-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2015; 4(5): 304-310

doi:10.5923/j.ijfa.20150405.08

Factors Affecting for Magnitude of Stock Price Reaction for Security Issue Announcements: Evidence from Colombo Stock Exchange

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLU. Chathurika Edirisinghe1, Y. M. Sandun Keerthipala2

1Department of Accountancy & Finance, Faculty of Management Studies, Sabaragamuwa University of Sri Lanka, Sri Lanka

2ANZ Bank, Business Centre, Geraldton, WA, Australia

Correspondence to: U. Chathurika Edirisinghe, Department of Accountancy & Finance, Faculty of Management Studies, Sabaragamuwa University of Sri Lanka, Sri Lanka.

| Email: |  |

Copyright © 2015 Scientific & Academic Publishing. All Rights Reserved.

This study focuses on investigating the impact which some selected factors have on the magnitude of the price reaction for right issue and debenture issue announcements of Colombo Stock Exchange during the period of 2005 to 2011. Stock reactions based on differences in the relative size of the issue, size of the firm, pre offer leverage ratio, stock price performance prior to issue was analyzed to identify the most influencing factor. Cross sectional regression analysis reveals a significant positive influence of issue size on price reaction for right issues but the influence by the rest of the factors were insignificant. In debenture issues, significant negative impact of pre offer leverage ratio on magnitude of price reaction could be identified while rest of the factors having an insignificant impact.

Keywords: Price Reaction, Right Issue, Debenture Issue, Cross Sectional Regression Analysis

Cite this paper: U. Chathurika Edirisinghe, Y. M. Sandun Keerthipala, Factors Affecting for Magnitude of Stock Price Reaction for Security Issue Announcements: Evidence from Colombo Stock Exchange, International Journal of Finance and Accounting , Vol. 4 No. 5, 2015, pp. 304-310. doi: 10.5923/j.ijfa.20150405.08.

Article Outline

1. Introduction

- Many studies in the past have concentrated on identifying the information efficiency of the market by analysing the stock price reaction for various information releasing to the market. Announcement of security issues is also one of the events which researchers had focuses on to identify the nature of the price reaction. Numerous empirical studies have shown that announcements of equity issues cause negative price reactions, whereas the news of a debt issue is followed by a positive price reaction. But very few have actually gone a further step to reveal “what factors impacts the magnitude of the return behavior during the announcement of various security issues’. Mikkelson (1985) was the first to investigate the factors affecting negative stock price responses to the capital structure changes by conducting a cross-sectional study on convertible security calls. From there onwards different scholars have selected various factors based on capital structure theories to identify the relationship with the stock price movements around capital issue announcements. Among factors that have been considered by later studies such as Asquith and Mullins (1986), Graham et al. (1999), Cheng et al. (2005), Chen and Shehu (2009) include factors such as firm size, leverage, growth option, bank debt reduction, stock performance prior to the offering and book to market ratio. Almost all of these studies are on developed stock markets like US & Japan and it is very rare to find widely cited empirical work based on Colombo Stock Exchange (CSE). Due to the wider differences of the market conditions, the findings of these developed markets cannot be presumed as same in the developing markets. Due to operationalization difficulties it is not practical to consider all the factors, thus if a study could be conducted with selecting few factors conditional upon the data availability would contribute to bridge this gap in the literature relevant to developing markets.This study attempt to provide empirical evidences with the objective to investigate whether factors such as size of the issue, leverage ratio, stock price performance prior to offering and size of the issuing firm has an influence over the magnitude of price reaction by analyzing the price reaction for 96 right issues and 20 debenture issues during the period of 2005 to 2011.

2. Literature Review

- Many studies in past, have been carried out hypothesizing range of different factors as the motivation for the price behaviour for security issue announcements. Size of the issue has frequently considered as one of the factors which determine the price changes. From those one of the main factors which has considered is “Size of the Issu” (Masulis 1980; Asquith & Mullins 1986: Mikkelson & Partch 1986; Korajczyk, et al., 1990; Schadler & Manuel 1994, Chen & Shehu 2009). Asquith and Mullins (1986) consider size of the issue as a variable to prove the information hypothesis and leverage related signal hypothesis. They provide evidence for an inverse relationship between the size of the issue and announcement day excess return and justifies that larger the size of the issues conveys the message of larger change in the capital structure, thus information which managers keep from outsiders regarding their future earnings is also high. But Baker and Wugler (2000) suggest an opposing view, stating that size of the issue is not an influence on price reaction because size of a new issue would only represent a small fraction of the total capital outstanding, thus would not be a substantial influencer to change the firm’s capital level. Though Korajczyk, et al., (1990) observe the same results (negative coefficient) they argue that the relationship between size of the issue and the negative price reaction may not necessarily be consistent with the information based hypothesis because larger the overvaluation of the firms security larger the incentive to issue more equity. Size of the issue may also be a factor influencing the price drop at the announcement of security issue but this argument loses its value with Scholes (1972) horizontal demand curve theory.The second factor considered in the current study is change in the firm leverage level, and it has been considered by scholars such as Masulis (1980), Dann and Mikkelson (1984), Asquith and Mullins (1986), Korajczyk, et al (1990), Baker and Wugler, (2002), Brounen and Eichholtz (2001), Cheng, et al., (2005), Chen and Shehu (2009). Due to reasons such as, choice of equity due to excessive debt levels, probability of financial distress due to higher leverage ratio this factor may have an impact over the magnitude of price reaction. Masulis (1980) also points out that the introduction of debt capital to the capital structure has an impact of reducing the stockholder-manager agency costs by increasing the managers’ proportional ownership in the firm’s equity. Also Graham et al. (1999) state that the average change in the market value of the firm is indistinguishable from the amount of debt retired by the firm which indicates the size of the capital issue or repurchase does not affect the price reaction. Chen and Shehu (2009) have witnessed firms with leverage ratio moving closer to the industry median, experience lesser negative stock price reaction comparing with firms who moves away from the industry median.Several studies such as Asquith and Mullins (1986), Mikkelson and Partch (1986), Korajczyk, et al., (1990), Li and Zhao (2003), Dutordoir and Hodrick (2012) made an effort to investigate a relationship between stock market reaction for security issue announcement and the market performance of the respective security during a considerable period prior to security issue announcement. Asquith and Mullins (1986) find that the announcement day price reduction is inversely related to stock price performance in the year prior to the announcement. Their justification for this result is, when there is a stock run up prior to the issue, investors take that as a bad news because they presume managers are been opportunistic to raise finance since shares are overvalued in the market. There justification for this result is, when there is a stock run up prior to the issue, investors take that as a bad news due to the presumption of managers been opportunistic to raise finance because shares are overvalued in the market.The relationship between the stock run-up and announcement effect can be described by Market Timing theory by Myers & Majluf (1984). A study based on Japanese market by Kang and Stulz (1996) provides different argument based on cultural difference in the countries. They argue, unlike American firms Japanese firms are less willing to scarify positive NPV project if the firms share price is performing poorly and the likelihood of Japanese firms issuing securities following positive excess returns is less compared to American firms. The main justification they provide for this cultural phenomena is the role played by the long term shareholders of Japanese firms.The relative size of the firm has been considered as factor by many studies though the explicit explanations are not available as the reason for such a behavior. Studies like Kang and Stulz (1996), Brav, et al., (2000) and Cheng et al. (2005) have considered size of the firm in terms of market value as a factor which describes the nature of the stock performance at a security issue. Kang & Stulz (1996) investigate the differences between US markets and Japanese markets and have observe that larger Japanese companies have lower abnormal returns for equity issue announcements compared to smaller Japanese firms. Kang & Stulz’s justification for these results are that, larger firms have better access to capital markets due to corporate control differences. Myers & Majluf, (1984) states that information asymmetry is higher in smaller firms in comparison to larger firms during an equity issue. But Cheng et al. (2005) provide opposite results which prove that larger the firms greater the negative abnormal returns for equity issues in Japanese stock Markets.

3. Data and Methodology

- The sample period for the study was right issues and debenture issues announcements during the period of 2005 to 2011. From 138 right issues during the period only 96 right issues were selected through sample selection criteria and only 20 right issues were selected from 30 debenture issues during the period. The whole study was based on secondary data sources. The two most important set of data were daily price behaviour around the security issues and the security announcement date. Daily price information of securities was obtained from the annual data library CD issued by CSE and the announcement date was considered as the earliest date which issue was appeared under the news & info heading of each listed companies profile in CSE official website.

3.1. List of Hypothesis

- Following alternative hypotheses were formed based on the identified factors,H1a: There is a significant influence by size of the issue on stock price reaction to the announcement of right & debenture issues.H1b: There is a significant influence by pre issue leverage ratio on stock price reaction to the announcement of right & debenture issues.H1d: There is a significant influence by stock price performance prior to issue on stock price reaction to the announcement of right & debenture issues.H1e: There is a significant influence by size of the issuing firm on stock price reaction to the announcement of right & debenture issues.

3.2. Cross sectional Analysis

- A cross-sectional analysis has been carried out to examine the relationship between price reaction and factors which assumed to be affecting such reaction. Four variables are considered as the factors affecting the price reaction, namely size of the issue, leverage ratio, market price before the issue (MP) & size of the firm. The cross-sectional regression model is given as follows:

| (1) |

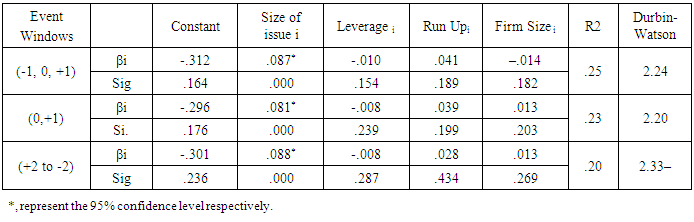

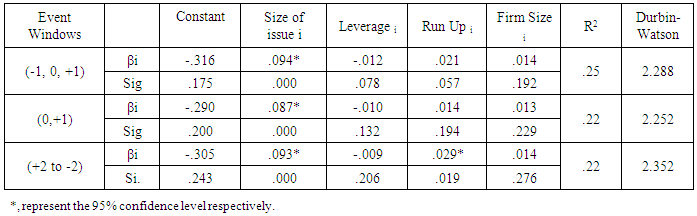

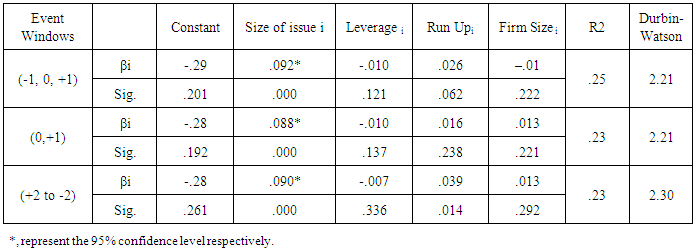

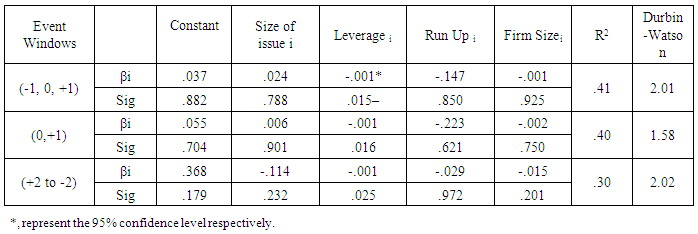

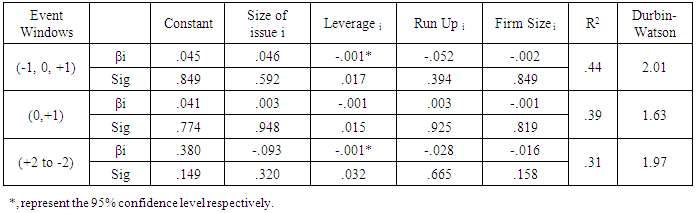

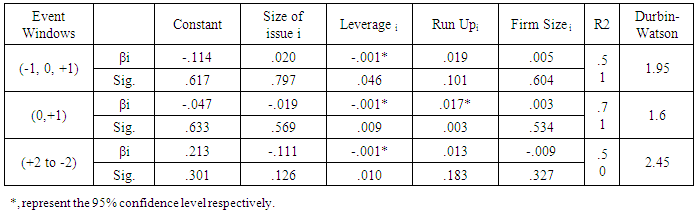

4. Results

- The following section of the study discusses the results of the cross sectional regression analysis of the selected factors which are assumed to be affecting on stock price reaction around security issue announcements. As literature have not suggested the most suitable event period to calculate CAAR, multiple events windows have been considered and multiple regressions have been carried out to recognize most suitable model to analyze price reaction. The event windows considered are (day -1, 0, day +1), (day -1,0), (day 0), (day 0,+1), (day -2 to day +2), (day -3 to +3), (day +10 to -10) only windows (day -1, 0, +1), (day 0, +1) and (day -2 to +2) has been accounted for final analysis considering the higher R2 value and coefficient significance.Table 1 shows the cross sectional regression result of the coefficient of each independent variable with the CAAR returns of 3 event windows according to MAR model. The coefficient of issue size, stock run up and firm size are positive in all three event windows according to MM model and coefficient of leverage being negative. But only coefficient of issue size is significant at the 95% confidence level in all three event windows. Therefore only H1a alternative hypothesis can be accepted concluding there is a significant positive relationship with stock price reaction and size of the issue. For all other three variables the null hypothesis has to be accepted. R2 value of all three event windows are nearly 0.2 which means that only 20% of the dependent variable is defined by the selected independent variable.

|

|

|

|

|

|

5. Conclusions

- This study attempts to investigates the factors which influence the magnitude of the price reaction of right issues and debenture issues and observed that from the selected factors only two have been significant enough to have an impact on the price reaction. The Coefficient of issue size is significantly positive for right issues announcements and positive yet insignificant for debenture issue announcements. These results contradicts with many of the previous studies such as Asquith and Mullins (1986), Mikkelson and Partch (1986), Brounen and Eichholtz, (2001), Chen and Shehu (2009), Cheng et al. (2005) who justifies a negative relationship between issue size and price reaction for equity/debt/convertible security offerings. The result of current study is also inconsistent with size of the issue being a function of tax disadvantage hypothesis, as a function of information asymmetry hypothesis and price pressure hypothesis.The next significant result can be observed when pre issue leverage ratio is taken as a variable effecting price reaction around security announcements. Although coefficients of both types of issues are negative only debenture issues provide statistical significance, which implies firms with higher leverage level would experience larger negative abnormal returns around the debenture issues. These results are contradicting with findings of Brounen & Eichholtz (2001), Cheng, et al., (2005) which proved the debt market accessibility hypothesis and financial distress hypothesis at higher leverage level. This study reveals that the market participants of CSE behave differently than the other markets, because findings of the current study are not consistent with the findings of previous studies. Though issue of the debt capital is preferred than equity capital in developed markets, shareholders perception is not the same in Sri Lanka. This negative perception may have built with the recent past bankruptcy stories of key financial institutions of Sri Lanka, because these institutions have heavily relied on higher debt capital and has raised further debt as the last resort to survive.. Though debt capital presumed to be the cheaper source of capital the cost of default risk and higher preference at the liquidation appears to be influencing more to the investors of Sri Lanka.The rest of the variable considered fails to justify statistical significance of the relationship with price reaction although stock run up showed a positive relationship with price reaction and firm size provides negative relationship with the price reaction for both right and debenture issues. Thus the discussion on those variables were not carried out further since the null hypothesis had to be accepted confirming there is no relationship [stock price performance prior to the issue and firm size do not have a relationship for price reaction around security issues.