-

Paper Information

- Next Paper

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2013; 2(4): 225-238

doi:10.5923/j.ijfa.20130204.06

Corporate Environmental Reporting in Tanzania; How Far have We Gone? A case of Manufacturing Companies Listed in Dar ES Salaam Stock Exchange (DSE)

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLKilugala Malimi

Faculty of Business University of Arusha, P. O. BOX 7, Usa River, Arusha, Tanzania

Correspondence to: Kilugala Malimi, Faculty of Business University of Arusha, P. O. BOX 7, Usa River, Arusha, Tanzania.

| Email: |  |

Copyright © 2012 Scientific & Academic Publishing. All Rights Reserved.

Over the recent years, issues relating to environment have preempted headlines, UN agendas, and debates in the general public. Air pollution, land degradation, water pollution, and depletion of ozone layer, to mention a few, have caused pierce reactions from various groups around the world. Reports show that the world is highly polluted due to human activities which leave unmanaged wastes to scatter around the open areas and water bodies, therefore, affecting the world’s ecosystems. The situation in Tanzania is not exceptional; the environment is getting seriously affected by the improperly disposed wastes. Unfortunately, the country has no laws or regulations mandating disclosure of environmental information in company’s annual accounts. As a result of environmental debates, the accounting discipline has been hugely moved by the fact that risks associated with the environmental performance of companies increase with the increasing public demand for corporate environmental reporting. In many countries therefore, corporate environmental reporting have become common if not a compulsory part of company’s annual disclosure. This study deals with corporate environmental reporting among the listed companies in Tanzania. Manufacturing companies are particularly sampled for the study due to the fact that the manufacturing activities often generate a lot of wastes which necessitate comprehensive disclosures. During the four years studied (2008 to 2011), corporate interest in environmental reporting have drastically grown. However, the environmental reports did not cover many of the significant environmental issues; therefore, the current reporting is not sufficient in terms of extent and the scope of coverage. The failure of the existing environmental reporting to grasp some of the important aspects of environmental disclosure is attributed to lack of laws, guidelines, and standards mandating comprehensive disclosure. Therefore, the legislature, National Board of Accountants and Auditors, and the Dar es salaam Stock Exchange should enforce corporate environmental reporting in the annual reports.

Keywords: Corporate Environmental Reporting, Dar ES Salaam Stock Exchange (DSE), The State of Environment Report (Soer), United Republic of Tanzania (URT)

Cite this paper: Kilugala Malimi, Corporate Environmental Reporting in Tanzania; How Far have We Gone? A case of Manufacturing Companies Listed in Dar ES Salaam Stock Exchange (DSE), International Journal of Finance and Accounting , Vol. 2 No. 4, 2013, pp. 225-238. doi: 10.5923/j.ijfa.20130204.06.

Article Outline

1. Introduction

- Just like most of the business activities, manufacturing activities heavily interacts with the environment. Ranging from extraction of raw materials, construction of industrial sites, to disposal of wastes, the environment inevitably becomes the host to many of these manufacturing activities. Unfortunately, some of the manufacturing activities pose negative impacts to the hosting environment resulting into costly damages. The environment referred here comprises of natural physical surroundings and includes air, water, land, flora, fauna and many non-renewable resources, such as fossil fuels and minerals (UN, 1998). Thus, some manufacturing activities negatively interact with the fore mentioned components of our environment. But often these interactions go unreported year after year making both the business firm and its stakeholders unaware of the extent to which the environment has been damaged, ultimately no control is exercised to the damaging activities. In recent years, environmental issues have drawn a serious concern at both national and international arena. Some say, the last decade of the twentieth century has been regarded as the decade of the environment (Mayya, 2009). Environmental degradation all over the world has led to a very grim picture of the state of natural resources we see today. Increase in water pollution, atmospheric pollution, pollution of coastal areas, decrease in size of forests, increase in emissions of greenhouse gases (GHGs), over-exploitation of land, dumping of waste matter and increase in pollutants, just to mention a few, have contributed to the threats faced by biodiversity and ecology of the Earth (ASOSAI, 2007). The impact of environmental degradation on water, land, forests, biodiversity, climate, atmosphere and marine/coastal areas draw and invite a significant attention that cannot be undermined. Meanwhile, Public and political concerns regarding environmental issues have been brought into sharp focus by highly publicised environmental disasters such as the British Petroleum Oil (BP) spillage in the Gulf of Mexico, Exxon Valdez, Chernobyl, Love Canal, Union Carbide at Bhopal, the explosion of the AZF chemical plant in France and the massive coal-ash spill at a Tennessee Valley Authority power plant, just to mention a few (Chiang, 2010).Records show that manufacturing activities have played a big role in degrading the environment we live in today. Reports reveal that each year tons of discarded wastes from the industrial activities find their way into the oceans, killing hundreds of thousands of marine mammals and ocean-going birds, and untold numbers of fishes (UNEP, 2007). The world’s seas and oceans are becoming increasingly tainted by untreated waste water, air-borne pollution, industrial effluent and silt from inadequately managed watersheds (UNEP, 2007). Thus, manufacturing activities are the responsible causes of this environmental downfall and many of the environmental scandals of the present age. For instance, based on a review of thousands of scientific publications, the Intergovernmental Panel on Climate Change (IPCC) has concluded that the warming of the Earth’s climate system is “unequivocal”, and that human activities are “very likely” the cause of this warming (WTO and UNEP, 2009). On the other hand, the accounting discipline requires full disclosure of all material items to users of financial statements. Full disclosure asserts that, accounting reports disclose fully and fairly the information they are prepared to present (Maheshwari, 2004). Thus, the financial reports should honestly disclose and give a fair and a true picture of performance and position of the business. As a way of ensuring full disclosure, materiality requires that all material items be included in the financial statements (Maheshwari, 2004). Materiality means a characteristic attached to a statement, fact, or item where by its disclosure or method of giving its expression would be likely to influence the judgement of a reasonable person (Maheshwari, 2004).It must also be noted that, for the businesses, the importance of accounting is rooted on the perception that it provides reliable, complete, and accurate financial information about the financial performance (through the statement of comprehensive income) and financial position (through the statement of financial position) of the business (Mayya, 2009). This importance of accountancy cannot be achieved if some of the performances and costs (for instance, environmental costs) are not properly disclosed. Thus, the assertion that financial statements give a true and fair view of the business will be unrealistic. In other words, the field of accounting requires that all material environmental damages or costs should be comprehensively disclosed.

2. Objectives of the Study

2.1. General Objectives

- Generally, this study is aimed at studying the emergence and growth of corporate environmental reporting in Tanzania. The study is articulated through the following specific objectives;

2.2. Specific Objectives

- i. To determine the types environmental information currently reported;ii. To determine extent of the current corporate environmental reporting;iii. To determine adequacy of the current corporate environmental reportingiv. To recommend improvements for better corporate environmental reporting.

3. The Emergence of Corporate Environmental Reporting

- The concept of public environmental reporting received greater and international publicity since the United Nations Conference on Environment and Development held in Rio de Janeiro in June 1992 (Razeed, 2008). Since then, issues associated with accounting for the environment have become increasingly relevant to enterprises as the pollution of the environment has become a more prominent economic, social and political problem throughout the world. Environmental risk has been a focus to many stakeholders. For instance, how an enterprise’s environmental performance affects its financial health and how financial information relating to such performance can be used to assess environmental risk, and the management of such risk, are often matters of concern to creditors, suppliers, and investors and their advisers (UN, 1998). Currently, steps are being taken at both the national and international level to protect the environment and to reduce, prevent and mitigate the effects of pollution. As a consequence, enterprises are now expected, or even required, to disclose information about their environmental policies, environmental objectives, and programmes undertaken, and the expenditures incurred in pursuit of these policies, objectives and programmes, and to disclose and provide for environmental risks (UN, 1998). Many countries and security market agencies have established various laws and requirements for environmental disclosure. For example, the US securities regulations explicitly require registered firms to disclose:i. The material costs of complying with environmental regulations in future years;ii. the costs of remediating contaminated sites if a liability is likely to have been incurred and its magnitude can be approximately estimated;iii. other contingent liabilities arising from environmental exposures;iv. involvement as a party to a legal proceeding about an environmental issue, especially with an agency of government; v. Any known trend or uncertainty involving environmental issues, including pending regulation that would have a material effect on the company’s business (Razeed, 2008).However, in Tanzania, environmental reporting is still a non-mandatory requirement. Non-mandatory disclosures are made without being prescribed by regulations, laws, stock markets agencies, or the accounting professional bodies. It has been established that, non-mandatory environmental disclosures are voluntarily incorporated within the Annual/Financial Report to increase stakeholders’ awareness of the company’s activities, performance and interactions with the environment during the year (Jones, 2000). The Dar es salaam Stock Exchange (DSE) also simply requires the listed companies to prepare final accounts following the guidelines as per International Financial Reporting Standards (IFRS) (DSE, 2011) which do not require environmental disclosure.

3.1. A Need for Corporate Environmental Reporting

- Centered in the concept of full disclosure and materiality, environmental disclosure has in recent years drawn serious attentions to a wider range of stakeholders. The aim is as just mentioned previously; the business should fully communicate all material information to the interested users. In as far as environmental information is a strategic issue; its disclosure also plays an important strategic role to decision makers. This means, environmental information if material, should be communicated to the users of company’s information through comprehensive disclosures.Basically, environmental external reporting refers to the process of communicating externally the environmental effect of organization’s economic actions through the corporate annual report or a separate stand-alone publicly available environment report (Hibbitt, 2009). In a broad corporate view, the corporate environmental external reporting refers to the external communication of environmental, health and safety issues relating to policies, activities, undertakings and beliefs of an organization through company-wide reports which are placed in the public domain on a regular and continuing basis (O’Dwyer, 2001). Thus, corporate environment reporting involves external communication of company’s environmental policies, objectives, beliefs, activities, damages, and commitments. The United Nations through the Economic and social council, Commission on transnational Corporations (hereafter, UN CTC) requires companies to disclose information regarding;i. A discussion about the type of environmental issues that are related to the business and its industry;ii. A statement as to what formal environmental policies and programmes had been adopted by the firm and what improvements had been achieved;iii. Information about emission targets and performance and the extent to which measures are being taken as a result of government legislation and how far the requirement are being achieved;iv. Any material legal proceedings and known potentially significant environmental problems;v. The financial or operational effects of environmental protection measures on the capital expenditure programmes and earnings of the business for the current period as well as future periods ( e.g. in relation to clean-up and restoration costs);vi. Where material, amounts charged to operations in the current period and accumulated capitalised relating to environmental protection;vii. The company’s policies for accounting of environmental protection measures in relation to matters such as the recording of liabilities and provisions, setting up catastrophe reserves out of retained earnings and disclosing contingent liabilities (UN CTC,1991).

3.2. Recognition of Environmental Costs

- Environmental costs should be charged to the income in the period in which they are identified, unless the criteria for recognition as an asset have been met, in which they should be capitalized and amortized to the income statement over the current and appropriate future periods (UN, 1998).Environmental costs should be capitalized if they relate, directly or indirectly, to future economic benefits that will flow to the enterprise through:i. Increasing the capacity, or improving the safety or efficiency of other assets owned by the enterprise;ii. reducing or preventing environmental contamination likely to occur as a result of future operations; oriii. Conserving the environment.In this case, environmental cost becomes an asset. Environmental assets are environmental costs that are capitalized and amortized over the current and future periods because they satisfy the criteria for recognition as an asset (UN, 1998).

3.3. Recognition of Environmental Liabilities

- Environmental liabilities are obligations relating to environmental costs that are incurred by an enterprise and that meet the criteria for recognition as a liability. When the amount or timing of the expenditure that will be incurred to settle the liability is uncertain, "environmental liabilities" are referred to in some countries as "provisions for environmental liabilities" (UN, 1998). An environmental liability should be recognized when there is an obligation on the part of the enterprise to incur an environmental cost.

3.4. Location of Environment Information in the Annual Reports

- The environment is one of the important strategic issues for decision making; therefore, it should be given equal disclosure opportunity in the annual reports just like other strategic issues. Depending on the nature and activities of the business, environment information may be presented in each section of the annual report of the particular year. However, environmental information should not be included just to increase the overall level of disclosure, it should provide added value to the reader to further enhance their understanding of the company’s environmental activities, performance and interactions with the environment (Jones, 2000). Basically, environmental disclosures in the Annual/Financial Report should present a ‘true and fair’ view not just in words but also in quantitative data where possible (Jones, 2000). In the study carried out at university of Sunderland for Environmental disclosure of European Companies, the following locations of environment information were identified;i. Review of Operations/ Business Units; This is a detailed review, usually division by division, covering in detail the activities of the various parts of the group, where, and how the groups various markets are shaping, and where the focus of management lies. Currently the environment disclosure in this section is about the environment product. ii. Chairman’s or Chief Executive Officer’s Statement; This is a section concerned with the following details;a) The overall trading conditions during the period, current climate and general outlook.b) The performance achieved by each activity, current trading and future prospects.c) Changes to the Board.d) Company strategy and plans for the future. The chairman’s report is one of the best sections to disclose environment information as it indicates the commitments of the top management on environment. Chairman’s or Chief Executive Officers statement should include references to the existence of environmental policy/principles, Environmental Management Systems, environmental targets or objectives and refer the reader to locations within the Annual Report, Environmental Report or other publications where more detailed information can be found.iii. Company Descriptions, This is the section that describe Statements relating to ‘who the company is,’ ‘what it does’ and their ‘values for the future’ (mission statement). In this section the management state how well it is focused on preserving the environment.iv. Shareholder Value, This is the section that gives details about; (a). Summery share performance data. (b) Shareholder profiles. (c) Financial calendar. (d) Notification of the Annual General Meeting. (e) Other Publications.Environmental matters may fit to appear in this section to be included in other publications or the calendar showing environment workshops. v. Highlights; This section highlights significant developments and achievements. The type of environmental disclosures in this section will depend on the activities and progress of each individual company during each particular year.vi. Financial Review;This section provides Information to explain the accounts and sheds light on financial performance and strategy. Disclosures in this location should relate to environmental financial information which should be quantified, where possible, and accompanied by additional information to qualify the data presented.vii. Research and Technology;This location provides information to demonstrate the development of new products or processes to meet the demands from legislators and customers. Information should be provided showing how environment friendly the future product or process will be and how will the environment impacts (if any) be managed. Current and future disclosures should relate to environmental research and development.viii. Environmental Section or Subsection;This section provides detailed information relating to environmental performance and activities during the year. Current and future disclosures should relate to environmental managerial, physical and financial information (Jones, 2000).ix. Director’s ReportIn this report, the director gives the summary of the company’s operations covering details like; a) Review of the business during the year.b) Indication of likely future developments.c) Names and shareholdings of directors.d) Research and development.Environmental matters should be equally addressed in this section just like other prioritized strategic issues. Details in this section include quantified environmental provisions, environmental legislation and compliance, environmental expenditures, liabilities and contingent liabilities.x. Accounting Policy or Principles;This section provides policies and principles and which the financial reports were prepared. Currently the majority of disclosures relate to statements about when environmental accruals are incurred. However, further contextual information for example what is covered by environmental provisions or expenditures and how they are accounted for should also be disclosed.xi. The Statement of Comprehensive Income;This is a financial statement which shows whether a company has made a profit or loss for a particular period and how that profit or loss has been arrived at. In this statement current environment cost should be separately disclosed.xii. Notes to the Statement of Comprehensive Income; At this section, further details are given giving additional details about items included in the statement of comprehensive income, this should include environment details.xiii. The Statement of Financial Position;Financial statement which shows the financial position of the company at a particular time i.e. what they own (assets) less what they owe (liabilities). Provisions for environmental liabilities should be quantified, if material.xiv. Notes to the Statement of Financial Position;This is done for amplification and extension to the figures shown in the balance sheet beyond the legal minimum disclosure requirements. Provisions for environmental liabilities should be quantified, if material.xv. Director’s Responsibility;Statement of the responsibilities of the director’s in regard to the financial statements. if the company has included a lot of environmental expenditure information then they may become a significant part of the account and require the director’s to affirm their responsibility to presenting ‘true and fair’ information (Jones, 2000).

3.5. Types of Environmental Information

- To be effective and informative, environmental reporting should cover all the important aspects of environment as mirrored by its operations. Many institutions have tried to develop environmental reporting frameworks; however, the best framework should be that which will fully disclose sufficient environmental information to users.A review of European companies disclosing environmental matters revealed the following environmental information that need to be disclosed.a) Environmental Management SystemsIt is important that companies should disclose the existence of any Environmental Management System. If they have sites certified to an Environmental Management System standard they should specify which standard has been achieved and quantify the absolute number of sites certified as well as the percentage of the total number of sites they represent.b) Environmental Targets or ObjectivesEnvironmental targets and objectives represent the minimum requirement to meet at a given time and resource. It is recommended that companies should mention the existence of their environmental targets and objectives, how many are in place, how many they achieved during the year or are on-going, postponed or abolished. If significant progress was made against any one or two targets those targets should be presented alongside information relating to actions undertaken and progress made, possibly using time series data.c) Environmental Policy or PrinciplesThe environmental policy or principles outlines the company’s overall intentions towards environmental improvements. It is therefore recommended that companies should mention the existence of their environmental policy or principles. If revised or updated during the year state why and how it has changed and give consideration to the inclusion in full of the revised policy. Companies should state how copies of the environmental policy can be obtained.d) Environmental Legislations and ComplianceCompanies often operate in the countries that have environment legislations in place. These legislations will always need to be complied within a strict notice. It is therefore recommended that companies should make disclosures in relation to environmental legislation and compliance specifically information relating to the effects of current and future environmental legislation and actions undertaken to comply with this legislation, environmental fines or penalties and legal proceedings.e) References to the Environmental ReportReferences to the Environmental Report and other environmental related documents are important to direct the reader to further information for which there is no space in the Annual Report. These references may direct the reader to a certain page, report (other than annual report) or website for more details of environment concern. It is therefore recommended that references should be made to the Environmental Report from throughout the Annual Report, if possible referring to specific pages or information. A variety of ways should be given through which those documents can be obtained (e.g. address, telephone, fax, email, and web address).f) Environmental Products and ProcessesEnvironmental products and process refers to how environment friendly are the company’s products and process. Companies should disclose information in relation to their environmental products and processes placing these disclosures in context and, where possible, alongside quantitative data relating to the demand for environmental products or sales from environmental products highlighting the financial link to environmental product developments.g) Greenhouse Gas Emissions, Water treatment, Waste, Recycling or re-use, and Energy Efficiency and ConsumptionIt is therefore recommended that the following should be quantified, where possible:-i. Greenhouse gases Emission levels and/or reductions.ii. Water consumption, energy efficiency and/or water quality.iii. Waste levels and/or reductions.iv. Recycling levels.v. Energy efficiency and/or consumption.Consideration should be given to presenting this information graphically or in tables thus allowing for time series data and targets to be presented. It should also be accompanied by qualitative information that can explain anomalies or trends and describe actions related to improving their performance.h) Environmental Financial InformationIt is often advocated that environmental financial information be clearly disclosed and each of the item be separately identified. Disclosure of environmental information involves the following;i. Mention environmental expenditures, ii. Quantified expenditures on individual environmental investment projects, iii. Quantified capital environmental investments, iv. Quantified operational environmental expenditures,v. Environmental savings,vi. Environmental provisions, vii. Environmental remediation costs,viii. Environmental fines, ix. Environmental taxes, x. Environmental insurance, xi. Compensation to third parties, and xii. Addition costs of certificationi) External Awards or Recognition;External environmental awards or recognition are a way in which companies can validate their environmental activities and/or performance. In this section the company details the gift or award given to promote environment awareness and conservation.j) Environmental Audits;Environmental audit are meant to certify some specific areas in which the management identifies to be more risky. The auditor identifies possible current or future risks facing the company emanating from damaging the environment.k) Environmental Research and DevelopmentIn this category the company discloses how much is invested for research and development regarding environment protection. It is expected that as the company budget funds for research and development of new products and process, some funds should be assigned to investigate the impacts of the same products and process on the environment (Jones, 2000).

3.6. Potential Benefit of Environmental Disclosure

- Environmental disclosure, like many other disclosures offers many benefits to both the disclosing company and stakeholders. Analysts typically cite three types of rationales for public involvement in which these befits can be experienced: normative, instrumental, and substantive (Fiorino 199, Perhac 1996).a) Normative RationaleThe normative rationale is cantered in a principal called ``right to know’’ (Beierle, 2003). Thus, disclosing information gives the public the right of getting information it wants and the risks resident to that information. b) Substantive RationalesSubstantive rationales for information disclosure argue that such programs produce data that lead to new insights and understanding of environmental problems and how to remedy them (Beierle, 2003). For the firm, the process of collecting information may reveal unrecognized opportunities for improving environmental performance, this entails why some programs require top management to sign off on disclosure reports (Graham, 2002).c) Instrumental RationalesInstrumental rationales argue that disclosure improves environmental performance (Beierle, 2003). This gives roots to the fact that, no information is just for right to know (Normative) or simply for data provision (Substantive). All information provision programs are intended to bring a change to the organization. For environment, such changes include reduces greenhouse gases emission, proper waste management, increased accident safety, pollution prevention, better regulatory compliance, hard waste disposal etc. others call this rationale as the ``shock and shame’’ dynamic by which new comprehensive risk environmental information shocks citizens, the media, agencies, and markets into driving change externally and shames companies themselves to drive change from within (Stephan, 2002).

3.7. The State of Environment in Tanzania

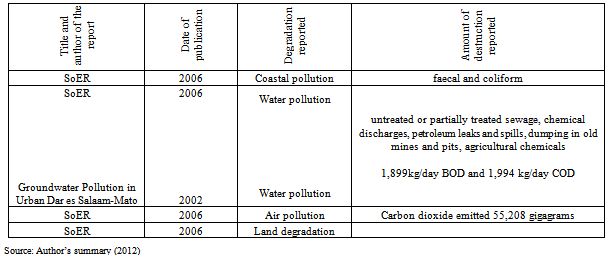

- Like many other developing countries, Tanzania faces fates of great proportions as the result of depleted environment. The discussion below focuses on some of the reported types of environmental degradation originating mainly from manufacturing business activities, the impacts thereafter, and future possibilities. a) Threats on Coastal and Marine Resources and EcosystemSoER (2006); identifies four threats in the coastal region; these include declining harvest of marine and coastal living resources, loss of coastal and marine habitants and biodiversity, coastal pollution, and beach erosion. It has also been identified that, the artisanal and industrial fisheries in Tanzania have been falling consistently in recent years, for example the artisanal fish landings have decreased from 54,327 tonnes in 1990 to 32,286 tonnes in 1994 (URT, 2006). Prawn fishery has also shown a decreasing trend, prawns being exported have declined drastically from about 1,360 tonnes in 2000 to 467 tonnes in 2005 (URT, 2006). In fishery industry, fishing methods have been identified to cause destruction; the most destructive fishing method is the use of dynamite and each blast of dynamite kills all living things including fishes and coral reefs within 15-20 meters radius (URT, 2006).b) Coastal PollutionCoastal areas experience a range of pollution; pollution originating from discharge of untreated water from sewer systems, pit latrines, soak pits, garbage dumps normally found their way to coastal waters and as a result pollution, high levels of nutrients, faecal and coliform have been recorded in coastal waters (URT, 2006).For example, various industrial wastes from Keko, Chang’ombe, Kurasini, Mtoni and Temeke in Dar es Salaam have been discharging untreated wastes into the shore via the Msimbazi creek. These pollutants include chemicals from textile industries such as dyes, paint wastes and strong alkalis (URT, 2006).c) Water Pollution In Tanzania, water pollution emanates from a number of points and diffuse sources including untreated or partially treated sewage, chemical discharges, petroleum leaks and spills, dumping in old mines and pits, agricultural chemicals that are washed off or seep underground from farm fields, and atmospheric deposition (URT, 2006). Industries account for the major part of water pollution, it is estimated that, about 80% of industries in Tanzania are located in urban areas and over 50% of these are found in large towns, mainly Dar es Salaam (URT, 2006). However, many of these industries were established years ago without adequate environmental attention, therefore, they have been operating without waste treatment facilities, some for more than 40 years (Mato, 2002). As a result, in most towns wastes from the industries are disposed of in inland rivers, depressions, pits, or on land (Mato, 2002). For instance, industrial effluents have been reported to pollute rivers like Msimbazi in Dar es Salaam, Karanga in Moshi, Mwirongo in Mwanza, and Themi in Arusha (Mato, 2002). Estimates show that, more than 122 industrial establishments in Dar es Salaam produce about 127 tonnes/day of hazardous waste, which is about 40% of the total industrial solid waste production (Mato, 2002). Despite of all these wastes, it has been found that most of industries have no waste treatment and holding facilities other than open ground, which results into pollution of both surface and ground water resources (URT, 2006).Reports have confirmed that, in Pangani basin, raw and partially treated effluents from industries in Arusha, Moshi and Tanga are causing pollution of water bodies in the basin (URT, 2006). It is estimated loads released in Pangani River from Arusha and Kilimanjaro industries are 3,281 and 7,489 tonnes per year. The Sigi River, in this basin, has an estimate of more than 135 mg/L, due largely to discharge of raw or partially treated wastewater from sisal processing industries (Mwanuzi, 2000). Also, Mato (2002) found that in Dar es Salaam alone, more than 25% of the filling station might be having leaking tanks.d) Agricultural Water Pollution Another important sector that much depends on environment is agriculture. To be more commercialized, agriculture uses a range of chemicals. It has been empirically observed that the intensive and indiscriminate use of agrochemicals in the Rufiji and neighbouring basins is causing deterioration of water quality and soil pollution (URT, 2006). Researchers also have found that even banned pesticides like DDT are in use even to date, though somewhat clandestinely (URT, 2006). Furthermore, storage of huge amounts of obsolete as well as viable pesticides is haphazard and the importation of the chemicals is unregulated, and this has led to importation of chemicals in excess of actual needs, apart from facilitating importation of banned pesticides (URT, 2006). In the Pangani River Basin, which is to the north east of the country, concentrations of soluble salts in water have been found to be as high as 750mg/L, presumably due to use of fertilisers (URT, 2006). Some polluted airs have also found to cause water pollution, it is reports that;Atmospheric deposition has been identified as the predominant source of nutrient loading to Lake Victoria with loads of 137,001 and 21,754 kg/day for total nitrogen and phosphorus, respectively and that total annual nutrient inputs to the lake including industrial and municipal sources are currently estimated at 162,224 and 28,949 tonnes of N and P, respectively (Nyanza et al, 2006).e) Air Pollution The major air pollution sources in Tanzania are transport activities, burning of agricultural wastes, manufacturing activities; residential burning of fossil fuels and wood and open field solid waste burning (Nyanza et al, 2006). In 1990, carbon dioxide emissions from Tanzania amounted to 55,208 gigagrams (URT, 2006). The weight of major GHGs (Carbon dioxide, methane and nitrous oxide) indicates that carbon dioxide is the highest (55%), followed by methane (44%) and nitrous oxide (1%) and when weighed sector-wise, findings in 1990 show that the highest contribution is from Land-use changes and forestry sector (53%), agriculture (33%), energy (13%) and waste management (1%) and the industrial processes contributed less than 1 % of potential warming (URT, 2006).

3.8. The Most Reported Forms of Environmental Degradation in Tanzania

- This study originates from the fact that, despite the presence of environmental degradation caused by manufacturing business activities, manufacturing companies have not disclosed or have not disclosed enough environmental information to give a true picture of their environmental performance. It is expected that, the information disclosed must tell how the company’s business activities have interacted with the environment and what the company has done to mitigate any negative impacts so caused.To substantiate this fact, a number of environmental pollutions emanating from the manufacturing activities have been reported in Tanzania. These pollutions include coastal areas pollution due to faecal and coliform depositions in the coasts. Others include water pollution, air pollution and land degradation. These pollutions have been empirically established by many reports; table 1 below summarizes these reported pollutions:

|

4. Content Analysis of the Manufacturing Companies’ Annual Reports

- Content analysis is the helpful tool in measuring the adequacy and extent to which qualitative reporting has been made. Content analysis turns the qualitative terms into decisive quantitative data. Therefore, content analysis is a process of turning the content of documents or other media into ‘precise, objective, quantitative data (Neuman. 2000). The aim of content analysis carried in this study is to determine the adequacy and extent to which environmental disclosure has been made which eventually mirrors the trend of environmental reporting interest.Many units can be used to carry out content analysis; these units include number of pages, number of paragraphs, number sentences, and number of words. Some studies have proposed sentences as the preferred recording unit in content analysis (for example studies by Milne & Adler 1999; Ingram & Frazier 1980). Ingram and Frazier (1980) used sentences as the recording (and measurement) unit arguing that ‘a sentence is easily identified, is less subject to inter-judge variation than phrases, clauses, or themes, and has been evaluated as an appropriate unit in previous research (Ingram and Frazier, 1980). Milne and Adler 1999 suggested that sentences should be the preferred unit of measurement in content analysis because quantification errors are less likely to occur when using sentences as the number of words in a document is greater than the number of sentences (Milne and Adler, 1999).However, Deegan and Gordon (1996) argue that words provide better detail than sentences when measuring the actual volume of disclosures (Deegan and Gordon, 1996). The number of words has been used as the unit of measurement in several other studies (See for example Deegan & Rankin 1996; Zeghal & Ahmed 199). Some researchers have criticised the use of words as decreasing reliability and providing meaningless results or measures, particularly during the coding stage (Milne & Adler, 1999); however, the effect on reliability is dependent upon the objectives of the research and the content analysis technique adopted (Cowan, 2007). Also, words are the smallest and therefore the safest unit for quantification purposes in written documents (Krippendorff, 1980). Since this study seek to establish the extent based on the volume of disclosure which does not require any coding, it was therefore, more convenient to use the number of words as the measurement unit. However, when the number of words failed, the number of pages was used to derive a conclusion.In order to measure the growing interest in corporate environmental reporting, this analysis used four consecutive years (2008, 2009, 2010 and 2011). These years were favourably selected because at the time of study they were the earliest years in which each of the studied company had its statements published.

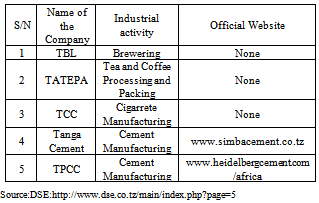

4.1. Manufacturing companies listed in Dar ES Salaam Stock Exchange (DSE)

- This study was conducted covering five (5) manufacturing companies operating and headquartered in Tanzania and whose shares are listed with the Dar es salaam stock exchange (DSE). The general expectation is that, public companies publish comprehensive information to the public in order to comply with the listing requirements.As of 26/09/2012 the Dar essalaam stock exchange had the following manufacturing companies

4.2. Environmental Reporting for Listed Manufacturing Companies from the Year 2008 to 2011

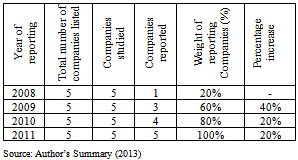

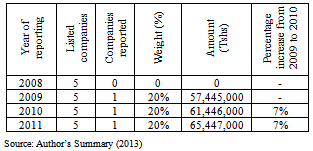

- During the reporting year 2008 five manufacturing companies had been listed in Dar es salaam stock exchange (DSE). Of these five, only one company reported environment information, this represents 20% of the listed manufacturing companies. In the year 2009, five (5) manufacturing companies had been listed in the DSE. Of these five (5) companies, three (3) companies reported environmental information; this represents sixty percent (60%) of the listed manufacturing companies and indicates 40% increase from the previous year, two manufacturing companies (equalling to 40%) did not report anything about the environment. During the financial year 2010 five (5) manufacturing companies had been listed in the DSE. Of these companies; four (4) reported environmental information, these represents eighty percent (80%) of total companies, this means there was an addition of one company (equalling to 20%) in environmental reporting; only one company did not report anything about the environment during the year 2010. Manufacturing companies reporting environmental information increased to five (5) in the year 2011. Thus, by the end of the year 2011 all the listed manufacturing companies were reporting environment information in their annual reports. Table 2 below summarises the companies reported environmental information. The simple implication here is that, throughout the studied period (2008 to 2011) environmental reporting has been growing with new companies joining each year, currently all the five listed manufacturing companies are making environmental reporting in their annual reports.

|

4.2.1. Adequacy and Extent of Environmental Reporting during the Period

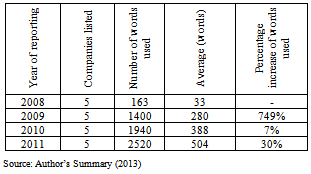

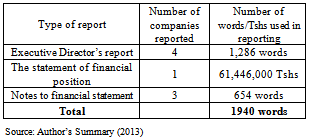

- Further analysis as indicated in table 3 below reveals that during the reporting year of 2008, 163 words were used in environmental reporting, in the year 2009, a total of 1400 words were used, these words increased to 1940 during the year 2010 and they amounted to 2520 for the year 2011. This means, the number of words used in environmental reporting increased by 749% from the year 2008 to 2009, by 7% from the year 2009 to 2010, and by 30% from the year 2010 to 2011. This simply means, each listed manufacturing companies on average reported 33 words, 280 words, 388 words, and 504 words for the year 2008, 2009, 2010, and 2011 respectively (Table 3). This increasing trend basically suggests that, there have been an increasing interest in environmental reporting by the listed manufacturing companies in Tanzania.

|

|

|

4.2.2. Location of Environmental Information in the Final Reports

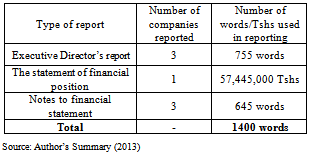

- Another important aspect of this analysis was to determine the popular locations of the environmental information in the annual reports. Locations in the annual reports were divided into fourteen (14) locations namely; review of operations/ business units, statement of the Chairman of the Board of directors, company descriptions, shareholder value, highlights, financial review, research and technology, environmental section or subsection, Executive Director’s report, accounting policy or principles, the statement of comprehensive income, the statement of financial position, notes to the financial statements, and statement of cash flows.a. Location of Environmental Information in the Annual Report of the Year 2008During the financial year 2008, only one company disclosed environmental information in the annual report. This information was whole reported in the statement of the Executive Director.b. Location of Environmental Information in the Annual Report of the Year 2009The locations of environmental information as summarized in table 6 below show that, three (3) of the five (5) listed manufacturing companies in the year 2009 reported a total of 755 words in the Executive Director’s section. This means, all the manufacturing companies reporting about environment used the Executive Director’s section in reporting their commitments to the environment. Furthermore, all the three (3) companies which reported environmental information in the year 2009 had their information reported in the disclosing notes with words amounting to 645. Finally, only one company reported environmental information in the statement of financial position (Balance sheet) for amount provided as provision liability (Provision for quarries restoration) to mitigate environmental impacts arisen from its operations.

|

|

|

5. Conclusions

- This study dealt with corporate environmental reporting for listed companies in Tanzania. Therefore, the study dealt with the whole essence of environmental reporting in which combinations of many observations were drawn. Therefore, it becomes inherent to draw many conclusions from these observations.

5.1. Environmental Disclosure

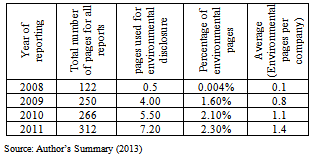

- During the year 2008, 2009, 2010 and 2011 the manufacturing companies disclosed environmental information covering to approximately, 0.5, 4.0, 5.5 and 7.20 pages respectively which stands for 0.004%, 1.6%, 2.1% and 2.3% of the whole final reports during the respective years. The study also revealed that, during the studied period, only one company provided fund for environment expenditure (quarry restoration), this stands for 20% of all the manufacturing companies. This means, though much improvement is needed, the environmental disclosure has emerged among the listed manufacturing companies and there have been a growing interest in making environmental reporting.

5.2. Types of Environmental Information Currently Disclosed

- During this period (from the year 2008 to 2011) the manufacturing listed companies disclosed the following three types of environmental information;i. Environmental policy; This is a document that includes statements declaring on what is expected of a company regarding the environment. These statements cover themes like how environmentally friendly or unfriendly the company’s activities are and what a company does to mitigate negative impacts if any. Environmental policy also may include environmental objectives or targets. ii. Record of compliance with environmental standards and regulationsOnly two companies have disclosed compliance statements with ISO 14001 that is applicable for cement manufacturers. It is obvious that the remaining three of the five manufacturing companies did not include any environmental law and standards compliance disclosure because there no such standards in their industry and that the existing environment management Act 20 and the Companies Act no. 12 do not have any compulsory environmental disclosure clause.iii. Environmental provisions; These are obligations expected to be settled in the future because of the damages arising from the current activities. These amounts are set aside for future uses in mitigating or eliminating the damages posed by the business activities during the current year. The content analysis as summarized in table 5 above shows that only one company had reported environmental provision. This is a provision for quarries restoration. This implies that, the manufacturing companies did not expect any future environmental expenditure due to the current operations or rather did not set amount for mitigating any possible environmental related damages.

5.3. Location of Environmental Information

- During this period (year 2008 to 2011), environmental disclosures were made using three locations. Depending on the nature of disclosure, the locations listed hereunder were used;i. Executive Director’s report: In this report, highlights of environmental policies and performances were made.ii. The statement of financial position: In this statement, environmental provision for quarries restoration of one cement company was made. No other disclosures were made in this statement.iii. Disclosure notes: In this location, additional details were given to explain some additional information which could not be sufficiently explained in the other reports.

5.4. Extent of the Current Disclosure

- To establish the desirable extent of a disclosure, it is needed to explain how much have the current environmental disclosure covered in terms on the quantity and the depth of reporting. This study found that the current disclosure covers three items namely; environmental policy, compliance with environmental standards, and provisions. The environmental information disclosed during the four years only took average 0.1, 0.8, 1.1 and 1.4 pages in the year 2008, 2009, 2010 and 2011 respectively. Put it in other terms, these items in total hold 0.004%, 1.6%, 2.1% and 2.3% of the reports for the year 2008, 2009, 2010 and 2011 respectively. Thus, in all the three most recent years (2009, 2010 and 2011) environmental disclosure holds about 2% of the total reports. Therefore, the current disclosure also is not enough in a sense that it only used approximately 2% of total pages. Thus, when compared to other disclosures such as corporate governance, social reports, and financial reports (which hold 98% of the total reports), environmental disclosure received the lowest attention.

5.5. Adequacy of the Current Disclosure

- One of the important aspects of this study was to establish whether the current disclosure is adequate. This is done by explaining whether the environmental disclosure was done at a sufficient coverage (scope). As previously observed, the current disclosure covers three items; environmental policy, environmental law and standards compliance, and provisions. In a country where reports show that tons of unmanaged wastes are disposed into water bodies or open spaces, tons of dusts and greenhouse gases are emitted into air, lands are highly depressed for underground raw materials extractions; it is obvious that the current disclosure is not adequately sufficient. These disclosures do not touch some of the important aspects such as current environmental expenditures, mitigation efforts, amount of wastes disposed annually, and recycling or other management activities. Therefore, the environmental disclosure should be increased in both the quantity and the scope to provide full environment image of the listed manufacturing companies in Tanzania.

6. Recommendations

- An important aspect of any study is to generate recommendations in order that improvements should be made. Deriving recommendations was a core objective of this study, this section comprises of five recommendations which entirely originate from the observations generated during the content analysis.

6.1. Companies should Widen-up the Scope of Their Environmental Disclosure

- Mostly, manufacturing companies report about their policies, standards compliance, and good intents regarding the environment. While plenty of evidences tell the presence of serious environment damages (see table 1), manufacturing companies have not reported how they damaged the environment, the implied effects of these damages to ecosystems, and their efforts towards mitigation. In order to increase the adequacy and appropriateness of environmental disclosure, listed manufacturing companies should widen up the scope of their environmental disclosure to include types of environmental damages, effects, and the amount involved or expected for mitigation.

6.2. External Auditors should Include in Their Audit Report Information about the Environment

- During the accounting year of 2008, 2009, 2010 and 2011 none of the external auditors gave an opinion on environmental performance of their clients. This means, the environmental performance of the companies is not an important focus of the external auditors at the present time. With the present seemingly increasing trend of environment pollutions, auditors should include in their audit opinions information about the impact of their clients’ operations to the environment. Thus, though not legally or professionally mandated, external auditors should deliberately give an opinion about the environmental performance of their clients.

6.3. The DSE should Include in the Listing Requirements Release of Annual Environmental Report

- Unlike most of the world famous stock exchange commissions; such as London stock exchange, stock exchange commission of USA, Sydney stock exchange; the Dar es salaam Stock Exchange has not included among listing requirements annual disclosure of environmental information in either as stand-alone or as part of other statements. This makes the listed companies particularly the manufacturing companies not to bother about environmental reporting. Therefore, the DSE should include among other disclosure requirements, release of comprehensive statement regarding the environment by the listed manufacturing companies.

6.4. The NBAA should Prepare a Compulsory Standard and Guideline for Environmental Reporting

- The National Board of Accountants and Auditors (hereafter NBAA) is the highest central body that deals with external financial reporting and auditing in Tanzania. Among other duties, the NBAA prepares and enforces reporting standards for companies operating in Tanzania especially the listed companies. But at times, there is no standard addressing the preparation and presentation of environmental information. Therefore, it is necessary that the NBAA should formulate a standard dealing with guidelines, procedures, and presentation of environmental information in the annual report.

6.5. The Companies Act No.12 (CA) and (or) the Environment Management Act No.20 (EMA) Should Recommend Presentation of Environmental Report

- The Companies Act no.12 (CA) prescribes much of the statements presented by companies at the end of the accounting period. The CA requires that the public limited companies should prepare Income Statement, Balance Sheet, Statement of cash flow, Statement of change in owner’s equity, and the statement of the chief Executive Director. This law does not require the companies to report about environment. The current Environmental Management Act no.20 (EMA) also does not require the manufacturing companies to make compulsory environmental external disclosure in the annual report. To enhance full disclosure and transparency of the manufacturing companies, both EMA and CA should demand a comprehensive environmental disclosure in the annual reports.