-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2018; 7(3): 57-66

doi:10.5923/j.ijfa.20180703.01

Verifying High School Accounting Curriculum Objectives: An Indirect Assessment of Students Learning Experiences, Outcomes and Gaps

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLNasiru Inusah , Joseph Yaw Dwommor

Department of Accounting Studies Education, University of Education, Winneba, Ghana

Correspondence to: Nasiru Inusah , Department of Accounting Studies Education, University of Education, Winneba, Ghana.

| Email: |  |

Copyright © 2018 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

The assessment of educational plans and outcomes for verification and validation purposes is an integral part of the teaching and learning process in accounting education. This study is an outcome verification study which seeks to find out the extent to which high school accounting module content, learning materials and learning objectives are encountered by graduates of Ghanaian Senior High School (SHS) accounting curriculum. The target population consist of all High School who completed the high school accounting curriculum in 2015. Out of this, those who gained admission into the BSc. Accounting Education program of the University of Education, Winneba, in 2015 is the sample of this study. The instruments used for collecting data is questionnaire on students’ ability to perform the tasks embedded in the SHS accounting curriculum learning objectives. The findings indicate that on average three-quarters of the learning objectives are attained by SHS accounting graduates. It is established that majority of the students have learning gaps in ‘Information Technology in Accounting’, ‘Accounting for VAT’, ‘Public Sector Accounting’, ‘Company Accounts’, ‘Accounting Ratios’, and ‘Cash Flow Statement’ content areas. The learning outcomes (attained learning or learning gap) are independent of gender of students. It is found that these content areas are rarely taught in schools and this is most probably because these topics are hardly examined by examination bodies. The findings show that teachers rarely recommend the suggested learning materials to their students and hence most of the students rarely use the suggested learning materials. This may be due to unavailability of the recommended learning materials. It is recommended that policy makers should ensure access to recommended reading materials and other requisite learning materials and examination bodies should spread their test items to cover the content areas identified to be a learning gap.

Keywords: Accounting Curriculum, Learning Gap, Learning Outcomes, Indirect Assessment

Cite this paper: Nasiru Inusah , Joseph Yaw Dwommor , Verifying High School Accounting Curriculum Objectives: An Indirect Assessment of Students Learning Experiences, Outcomes and Gaps, International Journal of Finance and Accounting , Vol. 7 No. 3, 2018, pp. 57-66. doi: 10.5923/j.ijfa.20180703.01.

Article Outline

1. Introduction

- In Ghana, potential accounting academics and professionals encounter accounting as a field of study and career path for the first time at the Senior High School (SHS) level where financial accounting is one of the modules of the SHS Business Program. Accounting competencies acquired by students at the SHS level is therefore the foundation for their professional and academic advancement in accounting education and training. Effective implementation of innovative changes in the SHS accounting curriculum is consequently crucial to accounting education at all levels in Ghana. A continuous monitoring and control of the SHS accounting module is necessary for two main reasons: (1) innovative changes to ensure that the curriculum is up to date - provides the necessary accounting experiences and competencies (2) effective implementation of the curriculum to ensure that the graduates of the accounting module acquire the intended competencies. However, effective monitoring and control of the implementation of the SHS accounting module require reliable and relevant information of which assessment and evaluation are the tools. The evaluation of educational plans and assessment of learning outcomes are critical and of great interest to accounting educators (Calderon, Green, & Harkness, 2004 [8]). B. D. Gannod, Gannod, and Henderson (2005 [14]) observed that continuous improvement of an educational system requires verification and validation of the curriculum involve. Verification of a curriculum is about answering the question “are students learning outcomes as intended?” and validation is about answering the question “are the intended learning outcomes appropriate?” (Gannod et al, 2005 [14]). Thus, verification is the assessment of students learning outcomes. According to (Coles, 2006 [9]), depending on the tool of assessment, assessment of learning outcomes may involve measuring the extent of achievement of all module learning objectives or measuring the level of achievement of a fraction of the course learning objectives.Generally, students learning outcomes of the SHS accounting module in Ghana are assess and evaluated using end of course exams conducted by West African Examination Council (WAEC). The purpose of this form of assessment is usually to measure students learning for certification and usually provide little information for addressing issues of effectiveness of curriculum strategy or determining the level of achievement of the module learning objectives (Porter and Smithson, 2001 [27]). Besides, such form of assessment usually do not cover all the learning objectives of the curriculum, and lack details that links the student exams performance to specific intended learning objectives. However, linking student learning outcomes to learning objectives provide vital information to support monitoring, and control for innovative change in the module goals, content and implementation strategies. In this context, Porter and Smithson (2001 [27]) asserted that to be useful for monitoring and control, indicator measures of the learned curriculum should describe the content that has been learned as well as the level of proficiency of the learner embedded in the test score. They also opined that the assessed student learning outcomes should be capable of being mapped to the intended curriculum to provide information on which aspect of the intended curriculum is achieved by most learners and which aspects require much attention. A plethora of research exist on students learning outcomes in accounting education as measured by the end of course exams or test, especially the issue of poor performance in exams or test and how to improve students’ performance in exams (see Ganyaupfu, 2013 [15]; Hoves et el, 2011 [20]; Lynn & Robinson-Backmon, 2006 [22]). Few studies exist on the assessment of the level of achievement of accounting modules learning objectives and competencies neither to talk of other related issues such as how to improve the level of achievement of specific learning objectives of a module in accounting education. The few studies on achievement of accounting education objectives are on achievement of accounting program objectives and not on accounting as a module or subject (see Hill, Perry, & Stein, 1998 [19]; Stivers et al., 2000 [32]). Besides, the existing studies focus on the overall success of the accounting program with no emphasis on achievements of specified knowledge, skills, attitudes and performance of specific task embedded in the goals and objectives of an accounting curriculum. Since the end of course exams and test approach used in assessing the SHS accounting curriculum learning outcomes is purposely for grading students, a holistic assessment of the extent of achievement of all the learning objectives is necessary to find answers to questions such as “What proportion of learning objectives is achieved by majority of students?” “Which learning objectives are not achieved by majority of student?” “Which content areas are rarely taught in schools?” Answers to these questions is necessary for strategic management of students learning in accounting education at the SHS level and for further research in accounting education.To serve as a humble contribution to the literature on students learning achievements in accounting education in general and accounting education at Senior High School in Ghana in particular, this paper assesses the extent to which students encounter the content, materials and attain the learning objectives of Senior High School accounting module.

1.1. Research Questions of the Study

- 1. To what extent do students encounter the suggested content and learning materials of the SHS accounting module?2. What proportion of the SHS accounting model learning objectives constitute attained learning and learning gap to majority of the students? 3. Which of the SHS accounting module content areas and learning objectives constitute leaning gaps to majority of the students?4. Does gender have any association with SHS accounting students’ learning outcomes?

2. Learning Objectives, Outcomes, and Related Terms

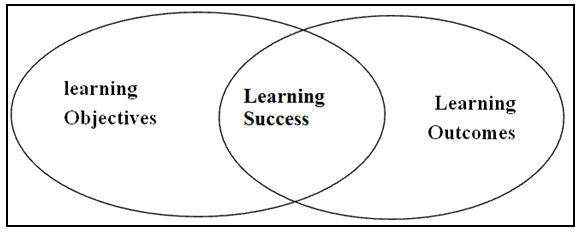

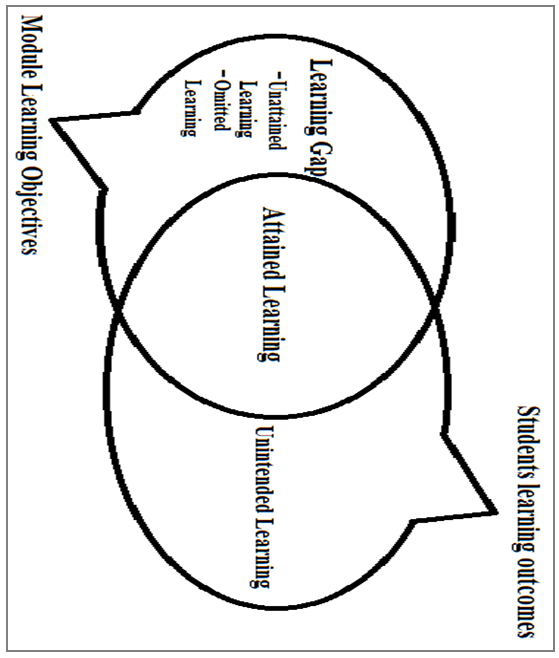

- Learning is an intangible concept and can best be described as a variable in terms of meaning. Merriam and Caffarella (1999 [24]), from the constructivist point of view, asserted that learning is how people make sense of their experience through reflection. Kolb (1984 [21]) conceived learning as a process grounded in experience and tested out of experience. According to Adamson, Becerro, Cullen, González-Vega, Sobrino, & Ryan (2010 [2]), learning is a process by which a sustainable change in learners’ knowledge, skill, attitude or competence occurs. This definition is quite suitable in the context of this paper.Students’ learning may be described as a learning outcome when it occur, a learning achievement when it is measured, a learning objective when it is in a learning plan, or learning success when it is viewed as an intersection of learning outcome and learning objective (Adamson et al, 2010 [2]; Euler and Hahn, 2004 [12]; European Centre for the Development of Vocational Training [CEDEFOP], 2010 [13]). Learning outcomes in the context of education and training, as defined by EQF 7, are “……. statements of what a learner knows, understands and is able to do on completion of a learning process, which are defined as knowledge, skills and competences” (European Parliament and Council of the EU, 2008, Annex I). Major variations in the understanding, use and interpretation of learning outcomes and related terminologies however exist in the literature and a comprehensive conceptualization of learning outcomes and the related concepts is crucial for curving a framework for this study. CEDEFOP (2010 [13]) observed that depending on the level and context in which learning outcomes are defined, they may fulfill different functions such as recognition of prior learning, award of credit, quality indicator, learning plans, key competences for life, credibility for employers and for modernizing the governance of education and training. Learning outcomes is most often confused with (considered synonymous) to concepts such as competency, learning objectives, learning output and others (CEDEFOP, 2010 [13]). Whiles competency is a context based learning outcome, learning outcomes are more comprehensive and encompasses competences and other non-contextual outcomes (Markowitsch & Luomi-Messerer, 2008 [23]). Regarding the link between learning outcomes and learning objectives, Adam (2004 [1]) maintains that learning outcomes are the achievements of the learner rather than the intentions of a curriculum package, course, a teacher or a program and that learning outcomes might encompass unintended learning outcomes as well. Learning objectives are learning outcomes prescribed before the beginning of the learning process and are learning outcomes expected of learners (CEDEFOP, 2010 [13]). In the same vein, Adamson et al (2010 [2]) described three types of learning outcomes: intended learning outcomes, expected learning outcomes, or actual learning outcomes. According to them, intended learning outcomes refer to the educational and instructional goals and objectives of a curriculum or a teacher that learners are to attain. Adamson et al (2010 [2]) observed that if the curriculum is effective and its goals achieved, the actual learning outcomes must meet at least the minimum intended learning outcomes requirements and that the actual learning outcomes may include additional outcomes which were unintended. They described expected learning outcomes as the amount of learning expected to be achieved before a particular qualification is earned and they indicated that expected learning outcomes are usually the concern of qualifications frameworks and professional standards. Euler and Hahn (2004 [12]), in their conceptualization of learning outcome as a concept, distinguished between learning outcomes, learning objectives and learning success. They described learning objectives as the knowledge, skills and competences the teacher expects learners to attain after going through the learning process. Learning outcomes on the other hand are described as all competences, knowledge and skills attained by the learner through the learning process whether intended or not. They termed the achieved learning objectives as learning success. Figure 1 below shows Euler and Hahn (2004 [12]) conceptual model of the concept of learning objectives and learning outcomes.

| Figure 1. Difference between Learning Objectives, Learning Outcomes and Learning Success (Adopted from Cedefop, 2010 p. 25) |

| Figure 2. The Framework of Learning Objectives, Learning Outcomes and Related Concepts |

2.1. Methods of Verifying Learning Outcomes

- According to Gentry et al (1998 [16]), measuring learning achievement is a necessary complement of the process of learning. Stake holders of the learning process will want to know if learners are actually learning or have actually learned what was intended or expected and hence determine the effectiveness of the strategies implemented. Gannod et al, (2005 [14]) identified two main purpose of assessment. They noted that the assessment of students’ actual learning experiences serve the purpose of curriculum verification. On the other hand they stated that skills gaps assessment and needs assessment for identification of the required and demanded outcomes of a learning process serves the purpose of curriculum validation.Students learning is mostly measured through direct assessment but could also be measured through indirect assessment. Gentry et al (1998 [16]) described learning measured through direct assessment as objective learning and learning measured using indirect assessment is perceived learning. Allen (2004 [4]), in the same vein, asserted that direct measures of learning assess actual learning and the indirect methods assess perception of learning. Objective learning as an indicator of students learning is reliable but lacks details whiles perceived learning as an indicator of students learning is less reliable but with variety of details to support monitoring and control (Allen, 2004 [4]; Alberta Education, 2011 [3]). Direct assessment or measurement of learning outcomes assesses students’ level of mastery of content or skills and the indirect assessment of learning outcomes assesses students’ perceptions of their own learning experience and achievement (Price & Rardall, 2008 [28]). Direct assessment of student learning provide visible evidence exactly what students have learned (Suskie, 2009 [33]). Indirect assessment of students learning is student self-assessment of their learning achievement. Andrade and Du (2007 [5]) indicated that during self-assessment students are engage in reflecting on the quality of learning and the extent to which the learning reflects clearly stated objectives. Self- reported measures of student learning assume that students’ perception of the extent to which they achieved a course objective is indicative of students’ actual learning achievement. Rose (2006 [30]) observed that teachers and for that matter stakeholders in educational assessment doubt the value and accuracy of self-assessment despite its widespread use both for classroom evaluation and research. Rose asserted that the weakness of self-assessment can be enhanced though training of students on self-assessment. Allen (2004 [4]) questioned the construct validity of indirect measures as indicators of student learning and describes them as inaccurate in indicating students learning. Calderon (2013 [8]) concluded from his findings that students perceived learning may not actually reflect their ability to demonstrate mastery of content and skills but a separate construct reflecting student’s satisfaction with their experience in the learning process. Despite the criticism against perceived learning as an indicator of learning, it is commonly used in the literature as the indicator of students learning (Beaumie, Williams & Dattilo, 2000 [6]). Duke, (2002 [11]; Gosen & Washbush, 1999 [19]; Rocha, 2000 [30]) noted that one of the techniques of assessing institution-specific learning outcomes is assessment of the perceptions of a critical stakeholder group and there is arguably no critical stakeholder in students learning than the students.The proponents of the indirect measures of students learning argue that self-assessment provide some benefits that direct assessment is unable to provide. Opportunity for students to reflect on their learning, more detail learning achievement information, students learning that is directly linked to curriculum and learning objectives are among some of the identified benefits of students’ self-assessment (Alberta Education, 2011 [3]; Spiller, 2012 [31]) observed that self-assessment fits the current shift from focus on teacher performance to an emphasis on student learning. Stivers et al. (2000 [32]) indicated that the indirect measures such as surveys of students’ perception of their learning and students self-assessment enable academic institutions and managers to collect data related to specific aspects intended learning outcomes. Similarly, Hill et al. (1998 [19]) asserts that students self-assessment of their learning is useful in determining whether students actually learned the skills they were exposed to.Surveys of student perceptions of their learning achievement, according to (Glynn et al., 1993 [17]) have a degree of validity because graduates of a program are assumed to have a reasonable comprehension of the program. Sutton (2005), cited in Alberta Education (2011 [3]), argued that learners are those who know what they know, and what they don’t know. Graduates should not dependent on others to know the level of competency they have attained in the learning process (Costa & Kallack, 2003 [10]). Hill et al., (1998 [19]) observed that students are in a unique position to assess their measure and evaluate their own skills.

3. Research Methodology

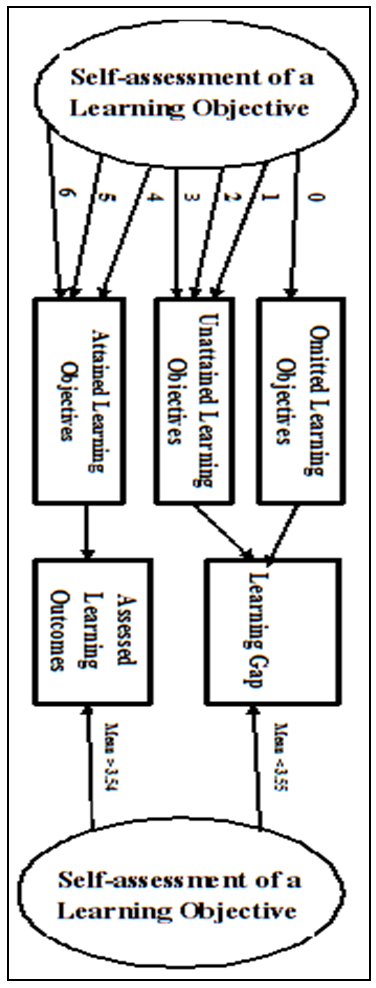

- This study is a curriculum verification study that seeks to verify students’ knowledge, skills and competency to make judgment on whether course content is delivered and course objectives are achieved. Descriptive design is a more suitable research design in this case. Thus, in terms of design this study is a descriptive study executed through the survey approach. Descriptive Studies observe the current state of a situation and report accordingly (Olds, Moskal, & Miller, 2005 [26]). Olds, Moskal, and Miller (2005 [26]) indicated that current studies on measurement and evaluation of learning outcomes are descriptive or experimental in design. The population of the study is all SHS graduates in the year 2015 who studied financial accounting and gained admission into the Universities to pursue advance studies in accounting. However, for this study all SHS graduates who graduated in 2015 and were admitted to pursue a BSc. Accounting Education program of the University of Education, Winneba, in Ghana for the 2015/ 2016 academic year, were selected.A self-assessment survey items was designed and administered to the sample of the study. The survey asked respondents to indicate the extent to which they are able to perform the task involve in each of the 183 learning objective of the SHS accounting curriculum on a six point Likert scale of 0( not covered), 1(not at all) to 6(to a very large extent). The data is analyzed using statistical measures such as mean, and frequency distributions. Specifically, the data was first coded in excel, mean responses computed and categorized into three categories which are termed: omitted learning objectives (0), unattained learning objectives (1, 2, 3), attained learning (4, 5, 6). These categories are further classified into measured learning outcomes (attained learning) and learning gap (omitted learning, unattained learning). Attained learning represents achieved of learning and learning gap represents unachieved learning. Figure 3 shows the framework of the data analysis.

| Figure 3. Framework for Data Analysis |

4. Results and Discussion

- Out of 426 questionnaires administered, 319(74.9%) were returned. Out of the 319 questionnaire received, 251(78.7%) were validated and used in this study. The rest of the received questionnaires were significantly incomplete and hence not considered in the data analysis. About 85% of the students involved in the study scored grade ‘A1’ or ‘B2’ in the WASSCE accounting paper, 10% scored grade ‘B3’ and 5% scored grade ‘C4. The results of the data analysis is presented and discussed below. In terms of gender, 37% are females and 63% are males.

4.1. Students Learning Experiences

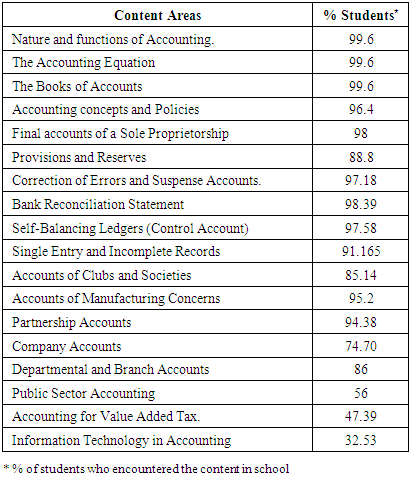

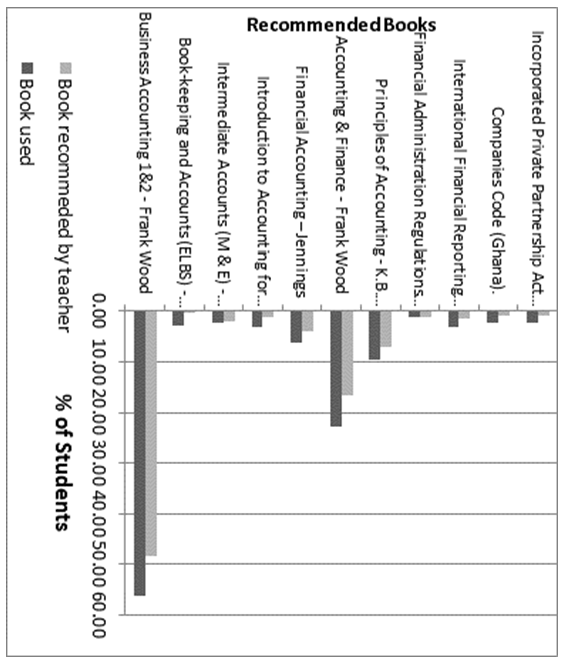

- One of the questions this study aimed to answer is “what proportion of the SHS accounting graduates encountered the various content areas (topics) and learning materials (recommended books) specified in the SHS accounting module guide?” Table 1 shows the bar chat of the topics of the SHS accounting curriculum guide and the percentage of students who encountered or covered those topics in school, and Figure 4 shows the bar chat of the suggested learning materials and the percentage of students who used them as well as those to whom the learning materials were recommended by their accounting teachers or schools.

|

| Figure 4. Learning Material Recommended and Used by Students |

4.2. Extent of SHS Accounting Graduates Learning Outcomes

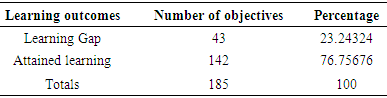

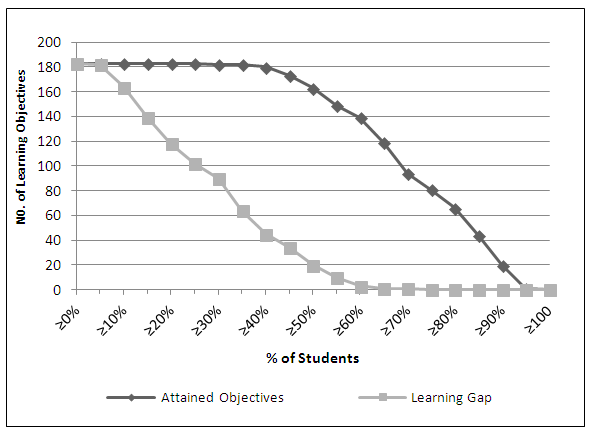

- The SHS accounting curriculum has 183 learning objectives which are stated with 23 precise action verbs. The key concern of this study is to establish the extent to which the learning objectives of the SHS accounting module is attained by students who have gone through the accounting module. The summary of the data collected in this respect is presented in Table 2, Figure 5, Table 3a and Table 3b bellow.

|

| Figure 5. Number of Attained Learning and Learning Gap of SHS Accounting Learning Objectives per Proportion of Students |

4.3. Scope of SHS Accounting Learning Success and Gap

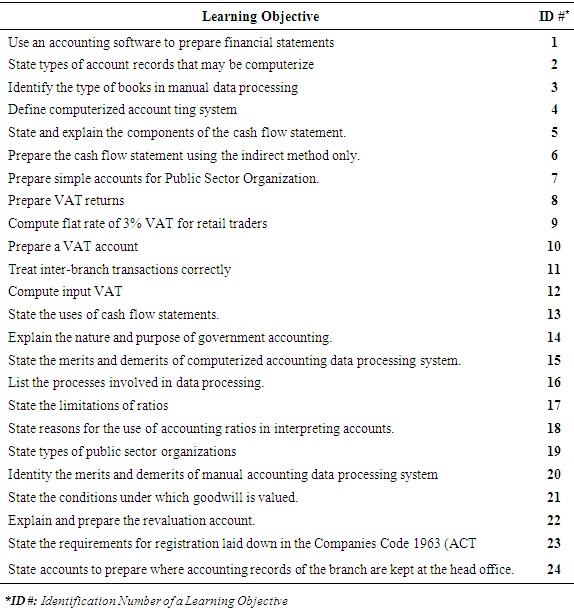

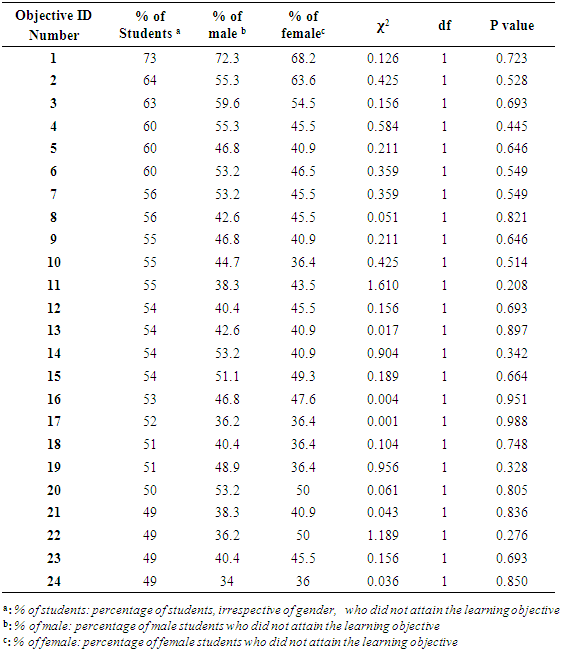

- It is not enough to know the proportion of learning objectives attained or not attained by majority of learners. It is even more important to identify the objectives that are attained and the objectives that are learning gaps. Table 1 shows the summary of learning gaps of the SHS accounting module. Specifically, Table 3a and Table 3b shows the learning objectives that were not achieved by at least half of the SHS accounting graduates, the percentage of students who did not achieve each of these learning objective, the percentage of males and females who did not achieve these objectives and chi-square statistics of the association between gender and the learning outcomes of the students. Specifically, Table 3a shows the learning objectives not achieved by about half or more of the students and the ID number assigned to each of these objectives. Table 3b shows the identification number of the learning objectives and the rest of the details mentioned above.

|

|

5. Implications and Conclusions

- The results of the study suggest that, among the topic of the SHS accounting curriculum, ‘information technology in accounting’ is more likely not be covered in schools than any of the other topic followed by ‘accounting for VAT’, ‘public sector accounting’ and ‘company accounts’. The findings suggest that schools and teachers are most likely not to recommend any of the suggested learning materials to their students and students rarely use the suggested learning materials. The recommended learning material that schools and teachers may not recommend to students and students may never get the opportunity to use are Financial Administration Regulations 2004, International Financial Reporting Standards, Companies Code (Ghana), Incorporated Private Partnership Act 1962 Act 152 and Value Added Tax (VAT) Guide for Facilitators. The study revealed that on average majority of the learning objectives are attained by the SHS accounting graduates though on average a quarter of the learning objectives are learning gap. None of the learning objectives was achieved by all the students involved in this study. It also obvious that some of the learning objectives was not covered given that some content areas were not covered. To some students (a fifth percentile) almost all the learning objectives (182 out of 183) are learning gaps. The findings indicates that learning gaps, in the High school accounting module, are more prevalent in IT accounting, accounting for VAT, Public sector accounting, company accounting, accounting ratios and cash flow statements. These learning gaps are independent of gender of the students and hence both malees and females have similar learning gaps experiences. The fact that this learning gap is identified with respect to students who scored not less that grade B in the WASSCE exams points to how vide it may be if students who scored lower that grade B were surveyed. Plausible unempirical reasons base on observations are that (1) this content areas are mostly not examined by WAEC (2) unavailability of resources such as computers and requisite software and (3) teachers may not have the requisite knowledge and skills in these content areas. These findings implies that, majority of the students who are enrolled in the accounting degree programs may lack most of the requisite accounting competencies for the program despite the fact that they graduate with grade A, B+ or B in accounting at the WASSCE. The situation may be worst in the case of students who attained grades lower than grade B. A significant proportion of the learning objectives are not achieved and hence constitute learning gap. Whiles coverage is an issue, students inability to perform task involve in the learning objectives covered in school is even much greater an issue. These problems may be attributed to a host of factors yet to be investigated. Going forward, more research is needed to find out empirical explanation to these findings. The single most prominent suggestion to eliminate the learning gap identified is for WAEC to extend exam questions to these content areas. This will motivate both teachers and students to give much attention to these areas. Provision of learning materials such the recommended text books and resources may also help reduce the learning gap.