-

Paper Information

- Next Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2016; 5(2): 90-97

doi:10.5923/j.ijfa.20160502.03

Tax Administration in Tanzania: An Assessment of Factors Affecting Tax Morale and Voluntary Tax Compliance towards Effective Tax Administration

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLFlavianus Benedicto Ng’eni 1, 2

1Department of Commerce and Business Administration, Acharya Nagarjuna University (ANU), India

2Institute of Finance Management (IFM), Dar Es Salaam, Tanzania

Correspondence to: Flavianus Benedicto Ng’eni , Department of Commerce and Business Administration, Acharya Nagarjuna University (ANU), India.

| Email: |  |

Copyright © 2016 Scientific & Academic Publishing. All Rights Reserved.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Tax is the main source of Government revenue not only for developed countries but also for developing countries like Tanzania. Due to importance of tax revenue and given that most public social services are funded by tax revenue, this study is bestowed on effective tax administration as an engine of tax collections. This desktop and library study aims at reviewing the general mechanisms of tax administration focusing on the tax morale and voluntary tax compliance as the key attributes of tax revenue collections. The focus on tax administration is motivated by the fact that most government revenues are lost due to inefficient and ineffective administration mechanisms, poor taxation policy and improper management in encouraging tax morale and voluntary tax compliance. It is indisputable fact that tax administration is very important in the whole process of improving government revenues. The study unveils crucial aspects of tax administration which tax authority need to assess their cause and effects towards effective tax administration. Key attributes of tax administration apart from tax morale and voluntary tax compliance are sensitization about the importance of paying taxes in order to enable government to provide quality social services to the general public. It is notable that tax is a main source of government revenue, such that recommendations for improving its administration are of importance to the policy makers and implementers across the world. This paper is as equally important to developing countries (Tanzania) and the rest of the world.

Keywords: Tax administration, Tax morale, Voluntary compliance

Cite this paper: Flavianus Benedicto Ng’eni , Tax Administration in Tanzania: An Assessment of Factors Affecting Tax Morale and Voluntary Tax Compliance towards Effective Tax Administration, International Journal of Finance and Accounting , Vol. 5 No. 2, 2016, pp. 90-97. doi: 10.5923/j.ijfa.20160502.03.

Article Outline

1. Introduction

- One of the problems facing developing countries is lack of speedy, evenhanded and sustainable economic growth. Most studies advocate that the problem of economic growth can be overcome by having a stable budget position (Bird, 1992). The most imperative thing is that revenue must be adequate to finance government investment in human capital development and allocate a higher proportion of expenditures to social expenditures (education, health) and provision of basic infrastructure such as water, reliable electricity, communication systems infrastructure, a good transport system and other public social services. In order to achieve all these services, governments require an efficient and well-designed tax system equipped with strong tax administration.Since 1988, Tanzania has been implementing fairly comprehensive tax reforms as part of widening economic reform program to bolster growth and achieve sustained macroeconomic stability (low inflation, prudent fiscal stance, stable exchange rate and favorable balance of payments position). Reforms on the fiscal front have focused on improving revenue administration, reducing of tax rates, simplifying the tax structure, introducing value added tax and broadening of the tax base. In spite of these reforms, Tanzania still has a relatively low tax to GDP ratio, which lies considerably below average for sub-Saharan Africa. Tax stands as a major source of government revenue not only for developed countries but also for developing countries such as Tanzania. Tax revenues guide national government development and also are used to finance substantial part of government operations including provision of public social services (Jamala et al; 2013). In any country, taxation policy acts as a fundamental element for economic policies and also helps to ensure countries’ economic growth and improvement of global competitiveness (Taha and Loganathan; 2008). The efforts of collecting tax revenues cannot be achieved unless there is strong tax administration which ensures proper tax collections and minimizing or engulfing tax evasion.One of the problems which faces developing countries to collect low tax revenues is inefficient and ineffective tax administration (Okoye and Ezejiofor; 2014). The main advantageous of effective tax administration is to help countries to collect all taxes appropriately and also to rethink on the proper ways of administering tax revenues, tax evasion and fight against corruption on taxation issues.In addressing the importance of internal generated revenues, Adenugba and Ogechi (2013) reveal that revenue administration agencies are very important in fostering revenue collections however; their mechanisms need to be reviewed in order to work out any weaknesses noted in their operations. In general, under-funding of basic social services remains critical (Ame, Chaya & John; 2013) impediment to economic growth and progress in sustainable human development. Moreover, a large proportion of the budget still depends on unpredictable funds from development partners (DPs). These challenges prompt and motivate a re-examination of Tanzania’s tax system on the aspects of tax administration’s efficiency and effectiveness in enhancing government revenues. This study aims at reviewing and analyzing the contribution and performance of Tax administration in Tanzania on the basis of three major objectives of taxation namely, efficiency, equity and revenue generation, with the ultimate aim of offering some suggestions for improvement. The focus on tax administration is motivated by the fact that most government revenues are lost due inefficient and ineffective administration, poor taxation policy and improper management in encouraging tax morale and voluntary tax compliance. It is notable that tax is the main source of government revenue, such that recommendations for improving its administration are of importance to the policy makers and implementers across the world. This paper is as equally important to developing countries (Tanzania) and the rest of the world. The rest of this paper is organized as follows; Methodology; Tax administration in general; Compliance and measures of enforcing voluntary tax compliance; The role of tax morale in tax compliance and collections; Tax administration in Tanzanian context (tax compliance and tax evasion) and the last part is Concluding remarks and recommendations.

2. Methodology

- This is a desktop studying which has considered published and unpublished materials. Also the study has made use of library services in undertaking this study. In undertaking this study the author conducted a rigorous literature review including the use of library and e-Journals. The paper is thus purely based on desktop and library research methodology. In this regard various journals and research papers/ paper articles germane to public sector tax administration and current issues in taxation have been surveyed extremely in undertaking this study. Also, the study has surveyed in greater detail all various government statistics which signify the whole role of tax administration in Tanzania and the rest of the world.

2.1. Tax Administration in General

- The primary function of the tax administration is to scrutinize compliance and also to enforce sanctions to offenders as provided in the rules and regulations (Bird, 2004). The effective tax administration needs to be connected with identification, assessment and collections of tax revenues (Gurawa & Mansor, (2015) and Bird, 2004). Effective tax administration is a key machinery of tax revenue collections in both developed and developing economy. Vehorn and Ahmad (1997) point out four models of tax administration in a decentralized environment which are central government tax administration, central government tax administration with assignment of taxing powers to different levels of government, multilevel administration with revenue sharing and self-administration by each level of government. The choice of the tax administration model depends on the structure and complexity of the country governing system for example for unitary states or federal states. Another tax administration model which is mostly preferred by most Tanzanian local governments is contracting out services to private companies. Mikesell (2003) expounds that the extent to which national and sub national authorities cooperate independently the more reliance is likely to continue. In this situation, intergovernmental fund transfer becomes revenue building capacity for financing local government operations. In either way, tax administration is very important and tax authorities need to design tax administration reform that can help to identify bottlenecks (Silvan and Baer; 1997) that in one way or other affects tax administration operations.Globalization is expanding and the number of critical taxpayer services and compliance oversight tools such as policing transfer pricing practices emerge which helps to administer taxes effectively. However, as stressed by Burgess and Stern (1993), taxation mechanism in developing countries remains fundamentally different from developed countries. This contention is not surprising because most economic activities in developing economy occur in the informal or shadow economy and thus bypasses taxation rules and regulations. Additionally, the tax administration capacities for developing and transition governments are usually weak may be due to poor technological infrastructure. Stiglitz (2009:2) proposes that redesigning taxing institutions and policies, including what he calls “corruption resistant tax structures”, should be a central concern of fiscal reform for developing countries. However, while the shadow economies of developing countries are characterized by low capital intensities, small scale of operation, traditional technologies, and often low profit margins; unsanctioned production in transition economies is more often done in big enterprises (Stiglitz; 2009). Fiscal reform should help to transform informal sector into formal sector in order to allow tax rules and regulations to work through and enforce voluntary tax compliance.Aurioll and Warlters (2005) suggest that developing country governments consciously need to relax and open barriers to entry into the formal sector in an effort to enhance tax administration and maximize tax revenue. According to Aurioll and Warlters (2005), Governments in developing countries need to work out observed internally degrees of corruption, malfeasance, and general administrative inefficiencies in tax revenue collection. In an attempt to address the challenges of tax administration on collecting government revenue in developing countries, Abiola and Asiweh (2012) examine tax administration focusing on its crucial role of reducing tax evasion. Their study revealed that effective enforcement machinery is very significant in increasing tax revenue. The objective of maximizing revenue should be in line with effective tax administration that can help to work against corruption, tax evasion and all other bottlenecks of the system.

2.2. Compliance and Measures of Enforcing Voluntary Tax Compliance

- Facilitating compliance involves strengthening key elements such as improving services to taxpayers by providing them with clear instructions, understandable forms, and assistance and information as necessary. James and Alley (2004) assert that tax compliance is very important in the whole process of collecting tax revenues. It is of particular importance as compared to self assessment and electronic commerce which are strongly given high attention currently. Monitoring tax compliance is very important and requires proper maintenance of taxpayer current accounts and management information systems which include both taxpayers and third-party agents involved in the tax system as well as appropriate and prompt procedures to detect and enforce tax payment promptly (Bird, 2015). Notwithstanding, penalties can be used as one of the methods of enforcing tax compliance but creating tax awareness to tax payers is very significant in sensitizing them to fulfill tax obligations effortlessly (James and Alley; 2004). Improving compliance requires a mix of both measures as well as additional measures to deter non-compliance such as establishing a reasonable risk of detection and the effective application of penalties. According to Gemmel and Hasseldine (2014), tax compliance is generally concerned with tax evasion, tax avoidance, compliance and non compliance. The proper means of achieving tax compliance need to be designed in such a way that can help to deal with tax evasion and tax avoidance. Ideally, such measures should be combined so as to maximize their effort on tax compliance and maximizing government revenue. In addressing electronic transparent as a means of enhancing voluntary tax compliance, Lubua (2014) reveals that awareness of tax laws, business experience and the integrity of employees together with training needs are very important in compliance process. Improving tax compliance is not the same as discouraging noncompliance. Tax administration exists to ensure tax compliance and discourage non compliance (Alm and Martinez-Vazquez; 2003). “The standard Economic Approach to taxation usually ignores such key administrative issues as evasion and avoidance, administrative and compliance costs and how the way in which taxpayers and tax officials conceptualize and carry out the process of assessing, collecting and enforcing taxes may profoundly alter the effects of the system” (Bird, 2015 pp1). Also Thiga and Muturi (2015) divulge that tax rate and tax compliance cost are very significant aspects of tax compliance and tax awareness to tax payers. Administrative and compliance cost are very important aspects of tax compliance and should not be ignored when designing efficient and effective compliance strategy. Also, Alabede, Ariffin and Ichis (2011) reveal further that tax payers’ attitude on tax evasion has positive relationship with compliance behavior. In a broad sense, it can be argued that some tax payers do comply with tax laws not only because they want to comply, simply because they understand the importance of tax and tax compliance for the prosperity of the nation. For this reason, tax awareness is very important and also can help to engulf tax evasion and tax avoidance. Also, non compliance behavior can be reduced by focusing on changing rules rather than reducing tax gap in the tax system (Gemmel and Hasseldine; 2014).

2.3. The Role of Tax Morale in Tax Compliance and Tax Collections

- Tax morale is one of the key factors which determines the level of compliance for tax collections in most developing countries (Sa, Martins and Gomes; 2014). It is a motivational behavior of paying taxes as a civil (constitutional) obligation (Torgler, 2003). In general, tax morale is very important in the whole mechanism of tax administration and plays significant roles on reducing tax evasion through encouraging smooth tax compliance. The most factors that contribute to low tax collections in developing economy among others are tax evasion (Lis, 2013). An attempt of changing a nation's broadly embedded culture of non-compliance into one of improved voluntary compliance warrants more qualitatively oriented and interactive research from its tax administrators (ATO, 1998). In order to react against tax evasion, regulators and policy makers need to strengthen monitoring and impose severe penalties to tax evaders. However, Frey (2003) claims that enforcing citizens to pay tax is very costly strategy, instead, authorities need to work closely with citizens in all material aspects of taxation policy. Authorities are challenged to build a trust on the use of public funds and to act against corruption in order to raise tax morale. In a nutshell, when thinking about the improvement of tax collections, tax morale and tax compliance should be in a forefront of the whole mechanism of tax administration. According to Adebisi and Gbegi (2013), proper use of public funds has strong influence on enhancing tax morale and compliance for tax payers. The system of fairness, trust and a sense of acceptance or belonging among citizens who share a unified, national identity (Uslaner, 2003) may bear very significant consequential situations and alternative acts of social conduct that mitigate non-compliance. The efficient and effective provision of quality public goods has embedded effect on lessening tax evasion and tax avoidance. Tax payment is constitutional obligation of the citizens, but bad behavior of the government officials can enforce tax payers to shift to shadow economy. Also, institutional arrangement of the public governance can affect tax morale as well. Guth, Lerati and Sausgruber (2003) point out that decentralization and centralization have different operating environment on tax collection issues. In a decentralized system, citizens are easily ready to pay tax given the idea that they can enjoy directly benefits of tax but it is otherwise for centralization system. Following this contention, the idea of raising tax awareness to tax payers is inevitable (Sumartaya and Hafidiah; 2014) and for sure this strategy can help to fight against tax evasion. Martinez-Vazquez and Wallace (1999) point out that personal income tax compliance rate is higher as compared to VAT compliance rate. A high level of tax evasion jeopardizes government's ability to provide fundamental services. There is a growing recognition that there are notable differences across countries in their levels of tax compliance and that standard economic models of taxpayer compliance are unable to explain these differences. In the face of these difficulties, many researchers such as Sa, Martins & Gomes (2014), Daude, Guterrez & Melguizo (2013) and Lillemets (2010) have suggested that the intrinsic motivation for individuals to pay taxes differs across countries and that these differences in tax morale across countries which may explain much of the differences is observed in compliance behavior. For example with reference to developing countries, Daude, Guterrez and Melguizo (2013) explain that tax morale is driven by age, religion, gender, educational level and employment status. Also, they further argue that satisfaction of the quality of social public services provided by the government has high impact on the tax morale and tax compliance. Also, in their study Torgler and Scheneider (2007) reveal that improved social institutions such as tax morale, voice and accountability, the rule of law, government effectiveness and reducing corruption helps to reduce shadow economy activities. Following this discussion of tax morale, it is now clear that tax revenue collections can be improved by lessening shadow economy activities, raising awareness to tax payers, encouraging voluntary tax compliance and building trust to citizens in order to inbuilt tax morale in their hearts. One of the most serious problems undermining tax compliance is the perception among citizens that the taxes they pay are not spent on public services. Despite significant improvements in public service delivery in recent years, data show that citizens still feel getting little in return for taxes paid in Tanzania. This perception erodes residents’ confidence in the capacity of local councils to supply essential services which, in turn, impacts their willingness to pay taxes (Odd-Helge et al, 2006). Kelly (2000) points out that major problem exist in property tax administration particularly for developing countries. For the property tax, the case is somehow astonishing because tax rate are very minimal and enforcement against non compliance is simply missing. In order to facilitate efficient revenue collection, Jenkins (1994) calls for a restructuring of revenue administrations to provide independence for the authority responsible for tax collections. The authority should establish clear and transparent operating policies to be well adhered by tax collectors. It is clear that independent revenue administrations should be given mandate and being fully responsible for their own recruitment, training, and salary structure in order to control general conduct of the tax collectors.

2.4. Tax Administration in Tanzanian Context: Tax Compliance and Tax Evasion

- Drawing from most developing countries, Tanzania also depends heavily on tax as a key source of government revenue. Most development projects and recurrent spending are funded by tax revenues and also partially are funded by development partners (DPs). Also, local government authorities’ projects and operating activities are funded by intergovernmental fund transfer (tax) from central government, internally collected revenues and borrowing. Therefore, no doubt that tax is very important in both local governments and central governments. Local governments have constitutional obligation of providing public social services to citizens at local level. For the local governments to provide quality public social services like water, health, education and road infrastructure, there should be a discipline in collecting and spending tax revenues.For all these to be achieved, Tanzania needs strong tax administration equipped with tax awareness to tax payers, tax morale and voluntary tax compliance. Tax administrators should be in a position of encouraging tax morale, voluntary tax compliance through tax awareness and being able to fight against corruption in order to built trust amongst tax payers. In Tanzania, tax collection is controlled and serviced by Tanzania Revenue Authority (TRA) which came into operation in 1996 after being established by Act of Parliament No. 11 of 1995.Lubua (2014) points out that voluntary tax compliance is very important in the whole process of tax administration in Tanzania. The study revealed that tax compliance is influenced by awareness of tax laws, business experience, integrity of employees and training needs. Due to the importance of voluntary tax compliance, the author recommends effort on awareness of tax laws to all tax payers in order to improve government revenues. Also, Machogu & Amayi (2013) and Aiko (2013) found that tax knowledge is very important in promoting voluntary tax compliance. In order to enhance domestic tax collections, tax authorities need to promote tax education and integrating tax education in Tanzanian school curriculum for enhancing voluntary tax compliance and building tax morale. Tax knowledge can help tax payers to know the importance of tax and hence keep proper record of accounting for determining tax payments. Also, information communication technology (ICT) has strong influence on the performance of tax administrators in collecting tax revenues. Chatama (2013) found that ICT contributes significantly on the tax collections in the large tax payers’ department of Tanzania Revenue Authority (TRA). The study revealed that ICT has improved processing returns in time, minimising operational costs and timely access of customers’ tax records. Therefore, tax authorities should focus of improving ICT infrastructure in order to easy tax collection mechanisms and boost government revenue.

|

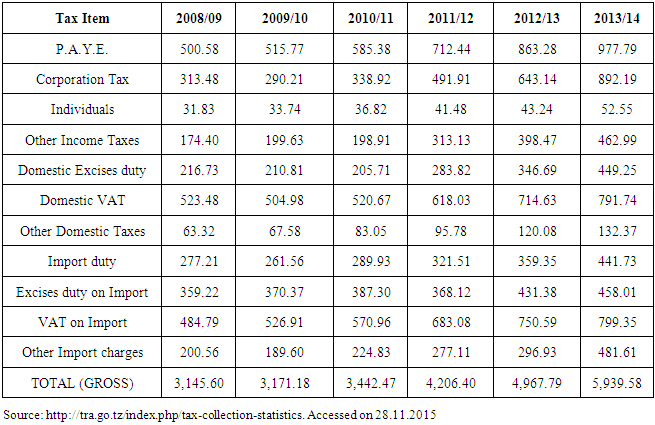

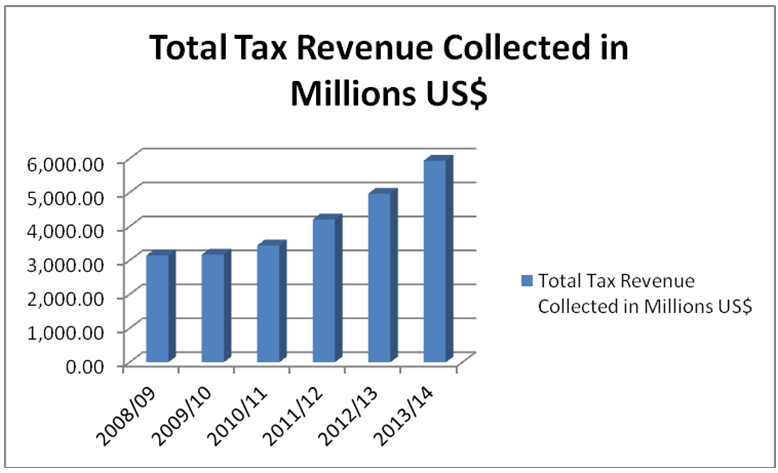

| Graph 3.1. Total Tax Revenues collected for Six years |

|

3. Concluding Remarks and Recommendations

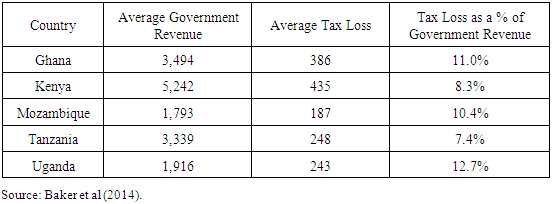

- Even though paying taxes is a primacy civil obligation, the level of voluntary compliance remains low. Table 3.2 indicates that Tanzania looses 7.4% of the average total revenue due to trade mis-invoicing, indicating that there is a serious problem on tax administration, alarming responsible authorities to react quickly and attentively on this matter for the betterment of the national economy and citizens’ social welfare. TRA has to continue to carryout taxpayer education campaigns so as to uplift the level of public awareness on the importance of paying taxes and that tax evasion is criminal offence. Also, efforts should be directed on building trust, tax morale and encourage voluntary tax compliance. The Authority has to widen up a number of taxpayer sensitization seminars and workshops on various tax laws. The idea of enhancing tax collections is not to increase tax rate rather to enforce customs and tax administration and also to incorporate SMEs operations on the tax policy in order to increase government revenue. Also, TRA should ensure that Customs and Excise department in strongly committed to collect all government revenue through taxes and the reforms which are taking place in the department are successful. It is therefore a challenge to the government to proceed with tax reforms in order to identify new sources of tax revenues and increase efforts on fighting against corruptions. Also, TRA management should work strongly and promoting effectiveness and efficiency in the department in order to achieve the targeted revenue collection. Enhance human resource capacity and organization-review in the departmental structure, maintain high level of staff integrity in tax revenue collection, eradicating dumping of transit goods by conducting risk based verification audits, preventing smuggling across all Tanzanian borders by conducting surprise visits to most risk areas, proper valuation and classify locally imported and transit goods by identifying sensitive commodities. Account for each tax assessment by identifying overdue assessments and make timely follow up to recover the assessed tax, prevent revenue leakage from exemptions, account for all cargo arriving at the port, airport and border stations by developing a system that will record inward and outward movement of goods.

Note

- 1. The amounts were translated in US$ using annual average rate from http://www.usforex.com/forex-tools/historical-rate-tools/yearly-average-rates