-

Paper Information

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2018; 7(3): 76-81

doi:10.5923/j.ijfa.20180703.03

Good Corporate Governance; Evidence from Fijian Listed Entities

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLVishwa H. Prasad1, Kieran James2

1College of Business, Hospitality and Tourism Studies, Fiji National University, Lautoka Campus, Fiji Islands

2Senior Lecturer in Accounting, University of the West of Scotland, Paisley Campus, Paisley, Scotland

Correspondence to: Vishwa H. Prasad, College of Business, Hospitality and Tourism Studies, Fiji National University, Lautoka Campus, Fiji Islands.

| Email: |  |

Copyright © 2018 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Good Corporate Governance is the process of how the companies are directed and controlled. In Today’s market- based economy, corporations make a significant contribution to the gross domestic product. Good corporate governance means that corporations are run in the best interest of the members and the other stakeholders. Therefore, Good Corporate Governance has become an integral requirement in today’s fast changing, competitive and global economy. The scandals and failure of big corporate giants such as Enron, Arthur Anderson, Worldcom and HIH to name a few, calls for Accounting discipline to hold liability. The applicable Accounting standards including International financial reporting standards and the way accounting is practiced may open doors for corrupted Accountants. This paper examines corporate governance from an accounting perspective and suggests ways on how corporation’s valuable assets and corporate image can be protected by applying the best accounting practices and recommendations from capital markets unit of Reserve Bank of Fiji on good corporate governance. This paper uses a content analysis approach and examines the corporate governance practices from the annual reports of listed companies in Fiji.

Keywords: Good Corporate Governance, Corporate failure, Compliance, Accountability

Cite this paper: Vishwa H. Prasad, Kieran James, Good Corporate Governance; Evidence from Fijian Listed Entities, International Journal of Finance and Accounting , Vol. 7 No. 3, 2018, pp. 76-81. doi: 10.5923/j.ijfa.20180703.03.

Article Outline

1. Introduction

- In simple terms, governance is the way in which companies are directed and controlled. Good corporate governance (GCG) in companies maximizes the value of the shareholders legally, ethically and sustainably, while ensuring equity and transparency to every stakeholder – the company’s customers, employees, investors, suppliers, and the government Murthy, 2012). GCG is mandatory for ensuring the required values to different stakeholder groups. It increases the productivity of the corporations, by creating a business environment that sets an incentive for Accountants to maximize returns on investment, earnings per share Companies may attract best talents internationally, and Good corporate governance will create fairness, transparency and accountability in business activities among its board, management and employees (Oman, 2001).Many companies and policy makers are giving a lot of priority in embracing superior corporate governance techniques in their organizational structure within both managerial and financial; however, many stakeholders still hold the question whether good corporate governance is sufficient to lead an organization into better performance. Better stock trading is highly connected to the economic performance but, in today’s world financial results are increasingly considered together with social and environmental ones, in an integrated way and by the market players too. Sustainable value creation is a source of global competitive advantage for Corporates and sustainable companies have the same governance spirit, regardless of countries’ specific corporate governance rules and structures (Salvioni D.M., et.al, 2016).The separation of ownership and control in public corporations do impact corporate governance. This gives rise to agency problem. (Jenson and Meckling, 1976) The responsibility for control is vested in the board and management, the shareholder’s agents. The board appoints management (as their agents) led by the chief executive officer to manage the organization. When conflicts occur between managements goal (for example, job security or workers compensation) and the shareholders goal (increased value), management should do what is right for the company and its owners. Chances of conflicts in differing goals can be reduced by providing senior management share in the companies they run.It is believed that if the managers are also the owners, their interests would be more aligned with other shareholders interest and they will be less inclined to pursue activities which have a negative impact on the share price. Accounting is a process of compiling information for reporting the internal affairs of any entity to different stakeholders at the end of a certain interval (Steve, 2008). The International financial reporting standards greatly impact the accounting practices and the need arises to harmonise and align the different perceptions of the interested parties.Fiji has small size and small number of companies listed compared to other capital markets, and the flexibility provided by the principle-based approach will minimise compliance costs, as well as, encourage companies to adopt the spirit of the principles/code. (Reddy K., & Sharma, U. (2011). The principle-based approach requires companies to either, comply with the set Corporate Governance guidelines or, explain if deviating from those set guidelines. Therefore, it was assumed that the, “comply or explain” approach would ultimately lead to improved corporate governance practices in Fiji.

2. Methodology

- This study aims to investigate Good Corporate Governance f for firms listed on the South Pacific Stock Exchange (SPSE). Accordingly, this paper uses a content analysis approach and the data for this study was obtained from the South Pacific Stock exchange (SPSE- Website) and from the 2012-2016 annual reports of the companies listed in Fiji.Reference would also be made to secondary sources like published and unpublished scholarly papers, research articles, text books, international journals and websites.Accounting can be used as a valuable tool to enhance GCG. Therefore, the objective of this paper is to find out to what extend the Public Companies comply with corporate governance principles in Fiji.

3. Literature Review

- Corporate governance is defined as a “set of mechanisms that influence the decisions made by managers when there is a separation of ownership and control” (Larcker et.al 2007 p 1). This means that corporate governance focuses on mechanisms that involve operating the organization in an efficient and effective manner. Prior studies show that corporate value is enhanced through effective governance (Agrawal and Williamson 2006). Very often, the financial reports (accounting figures) are used by the shareholders to measure the performance of the governing bodies. The performance appraisal and rewards of the managers are dependent on the accounting numbers (Watts and Zimmerman, 1978, 1986; Healy, 1985; Sloan, 1993). Hence, corporate governance is required to ensure that the financial statements present a true and fair view.Prior academic research on the relationship between corporate governance practices and the integrity and reliability of corporate financial reporting by Uzun et.al (2004) find that firms with boards comprised of more outside and independent directors are less likely to commit fraud but find no significant effects for board size, frequency of board meetings of frequency of audit committee meetings. Agrawal and Chadha (2005) in their analysis on the relationship between governance characteristics and the probability of earnings restatements find no significant impact of board independence nor audit committee independence on the probability of restatement. It has been shown in prior research that the firm value is positively associated with corporate governance (Klapper and Love, 2004). Better protection of minority shareholders will also lead to increase in firm value (La Porta et.al, 2002). Firm value and earnings quality also increase with stronger governance mechanisms. (Bebchuk et.al, 2004). Iyengar et.al (2010) examined corporate governance mechanisms using ordinary least squares regression for a sample of 3551 firm- year observations in US and documented how certain governance mechanisms and managers at-risk pay affect the quality of reported earnings. They found that earnings quality is higher for firms where managerial at-risk pay is low as a proportion of total pay and established managerial retirement policy has a positive association with earnings quality.Good governance means that institutions develop processes which produce results that meet the needs of society while making the best use of resources at their disposal. The concept of efficiency in the context of good governance also covers the sustainable use of natural resources and the protection of the environment (Regina & Ukadike, 2011). The system of corporate governance addresses the multiple relationships between the participants in a corporation; in particular the management, board of directors, and shareholders of a company but also involving further stakeholders such as customers, employees or suppliers. Corporate governance allocates rights to the different groups of stakeholders but also imposes responsibilities and duties on these stakeholders. Corporate governance is not however limited to this interrelationship of corporate participants. It also provides structures for corporate procedures and operations. Moreover, corporate governance establishes a framework for the processes of decision-making and for the pursuance of corporate goals (Regina & Ukadike, 2011).Nowadays corporate governance comprises further relevant elements including business ethics and corporate social responsibility. Business ethics incorporate moral behaviour and thinking into business operations and corporate social responsibility emphasises the relevance of corporate awareness of environmental and social concerns in the setting in which the company operates. The importance of these factors is heightened by the fact that corporate success does not only depend on the positioning of a company but also on the corporation's performance within its setting (Hirsch et. al 2011).Soobaroyen and Mahadeo, (2012), examined how the expectations and requirements of corporate governance code impact accountability practiced by company board members in Mauritius. The study reveals a substantive change in the type of board accountability and a move to a more empowered maximalist board. In order to be successful, any corporate governance system also requires supporting and enforcing institutions and a legal framework which may consist of legislation, self-regulation measures and codes of conduct (Hirsch & Ukadike, 2011). Traditionally, corporate governance has evolved around the contract theory and agency problem based on separation of ownership and management. So, all standard texts, review and research papers and business committee reports base their arguments around agency problem only. The company/corporate law across the jurisdictions laid down the basic governing relation between owner and managers, whereas other relations like moral and beneficiary, economic and succession were left to mutual understanding between owners and managers. So, the objective of theory building was to strengthen the protection of interests of shareholders and other stakeholders against the management supremacy. (Indrajit, 2011).Wahab-Abdul, E.A., et.al (2007), studied on the impact of the Malaysian Code on Corporate Governance and find that firms with good governance practices perform significantly better then poorly governed firms. They also found that politically connected firms have weaker governance in place than politically independent firms. The authors also studied whether ethnicity was a significant factor for performance but they found that it was not.Over the years, theoretical boundaries of the corporate governance have expanded on the issues like relationship management between the different constituents of corporate. So, the objective of corporate governance not only laid the protection of interest of shareholders but towards economic and social prosperity (Indrajit, 2011). Over the last decade, there have been numerous frauds discovered in companies throughout the world. These frauds include Enron, Worldcom, Cendant, Adelphia, Parmalat, Vivendi, and SK Global. In most cases, it was alleged that the auditors should have detected the frauds and, as a result, they were sued for performing negligent audits. In order to determine whether auditors should be held liable for fraud, it is important to review why these large scale frauds occurred and the legislation and rules that have been instituted since their occurrence. (Steve, 2008).Disclosure and transparency requirements are often set by policy makers but is enforced by the regulatory actions and members rights come from a combination of regulations, where shareholders set demand for their rights in a corporation. (Samra, 2016).

4. Features of Good Corporate Governance

- Corporate governance comprises a set of relationships between an organisations management, its board of directors, its members (shareholders) and other interested parties. Good corporate governance is a structure with policies and processes through with the objectives of an organisation are established, attained and monitored. Good corporate governance is an important attribute within an organisation, therefore, effective implementation of good governance leads to continuous improvement of strategy, performance, compliance and accountability (Corporate Governance Handbook). Corporates need to monitor and evaluate their corporate governance framework and integrate strategic business plans, risk management plans, marketing plans, code of conduct, occupational health and safety and policies and manuals.In the changing global business, the critical elements of good governance are clear strategy setting, risk management, financial planning and budget and human resource planning. The tone set by the board of Directors has a major influence on the integrity and ethics in the organisation. For example, a code of conduct should be developed in consultation with the board, staff and management.It is very important to establish financial goals and a system needs to be devised to monitor and report on variances. There needs to be a very clear and documented procedures on the job description of each accounting staff and should be clearly communicated to them. The board members, especially the chairman should identify the right mix of skills and independence required by each committee. The skills need to cover functional areas of finance, production, marketing, engineering and legal aspects. The rules and regulations of corporations need compliance. Corporates also need to comply with the taxation regulations. Thus a company need to respond in a timely manner to all queries by the Fiji Revenue and Customs Authority. There is also a need to comply with the code of conduct and prevent any fraud from happening. GCG policies should at a minimum cover ethical behaviour, corporate social responsibility, financial management, fraud control, occupational health and safety and risk management. Lastly, Accountability in financial reporting must ensure implementation of business processes and to provide relevant and reliable information to the board of Directors and management on a timely manner. Financial reporting should cover both the actual and budgeted targets and it needs to be comprehensive to ensure that the board members are well informed. The key issues, risk management recommendations as well as graphic representations aid in effective communication. For large corporations, risk committees or an audit committee would be very useful for consideration of risk and audit issues.

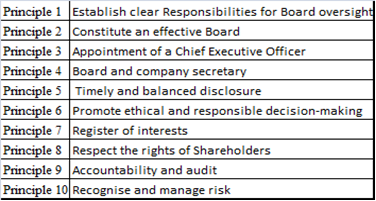

5. Role of Reserve Bank of Fiji and South Pacific Stock Exchange

- The Table 1 below lists the 10 principles provided by the capital markets unit of the reserve bank of Fiji (RBF).

|

6. Results and Recommendations

- For the Financial year ending 2012, the financial reports of nine (9) companies clearly identify the corporate governance principles and guidelines provided by the capital markets unit of RBF. They also have a separate content page for corporate governance. It is interesting to note that three (3) companies do not identify separately the corporate governance principles. However they do have directors report. In Comparison, the financial reports of (11) companies clearly identify the corporate governance principles and guidelines for the financial year 2013. This shows that compliance is greater in the year 2013. For the financial years, 2014-2016, all companies comply with the corporate governance principles The Directors report of 2015-2016 reveal for all companies listed, that they place greater emphasis on the governance structure of the company.In a nutshell, annual reports of listed companies have not clearly identified executive and non- executive directors. The board’s sub- committees are clearly identified for seven (7) companies for the financial year 2012 and for nine (9) companies for the year 2013 & 2014. However, there was improvement in 2015-2016, where (10) identified boards sub- committees, for example audit committee, risk committee and finance committee. However, again limited information is provided on whether the directors are executive or non executive on each of the committees for all the years studied.The lack of disclosure of each committee’s composition of directors may also create inconsistent reporting. The Asian Development Bank believes that the development of effective capital markets, partly through good accounting, is a most important way of promoting growth in the emerging economies (Chand, 2002).The “comply or explain” approach by SPSE is principle-based and whether this approach leads to improved corporate governance in Fiji is questionable. Financial reports of 92% of the companies listed show that they are committed to the recommendations by RBF (table 1) However, compliance does not does necessarily mean that the financial performance would be increased or profits would be higher in the next reporting period.It is also interesting to note that there has been very slight change in the number of listings on the SPSE. It can be simply said that Fiji’s capital market is quite small and comprehensive corporate governance studies could be difficult to embark upon.Some of the reasons may be that most investors in Fiji are risk averse. These investors may feel more secure to get a fixed rate of interest from bank deposits. There is also lack of investor education in Fiji. For example, most ordinary citizens of the country may not know that dividend income is exempted from tax while tax needs to be paid on interests earned from the financial institutions. Thus lack of understanding of the legislations and the listing rules may also hinder investments in capital markets. The directors’ reports of listed companies in Fiji clearly show that there are a high proportion of institutional investors. Therefore it can be concluded that minority investors are not protected fully under current legislation.Accounting Academics can play a vital and important role at enhancing market efficiency through research. In competitive business environment, the board, management, Accountants, auditors and Professional Accounting bodies need to work in harmony for a sound financial reporting process (European Commission, 2002). Greater transparency also stems from greater recognition and disclosure requirements, i.e. listing rules of SPSE. An entity’s financial performance has an impact on the wealth of its board member’s. An increase in profit would mean more perks are available to the board members. However, top management’s influence over the composition of the board may be a hurdle to effective governance.It’s greatly recommended that there should be mandatory rotation of auditors and the chief executive officer of the company should be prohibited from acting as the chairman of the board or be involved in the nomination of directors. There is also a need to establish continuing education requirement for board members so that they are better informed of the changing technologies and changes in the nature of the business.Therefore, in addressing problems that have been largely blamed on accounting quality and auditing by media, government or other stakeholders, we must first address the limitations of corporate governance.

7. Accounting for and Promoting Good Corporate Governance

- Accounting and auditing are only components of the broader system of corporate governance and cant be “fixed” in any lasting way without substantive changes in the overall governance process (Imhoff, 2003). The work of Accountants is very integral to effective governance in relation to its traditional focus on financial performance and accounting integrity (ACCA, 2008). One of the most important roles of an Accountant is to provide transparency in financial reporting to the members and other stakeholders. In order to maintain professional integrity, Accountants must follow accounting standards and do not let bias or prejudice to override their decisions. It is important to note that the accountants bring their knowledge on the financial reporting standards to the clients to drive through best practice. The board needs to ensure the integrity of the company’s financial reporting system. Independent audit committees and controls need to be present in every aspect of the accounting process. The high profile scandals and rising investor dissatisfaction with governance practices have led to demands to ‘raise the baseline’ of mandatory disclosure and compliance by corporations (Shil, 2008). The Sarbanes- Oxley act was developed in response to failure of giant corporations like Enron and world com in U.S. This law imposes a number of corporate governance rules on all public companies with stock traded in the United States.Good corporate governance practices are increasingly important in determining the cost of capital in a global market. Good corporate governance encourages companies to create value and maximize the wealth for the shareholders. Corporate governance influences how the objectives of a company are set and achieved, how risk is monitored and assessed and how performance is increased. Fijian companies must be equipped to compete globally and maintain investor confidence both locally and internationally.A commitment to good corporate governance in terms of well-defined shareholder rights, high levels of transparency and disclosure, an empowered board of directors etc. make a company more profitable and attractive to investors and lenders. (Black.et.al, 2006). Well governed companies benefit from higher prices for their shares, have access to cheaper debt and just perform better than their poorly governed peers. Firms with transparent and professional systems of direction and control are also more likely to understand the importance of taking social and environmental considerations seriously and mainstreaming them into their operations (Shil, 2008).

8. Conclusions

- The aim of corporate governance must be to increase a corporation's efficiency and economic growth and, moreover, the confidence of investors including shareholders in the corporation. Therefore, companies that have established good corporate governance practices can enhance their corporate value on a long term basis and thus be more competitive in helping to raise social wealth. Few ways highlighted in the paper in which corporate governance can be improved are having access to clear information, more specific details on strategies are given and accurate disclosure of information concerning remuneration of Directors and top management.The board of directors, owners and managers need to realise that they and their employees should start considering the interest of the stakeholders, not just the shareholders. Recent corporate failures of giant companies internationally have pointed out the need for substantive improvements in the corporate governance principles.Therefore, corporate governance plays a very vital and key role in enhancing an organisational performance and sustainable development. In future, researchers may like to examine how Institutions like World Bank, Asian Development Bank, may influence corporate governance practices and structures. Research could also explore non- listed companies in Fiji. Our research informs Fijian Executives, regulators and policy makers who may be interested in evaluating the practices of listed companies based on past reforms and regulations.