-

Paper Information

- Next Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2014; 3(2): 68-81

doi:10.5923/j.ijfa.20140302.03

Organizational Culture: Is-It an Explanatory Factor of Corporate Social Disclosure? A Validation Test in the Tunisian Context

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLDriss Rahma, Jarboui Anis

Department of Financial and Accounting Higher Institute of Business Administration (ISAAS), Tunisia

Correspondence to: Jarboui Anis, Department of Financial and Accounting Higher Institute of Business Administration (ISAAS), Tunisia.

| Email: |  |

Copyright © 2014 Scientific & Academic Publishing. All Rights Reserved.

The objective of this paper is to test the contribution of organizational culture on the decision of social disclosure in the annual reports of the Tunisian companies. In fact, we try to identify the cultural characteristics of the organization that motivates a firm to publish societal information. In our paper, the studied cultural characteristics are: involvement, consistency, adaptability and mission. The development of theoretical corpus allowed us to reformulate four research hypotheses. To measure the dependent variable, we use the technique of content analysis of five-year annual reports of 23 Tunisian firms (2007 to 2011). As for organizational culture, we followed the paradigm approach of Churchill [27]. Our results led us to conclude that culture is an explanatory factor of the extent of social disclosure through these cultural traits: involvement, consistency and mission.

Keywords: Social disclosure, Organizational culture, Content analysis, Annual reports

Cite this paper: Driss Rahma, Jarboui Anis, Organizational Culture: Is-It an Explanatory Factor of Corporate Social Disclosure? A Validation Test in the Tunisian Context, International Journal of Finance and Accounting , Vol. 3 No. 2, 2014, pp. 68-81. doi: 10.5923/j.ijfa.20140302.03.

Article Outline

1. Introduction

- In recent decades, there has been a continuous development of the concept of corporate social responsibility. Indeed, with the great contemporary social and environmental issues, a company is obliged to be socially responsible while exceeding the purely economic and financial interest. Currently, the company is required to strengthen its relationships with its stakeholders and to share its social responsibility. Therefore, the practice of social disclosure ensures the relationship of trust between the companies and its stakeholders.Several studies have focused on issues related to the scope, nature, extent, which identify the level and determinants of such a practice in the developed countries. However, few studies that examined this practice in the Tunisian context are voluntary and subject to the management discretion. Moreover, the explanatory factors are related to the internal and external characteristics of the company and ignore the cultural factors because of the measurement problems faced by researchers.Through this study, we try to answer the following research question about organizational culture: is-it an explanatory factor of social disclosure in the annual reports of the Tunisian companies?The remainder of this paper is organized as follows: first, we present the theoretical corpus in order to achieve the development of four major research hypotheses. Then, we present the methodological aspect of our paper. Finally, we discuss the generated results.

2. Theoretical Corpus

- According to Sharma [51], who set up a framework for corporate social disclosure, we can say that there is no complete theory that can precisely explain social disclosure. Therefore, we find that the majority of studies dealing with social disclosure are based on the stakeholder’s theory and the legitimacy theory [8, 31, 7, 6].

2.1. Stakeholder’s Theory

- The stakeholder’s theory plays a crucial role in the development of the current research dealing with social disclosure. Indeed, the main objective set by an officer, through practicing social disclosure, is to meet the expectations of the different stakeholders.According to this theory, the company is at the heart of a set of relationships not only with those who are the shareholders (the Shareholders), but also with not only those who are directly or indirectly involved in the decision- making and in activities of the company and who are concerned with the impact of these decisions on the common economic, social, cultural and environment (the stakeholders) [18]. To this end, several research projects are based on the stakeholder theory as a theoretical foundation of the decision of social disclosure [54, 49, 14, 42, 9, 60].As a result, the information’s about the social responsibility of the company which is disclosed to the public can provide a solid basis for the dialogue between the company and its stakeholders.

2.2. Legitimacy Theory

- Legitimacy theory has been requested by a variety of researches [29, 46, 13, 5, 41, 4, 2, 10, 43]. Under this theory, companies must operate within the rules and standards, which are generally accepted by the society.In this context and according to Brown and Deegan [5], the legitimacy theory can be defined as the fact that organizations are always to operate within the standards generally accepted by the community in which they operate. To do so, they must publish enough societal information to be considered as good citizens by the Company [59]. Therefore, operating in a lawful manner is particularly respecting the Company. In fact, the legitimacy theory is essentially based on respect for the social contract that binds the organization to the society in which it can operate.

3. Development of Research Hypotheses

- In what follows, we try to reformulate the assumptions of our research through theoretical developments.

3.1. Organizational Culture

- Culture has been the subject of many interpretations through the literature of the social sciences. However, after reviewing the literature on culture, we concluded that there is no consensus to define the ambiguous term [35].In the same context, culture is the most elusive term in the vocabulary of the social sciences [33]. However, this does not prevent us to state some definitions provided by previous authors. The culture means the attitudes, beliefs and values of a society [21]. Moreover, it includes knowledge, belief, art, law, morals, customs, and other capabilities that distinguish one group from other groups [56].Culture can be defined as a collective mental programming [30]. It is, essentially, the part of our ideas that we share with members of our society, our region, our group, but not of other nations, other regions. One of the first studies about the impact of the cultural dimension of information disclosure was Jaggi [32]. In addition to financial market development, several factors, including the cultural environment, can influence the strategies followed by the company, among other things, social disclosure decision [32]. Throughout literature, there are several researches that have focused on studying the influence of the cultural factors on the strategies of information disclosure via the company’s annual reports or other informational supports.After defining the concept of organizational culture, we propose to test the effect of the cultural dimension on the extent of social disclosure. To do this, we rephrase the following research hypothesis:H1: Organizational culture is a decisive explanatory factor of the practice of social disclosure in annual reports.The question that arises at this level is: what are the cultural characteristics of the organization motivating a firm to publish societal information?In this context, we made a literature review using the cultural factor as an exogenous variable in authors’ empirical models [30, 15, 28, 55, 44, 53]. In our research, we will rely on the study of Fey and Denison [22] entitled “Organizational Culture and Effectiveness: Can American Theory Be Applied in Russia?”. The concept of organizational culture can be identified through four axes, which include: involvement, consistency, adaptability and mission [22]. Subsequently, we will present an explanation of these components as it was provided by Fey and Denison [22] in their article. The analysis of the organizational culture requires the reformulation of four sub-hypotheses.InvolvementIn a climate of trust and mutual respect, leaders, managers and employees are committed to the company to which they belong. They participate, thereafter, in the decision-making process which has a direct link with the objectives set by the organization. Therefore, organizations with a high degree of involvement of their customers and employees give more importance to the social, environmental and financial side. They are, then, more interested in the disclosure of societal information in their annual reports.H1a: Firms with a high degree of involvement tend to disclose more societal information on annual reports.ConsistencyThe staff and the respective line managers are able to reach an agreement even if they do not share the same views [50]. Consistency, as a source of stability and internal integration, results from a common state of mind. Thus, an organization characterized by a coordination between departments and stakeholders will be encouraged to disclose more societal information.H1b: Firms with high coherence orientation tend to disclose more societal information on annual reports.AdaptabilityAdaptable organizations are those largely influenced by their customers [39, 50]. Thus, among the accepted contributions from an organization's customers we can include openness to innovation. In the same context, several studies consider that innovation is an organizational culture expressed in various ways. For example, it goes in the same direction as in the study of Wilderom et al. [57] with adaptability of Fey and Denison [22] and high-performance in the work of Mathew [36]. As a result, businesses encouraging innovation and adaptability tend to disclose information related to the environmental adaptability and innovative strategies followed by the leaders. This information is a part of the societal information.H1c: Firms with high adaptability tend to disclose more societal information on annual reports.MissionSuccessful organizations are those that linger to establish goals and define their strategic objectives in order to determine, even in a preliminary way, a complete vision of the future [48]. Therefore, to achieve their objectives, they have to establish a list of missions. This will have a direct impact on the decision-making of societal disclosure.H1d: Firms with high mission orientation tend to disclose more societal information on annual reports.

3.2. Control Variables

- After presenting the cultural factor, we indicate the following control variables that will strengthen our empirical model. These variables are mainly: performance, sector of activity and workforce. PerformancePart of the previous studies has resulted in a positive relationship between the realization of profits and the decision-making of societal information disclosure [49, 10, 23]. In contrast, other studies have found the no relationship [11, 3, 45, 43]. Therefore, we reformulate the research hypothesis as follows:H2: Performance has a positive impact on the practice of corporate social disclosure in annual reports.Sector of activitySeveral researches have verified a significant relationship between the level of social disclosure and the industry in which a company operates [40, 37, 24, 1, 52, 12]. Hence, we can reformulate the following hypothesis:H3: The sector of activity has a positive impact on the practice of corporate social disclosure in annual reports.WorkforceReferring to previous results, we find that the relationship between size and social disclosure decision-making is positive. In fact, the organization is required to publish more information about the climate, working conditions, the environment, hygiene ... and everything about the social aspect. Hence, our hypothesis is as follows:H4: The size of the firm has a positive impact on the practice of corporate social disclosure in annual reports.

4. Methodology

- To achieve our research objective, we follow a concise and structured methodology to answer our primary research question.

4.1. Sample, Study Period and Data Collection

- Our sample consists ultimately on 23 Tunisian companies after subtracting the companies belonging to the financial sector such as banks, financial institutions, insurance companies and investment firms (SICAF, SICAR and SICAV) and companies that we were not able to obtain complete data.Our empirical application covers a five-year period from 2007 to 2011.To achieve this empirical application, we use several data sources. Thus, data collection requires the monitoring of two main steps:The first step concerns data of the dependent variable and the control variables. It contains three main sources of data, namely, the annual management reports, annual reports and auditor’s sheets overview of companies. The second step involves the organizational culture which was measured through the distribution of a questionnaire to the same sample of firms.

4.2. Measurement of Variables

- Like all research, our empirical application contains a variable to be explained and explanatory variables.

4.2.1. The Dependent Variable: Social Disclosure

- To measure the social disclosure, we are based on the technique of content analysis of annual reports which allows us to classify information in the analyzed reports as societal information. To do this, we must follow the approach used by Ernst and Ernst [19] to analyse societal information to achieve our empirical application. So, we use this list of items related to social disclosure:Category (1): EnvironmentSub- Category (1): PollutionItem (1): Respect of standards for pollutionItem (2): Efforts made to reduce pollutionItem (3): Repair damage resulting from activitySub- Category (2): Recycling Item (1): Conservation of natural resources Item (2): Use of recycled materialsItem (3): Waste recoverySub- Category (3): EnergyItem (1): Optimal use of resources throughout the production processItem (2): Waste prevention Item (3): Reduction of energy consumption Sub- Category (4): Other Item (1): Contribution to the protection of natureItem (2): Monetary donations to help the protection of environment Category (2): Products Sub- Category (1): Research and development Item (1): Information related on development of products Item (2): Costs of research and development Item (3): Information related on improving future productsSub- Category (2): QualityItem (1): Information related on quality of productsSub- Category (3): Security Item (1): Information related on the product security Item (2): Information indicating compliance with the safety standard Item (3): Information on strengthening health qualities in the production processItem (4): Information related on the products safetySub- Category (4): OtherItem (1): Other information related to productsCategory (3): Human resources Sub-Category (1): Information on general working conditions Item (1): Terms of hygiene and safety Item (2): Employee motivation Item (3): Information on absenteeismItem (4): Improving general working conditionsItem (5): Provide medical support to the employee Sub- Category (2): Analysis and development of staff Item (1): Workforce Item (2): Distribution of employees by employment contract Item (3): Rotation or changing employees Sub- Category (3): Information on recruitment policies and compensation Item (1): Reasons for change in number of employees Item (2): Layoffs Item (3): compensation policies Item (4): Relationships with unions Item (5): Staff strikes and social conflicts Sub- Category (4): Training Item (1): Training plan Item (2): Number of trained employees Item (3): Training time Item (4): Training expenses Sub- Category (5): Other Item (1): Information on employee’s seniority Item (2): Information on work accidents Item (3): Social climate and work environment Category (4): Community involvement Sub- Category (1): ArtsItem (1): Donations for the arts Item (2): Sponsoring actions artsSub- Category (2): EducationItem (1): Donations for teaching and educationSub- Category (3): Human health Item (1): Donations for health Item (2): Help to the local employment development or other local activitiesRegarding the unit of measurement of societal information, we will use the number of sentences written in the annual reports of companies tested.

4.2.2. The Independent Variable: Organizational Culture

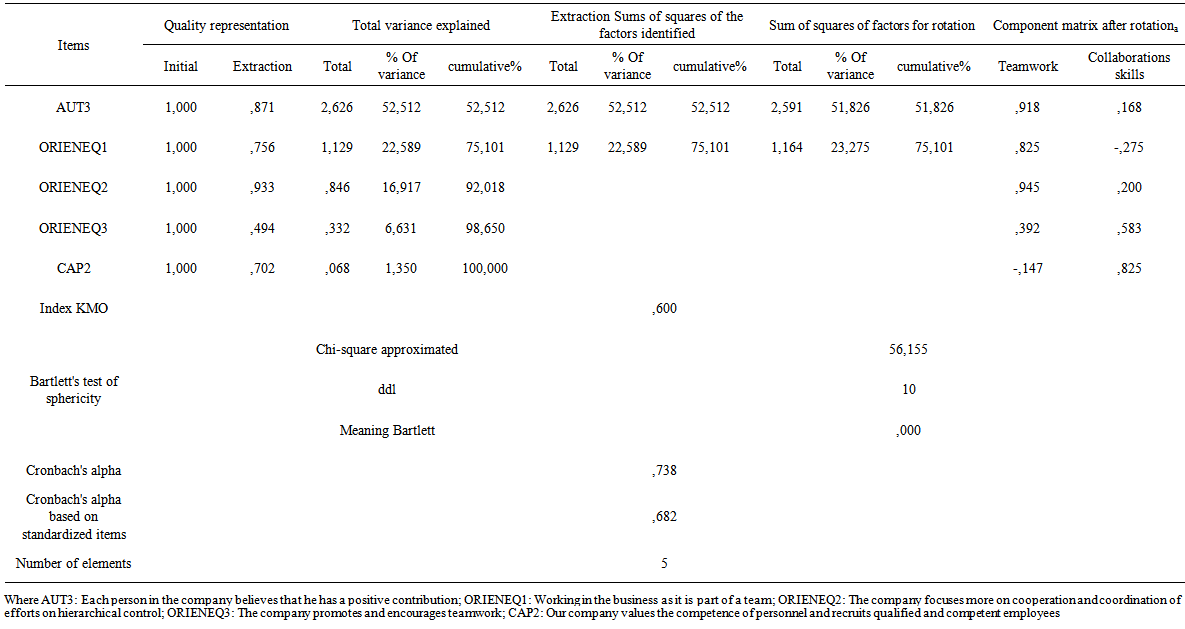

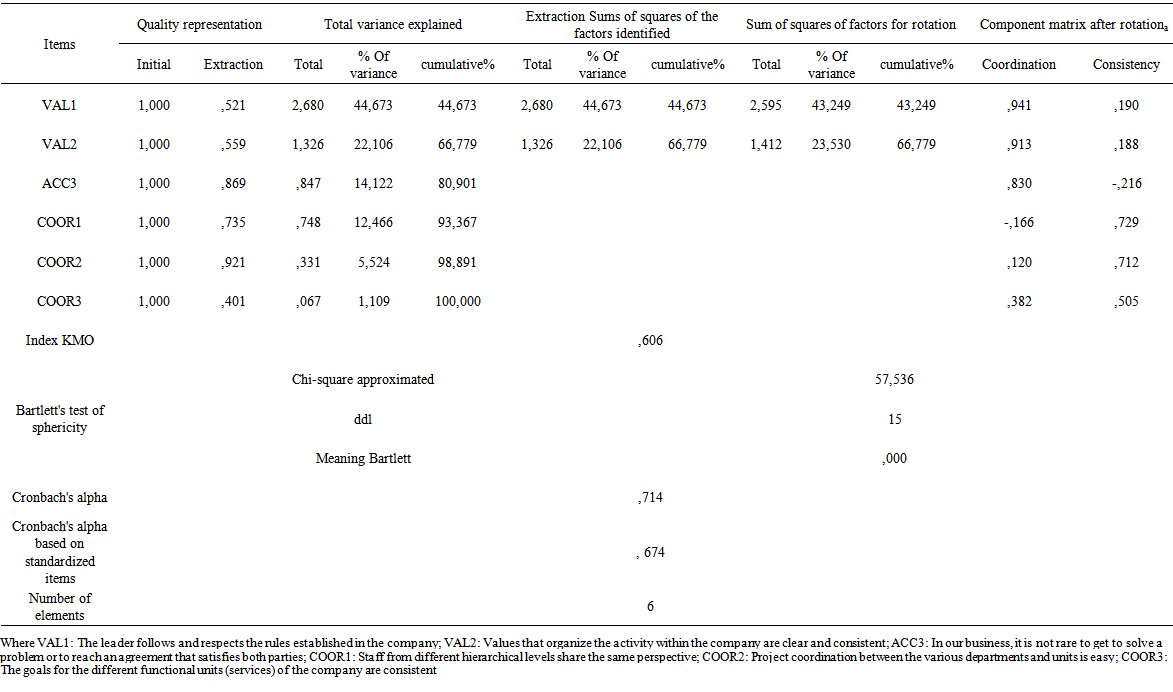

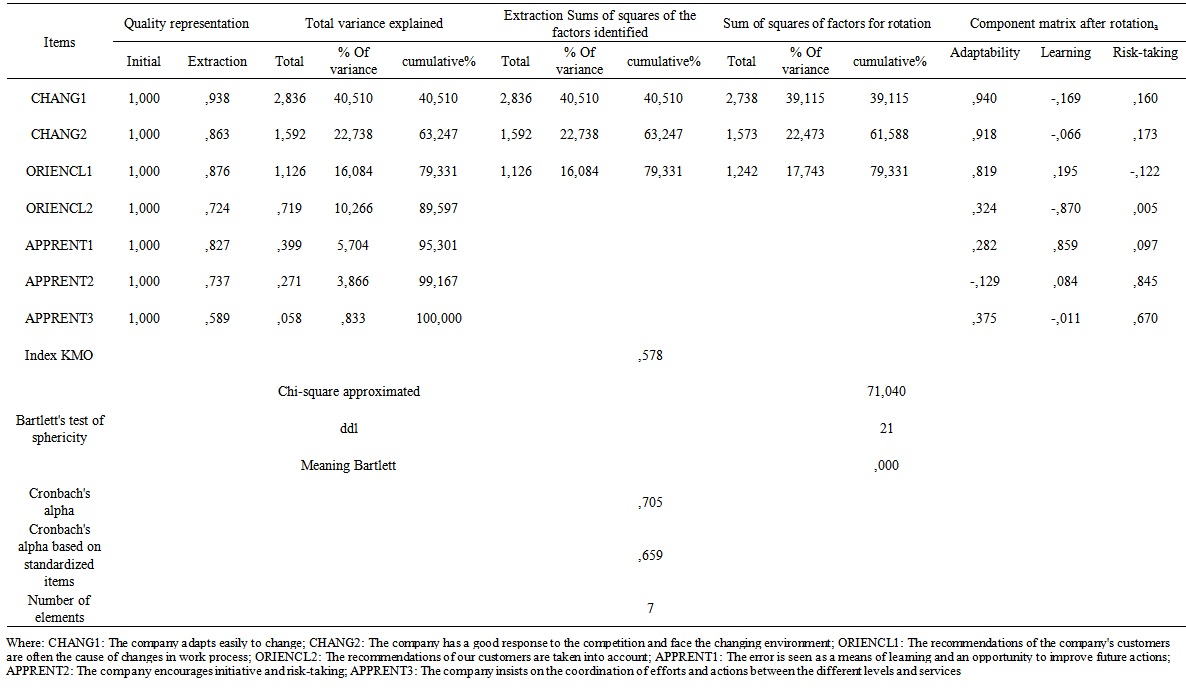

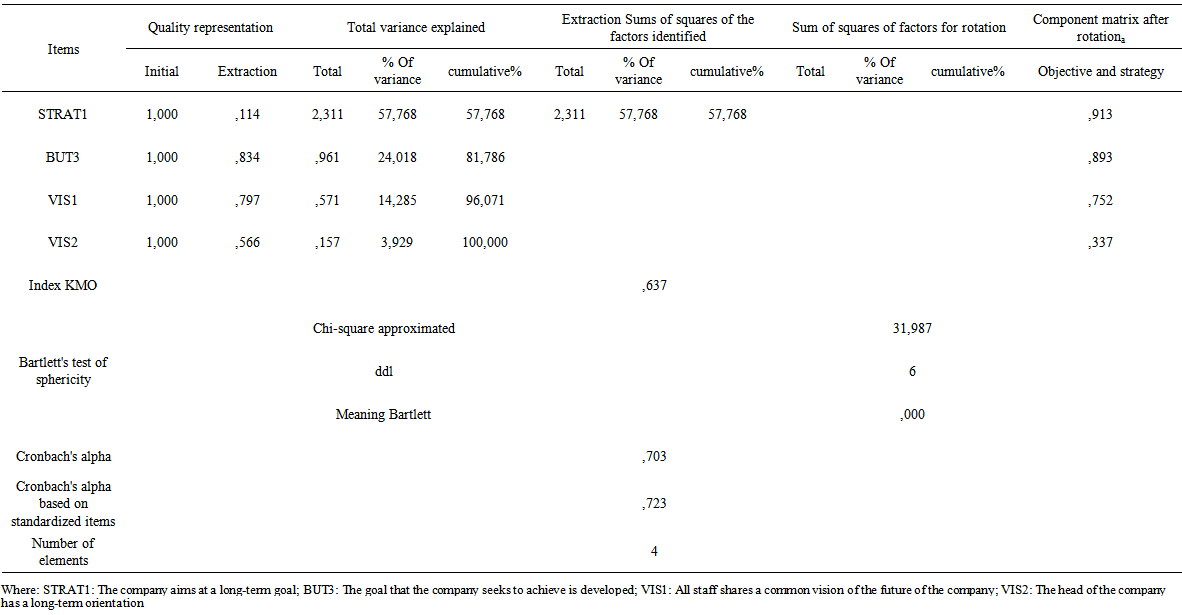

- The methodology applied is the use of scales of Liquert through the application of the paradigm of Churchill [27]. Indeed, these scales will follow the answers to the questions listed in the questionnaire distributed to companies. These answers will help us to evaluate items related to the culture which we are trying to measure and which will be made explicit in a list of items related to analysis of organizational culture. Cultural Trait n°1: Involvement First component of Involvement: The authority Item n°1: The decision is always taken by the most knowledgeable people in the business.Item n°2: Information is communicated to all levels so that everyone can easily get the information which they need at the right time.Item n°3: Each person in the company believes that he has a positive contribution.Second component of Involvement: The orientation teamItem n°1: Working in the business as it is part of a team.Item n°2: The company focuses more on cooperation and coordination of efforts on hierarchical control.Item n°3: The company promotes and encourages teamwork. Third component of Involvement: Capacity of development Item n°1: Compared to our competitors, our company is in a state of continuous improvement at all levels.Item n°2: Our company values the competence of personnel and recruits qualified and competent employees.Item n°3: Competence of human resources is considered by our company as a competitive advantage and competitive.Cultural Trait n°2: Consistency First component of Consistency: Core values Item n°1: The leader follows and respects the rules established in the company.Item n°2: Values that organize the activity within the company are clear and consistent. Item n°3: In our company, we refer to a code of ethics that guide our behavior and clarifies that everyone has the right to do and not do. Second component of Consistency: The agreement Item n°1: Faced with a situation of disagreement, we always try to find a solution that satisfies both parties.Item n°2: It is always possible to reach a consensus even in the most difficult cases.Item n°3: In our business, it is not rare to get to solve a problem or to reach an agreement that satisfies both parties.Third component of Consistency: Coordination and integrationItem n°1: Staff from different hierarchical levels share the same perspective.Item n°2: Project coordination between the various departments and units is easy.Item n°3: The goals for the different functional units (services) of the company are consistent.Cultural Trait n°3: Adaptability First component of Adaptability: Change Item n°1: The company adapts easily to change.Item n°2: The company has a good response to the competition and face the changing environment.Item n°3: The company is innovative and continues to improve its working methods. Second component of Adaptability: Customer orientation Item n°1: The recommendations of the company's customers are often the cause of changes in work process.Item n°2: The recommendations of our customers are taken into account.Item n°3: Client’s interests are sometimes ignored in the decisions of the company. Third component of Adaptability: Organizational learning Item n°1: The error is seen as a means of learning and an opportunity to improve future actions.Item n°2: The company encourages initiative and risk-taking.Item n°3: The company insists on the coordination of efforts and actions between the different levels and services.Cultural Trait 4: Mission First component of Mission: Strategy Item n°1: The company aims at a long-term goal.Item n°2: The company's goal is clear and gives meaning to the work of staff.Item n°3: The company develops a good and clear strategy for the future.Second component of Mission: Purpose and objectives Item n°1: All company managers agree on the goals set by management.Item n°2: The goals of the leader are ambitious and achievable.Item n°3: The goal that the company seeks to achieve is developed.Third component of Mission: Vision Item n°1: All staff shares a common vision of the future of the company.Item n°2: The head of the company has a long-term orientation.Item n°3: The projection of the company in the future is a motivator for staff.In what follows, we will analyze data related to cultural traits emerged from our questionnaire.To test the possibility of performing a factor analysis of our data, we used to determine the index of KMO and the Bartlett's test. However, to ensure a better representation of our items, we are obliged to remove some items and continue to validate our scales. Finally, we select items having a good quality of representation (> 0.4) as it is presented in Table 1.On our results, KMO is up from 0.6 is much higher than 0.5 what feels factor analysis is possible with items of involvement. This result is confirmed by Bartlett's test with significance equal to 0. Subsequently, our goal through this factor analysis is done to summarize the information in a few relevant dimensions formed by a combination of a set of items. To do this, in order to achieve the determination of the factors, we must apply the rule of Kaiser saying that we can not hold that the factors having proper values greater than 1. The factors have a value 2.591 and 1.164. The table shows the total variance explained two dimensions that summarize information. The two dimensions explain 75.101% of the total variance.We recommend, in general, stopping extracting factors when 60% of cumulative variance was extracted. This indicates that the cumulative variance reduction variables in two components keeps the essence of the phenomenon measured by five items finally selected. So, our representation of the first cultural trait of the involvement has a quality. Then, the component matrix shows the extracted dimensions with the components. Each column corresponds to a dimension containing the extracted factors or components that can be interpreted as correlation coefficients. From this matrix, we conclude that, on the one hand, the three items "Every person in the company believes that it has a positive contribution," "Working in the business is as part of a team "and" The company focuses more on cooperation and coordination of efforts on hierarchical control "belong to the first dimension which we give new name as" Teamwork ". On the other hand, the two items "The company promotes and encourages teamwork" and "Our company values the competence of personnel and recruits qualified and competent employees" belong to the second dimension which will be called "Collaboration skills".In this regard, we pass the test of reliability of the data based on the determination of Cronbach's alpha. The Cronbach's alpha related to the items level of commitment is up to 0,738. It is, therefore, a good value (between 0.7 and 0.8) [16]. Subsequently, we can approve the internal reliability of our scale.Concerning, the measurement of scale related to consistency, we have retained only six items among nine items starting up this scale. Through the results of the empirical validation of the measurement scale, we find that the KMO value was 0.606 which is as much greater than 0.5. As a result, the factor analysis is feasible with the items selected on coherence. The factors have a value 2.595 and 1.412. The table 2 shows the total variance explained two dimensions that summarize information. The two dimensions explain 66.779% of the total variance.Analysis of the first cultural trait: Involvement

| Table 1. Results related on first cultural trait: Involvement |

| Table 2. Results related on first cultural trait: Consistency |

| Table 3. Results related on first cultural trait: Adaptability |

| Table 4. Results related on first cultural trait: Mission |

4.2.3. The Control Variables

- In our research, we test the impact of three control variables on the decision to disclose societal information on annual reports. These variables include:Performance: Among the variety of methods, we include the main measures: the ratio Return on equity (ROE) [45, 49, 42] ... Return on Assets ratio (ROA) [45, 58, 12]… In our research, we adopt the following ratio: the ratio between the income and revenue used by many researches.The sector of activity: In our research, the sector of activity is a binary variable (dichotomous) which takes (1) if the company operates in a sensitive area to the problems of society and the environment (automotive sectors and equipment, industrial goods and services industry, the chemical, oil and gas sectors and health sectors), (0) otherwise.Workforce: This variable is measured by the number of employees working in the company.

4.3. Model

- Our research goal is to test if the corporate culture constitutes one of the factors explaining the practice of social disclosure in annual reports. To achieve our goal, we propose to try to validate empirically, in the Tunisian context, the following model:Social Disclosure = Organizational Culture + Performance + Sector of activity + workforceAfter measuring the main explanatory variable "organizational culture", we can present our research model with more specificity and accuracy:Social disclosure = α0 + α1 Teamwork + α2 Collaboration skills + α3 Coordination + α4 Consistency + α5 Adaptability + α6 Learning + α7 Risk-taking + α8 Objective and Strategy + α9Performance + α10 Sector of activity + α11Workforce+ε.The data used to work are considered panel data. Indeed, our empirical validation based on data from 23 Tunisian firms listed in Tunis for five years that (2007 to 2011). At this level, the econometric model proposed to be estimated can be presented as follows:Yit = α0 + α1 X1it + α2 X2it + α3 X3it + α4 X4it + α5 X5it + α6 X6it+ α7 X7it + α8 X8it + α9 X9it + α10 X10it + α11 X11it + εit.Where: Yit= Social Disclosure; X1= Teamwork; X2= Collaboration skills; X3= Coordination; X4= Consistency; X5= Adaptability; X6= Learning; X7= Risk-taking; X8= Objective and Strategy; X9= Performance; X10= Sector of activity; X11= WorkforceWith: i = 1,2,3,4,5,6,7,8,9,10……….23; t = 2007….. 2011.Thereafter, it should be noted that to perform our multivariate regression of the econometric equation presented, we will take as assumption that cultural variables are considered stable throughout the study period because answers to the questions proposed will be unchangeable from one year to another.

5. Results

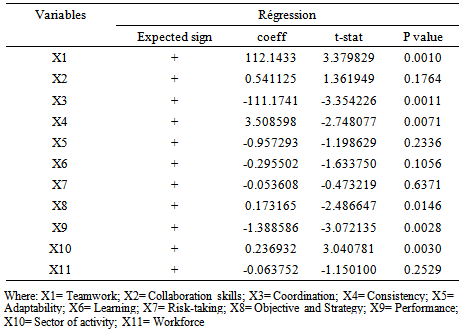

- At this level, it should be noted that we have adopted an empirical estimation by OLS (Method of ordinary Least Squares) on panel data using the software Eviews 5. This led us to introduce the following table which summarize the main findings emerged:

|

5.1. Hypothesis Concerning the Organizational Culture

- The assumption of the organizational culture has been deducted, using the theoretical development presented in four sub-hypotheses. These sub-hypotheses are:InvolvementThe level of involvement was represented by two cultural traits which are: teamwork and collaboration skills that were noted in the econometric model X1 and X2 respectively. Among these variables, the first is significant at the 1% level with a positive sign.In conclusion, the involvement is considered an explanatory factor in the practice of social disclosure. In fact, by analyzing the results of our study, we find that firms with a high degree of involvement are able to disclose more societal information in their annual reports. In fact, successful companies are trying, through their management strategies to integrate the different hierarchical levels in their main concerns and even daily. This strategy requires the presence of a spirit of cooperation and teamwork. It is a culture of communication adopted to promote good working conditions and a healthy environment and have better results. Therefore, these companies are interested in managing them, to the societal aspect which summarizes all the social and environmental issues. This implies that the level of disclosure increases with societal concerns of the company to meet the societal information needs of internal stakeholders involved in management decisions as well as stakeholders who need maximum of societal information in annual reports. ConsistencyConsistency was represented finally by two main variables, namely: coordination (X3) and consistency (X4). Regarding the variable X3, we find that it is significant at the 1% level but with a negative sign. This implies that coordination has a negative impact on the practice of corporate social disclosure in annual reports of Tunisian companies. For the variable X4, we find that it is significant at 1% with a positive sign.Hence, the hypothesis of consistency has been validated. So, consistency has a remarkable effect on the social disclosure. This can be explained by the fact that the disclosure of more societal information is an action resulting from the consistency in the decision- making by the company itself in the presence of several participants in this decision. This highlights the orientation of decision makers and this will be realized through the annual reports because they have material to disclose. In conclusion, avoiding the problems of disagreement between actors, and on the basis of an organizational culture of consistency, a company will be able to provide more information dealing with the environment and society. AdaptabilityThis assumption has not been validated. So, adaptability has no effect on the decision- making to disclose societal information on annual reports. This can be explained by the fact that, for our sample of research, company’s adaptable to external, specifically to the choice of customers, do not use social disclosure. This result can be strengthened by the first result on the level of involvement that is to say, the internal integration of stakeholders in the decision- making. In fact, theoretically, internal integration and external adaptation can often disagree [39, 50]. Therefore, the involvement is an explanatory factor of societal information’s disclosure, adaptability does not affect this practice.MissionThe dimension generated for the mission was named goal and strategy (X8). This variable is significant and positively correlated with the endogenous variable. This implies that mission is correlated with social disclosure practice through the establishment of a long-term goal. Indeed, giving importance to the setting of targets to track and process work to be undertaken, a company will be able to disclose more societal information. However, the main objective of a company is to meet the expectations of stakeholders.

5.2. Hypotheses about the Control Variables

- Control variables tested in our research are: performance, sector of activity and workforce. Firstly, performance, denoted by X9 has a significant impact on the model at the 1% with a negative sign. In fact, more than the Tunisian firms are less efficient they are concerned about societal voluntarily publish information in their annual reports. This can be explained by the costs incurred by disclosing such information.Secondly, the sector of activity is denoted by X10 in our model. This variable has a significant and positive effect on the social disclosure. In reality, this can be interpreted by the fact that the work in polluting industries requires companies to disclose information addressing environmental and social aspects to clarify the impact of these activities carried out by the company on the environment and society, including the working conditions of human resources. Finally, the hypothesis related to workforce has not been empirically validated. Indeed, this variable denoted by X11 is not significant. Therefore, it has no impact on the model tested. In conclusion, for our sample, the workforce that reflects the company size has no effect on the decision- making of societal disclosure.

6. Conclusions

- Several research studies have focused on topics relating to the social disclosure in annual reports of companies [38, 34, 61, 25, 47, 20, 26, 17]. In fact, the most of these studies have tested the impact of some internal company characteristics on the practice of corporate social disclosure. About this, we can give some examples of internal determinants such as the parameters of governance, debt, capital structure ... The main objective of our study was to test the influence of cultural factors on the practice of corporate social disclosure in annual reports of Tunisian companies. To measure the level of social disclosure, we use the technique of content analysis of annual reports. Concerning the organizational culture, we followed the paradigm approach of Churchill [27] to identify the main dimensions of the cultural factor to remember and to test their impact on the level of societal information disclosure. Theses cultural characteristics of the organization which motivate a firm to practice the social disclosure are, in our paper, involvement, consistency, adaptability and mission. In addition, we tested the contribution of three control variables in our model, these variables include: performance, sector of activity and workforce. Finally, as a result, we concluded that organizational culture has an influence on the practice of societal disclosure through the involvement, consistency and mission. Then, we find that firms with a high degree of involvement, a high coherence orientation and a high mission orientation tend to disclose more societal information through their annual reports. Concerning the control variables, the hypotheses related to performance and sector of activity have been validated.