-

Paper Information

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2013; 2(2): 125-130

doi:10.5923/j.ijfa.20130202.13

Challenges in Management Accounting Innovation Adoption: Evidence from Malaysian Companies

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLAliza Ramli 1, Suzana Sulaiman 1, Falconer Mitchell 2

1Faculty of Accountancy and Accounting Research Institute, Universiti Teknologi MARA, 40450 Shah Alam, Malaysia

2Management School and Economics, University of Edinburgh, Edinburgh, EH8 9AL, United Kingdom

Correspondence to: Aliza Ramli , Faculty of Accountancy and Accounting Research Institute, Universiti Teknologi MARA, 40450 Shah Alam, Malaysia.

| Email: |  |

Copyright © 2012 Scientific & Academic Publishing. All Rights Reserved.

The purpose of this paper is to highlight the main challenges or issues in the adoption of Value Engineering (VE) viewed as a management accounting innovative technique within Malaysian companies. VE relates to a systematic and multi-disciplinary team approach adopted by companies which analyze the functional requirements of new and existing products, projects or services. The aim is to achieve the essential function at the lowest overall cost while maintaining customers’ optimum value assurance. A survey was conducted to determine VE issues faced by companies within each of the Malaysian automotive and construction industries. The survey findings showed that time and attitude related issues encountered by both the industries were the main challenges that were holding up VE application. The paper contributes to the literature in management accounting innovation domain specifically in relation to VE by highlighting VE adoption critical challenges, as opposed to presenting critical success factors. The findings of the study will provide important insights for companies on possible challenges faced when contemplating how to introduce innovative technique such as VE into their social system. An understanding of the challenges in innovation adoption will bring greater confidence of success when implementing management accounting techniques such as VE.

Keywords: Management Accounting Techniques, Value Engineering, Innovation, Survey Method

Cite this paper: Aliza Ramli , Suzana Sulaiman , Falconer Mitchell , Challenges in Management Accounting Innovation Adoption: Evidence from Malaysian Companies, International Journal of Finance and Accounting, Vol. 2 No. 2, 2013, pp. 125-130. doi: 10.5923/j.ijfa.20130202.13.

Article Outline

1. Introduction

- Innovation defined as a new idea by individual or other unit of adoption[1] is perceived as an important research area as it is expected to aid organizations to successfully adapt to and continue to exist in volatile business environments ([2],[1]). While management and organizational literature has long studied innovation[3], management accounting innovation research only began to emerge after the 1990’s following criticisms about a lack of management accounting innovation[4]. As such, there has been keen interest and a great deal of literature on management accountingorganizational innovation. However, management accounting studies on explanatory factors (e.g., organization size and structure, industry competitiveness and customers preferences) have often produced mixed results ([5],[6]). These mixed results have subsequently led to several other observations on management accounting innovation, and these have served to motivate this study, which focuses on Value Engineering (VE). VE has been viewed as an innovative tool by researchers in both engineering ([7],[8]) and management accounting disciplines[9]. VE is defined as[10], p.74) “a philosophy or organized approach to identifying and eliminating unnecessary cost, to provide the necessary function at the least cost.” VE becomes a useful tool in resolving issues in an organization and this can be achieved by identifying the main function of design, product, project or service and subsequently eliminating unnecessary cost[11]. As a result, existing designs or decisions could be improved.Research showed that organizations in the local automotive and construction industries are experiencing increase product and project complexity, intense pressures to lower costs and tight budgets. In order to survive or ensure continued success it is essential that organizations continuously manage their costs, increase their profit position, and maintain better quality products that meet the customers changing needs and desires. VE, which focuses on creating value for customers, is one of the tools to meet these challenges. In a sense, this provides an interesting opportunity to study the mechanism of a management accounting innovation such as VE. The work of[7] further showed that a clear effort is needed to educate industrial practitioners on VE. According to[12], VE tool has been in use for half a century but there is a mixed public opinion of the usefulness of the tool. Reference[13] had pointed out also about the misconception and resistance towards VE among practitioners. Increasing competitive pressures and the gaps revealed above provide an opportunity for such a study within the Malaysian automotive and construction industries to be carried out. Thus, the objective of the paper is to determine the main challenges in VE adoption within Malaysian automotive and construction industries. The paper also explores the characteristics of organizations that used VE within both the industries. The remainder of the paper is organized into four sections. Section 2 draws on previous research on challenges in VE. The use of survey method is explained in Section 3. While, the survey findings on the automotive and construction industries are presented in Section 4. Finally, Section 5 concludes by presenting the contributions and limitations of the present study, and suggestions for future research.

2. Challenges in Value Engineering (VE)

- Despite a variety of critical factors identified for VE success in the literature, organizations have faced many challenges or issues when trying to realize the benefits of VE. One of the major hindrances facing VE within both manufacturing and construction industries are time related, insufficient knowledge and information and attitude related issues. Reference[14] showed that manufacturing companies experienced VE challenges such as limited internal resources to implement VE, lack of commitment for VE workshop, difficult to obtain customer approval and inability to understand customers’ priorities. Other attitude issues faced by manufacturing companies included resistance to change, territoriality, and sensitivity to criticism of work (Fisher, 1999). It was also apparent that construction companies experienced behavioral issues in VE exercises. Examples of these behavioral issues are lack of support from authority[7], lack of support from client[15], and lack of commitment from VE participants[13]. Further to that, according to[16], advanced technological development and intense market conditions have resulted in clients demanding shorter and more focused VE studies. However, the size and complexity of the projects that are subject to VE studies are continually increasing. The application of VE may delay the design process as some recommendation will involve some major or minor re-design work. Hence, it seems that lack of time to apply VE appeared to be a common impediment in VE application which users perceived could compromise quality. Another point to note is that the attitude barriers encountered in VE application can be related to the stakeholders, VE workshop participants, owners and developers. Reference[17] found that lack of proper planning for the VE workshop and insufficient education of the stakeholders and participants were among the attitude barriers encountered during the VE exercise. Meanwhile, the owners believed that VE provides a short-term economic investment environment[18] and the developers, who are profit oriented and shortsighted seemed to be more concerned with getting the investment return instead of value improvement[19]. It is also apparent that insufficient VE education would lead to poor understanding about VE methodology, which appears to be common amongst users. Lack of information (e.g., project information) could also lead to several issues, such as difficulty in completing the VE study and understanding customers’ priorities. Reference[20] emphasized that many potential adopters in the construction field are unwilling to use VE due to the lack of tools that can measure the effectiveness of VE studies. They also assert that there is limited performance measurement of VE studies in the literature because of the lack of a rigorous model. Hence, without a reasonable and accurate evaluation of the effectiveness of VE studies in achieving users’ targets, it can be difficult to determine possible and relevant changes which can in fact contribute to more benefits.

3. Survey Method

- A survey was each conducted on the automotive industry and the construction industry. A study of the literature aided the development of both questionnaires used in the survey. As suggested by[21], the questionnaire was customized according to the two different industry types. The survey instrument was developed to collect specific information about company characteristics, VE application and VE performance. However, only findings relating to organizational characteristics and VE issues are discussed in this paper. The measure for level of agreement with various issues was based on 18 items. The measure of possible issues relating to VE was based on several prior studies ([7],[14],[13],[15],[17]). A 5-point scale was used and it ranged from ‘strongly disagreed’ (1) to ‘strongly agree’ (5). National Automotive Vendors Association (NAVA), the sample for the automotive industry represents the national car manufacturer’s fraternity, which was launched in 1992. The 133 registered members are among the main suppliers and manufacturers of automotive parts and components in the country. The latest NAVA Directory provided the members list. The sample for the construction industry comprised of ordinary members of the Master Builders Association Malaysia (MBAM) that practise the trade of contracting and/or construction in this country. The MBAM was founded in 1954 by a group of pioneer Malaysian Master Builders. It plays an important role in the development and advancement of the construction industry in Malaysia. There are 403 ordinary members registered with the MBAM. The list of registered organizations was obtained from the association’s website. Respondents in both industries were from different management levels. CEOs and MDs were examples of respondents from the highest level of management, while managers represented the lowest level of management. However, there were also responses from non-management staff such as the executives. The variation provided views on VE from different perspectives. The entire population of NAVA was selected for Survey 1, while only 39.7% of MBAM agreed to participate in Survey 2 (based on the Dillman Method[21]. The response rate for the survey on the automotive industry was 31.6% (42/133), while 26.3% (42/160) was generated for the construction industry.

4. Discussions of Findings

- This sub-section delves into the descriptive analysis on adopters of VE and issues in VE adoption within the automotive industry and the construction industry.

4.1. Adopters of VE

- As shown in Table 1, the distinct characteristics of the majority of VE adopters within the automotive industry demonstrated that they were mature companies, since the majority of them had been established for more than 20 years, were involved in manufacturing metal components, had low to high product variance and mixed production process complexity. In terms of size of the organizations, there were a considerable spread in the number of employees. This shows size does not probably matter whether organization used or not used VE. 54.1% were First Tier indicating that they supplied their products directly to Original Equipment Manufacturers (OEM) and that they were position high up in this industry’s supply chain. The mixed product variance and the production process complexity suggested that VE was adopted irrespective of the different types of production processes. Similarly, a substantial number of theconstruction companies were mature companies and well-established, because over a third (34.3%) had been incorporated for more than 20 years. They were generally small sized companies, since a relatively low number of employees employed (< 50 employees). A higher number of companies (62%) had undertaken construction of buildings compared to civil, mechanical and electrical engineering types of projects. In addition, 70% of the construction companies had completed fewer than 10 projects over the previous five years (2002-2006), suggesting low product variance. A possible explanation for this is the nature of construction activities, in which a project normally takes a considerable length of time to complete, compared to the production of products in the manufacturing industry.

|

4.2. Issues in VE

- Tables 2 and 3 present descriptive results on all the 18 items that measure issues in VE adoption respectively, in the automotive and construction industries. All the standard deviations were closed to one. The median values ranged from 3 to 4, thus indicates that most organizations were either neutral or in agreement with the 18 issues experienced by them.

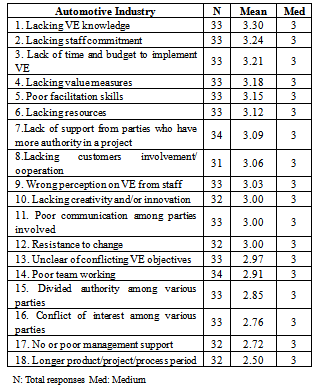

4.2.1. Automotive Industry

- Table 2 shows that the most common impediments to VE application was the lack of VE knowledge (mean = 3.30), followed by lack of staff commitment (mean = 3.24) and lack of time and budget to implement VE (mean = 3.21). There are other explanations, which could be due to insufficient education of some of the staff involved in VE, which may have resulted into a lack of commitment from them. The application of VE could cause delays or lead to some major or minor re-design work. These could result in more time needed for completion and higher costs. The lack of proper planning for VE workshop could also lead to lack of time to implement VE. This suggests that attitude, time and costs barriers were most common impediments encountered during VE exercise in the automotive industry. This result is similar to the findings from several studies such as[17],[19],[7]. On the other hand, the remaining issues were not perceived as serious impediments by respondents from automotive organizations.

|

4.2.2. Construction Industry

- Table 3 revealed that the most serious impediments experienced by construction organizations were the lack of support from parties who have authority in a project (mean = 4.12), followed by the lack of customers’ involvement or cooperation (mean = 3.88) and conflict of interest among various parties (mean = 3.74). Government, owners and customers who had more authority in a project were perceived to be the leaders and their support was very much needed for the successful implementation and application of VE, but this was not evidenced in this survey. Thus, the management style for successful VE should focus on the customer. Customer involvement in VE exercises is crucial because customers could contribute to the creation of values of the products. Furthermore, VE is a method to solve problem pertaining to the value of products or services from customer’s viewpoint. Therefore, the finding in this survey indicates the important role of parties such as government, owners and customers in contributing towards the success of VE in an organization. For example, besides having the authority to make decisions, the owners being trusted can definitely ease the implementation and application of VE.

|

5. Conclusions

- This study has identified some of the factors impeding the adoption of a particular management accounting innovation (VE). The two survey findings managed to identify the key issues (time and attitude related issues) encountered by both the automotive and constructions industries that were holding up VE application. These issues were consistent with the common problems highlighted by previous researchers (e.g.,[7],[13],[20]. However, the study showed that the lack of management support was not a determiner of the extent of VE adoption within the automotive industry. On the other hand, the construction industry normally encountered fewer of these issues and enjoyed higher VE application. In addition, this study indicated the possible crucial role of the government in driving the use of VE in Malaysia. Despite, a variety of critical factors identified for management accounting techniques adoption success in the literature, organisations have faced many challenges when trying to realise the benefits of the techniques. Thus, the paper contributes to the literature in management accounting innovation domain specifically in relation to VE by highlighting the VE adoption critical challenges or issues, as opposed to presenting critical success factors. The findings of the study will also provide important insights for organizations which are contemplating how to introduce innovative technique such as VE into their social system. An understanding of the challenges in innovation adoption will bring greater confidence of success when implementing management accounting techniques. Apart from the normal limitations associated with survey research, such as low response rate, non-response bias, additional limitations are related to the generalization issue and sample size of the study. However, a mitigating consideration is that the respondents most likely formed a fairly representative sample of the actual population of existing automotive components manufacturing and constructions organizations within the country. Another important contribution of the present study is to highlight the need for additional in-depth research on issues in management accounting innovation adoption such as VE in the Malaysian automotive and construction industries, as well as in other industries using case study method. This is because case study method embraces interaction and curiosity about the organizational and social worlds of subjects and captures the understanding of the actors from within, thus enabling the researcher to penetrate and capture multiple constructed realities[23]. Future study could replicate the exploratory cross-sectional surveys with a larger sample within the automotive and the construction industries, as well as within other industries to substantiate the present findings, and with different types of management accounting innovations.

ACKNOWLEDGEMENTS

- The authors wish to acknowledge all respondents for their participation in both the surveys.