-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2014; 3(6): 349-355

doi:10.5923/j.ijfa.20140306.03

An Assessment of Environmental Information Disclosure Practices of Selected Nigerian Manufacturing Companies

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLOnyali Chidiebele Innocent, Okafor Tochukwu Gloria, Egolum Priscilla

Department of Accountancy, Faculty of Management Sciences, Nnamdi Azikiwe University, Awka, Nigeria

Correspondence to: Onyali Chidiebele Innocent, Department of Accountancy, Faculty of Management Sciences, Nnamdi Azikiwe University, Awka, Nigeria.

| Email: |  |

Copyright © 2014 Scientific & Academic Publishing. All Rights Reserved.

Information disclosure policies have become a key component of environmental policy globally. Recently, there have been increased hue and cry about environmental degradation, an advent traceable to industrial revolution. Firms are now expected to address the impact of their operations on the environment and society in general. In the light of these, the study assessed the extent, nature and quality of environmental information disclosure practices of manufacturing firms in Nigeria. Content analysis was adopted in analyzing the annual report of the selected firms with regards to their environmental disclosure practices. Furthermore, a survey was carried out in order to ascertain whether the environmental disclosure practices of firms in Nigeria has improved. This was done with the aid of questionnaire administered to 40 Chartered accountants. The study adopted one sample t - test in testing the formulated hypothesis. The findings of the study indicated that the environmental disclosure practices of firms in Nigeria is still ad hoc and contains little or no quantifiable data. The study therefore recommends the development of environmental disclosure standards that will harmonize the disclosure practices of firms as well as results in providing environmental quantifiable data.

Keywords: Environmental Accounting and Disclosure

Cite this paper: Onyali Chidiebele Innocent, Okafor Tochukwu Gloria, Egolum Priscilla, An Assessment of Environmental Information Disclosure Practices of Selected Nigerian Manufacturing Companies, International Journal of Finance and Accounting , Vol. 3 No. 6, 2014, pp. 349-355. doi: 10.5923/j.ijfa.20140306.03.

Article Outline

1. Introduction

- The state of the world's environment and the impact of mankind on the ecology of the world have led to increased public concern and scrutiny of the operations and performances of organizations (Uwuigbe, 2012). Organizations are now expected to address the impact of their operations on the environment and society in general. Most environmental degradations and emissions are anthropogenic, an advent traceable to the industrial revolution of late 18th century where economic activities in many communities moved from agriculture to manufacturing. Production shifted from its traditional locations in the home and the small workshop to factories. The overall amount of goods and services produced expanded dramatically. New groups of investors, businesspeople and managers took financial risks and reaped great rewards. Industrialization has brought factory pollutants and greater land use, which have harmed the natural environment (Mastrandrea and Schneider, 2008). For instance, the application of machinery and science to agriculture has led to greater land use and, therefore, extensive loss of habitat for animals and plants. These factors, in turn, have caused many species to become extinct or endangered.The use of natural resources including energy is indeed indispensable to economic development (Akinbami and Adegbulugbe, 1998), and not devoid of environmental consequences as traceable to the environmental degradation and atmospheric pollution experienced in Nigeria. Recently, there have been increased hue and cry about climate change in the world, as it has been highly inimical to our existence; ocean levels keep rising, global warming keeps threatening; yet, natural resources like the forest, serving as natural processor that regulates an appealing atmosphere is being cut down, and the capacity of trees which removes carbon dioxide from the earth is being diminished. The northern part of the country is being literally "blown away" by wind erosion while the southern part is being washed away into the ocean. Between 1976 and 1988, a total of 2,000 reports of oil spillages were recorded with the discharge of two million barrels of oil into the environment (Ikporukpo, 1988). Urban cities and town in Nigeria are increasingly threatened by pollution of air and water and improper disposal of solid wastes while the rural areas are plagued by soil erosion, deforestation, and bush burning (NEST, 1991).Over 2 million tonnes of soil are lost annually in south-central Nigeria, and this has caused great decline in agricultural yield (Dike, 1995). According to the NNPC (2010), a large proportion (about 63%) of the gas produced in Nigeria is being flared. By 2002 and 2003, gas flared remained as high as 45.4% and 42.7% while gas used was 54.6% and 57.3%, respectively. The economic costs in terms of lost incomes and reduction in the standard of living can therefore, be expected to be staggering.Ban (2007), in his address at the release of the Intergovernmental Panel on Climate Change (IPCC) Fourth Assessment Synthesis Report, said that “slowing and reversing these threats posed by climate change are the defining challenge of our age''. The primary way companies can contribute to solutions is to reduce carbon dioxide and other greenhouse gas emissions in their own operations and supply chains. Consequently, corporate climate reporting on carbon emissions and other environmental degradations has become a major focus, as disclosure prompts corporate responsibility. The need for Environmental Accounting has become the concern and focus of nations and responsible corporate managements. It became one of the foremost issues on the agenda of nations and businesses earlier in the 1990s and the reasons for this were varied emanating from both within and outside of the firm and particularly at the global level (Okoye and Ngwakwe, 2004). A lot of government enactments, laws and regulations on environmental protection have been made in several nations of the world and Nigeria is slowly responding. The world at large has need to evaluate, assess and effect accounting reporting for raw materials, energy consumption and use of natural resources which have systematically depleted the environment. Besides, the negative impact on the biodiversity through human and industrial activities and the nations’ need to protect the environment, have made for global regulations. These regulatory environmental laws however require only voluntary disclosure in financial statements of environmental information on industrial emissions, degradations, industrial wastages and all activities which impact negatively on the environment. In the light of the awakening to environment protection, various laws and regulations such as the Environmental Impact Assessment Act, 1992 and the Department of Petroleum Resources (DPR) Environmental Guidelines and Standards for the Petroleum Industry in Nigeria (EGASPIN: 2002) were enacted. These require corporate managements to consider the environmental implications of all internal decisions of their managements. Also, all organizations monitored by environmental policy agencies in Nigeria are expected to demonstrate much consideration in decision making. To this end, the study is specifically focused on:1. Examining the extent of environmental disclosure by Nigerian companies2. Ascertaining the nature and quality of information disclosed by these companies.Predicated on the above objectives, the following research questions will be addressed:1. To what extent does Nigerian companies disclose environmental information in their annual report?2. What is the nature and quality of the environmental information disclosed?Hypothesis Formulation:H0: The extent, nature and quality of environmental information disclosure by Nigerian firms have not improved.H1: The extent, nature and quality of environmental information disclosure by Nigerian firms have improved.

2. Review of Related Literature

2.1. The Concept and Principles of Environmental Accounting

- Environmental accounting covers information relating to all aspects of the environment. It includes environment - related expenditure, environmental benefits of products and details regarding sustainable operations (Irish times, 2000). According to the world conservative union consumption of natural capital- the depletion of natural capital - forests, in particular - is accounted for as income. Thus the accounts of a country which harvests trees very quickly will show quite high income for a few years, but nothing will show the destruction of a productive asset, the forest. Whereas in accordance with conventional business accounting principles, the gradual depletion of physical capital-machines and other equipment – are treated as depletion rather than income. However, most experts on environmental accounting agree that the depletion of natural capital should be accounted for in the same way as other productive assets.Yakhou and dorweiler (2003) specified that Environmental accounting is an inclusive field of accounting. It provides reports for both internal use, generating environmental information to help make management decisions on pricing, controlling overhead and capital budgeting, and external use, disclosing environmental information of interest to the public and to the financial community. Environmental Accounting enables organizations to track their environmental data and other greenhouse gas (GHG) emissions against reduction targets, and facilitates environmental reporting to provide sustainability related data that is comprehensive, auditable, and timely to advance and strengthen the interdependent and mutually reinforcing pillars of sustainable development - economic development, social development and environmental protection in Nigeria, (UNCTAD, 2003).The consciousness and need to protect the environment will make for environmental costs to be identified, accurately measured and reported. The term environmental cost does not only refer to costs paid to comply with regulatory standards, costs which have been incurred in order to reduce or eliminate releases of hazardous substances but all other costs associated with corporate processes which reduce adverse effect on the environment. Several definitions have been proffered for Environmental Accounting.Hansen and Mowen (2000) have defined environmental costs ‘as costs associated with the creation, detection, remediation and prevention of environmental degradation’ According to the US EPA (1995a:2), Green Accounting or Environmental Accounting is defined as: ‘Identifying and measuring the costs of environmental materials and activities and using this information for environmental management decisions. The purpose is to recognize and seek to mitigate the negative environmental effects of activities and systems’.Howes (2002) defines Environmental Accounting as ‘The generation, analysis and use of monetarized environmentally related information in order to improve corporate environmental and economic performance’ In his opinion Environmental Accounting does not only focus on internal and external environmental accounting but links environmental and financial performance more visibly. Environmental accounting assists in getting environmental sustainability embedded within an organization’s culture and operations. The aim is to provide decision makers with the information that enable the organization to reduce costs and business risks and to add value. According to Yakhou and Dorweiler (2003), Companies are expected to engage in environmental accounting to:◗ reassure consumers that they take their responsibilities seriously◗ comply with national guidelines◗ comply with financial reporting requirements◗ express the company’s environmental concerns and communicate them to a range of stakeholders.In other to understand the rationale behind environmental reporting, and the basis on which it is suggested that such reporting operates, it is necessary therefore to consider the principles upon which environmental reporting operates. There are three basic principles of environmental reporting as identified by Schaltegger, Muller and Hindrichsen (1996) includes: i) Sustainability: Sustainability is concerned with the effect which action taken in the present has upon the options available in the future. If resources are utilized in the present then they are no longer available for use in the future, and this is of particular concern if the resources are finite in quantity. Thus, raw materials of an extractive nature, such as coal, iron or oil are finite in quantity and once used, are not available for future use. At some point in the future therefore, alternatives will be needed to fulfill the functions currently provided by these resources. These may be at some points in the relatively distant future but of more immediate concern is the fact that as resources become depleted, then the cost of acquiring the remaining resources tends to increase and hence the operational costs of organisations tends to increase. The principle of sustainability in environmental reporting therefore implies that society must not use resources more than it can regenerate. This can be defined in terms of carrying capacity of the ecosystem (Hawken, 1993 and Davenport, 2000) and described with input- output model of resource consumption. 59 ii) Accountability: Accountability is concerned with an organization recognizing that its actions affect the external environment and therefore assuming responsibility for the effect of its actions. This principle therefore implies a quantification of the effects of actions taken, both internal to the organization and external. More specifically, the principle implies the reporting of those quantifications to all parties affected by those actions. This implies a reporting to external stakeholders of the effects of actions taken by the organization and how they are affecting those stakeholders. The principle therefore implies recognition that the organization is part of a wider societal network and has responsibility to that entire network rather than just to the owners of the organization. Accountability therefore necessitates the developments of appropriate measures of environmental performance and reporting of the actions of the firm. This necessitates costs on the part of the organization in developing, recording and reporting such performance and to be of value, the benefit must exceed the cost. Benefit must be determined by the usefulness of the measure selected to the decision-making process and by the way in which they facilitate resource allocation, both within the organization and with other stakeholders. iii) Transparency: Transparency as a principle in environmental reporting, means that the external impact of the actions of the organization can be ascertained from organisations reporting and pertinent fact are not disguised within that reporting. Thus, all the effects of the actions of the organization, including external impact, should be apparent to all from using the information provided by the organization‟s reporting mechanisms. Transparency is of particular importance to external users of such information as these users lack the background details and knowledge available to internal users of such information. Transparency therefore can be seen to follow from the other two principles and equally can be seen to be a part of the process of recognition of responsibility on the part of the organization for the external effect of its actions.

2.2. The Origin of Environmental Reporting and Its Practice in Nigeria

- There were many environmental problems threatening Nigeria both at pre-colonial and colonial times. Since the beginning of oil exploration and exploitation in Nigeria for instance, many environmental impacts emanated from oil activities but were not taken serious because oil is the major source of Nigerian economic growth (Musa 2011). Though environmental problems have been in existence in Nigeria, even before her independence, they only came into public awareness and attracted Medias’ attention in the 1980s. In 1988, some poisonous chemicals were discovered at a place called “Koko” in Bendel State (now divided into two states; Edo and Delta state). The discovery of 4,000 tons of toxic industrial wastes from Italy dumped illegally in the village escalated vigorous media attention (Babangida, 1989). This incident coupled with the previous attention received from the report "Our Common Future” by the World Commission on Environment and Development of 1987, pushed the then military government in Nigeria to institute FEPA. This Koko incidence triggered Nigeria to signing the Basel Convention. This Koko incidence started the framing of environmental policy and institution in Nigeria (Salau, 1997).National Policy on Environment (NPE) was the first environmental policy document to be produced by Nigeria. It was produced in order to achieve the desired environmental management goals in Nigeria, in a more legally binding and professional way. It was launched in 1989 by the federal environmental protection agency of Nigeria. And the revised version of the National Policy on Environment was launched in 1999 during the Nigerian constitution review. The National Policy on Environment emphasized so much on sustainable development; integration of economic activities with environmental improvement to achieve socio-cultural benefit for the citizens. The policy goals that are conspicuously mentioned in the document propose sustainable development; integration of economic activities with environmental improvement to achieve socio-cultural benefit for the citizens. The policy goals that are conspicuously mentioned in the document propose sustainable qualities in all measurements and these goals are: provision of suitable and quality environment to all Nigerians; marriage between the economic growth and environmental improvement; ensure sustainable use of Nigerian natural and environmental resources for the benefit of both the present and future Nigerian generations; and quests to enhance international corporation towards environmental improvement (FEPA, 1989). Although some developed countries have initiated mandatory disclosures in the reporting requirements, however, in most developing countries environmental disclosures still heavily rely on voluntary initiatives of the reporting entities.

2.3. Environmental Reporting Laws in Nigeria

- Environmental related Acts and Decree have been enacted in Nigeria before the inception of Nigerian independence under different context by her colonial master- Great Britain. These laws were scattered and uncoordinated as there was no fully organised institution to coordinate and discharge environmental related duties. In 1950s, the Criminal Code Act and Noxious Act were enacted to control odour and noise pollutions against neighbours. Later, the Public Health Acts were enacted aimed at vitiating the indiscriminate disposal of waste into the surrounding environment- especially water bodies, and its specific health goal was to reduce the spread of contagious diseases (Ola, 1984, cited in Chokor, 1993). At late 1960s and early 1970s, some Acts such as Water Courses Act of 1969, and Refining Act of 1974 were enacted to control oil pollution of land and navigable waters, and the fishing methods. The first legal document that made mention of environmental impacts and mitigation was the Fourth National Development Plan (1981-1985). This document urged the public and private industries to produce the environmental impact assessment (EIA) of their projects, and to acquire facilities for environmental assessments. Also, it called for researches and studies into Nigerian environmental features, and the reason for environmental quality standards and public environmental education.In 1979, the then Nigerian constitution stipulated the need for environmental hygiene, cleanliness, and refuge management of which the local government councils were delegated to supervise the activities. This law was made towards planning and beautification of the surrounding environment. But, there are some other laws directed towards environmental conservation and protection that were made by different sectors or ministries in Nigeria before the creation of environmental institution. These laws are mainly found in the oil industries for oil exploration and exploitation related activities, and the ministry of works and housing (before the creation of ministry of environment) was given the responsible to handle all environmental related activities. Such laws enacted in these ministries (ministry of petroleum and ministry of works and housing) for ecological conservations were/are: oil pipeline ordinance of 1965; oil in navigable water regulation of 1968; petroleum drilling and production regulation of 1969. And these laws were enacted and enforced by the department of Petroleum Resources (DPR) of Nigerian National Petroleum Corporation (NNPC is an oil corporation via which Nigerian government participates and regulates oil activities and operations in Nigeria). Though oil policies and other environmental related laws started some decades earlier than the national environmental policy (late 1960s), the beginning of environmental policy and laws started by the inception of the Federal Environmental Protection Agency of Nigeria (FEPA; it has the mandate to protect the Nigerian environment and also to design environmental guidelines, standards and criteria, and also to implementing and prosecute defaulters of environmental standards). But before FEPA’s formation, Lagos state in Nigeria had already instituted and setup a separate Ministry of Environment in 1979; being the first in the country. Infact, FEPA became “the supreme reference authority in environmental matters in Nigeria” (Adelegan, 2004). Around mid-1990s state authorities created their own environmental agencies known as state environmental protection agency (SEPA), charged with similar duties as FEPA, but at state level, and both have been working together since then to protect Nigerian environment (Adeoti, 2007). In 1989, Nigerian government produced National Environmental Policy (NPE: identifies the key sectors that should integrate environmental concerns with sustainable economic development and the strategies to achieve it), which was the first ever produced environmental policy in Africa. Nigeria never stopped there; in 1989 she signed the Basel Convention on Trans boundary Movement of Hazardous Waste- becoming the first in West Africa. These historical steps taken by Nigerian government towards environmental matters caused Nigeria to become prominent in environment matters, and Nigeria has signed about 30 conventions on the improvement of environment as of 1997 (Salau, 1997). Thereafter in 2000, FEPA was upgraded to a full functional ministry called the Federal Ministry of Environmental (FME: assumes FEPA’s duties and some environmental related duties from other ministries), Nigeria.

3. Research Methodology

- To analyze the level of corporate environmental disclosure practice in Nigeria, this study intends to evaluate the corporate environmental reporting practice among listed manufacturing firms in the Nigerian stock exchange. Content analysis was adopted in analyzing the content of the corporate annual reports of the selected listed firms. The content analysis method was adopted because it is one of the most systematic, objective and quantitative method of data analysis technique employed in other prior research studies involving corporate environmental disclosures practices (Wiseman, 1982; Deegan & Gordon, 1996; Hackston and Milne, 1996; Krippendorff, 2004). Furthermore, a survey research design was adopted to obtain the response of 40chartered accountant sampled.In order to find out the level of corporate environmental disclosure practice among the selected manufacturing companies in Nigeria, this study will measure the level of corporate environmental disclosure in terms of number of sentences disclosed given that the coded data is required to reflect the emphasis that companies make on each information categories based on Hackston & Milne's (1996) method. Previous research has used a number of methods, including proportion of pages of corporate environmental disclosure (Gray et al., 1995b), and number of words disclosed (Davey, 1982). Number of sentences disclosed was adopted because proportion of pages of disclosure does not consider different print and page sizes (Hackston & Milne, 1996). Number of sentences disclosed was also used because measuring number of words disclosed is time consuming as words are smaller and more numerous as a unit of measurement compared to sentences. Finally, according to Milne & Adler (1999), the construction of a categorization scheme is an essential stage in content analysis research. This involves the selection and development of categories into which content units can be classified (Tilt, 2000). The measurement instrument used in this study is adapted from Hackston & Milne‟s (1996) study. The measurement instrument to be used contains 16 content categories within four testable dimensions. These are summarized below: a) Theme: environment, energy, products and consumers, community involvement, employees and others (Ernst & Ernst, 1978) b) Evidence: monetary, non-monetary-quantitative and declarative (Ernst & Ernst, 1978). c) News type: good, bad and neutral d) Location in annual report: Chairman's Statement, Operations Review, Corporate Diary and Others

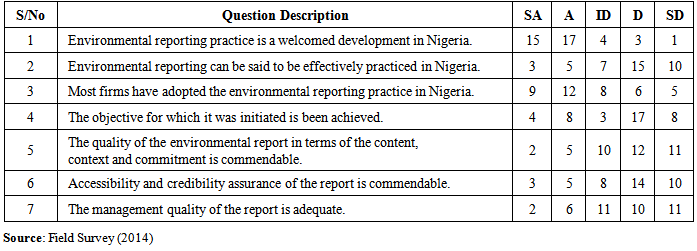

4. Analysis of Data and Test of Hypothesis

|

|

|

|

|

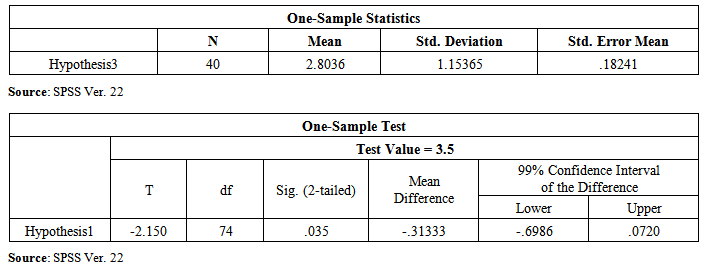

Decision Rule: t-computed (-2.150) < t-table value (2.756) with p-value < .05, we accept the null hypothesis, “The extent, nature and quality of environmental information disclosure by Nigerian firms have not improved”.

Decision Rule: t-computed (-2.150) < t-table value (2.756) with p-value < .05, we accept the null hypothesis, “The extent, nature and quality of environmental information disclosure by Nigerian firms have not improved”.5. Discussion of Findings and Conclusions

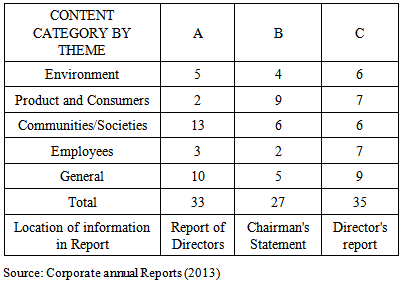

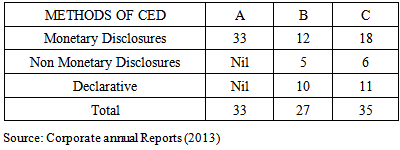

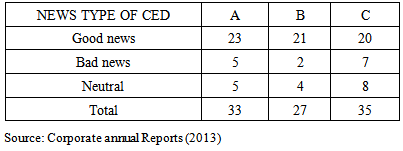

- Table 4.2 above gives a detailed breakdown of the number of sentences disclosed by companies as it relates to corporate environmental disclosures by themes. On the whole, it is seen clearly that companies are more highly disposed to disclosing environmental information in the area of Communities/Societies, products and consumers than in other areas.In line with previous studies, corporate environmental disclosures were categorized according to their methods, i.e., monetary, non-monetary quantitative and declarative. The different methods of environmental disclosures as used in the annual reports of the sampled companies are as shown in table 4.3 above. The findings here show that corporate environmental disclosures in company's annual reports are dominated by monetary disclosures. Companies here are more interested in reporting on corporate social responsibility issues rather than an outright declarative environmental disclosure statement.As in similar previous studies, corporate environmental disclosures were categorized into three groups based on their news type. The outcome as shown in table 4.4 indicates that about 67% of the sampled firms concentrated more on the disclosure relating to good news rather than bad and neutral news where about 15% and 18% were noticed respectively.

6. Conclusions

- Information disclosure policies have become a key component of environmental policy globally. This study concludes that most companies majorly disclose information related to products and consumers, employees and community involvement. It was also observed that the Corporate Environmental Disclosure (CED) practice of these companies contains little quantifiable data. The analysis results provided further evidence that CED practice in Nigeria is still very ad-hoc, general and self-laudatory in nature. The study therefore recommends the development of environmental disclosure standards that will harmonize the disclosure practices of firms as well as aid in providing environmental quantifiable data. This is necessitated by the need to solve the problem of entity based environmental disclosure practice which is rampant in Nigeria.