-

Paper Information

- Next Paper

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Finance and Accounting

p-ISSN: 2168-4812 e-ISSN: 2168-4820

2013; 2(2): 89-93

doi:10.5923/j.ijfa.20130202.06

Changing Roles of Management Accountants in Malaysian Companies: A Preliminary Study

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLAliza Ramli , Zairul Nurshazana Zainuddin , Suzana Sulaiman , Rosni Muda

Faculty of Accountancy and Accounting Research Institute, Universiti Teknologi MARA, 40450 Shah Alam, Malaysia

Correspondence to: Aliza Ramli , Faculty of Accountancy and Accounting Research Institute, Universiti Teknologi MARA, 40450 Shah Alam, Malaysia.

| Email: |  |

Copyright © 2012 Scientific & Academic Publishing. All Rights Reserved.

lobalization, intense competition, governmental regulations and innovation in technology have greatly changed the business environment. Organizations demand for more proactive management accountants, who can continuously steer the business to success. This definitely changes the roles and tasks of management accountants. The objective of this study is to explore past and future management accountants’ tasks and skills in Malaysian organizations. A survey was conducted on registered management accountants with CIMA Malaysian division. The survey findings revealed that future management accountants are required to have a broad view of the business it is in and therefore spend less time dealing with accounting issues. Management accountants are also expected to have a more strategic focus, which included the use of a range of performance measures such as non-financial measures to enhance business performance. Overall, the findings revealed that management accountants’ roles and tasks changed overtime and they are facing ongoing transformation.

Keywords: anagement Accountants’ Roles, Tasks, Management Accounting Tools, Techniques, Management Accounting Change, Factors Driving Change

Cite this paper: Aliza Ramli , Zairul Nurshazana Zainuddin , Suzana Sulaiman , Rosni Muda , Changing Roles of Management Accountants in Malaysian Companies: A Preliminary Study, International Journal of Finance and Accounting, Vol. 2 No. 2, 2013, pp. 89-93. doi: 10.5923/j.ijfa.20130202.06.

Article Outline

1. Introduction

- By means of a survey method, this paper explores the changing tasks and skills of management accountants in Malaysian organizations. The findings from this study aims to establish new criteria expected of management accountants to enable them to cope with industrial needs. Academician and practitioners will also find the results of the study relevant in designing pre-career and ongoing professional development for management accountants.Management accounting is regarded as an essential part in any organization activities. Management accounting information will enable internal users to make decision effectively and contribute to the improvement of the efficiency and effectiveness of existing operation. Management accounting has evolved from focusing on cost determination and financial control to creation of value through effective use of resources[1], thus the roles of management accountants have also changed in line with the changes in management accounting techniques. The management accounting practices in organizations, now covers a broader scope and it has also become an integral part of the management process. According to[2], management accounting attempts to influence human beings behaviour by using and interpreting financial information and seeking to link it to business strategy. In other words, management accountants provide the financial information necessary for the planning and control of organisations and commercial companies[1]. They establish and maintain financial policies and management information systems, as well as liaise with personnel from different management levels on all aspects of finance.

1.1. Research Problem and Study Objectives

- Malaysia as a developing country has moved towards global competitiveness[3]. Similar to their counterparts in other countries, Malaysian companies were experiencing changes in their business operation and have to cope with the current changes[4]. Hence, as important contributors to the Malaysian economy, companies in Malaysia must strategise well to enhance competitiveness[5]. It is imperative that companies be proactive and remained competitive to enable them to sustain their position in the market[4].[5] also pointed out that the greater global competition has led Malaysian organizations to be more forward-looking and proactive. This trend has eventually increased the significance of management accountants’ tasks, skills and tools. Nevertheless, to more closely meet the changing information needs of business unit managers, several calls have been made for management accountants to spend more time working in business units with the users of management accounting information instead of working at length within the accounting function[6]. Further to that, the ways in which management accountants interact with others have increasingly been of concern. Hence, this study was undertaken to explore the changing roles of management accountants in Malaysian organizations. A survey method was adopted to identify the past and future tasks and skills of management accountants in the local context. The remainder of the paper is organized into five sections. Section 2 draws on previous studies on the past and future management accountants’ roles, tasks and skills. While, the use of survey method is explained in Section 3. The survey findings on management accountants’ past and future tasks and skills are presented in Section 4. Finally, Section 5 concludes by presenting the contributions of the study, limitations of research method used and suggestions for future research.

2. Literature Review

2.1. Management Accountants’ Tasks

- Management accountant is a profession that involves partnering in management’s decision making, devising planning and performance management systems, and provides expertise in financial reporting and control in order to assist management in the formulation and implementation of an organization’s strategy[7]. Management accountants regardless private or public sector are closely involved in supporting, planning, controlling, directing, communicating and coordinating the organizational decision-making activities[8]. Managers of an organization are commonly the ‘customers’ of the management accountant as far as management accounting information is concerned[9]. Thus, it is important for management accountants to continuously enhance their knowledge and skill in order to fulfil the managers’ need and requirement in an organization[8]. Traditionally, management accountant is the person who gather, interpret and present financial information to people within the organization[10]. The vital roles of management accountant were believed to be information provider for both management and staff level, participants of planning and control activities[11]. Nowadays, much of management accountants’role has shifted towards supporting the manager’s decision, anticipating the information needs[10], acting as organization’s internal business consultants and involving in multi-functional team[12]. They also lead business strategies agenda and make strategic plans for business future[13] loud, 2000). Management accountants in the twentieth centuries are no longer a traditional ‘bean counter’, but now have become a ‘strategic partner’ and ‘value creator’ within an organization[14]. According to Siegel and Sorensen[9], management accountants have been working closely with their ‘customers’ and have significant role in providing accurate information, as well as, assisting in decision making. Nowadays they act as the organization’s internal business consultants and part of the multi-functional team. Researchers have also advocated for increased involvement of management accountants with users of management accounting information and less involvement in the accounting function, as a means of meeting the changing information needs of business unit managers[15] This suggests that management accountants role involvement can be both functional accounting and business unit oriented[16] Thus, to remain relevant, management accountants are expected to use more innovative tools and to play more strategic role rather than operational role[17]. The emergence of new advanced manufacturing techologies demand for more proactive management accountants, who are now expected to become part of management team within a business activity[18]. Ref.[19] posited that accountants must be prepared for changes in traditional ways of doing accounting and be ready to accept exciting challenges ahead. This is because, management accounting has made a quantum leap in recent years[10].During the past 10 years, management accountants’ roles faced ongoing transformation from ‘bean counters’ and ‘corporate cops’ to ‘business partners’ and ‘value team members’ at a center of the strategic activity[9]. Even though, management accounting profession retains its core responsibility of overseeing the finance function, its job scope has progresses beyond their traditional boundary[21]. Management accountants, currently are regarded as ‘value creator’ accountants in the business environment, which is different from a very specialist role of external financial reporting[17] It is noted that financial reporting is crucial in every business, but making the billion dollars is much more difficult than reporting the billion dollars[21]. This suggests that a value creator role is seen as a much broader role than just external reporting. Therefore, management accountant these days are required to become distinct true partners within the business who can steer the business to greater success[18]. Management accountants must look at how they can assist in adding the organization’s value and become involve in managerial decision making rather than play traditional role of ‘number crunching’ and ‘bean counting’ tasks[22].

2.2. Management Accountants’ Skills

- Management accountants’ conventional task focussed on overseeing the transaction processes and financial report preparations. However, with changes in the technology, management accountants have been able to take on more proactive roles as business planner, leader, communicator and problem solving role. The problem solving role has become relatively more important as business unit managers have faced increase uncertainty in the external environments where new and different information is needed to manage those uncertainties. Where management accounting information has not kept pace with these uncertainties, the relevance of management accounting has been increasingly questioned by business unit managers[26]. It is clear that management accountants are also required to understand operational processes together with the need to embed management accounting systems within operational activities[24]. He further added that accounting personnel should be working very closely with manufacturing managers, product and process engineers. According to Stetter[26] accountants are frequently involved with technical people in the development of new products. For example, the design of an automotive component for a certain model requires collaboration among more than a hundred people: industrial designers, design engineers, project managers, prototype experts, as well as, accountants to achieve the technical and economic objectives. According to[27], by including management accountants as part of the team members, the team can capitalize on the application of the latest cost accounting techniques in product creation process. Other benefit of including management accountants in the product development team is to develop a capital proposal on new equipment[28b].

3. Survey Method

- A survey method was employed in this study. Data were gathered through structured mail questionnaires sent to 2130 Malaysian Registered Chartered Institute of Management Accountants (CIMA) members. The aim of the questionnaire was to examine the perception of management accountants on their roles, tasks and skills. The questionnaire used in this survey was adapted from Sulaiman et al (2008), Burns and Yazdifar (2001), and other related literature. The perception of management accountants on importance of their tasks and skills over the past years (2008-2012) was measured using a five point scale that ranged from ‘Not important’ (1) to ‘Most important’ (5). Respondents were required to identify five most important tasks and skills by the year 2017, from a list of tasks and skills provided. The questionnaire was pilot tested for logical inconsistencies, questions sequence and task relevance. The distribution of the questionnaire was administered by the professional body as the members list is kept confidential. Through CIMA Malaysian, a general reminder was emailed to all members. Despite the follow-up, an overall usable response rate of 4.7 percent (100/2130) was obtained. The present survey results were tested for non-response bias using t-test[29].

4. Results and Findings

4.1. Demographic Results

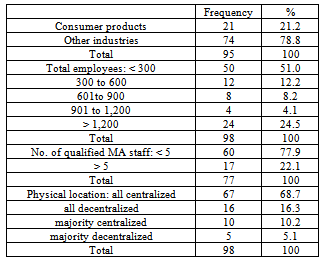

- A higher number of the respondents organizations (21.2 percent) or 21 were involved in consumer products (Table 1). Other respondents were employed by several other industries such as trading/services and industrial products. Exactly half of the organizations had total employees of less than 300. A larger proportion of the organizations or 77.9 percent (60) had less than five qualified management accountants. More than half of the organizations or 68.7 percent (67) had their management accountants centrally located along with other members of the finance function.

|

4.2. Management Accountants’ Tasks

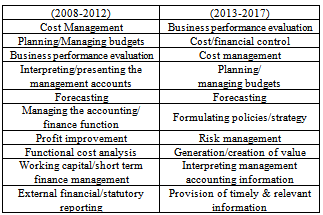

- Table 2 reveals that only ‘Business performance evaluation’ rose from rank 3 to 1 to become the most important tasks for management accountants by 2017. Meanwhile, ‘Cost management’ (rank 1 to 3), ‘Planning/ anaging budgets’ (rank 2 to 4) and ‘Interpreting/presenting the management accounts’ (rank 4 to 9) were ranked lower in the next period. ‘Cost/financial control was the only new item being ranked higher (rank 2). Other items newly included were ‘Formulating policies/trategies’ (rank 6), ‘Risk management’ (rank 7), ‘Generation and creation of value’ (rank 8) and ‘Provision of timely and relevant information (rank 10). However, five tasks that disappeared were ‘Managing the accounting inance function’, ‘Profit improvement’, Functional cost analysis’, ‘Working capital/ hort term finance’ and ‘External financial/statutory reporting’ (rank 10). Other tasks such as ‘Managing the accounting/ inance function’ and ‘Profit improvement’ were all demoted.

|

4.3. Management Accountants’ Skills

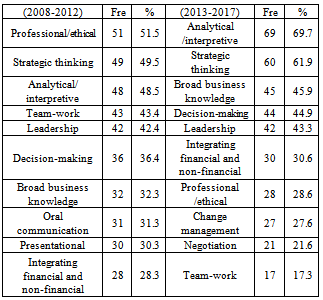

- Table 3 shows that only two new items were introduced in the 2013 to 2017 ratings i.e. ‘Change management’ and ‘Negotiation’ (rank 8 and 9). There were marked increases for ‘Broad business knowledge’ (rank 7 to 3) and ‘Integration of financial and non-financial information’ (rank 10 to 6), while a marginal increase for ‘Analytical/ nterpretative’ (rank 3 to 1). Demotion was evident for ‘Professional/Ethical’ (rank 1 to 7) and ‘Team-work’ (rank 4 to 10). ‘Oral communication’ and ‘Presentational’ were the two items which were dropped from the top ten skills list. Similarly as reported in Sulaiman et al. (2008), the present results also show a greater emphasis on strategic and value creating skills.

|

5. Conclusions, Limitations and Future Research

- The present study have explored management accountants’ perception of their past and future tasks and skills in Malaysian organizations. The survey main findings revealed that ‘Business performance evaluation’, ‘Cost management’ and ‘Planning/managing budgets’ remain the most important tasks in both short term and long term, suggesting continued broader task of practicing management accountants. Value creation and risk management are expected also to become significant tasks of management accountants. Management accountants are expected to have more strategic focus, besides increased in the use of non-financial measures to assess business performance too. With more strategic view amongst management accountants, emphasis would be on managing the capacity efficiently and effectively in enhancing an organization’s performance. They are also required to be analytical and able to interpret information which will aid management in the decision-making process. This is only possible if they have a sound understanding of the whole business in the operation and environment it is in. These skills are also essential in order for management accountants to participate in the strategic, planning and decision making processes. Managing accountants are expected to acquire the ability to drive rather than measure the business; distilling diverse information, putting it into a useful format and facilitating management decision-making. Nevertheless, in conclusion, the finding provides evidence that management accountants’ roles and tasks changed overtime and they are facing ongoing transformation. At the academic level, the results of the study would be relevant in designing pre-career and ongoing professional development for management accountants. The findings from this study can be viewed as providing additional insights into new criteria expected of management accountants to enable them to effectively cope with industrial needs locally, as well as, internationally. The limitations associated with the present study include the low response rate, sample size and generalization issue. The sample selected is limited to Malaysian Registered CIMA members. Therefore the findings from this study cannot be generalized to the whole population of management accountants’ in the country. Several potential areas for future research are suggested. Firstly, a comparative study can be carried out on management accountants’ roles, tasks and skills in different countries. Secondly, a study can be carried out to determine what drives management accountants’ role, tasks and skills to change in different countries. Thirdly, investigation can also be conducted to examine how much various factors specifically influence management accountant tasks, skills and management accounting tools to change. Finally, a case study method can be adopted to provide an in-depth understanding of factors driving the change in management accountants’ roles, tasks and skills. Thus, an understanding of the overall phenomena in its natural settings ensures deeper explanatory power to the investigation.