 23(2), pp.135-142. |

| [2] | Agus, A. and Noor, Z.M. 2006. Supply chain management and performance. An Empirical Study. A working paper university of Malaysia. |

| [3] | Akoto, R.K., Awunyo-Vitor, D. and Angmor, P.L. 2013. Working capital management and profitability: Evidence from Ghanaian listed manufacturing firms. Journal of Economics and International Finance. 5(9), p.373. |

| [4] | Aliakbari, M., Banimahd, B., Talebnia, G. & Roodposhti, F. R. 2015. The Effect of Abnormal Operating Cash Flows on Unconditional Conservatism. International Journal of Academic Research in Accounting, Finance and Management Sciences. 5(1), 39–45. |

| [5] | Amagoh, F. 2008. Perspectives on organizational change: systems and complexity theories. The Innovation Journal: The public sector innovation journal. 13(3), pp.1-14. |

| [6] | Amedahe, F. K. 2002. Fundamentals of educational research methods. Cape Coast: University of Cape Coast Press. |

| [7] | Amuzu, M. S. 2010. Cash Flow Ratio as a Measure of Performance of Listed Companies in Emerging Economies: The Ghana Example. Unpublished Dissertation. St. Clements University Turks and Caicos Islands. |

| [8] | Andersson, J., Skoogh, A. and Johansson, B. 2011. Environmental activity based cost using discrete event simulation. In Proceedings of the Winter Simulation Conference. pp. 891-902. |

| [9] | Anene, E. C. 2014. What Difference Does Inventory Control Make In Typical Small Scale Farms’ Profitability? International Journal of Management Sciences and Business Research. 3(10), 1-4. |

| [10] | Appiah, P. 2014. Assessing the effects of inventory control management in mining companies in Ghana. Unpublished undergraduate project work, K.N.U.ST, Ghana. |

| [11] | Arora, A. and Ceccagnoli, M., 2006. Patent protection, complementary assets, and firms’ incentives for technology licensing. Management Science. 52 (2), pp.293-308. |

| [12] | Arrelid, D. and Backman, S. 2012. How to manage and improve inventory control: A study at AB Ph Nederman and Co for products with different demand patterns. |

| [13] | Augustine, A.N. and Agu, O.A. 2013. Effect of Inventory Management on Organisational Effectiveness in Nigeria. European Journal of Business and Management. 5, p.19. |

| [14] | Axsäter, S. 2015. Inventory control. Vancouver. Springer. Vol. 225. |

| [15] | Bai, L. and Zhong, Y., 2008. Improving Inventory Management in Small Business: A Case Study. |

| [16] | Bloomberg, D. J., Lemay, S. and Hanna, J. B. 2002. Logistics. New Jersey: Prentice Hall. |

| [17] | Bratland, E. and Hornbrinck, J. 2013. An empirical study of the relationship between working capital policies and stock performance in Sweden. |

| [18] | Carter, R. J. 2002. Purchasing and Supply Management, London: Pitman Publishing. |

| [19] | Chase, R.B., Aquilano, N. J., and Hayes, R. 1995. Production and Operations Management: Manufacturing and Services, Chicago, IL: Irwin. |

| [20] | Coase, R.H. 1937. The nature of the firm. Economica. 4 (16), pp.386-405. |

| [21] | Delhi: Prentice Hall of India. |

| [22] | Demsetz, H. 1983. The structure of ownership and the theory of the firm. The Journal of Law and Economics. 26 (2), pp.375-390. |

| [23] | Demsetz, H. and Lehn, K. 1985. The structure of corporate ownership: Causes and consequences. Journal of political economy. 93 (6), pp.1155-1177. |

| [24] | Dervitsiotis, K.N. 1981. Operations management. McGraw-Hill Companies. |

| [25] | Dick, M., Green, M.A. and Aydogan, G. 2008. Six Sigma Systems, Inc., System and Method for Collecting Revenue. U.S. Patent Application. 12/059,883. |

| [26] | Drurry, C. 2004. Management and Cost accounting. London: Prentice Hall. |

| [27] | Duhovnik, M. 2008. Improvements of the Cash-Flow Statement Control Function in Financial Reporting. Zb. rad. Ekon. fak. Rij. 26(1), 123-150. |

| [28] | Duru, A. N., Oleka, C. D. and Okpe, I. 2014. Inventory Management on the Profitability of Building Materials, Chemical, and Paint Companies in Nigeria. World Journal of Management and Behavioral Studies. 2(2), 21-27. |

| [29] | Eckert, S.G. 2007. Inventory management and its effects on customer satisfaction. Journal of Business and Public Policy (ISSN: 1936-9794). 1(3), p.1. |

| [30] | Eneje, C., Nweze, A. and Udeh, A. 2012. Effect of efficient inventory management on profitability: Evidence from selected brewery firms in Nigeria. International Journal of current Research. 4, pp.350-354. |

| [31] | Etale, L.M. and Bingilar, P.F. 2016. The Effect of Inventory Cost Management on Profitability: A Study of Listed Brewery Companies in Nigeria. International Journal of Economics, Commerce and Management. 4(6), pp.446-455. |

| [32] | Fama, E.F. and Jensen, M.C. 1983. Separation of ownership and control. The journal of law and Economics. 26 (2), pp.301-325. |

| [33] | Farah, M. and Nina, S. 2016. Factors Affecting Profitability of Small Medium Enterprises (SMEs) Firm Listed in Indonesia Stock Exchange. Journal of Economics, Business and Management. 4(2), 132-137. |

| [34] | Fariza, H., Nasaruddin, Z. M., and Ahmad, R. 2009. Development of an online image repository system for cardiac modelling. WSEAS Transactions on Information Science and Applications. 6 (1), pp.222-231. |

| [35] | Felmlee, D., Sprecher, S. and Bassin, E. 1990. The dissolution of intimate relationships: A hazard model. Social Psychology Quarterly. Pp.13-30. |

| [36] | Fosu, B.A. 2016. The Relationship between Inventory Management and Productivity in Ghanaian Manufacturing Industries. International Journal of Innovative Research and Development// ISSN. 2278–0211. 5(7). |

| [37] | Ghana stock exchange, 2017. Listed manufacturing firms in Ghana. Accessed 21th July 2017. |

| [38] | Gillham, B. 2000. Case study research methods. Bloomsbury Publishing. |

| [39] | Hashim, N. L., Mohd Ghouse, N. Z., and Ismail, N. 2012. A requirement model for managing inventory of raw materials. |

| [40] | Hassan, U.O., Mberia, H.K. and Muturi, W. 2017. Effect of working capital management on firm’ financial performance: A survey of water processing firms in Puntland. |

| [41] | Hendricks, K.B. and Singhal, V.R. 2005. An empirical analysis of the effect of supply chain disruptions on long‐run stock price performance and equity risk of the firm. Production and Operations management. 14 (1), pp.35-52. |

| [42] | Hennart, J.F. 1989. The transaction-cost rationale for countertrade. Journal of Law, Economics, and Organization. 5 (1), pp.127-153. |

| [43] | Inyang, F., Inyang, B. and Glory, B. 2013. Corporate profitability through effective management of materials, the case of flour mills company Lagos. European Journal of Business and Management. 5, p.29. |

| [44] | Jensen, M.C. and Meckling, W.H. 1976. Theory of the firm: Managerial behaviour, agency costs and ownership structure. Journal of financial economics. 3 (4), pp.305-360. |

| [45] | Jessop, B. 1999. Narrating the future of the national economy and the national state? Remarks on remapping regulation and reinventing governance. State/culture: State formation after the cultural turn. Pp.378-405. |

| [46] | Kabethi, J.M., Ng’ang’a, S.I., and Kiumbe, P.M. 2013. Technology adoption in rural areas for sustainable economic development. |

| [47] | Kariuki, J. N. 2013. An Assessment of the Factors Influencing Effectiveness of Inventory Control; Ministry of State for Provincial Administration and Internal Security, Nairobi – Kenya. International Journal of Business and Commerce. 3(1), 33-53. |

| [48] | Kazim, A., Liu, H.T. and Forges, P. 1999. Modelling of performance of PEM fuel cells with conventional and interdigitated flow fields. Journal of Applied Electrochemistry. 29 (12), pp.1409-1416. |

| [49] | Keth L, A Muhlemen, J Oakland. 1994. Production and Operations Management. London: Pitman Publisher. |

| [50] | Kontuš, E., 2014. Management of inventory in a company. Ekonomski Vjesnik/Econviews: Review of contemporary business, entrepreneurship and economic issues. 27 (2), pp.245-256. |

| [51] | Kootanaee, A. J., Nagendra, B. and Hamidreza, F. T. 2013. Just-in-Time Manufacturing System: From Introduction to Implement. International Journal of Economics, Business and Finance. 1(2), 07-25. |

| [52] | Kotler, P. 2002. Marketing Management, 2nd Edition, the Millennium Edition. New |

| [53] | Koumanakos, D.P. 2008. The effect of inventory management on firm performance. International journal of productivity and performance management. 57 (5), pp.355-369. |

| [54] | Krar, S.F. and Gill, A. 2003. Exploring advanced manufacturing technologies. Industrial Press Inc. |

| [55] | Kumar, R. 2016. Economic Order Quantity (EOQ) Model. Global Journal of Finance and Economic Management. 5(1), 1-5. |

| [56] | Liston, P., Byrne, J., Byrne, P.J. and Heavey, C., 2007. Contract costing in outsourcing enterprises: Exploring the benefits of discrete-event simulation. International Journal of Production Economics. 110(1), pp.97-114. |

| [57] | Lucey, T. 1992. Quantitative Techniques. 4th Edition. London: Ashford Colour Press. |

| [58] | Lwiki, T., Ojera, P.B., Mugend, N. and Wachira, V. 2013. The impact of inventory management practices on financial performance of sugar manufacturing firms in Kenya. International Journal of Business, Humanities and Technology. 3 (5), pp.75-85. |

| [59] | Machiuka, N. K. 2010. Growth strategies used by commercial banks in Kenya. Unpublished MBA research project, School of Business, University of Nairobi, Kenya. |

| [60] | Majed, A. M. K., Said, M. A. and Firas, N. D. 2012. The Relationship between the ROA, ROE and ROI Ratios with Jordanian Insurance Public Companies Market Share Prices. International Journal of Humanities and Social Science. 2(11), 115-120. |

| [61] | Maymand, M.M., Daraei, M.R. and Ekhtari, H. 2014. Providing a conceptual model for surveying the impact of employee empowerment on organizational citizenship behavior (ocb) in alborz insurance company. Journal of Current Research in Science. 2(6), p.794. |

| [62] | Mensah, J.M.K. 2015. Working Capital Management and Profitability of Firms: A Study of Listed Manufacturing Firms in Ghana. Browser Download This Paper. |

| [63] | Miller, M.H. and Modigliani, F. 1961. Dividend policy, growth, and the valuation of shares. The Journal of Business. 34(4), pp.411-433. |

| [64] | Monks J. G. 1996. Schaum’s Outline of Theory and problems of Operations Management, 2nd Edition. New York: McGraw Hill Inc. |

| [65] | Morris, C. 1995. Dynamic re-order point inventory control with lead time uncertainty: analysis and empirical investigation. International Journal of Production Research. |

| [66] | Munyao, R.M., Omulo, V.O., Mwithiga, M.W. and Chepkulei, B. 2015. ‘Role of Inventory Management Practices on Performance of Production Department, a Case of Manufacturing Firms. International Journal of Economics, Commerce and Management. 3(5), pp.1625-1656. |

| [67] | Muturi, H.M., Wachira, V. and Lyria, R.K., 2015. Effects of Inventory Conversion Period on Profitability of Tea Factories in Meru County, Kenya. International Journal of Economics, Commerce and Management. 3(10), pp.366-378. |

| [68] | Muya, T. W. and Gathogo, G. 2016. Effect of Working Capital Management on the Profitability of Manufacturing Firms in Nakuru Town, Kenya. International Journal of Economics, Commerce and Management. 4(4), 1082-1105. |

| [69] | Mwangi, L. 2016. The effect of inventory management on firm profitability and operating cash flows of Kenya Breweries Limited, beer distribution firms in Nairobi County. Doctoral dissertation, School of Business, University of Nairobi. |

| [70] | Mwangi, W. and Nyambura, M.T. 2015. The role of inventory management on performance of food processing companies: A case study of Crown foods Limited Kenya. European Journal of Business and Social Sciences. 4(04), pp.64-78. |

| [71] | Naliaka, V.W. and Namusonge, G.S. 2015. Role of inventory management on competitive advantage among manufacturing firms in Kenya: a case study of UNGA group limited. International Journal of Academic Research in Business and Social Sciences. 5(5), pp.87-104. |

| [72] | Niresh, J. A. and Velnampy, T. 2014. Firm Size and Profitability: A Study of Listed Manufacturing Firms in Sri Lanka. International Journal of Business and Management. 9(4), 57-64. |

| [73] | Nwanyanwu, L. A. 2015. Cash flow and Organizational Performance in Nigeria: Hospitality and Print Media Industries Perspectives. European Journal of Business, Economics and Accountancy. 3(3), 66-72. |

| [74] | Nwosu, H. E. 2014. Materials, Management and Firm's Profitability. The International Journal of Business and Management. 2(7), 80-93. |

| [75] | Obiri-Yeboah, H., Ackah, D. and Makafui, R. A. 2015. Assessing the Impact of Efficient Inventory Management in on Organization. International Journal of Advanced Research in Computer Science and Software Engineering. 5(8), 86-103. |

| [76] | Ogbadu, E. E. 2009. Profitability through Effective Management of Materials. Journal of Economics and International Finance. 1(4), 099-105. |

| [77] | Ogbo, A.I. and Ukpere, W.I. 2014. The impact of effective inventory control management on organisational performance: A study of 7up bottling company Nile mile Enugu, Nigeria. Mediterranean Journal of Social Sciences. 5(10), p.109. |

| [78] | Olufemi, A.J., Olaleke, O., Augusta, A., Maxwel, O, and Fred, I. 2016. Inventory control and performance of manufacturing firms in Nigeria. Journal of Engineering and Applied Sciences. 11(2), pp. 199-203. |

| [79] | Pandey I.M. 1995. Financial Management, 7th Edition. New Delhi: Vikas Publishing. |

| [80] | Panigrahi, A. K. 2013. Relationship between Inventory Management and Profitability: An Empirical Analysis of Indian Cement Companies. Asia Pacific Journal of Marketing and Management Review. 2 (7), 107-120. |

| [81] | Peterson, R. and Joyce, E. A. 2007. Decision Systems for Inventory Management and Production Planning. New York: John Wiley and Sons. |

| [82] | Predescu, I. 2008. The Influence of the Financial Factors on Cash Flow, As Determining Factor of Firm’s Investment Decisions. Romanian American University. |

| [83] | Prempeh, K.B. 2016. The impact of efficient inventory management on profitability: evidence from selected manufacturing firms in Ghana. International Journal of Finance and Accounting. 5 (1), pp.22-26. |

| [84] | Priyanka M. T. and Hemant R. T. 2015. Review of Inventory Management Strategies. International Journal of Advanced Research in Engineering, Science and Management. 1(1), 1-5. |

| [85] | Radzuan, K., Othman, A. A., Anuar, H. S., and Osman, W. N. 2014. Measuring the impact of inventory control practices: A conceptual framework. |

| [86] | Rashvand, A. and Tariverdi, Y. 2015. Effect of Working Capital Management on Operating Cash Flow. Journal of Applied Environmental and Biological Sciences. 5(11), 39-46. |

| [87] | Rasmusson, S. and Sunesson, B. 2010. Coordinated inventory control-A case study on its performance compared to the current system at IKEA. |

| [88] | Ravinder, H. and Misra, R.B. 2014. ABC analysis for inventory management: Bridging the gap between research and classroom. American Journal of Business Education. 7(3), p.257. |

| [89] | Salman, A. K. and Yazdanfar, D. 2012. Profitability in Swedish Micro Firms: A Quantile Regression Approach. International Business Research. 5(8), 94-106. |

| [90] | Schmitt, A.J. and Singh, M. 2009, December. Quantifying supply chain disruption risk using Monte Carlo and discrete-event simulation. In Winter Simulation Conference. pp. 1237-1248. |

| [91] | Schreibfeder, J. 2006. Inventory Management: Analyzing Inventory to Maximize Profitability. Effective Inventory Management, Inc. |

| [92] | Schroeder RG 2000. Operations Management- Contemporary Concepts and Cases. USA: International Edition. |

| [93] | Sevkli, M., Lenny Koh, S.C., Zaim, S., Demirbag, M. and Tatoglu, E. 2007. An application of data envelopment analytic hierarchy process for supplier selection: a case study of BEKO in Turkey. International Journal of Production Research. 45 (9), pp.1973-2003. |

| [94] | Shin, S., Ennis, K.L. and Spurlin, W.P. 2015. Effect of inventory management efficiency on profitability: Current evidence from the US manufacturing industry. Journal of Economics and Economic Education Research. 16(1), p.98. |

| [95] | Singhal, V.R. 2005. Excess inventory and long-term stock price performance. College of Management, Georgia Institute of Technology. |

| [96] | Sitienei, E. and Memba, F. 2015. The effect of inventory management on profitability of cement manufacturing companies in Kenya: A case study of listed cement manufacturing companies in Kenya. International journal of management and commerce innovations. 3 (2), pp.111-119. |

| [97] | Sprecher, S. and Bassin, E. 1990. The dissolution of intimate relationships: A hazard model. Social Psychology Quarterly. pp 13-30. |

| [98] | Stierwald, A. 2010. Determinants of Profitability: An Analysis of Large Australian Firms. Melbourne Institute Working Paper No. 3/10. |

| [99] | Teal, F. 1999. The Ghanaian manufacturing sector 1991–95: Firm growth, productivity and convergence. The Journal of Development Studies. 36(1), pp.109-127. |

| [100] | Telmoudi, A., Ziadi, J. and Noubbigh, H. 2010. Factors Determining Operating Cash Flow: Case of the Tunisian Commercial Companies. International Journal of Business and Management. 5(5), 188-200. |

| [101] | Thogori M. and Gathenya, J. 2014. Role of Inventory Management on Customer Satisfaction among the Manufacturing Firms in Kenya: A Case Study of Delmonte Kenya. International Journal of Academic Research in Business and Social Sciences. 4(1), 108 – 121. |

| [102] | Thorelli, H.B. 1986. Networks: Between markets and hierarchies. Strategic management journal. 7 (1), pp.37-51. |

| [103] | Tradegecko. 2017. Inventory control. Available at https://www.tradegecko.com/learning-centre/what-is-inventory-control [assessed 10 April 2017]. |

| [104] | Williamson, O.E. 1991. Comparative economic organization: The analysis of discrete structural alternatives. Administrative science quarterly. Pp.269-296. |

| [105] | Womack, J.P. and Jones, D.T. 2010. Lean thinking: banish waste and create wealth in your corporation. Simon and Schuster. Vancouver. |

| [106] | Yin, R.K., 2003. Case study research: Design and methods. Thousand Oaks. Sage. |

| [107] | Ziukov, S. 2015. A literature review on models of inventory management under uncertainty. Verslo Sistemos ir Ekonomika. 5(1). |

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTML

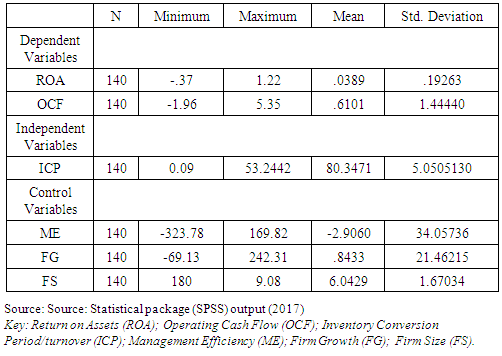

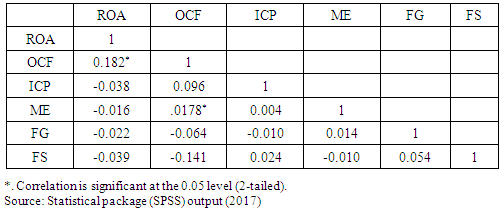

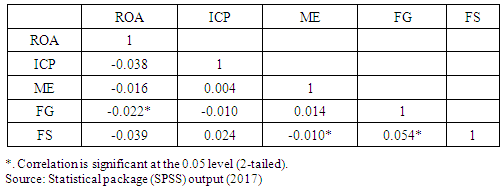

The results showed that there is a negative insignificant relationship between profitability and inventory conversion period, management efficiency and firm size. Profitability is positively related to firm growth of manufacturing firms. The R-squared value is 0.04, an indication that 4% of variation in return on assets is explained by the independent variables; inventory conversion period, management efficiency, firm growth and firm size. The calculated F statistics value of 0.120 shows that P-value 0.0178 < 0.05 and is insignificant at 5% level. Hence, the findings are observed to be conflicting to the second hypothesis and the study conclude that there is a negative insignificance relationship between inventory management and profitability of manufacturing firms in Ghana. Furthermore, Table 4.6 shows the results for the ordinary least squares using operating cash flow as a dependent variable.

The results showed that there is a negative insignificant relationship between profitability and inventory conversion period, management efficiency and firm size. Profitability is positively related to firm growth of manufacturing firms. The R-squared value is 0.04, an indication that 4% of variation in return on assets is explained by the independent variables; inventory conversion period, management efficiency, firm growth and firm size. The calculated F statistics value of 0.120 shows that P-value 0.0178 < 0.05 and is insignificant at 5% level. Hence, the findings are observed to be conflicting to the second hypothesis and the study conclude that there is a negative insignificance relationship between inventory management and profitability of manufacturing firms in Ghana. Furthermore, Table 4.6 shows the results for the ordinary least squares using operating cash flow as a dependent variable.

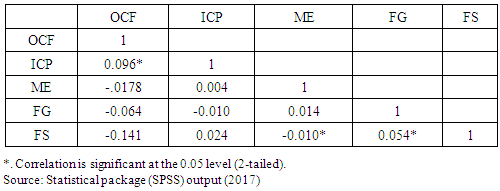

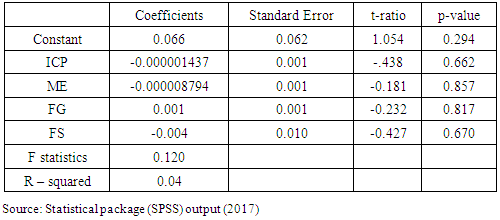

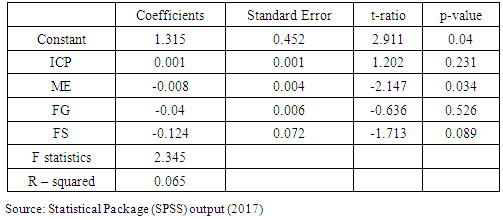

The results show that operating cash flow of manufacturing firms in Ghana have a relationship with inventory conversion period of manufacturing firms in Ghana. In addition, the results show a negative relationship between operating cash flow and management efficiency, firm growth and firm size. The resultant R-square value of 0.065 indicates that 6.5% of operating cash flow is explained by independent variables; inventory conversion period, management efficiency, firm growth and firm size. The calculated F statistics value of 2.345 shows an insignificance of P-value 0.006 < 0.05 at 5% level. Hence, the finding is also divergent from the third hypothesis and the study conclude that there is a negative relationship between inventory management and operating cash flow of manufacturing firms in Ghana.

The results show that operating cash flow of manufacturing firms in Ghana have a relationship with inventory conversion period of manufacturing firms in Ghana. In addition, the results show a negative relationship between operating cash flow and management efficiency, firm growth and firm size. The resultant R-square value of 0.065 indicates that 6.5% of operating cash flow is explained by independent variables; inventory conversion period, management efficiency, firm growth and firm size. The calculated F statistics value of 2.345 shows an insignificance of P-value 0.006 < 0.05 at 5% level. Hence, the finding is also divergent from the third hypothesis and the study conclude that there is a negative relationship between inventory management and operating cash flow of manufacturing firms in Ghana.