-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Construction Engineering and Management

p-ISSN: 2326-1080 e-ISSN: 2326-1102

2024; 13(1): 5-20

doi:10.5923/j.ijcem.20241301.02

Received: Oct. 22, 2024; Accepted: Nov. 15, 2024; Published: Nov. 22, 2024

Developing and Validating a Framework for Collecting and Reporting Maintenance Data for Life Cycle Costing of Public Buildings in Tanzania - The Case of University of Dar es Salaam and Muhimbili University of Health and Allied Sciences

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLKevin Ntiyakunze, Harrieth Eliufoo, Kimata Malekela

School of Architecture and Construction Economics (SACEM), Department of Building Economics, ARDHI University (ARU), Dar-es-Salaam, Tanzania

Correspondence to: Kevin Ntiyakunze, School of Architecture and Construction Economics (SACEM), Department of Building Economics, ARDHI University (ARU), Dar-es-Salaam, Tanzania.

| Email: |  |

Copyright © 2024 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

The study was about collection and reporting of maintenance data required for life cycle costing (LCC) of public buildings in Tanzania. The practice of LCC is important in building maintenance as through LCC, design solutions that optimize future maintenance costs can be made at an early stage of a building project. Moreover, when a building is in use, maintenance strategies and policies can be revised based on their life cycle cost impact. Despite of the importance of LCC in building projects, its practice has not yet been utilized in Tanzanian’s building industry. One of the key hindrances to the practice has been lack of reliable data. The challenge is particularly so, in maintenance whereby even though various public institutions in Tanzania undergo regular maintenance there is no centralized source of data that can be used for LCC. The study aimed to address this challenge by developing a framework for collecting and reporting maintenance data for LCC of public buildings in Tanzania. A multi-case study of two cases which were the University of Dar es Salaam and Muhimbili University of Health and Allied Science was done. It was revealed that the main issue hindering the availability of reliable maintenance data for LCC is decentralization. The estate offices do not centralize data to the building level and as a result they lack building maintenance databases for LCC. Therefore, addressing the issue of decentralization of data, a framework was developed by outlining a detailed means by which a maintenance database for LCC can be established and how maintenance data can be collected and reported in order to continuously update the database. The developed framework was then validated by experts from National Housing Corporation, Ardhi university and Muhimbili National Hospital in order to determine its adaptability, applicability and suitability in collecting and reporting maintenance data required for LCC of public buildings in Tanzania.

Keywords: Life cycle Costing, Building maintenance, Framework

Cite this paper: Kevin Ntiyakunze, Harrieth Eliufoo, Kimata Malekela, Developing and Validating a Framework for Collecting and Reporting Maintenance Data for Life Cycle Costing of Public Buildings in Tanzania - The Case of University of Dar es Salaam and Muhimbili University of Health and Allied Sciences, International Journal of Construction Engineering and Management , Vol. 13 No. 1, 2024, pp. 5-20. doi: 10.5923/j.ijcem.20241301.02.

Article Outline

1. Introduction

- Life cycle costs refers to the costs which occur during the whole life of a building. These costs include the costs of construction, renewal, maintenance and end of life [38]. The process by which these costs are calculated under an economic evaluation, is known as life cycle costing [13]. Life cycle costing (LCC) can be done during various phases of the building project starting from the inception, design, procurement, construction and when the building is in use [3]. Maintenance costs form a significant part of the economic evaluation under which life cycle costs are calculated. LCC decisions made in the design phase affects the future maintenance costs of the proposed building [12]. Furthermore, application of LCC facilitates best value for money decision and promotes realistic budgeting of maintenance and repair [38]. Despite the importance of LCC in informing design decisions [12] and its useful application in maintenance [3] and [38]. The practice has been heavily challenged by the lack of reliable data [13] and [7]. This has been a problem in various parts of the world such as Czech Republic where there are no industrial standards for reporting life cycle data [13]. Similarly, in African countries such as in Nigeria, a study by [2] revealed that one of the problems limiting the practice of life cycle costing is the difficulty in obtaining relevant and reliable data. The state of Tanzanian’s construction industry is also challenged by a lack of reliable data for LCC [25]. A study by [26] on the availability of whole life cycle cost data in Tanzania, revealed that currently there is no centralized source of running (maintenance and operational) cost data in Tanzania [26]. The problem of lack of reliable data for LCC is rooted in lack of knowledge on what data needs to be collected [4]. In addition to that, the format in which the data is reported by the estates is rarely in a form that is readily usable for LCC [38]. The challenge is particularly so in maintenance data as a lot of information is needed for accurate costing of maintenance during the life cycle of a building. [4] and [9] addressed the challenge in collection of data for LCC by detailing the maintenance data that is needed for LCC. However, it has not yet been addressed specifically, how such data can be collected and reported by the estate department in an institution in order to constitute a centralized source of data for LCC of building maintenance. Therefore, addressing the problem, the study aimed to develop a framework so that an estate department of a given public institution in Tanzania can be able to collect and report maintenance data to constitute building maintenance databases reliable for LCC.

2. Literature Review

2.1. Overview of LCC

- LCC involves an economic evaluation of life cycle costs over a period of analysis [13] and [38]. The period of analysis could be a building’s economical, technological or design life [3]. The aspects of costs considered under LCC are construction, operational, renewal, maintenance and end of life costs [14]. The construction costs include the costs of construction, professional fees, infrastructure and statutory charges [38]. Operational costs cover aspects such as the cost of cleaning, waste management and utilities such as electricity, water and gas [38]. The end-of-life costs represent the cost which occur at the end of life of the building. They include the costs of inspection, decommissioning and demolition [14]. The common economic measures of LCC are the Present Value (PV) and Annual Equivalent (AE) [38]. These are the common economic measures by which construction, operational, maintenance, renewal and end of life costs are calculated during a building’s life cycle. Through the present value method, the sums of all the future life cycle costs in a building’s life are projected and discounted to the present as a single sum. It a method that is suitable when comparing the alternative costs of investments having similar periods of analysis. The other method of LCC is the annual equivalent method. [40] defined annual equivalent costs as the uniform annual equivalent of the project’s real cost discounted over the period of analysis. It is a method suitable when one wants to determine the annualized costs of owning an asset based on different design alternatives.LCC can be done at the inception, design and during the occupancy period of a building project [3]. It is argued that it is at the early stages of the project where the maximum benefits of LCC can be realized [13]. At the inception and early design stage, the potential of cost reduction of a change in design is high and the consequent cost of the change is lower compared to later stages of the project [3]. At the early phase of the project there is high optimization potential at a very low cost [13]. LCC decisions made at the inception and design stage such as a change in design to optimize natural ventilation to reduce the costs of operations or a choice of durable materials to reduce the frequency of maintenance and repairs are easier to implement. When the building has already been constructed or when its in operation phase, the changes become costly and difficult to implement as to achieve the intended life cycle costs benefit, there would be a need of removal of already installed building components or even a complete renovation of the building. However, this does not imply that the application of LCC ceases when the building is in the occupancy stage. During the occupancy stage, LCC can be applied wherein the actual costs of operation and maintenance can be monitored versus the planned costs during the LCC calculations and provide feedback for facility management [12]. Also, through LCC realistic budgets for operation, repair and maintenance of the building can be made [38].

2.2. LCC of Building Maintenance

- According to [5] the process of LCC of maintenance involves a systematic economic evaluation of life cycle costs after the construction phase and before the end of life in order to generate maintain and renewal plans. [5] categorized maintenance costs into maintain and renewal costs. [5] Maintain costs cover annualized costs of planned, unplanned and proactive maintenance whereas renewal costs cover the annualized costs of scheduled renewal of major systems and components apart from those which fall under unplanned maintenance. In this regard the process of LCC of maintenance differs from the [14] standard whereby renewal costs are not categorized in the same life cycle cost group as maintenance costs.The process of LCC of building maintenance involves various factors that affect maintenance costs such as height of the building, age and building materials [31]. Previous authors have developed models for predicting future life cycle costs of maintenance [17] and [19]. [19] developed a LCC model from a case study of 4 universities through analysis of their 42 years maintenance and repair data. The authors developed a back propagation neural model which predicted life cycle costs of maintenance and renovations depending on age, number of floors and elevators in the buildings. Similarly, [17] studied cost data records of 13 university buildings in Osijek and developed a model for predicting life cycle costs of operation and maintenance of the buildings.

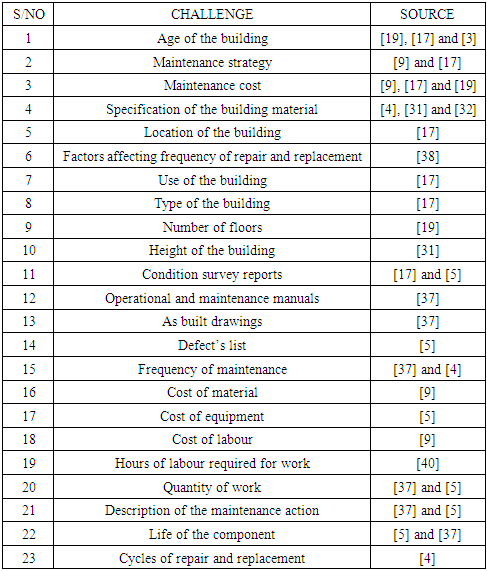

2.3. Maintenance Data Required for LCC

- The accuracy of the results from LCC is largely dependent on data [12]. The argument is also supported by [38] regarding LCC as a data intensive tool hence stressing its dependence on availability of sufficient data. Findings from studies such as [19] and [17] show that the reliability of maintenance data to yield accurate prediction of future life cycle costs is not merely on the presence of a maintenance cost database but rather there is a need for other supporting data such as the age of the building, maintenance strategy and quality of the structure. The following table 2.1 shows a summary of maintenance data required for LCC as identified from the literature.

|

2.4. Systems of Collecting and Managing Maintenance Data

- As revealed from the literature there are various systems from which maintenance data can be collected and reported during the life cycle of a building. Those systems included the manual filling system, computerized maintenance systems (CMMS), building information modelling and automated systems. The manual filling system is the traditional method of collecting and managing maintenance information that is based on human written documents [34]. It is the most common method used for collecting maintenance data among public institution in Tanzania [30]. However, it has its drawbacks, it is time consuming [1] and it leads to dispersion of data [34]. Due to this, there has been a shift towards the use of computerized systems in collecting and managing maintenance information.CMMS(s) improve the practice of collecting and managing maintenance data. Through CMMS, maintenance works can be scheduled [40], data concerning an equipment maintenance history can be tracked [10]. Moreover, it can also be used as a tool for maintenance management and facilitate a maintenance practice that is geared towards a more proactive approach [40]. However, the use of CMMS does not come without its limitations such as poor connectivity, difficulty of use and it can also be prone to errors as even though the data is managed by computers it is still entered in by humans [25].The other system of collecting and managing building maintenance information is the use of Building Information Modelling [6] and [8]. Whereby [15], integrated it with CMMS in order to develop systems for diagnosis and detection of defects. There have also been studies that have geared towards automated systems of collecting building maintenance information such as the use of digital twins [21], [27] and other sensor-based systems [34].

2.5. Previous Frameworks for Collecting and Reporting Life Cycle Cost Data

- A review of the literature identified two previous frameworks that addressed collection of maintenance data for life cycle costing. The frameworks were developed by [4] and [9]. [9] developed a generic framework for collecting whole life cycle cost data whereas the life cycle costs of an institution were broken down according to the building hierarchy. [4], developed a framework that showed details of maintenance required for LCC and the way in which the data could be structured so as to facilitate data flow into a facility management software for LCC. The following is the review of each framework.

2.5.1. Generic Framework for Collecting Whole Life Cost Data

- The framework by [9] was structured into five (5) levels. Level 1 of the framework was based on breaking down the overall cost of the project into three phases which were the capital, facility management and disposal phase. Level 2 of the framework which was called the phase level, categorized each phase in level 1 into their respective cost categories for example the facility management phase was broken down into costs of operation, maintenance and replacements. The framework by [9] presents categories of life cycle costs similar to the LCC framework by [19], whereby they have similar cost categories of operational, maintenance and replacement costs. However, there is a difference between the [14] and [9] framework. The difference is that the framework by [9] provided a much more detailed breakdown of the life cycle costs. For example, maintenance and life cycle replacement costs were broken down into cost categories of planned, reactive and life cycle replacement cost for each of maintenance work that is carried out and each cost was further broken down into the direct costs of materials, labour and equipment respectively. The framework provided a dataset of maintenance data required for LCC up to a given building’s component level. Whereas, cost of labour, materials and equipment which are essential for LCC [5] were detailed in the framework. However, there were missing information which is also vital for life cycle costing of maintenance such as the timing upon which those costs were incurred [4].

2.5.2. A Framework for Modelling and Management of Data Flow for LCC

- [4] developed a framework of data flow for LCC modelling and management. The framework consisted of three main steps. The first step of the framework involved aggregating the price of items into individual functional parts of a building. Aggregation of priced items as given in the framework [4] involved the summation of all the items that form a particular component of a building that performs a specific function. For example, summing the price of façade boards and contact insulation as the total price of external insulation to a wall of a building [4]. The second step of the framework involved acquiring life cycle information about a particular functional part of a building. The life cycle data as proposed in the framework included description, timing, quantity and unit rate of cost for each maintenance, repairs and replacements works that have occurred during a given period of a building’s functional part [4]. The framework also provided formulae which can be used to calculate parameter for LCC such as average cycles and costs of maintenance. The data obtained in step 2 is then entered into a facility management software and thereafter used as input for step three of the framework whereby the data entered into the software is used for LCC. The framework by [4] provides further details on the description of maintenance work and timing of the works which is vital for LCC [3].

3. Research Methodology

- Development and validation of the framework followed four main steps which were:i) Literature reviewii) Study of previous frameworksiii) Multi-case studyiv) Validation of the frameworkThe following is the detailed explanation on how each step contributed towards the development and validation of the framework.

3.1. Literature Review

- The first step towards development of the framework was a review on the relevant literature concerning LCC of building maintenance, details of maintenance data required for LCC, systems of collecting maintenance data and reporting of life cycle costs.Through the literature review, the researcher identified the details of maintenance data required for LCC and the means upon which the data required can be collected in order to develop a framework for collecting and reporting maintenance data for LCC of public buildings in Tanzania.

3.2. Study of Previous Frameworks Relevant to Collection and Reporting of Maintenance Data Required for LCC of Buildings

- Two relevant frameworks were studied refer to 2.5 whereby through those frameworks the researcher adopted aspects to be included in the proposed framework.The second step towards development of the framework was a study of previous frameworks relevant to collection and reporting of maintenance data required for LCC. The aspects of collecting and reporting life cycle cost data as proposed in the frameworks by [4] and [9] were adopted in the developed framework They were adopted since they detailed and comprehensive structure on the collection and reporting of maintenance data for LCC. [4] guided the researcher at the overall structure of presenting and categorizing maintenance data for LCC from the building level up to the component level. [9] guided the researcher as to the structure of reporting and details of maintenance data required for LCC of a building’s functional part.

3.3. Multi-Case Study

- The research design adopted for the study to constitute findings for the development of the framework was a multi-case study design. A case study design involves an in-depth description and analysis of the case [28]. In order to develop the framework, the researcher needed an in-depth understanding of how maintenance data is collected and reported in public institutions. Due to this reason, the researcher adopted a case study design. A case study design could either be a single case or a multi-case study. The primary focus of a multi-case study design differs from that of a single case. A multi-case study design is focused towards reaching a better understanding of the quintain as revealed from different cases while a single case study design leans more towards an understanding of the case [39]. Due to this, the study adopted a multi-case study design since the study required a better understanding of how maintenance data is collected and reported so that a framework could be developed. Similar to [41], the multi-case study included two public institutions in Tanzania. The criteria for selecting the institutions to be included in the study were that the institutions had to: (i) have an estate department (ii) Undergo frequent maintenance at least annually (iii) have buildings of various functionalities in a single location. The public institutions chosen for the study were the University of Dar Es Salaam (UDSM) and Muhimbili University of Health and Allied Sciences (MUHAS). Both institutions have old buildings which require frequent maintenance and they have various facilities in their campuses such as lecture halls, offices, dispensaries and cafeteria. Due to these reasons, they were selected as cases for the study.

3.4. Validation of the Framework

- The framework was validated following two main approaches. The first approach was through the use of the economic measures of LCC and the second approach was through the use of experts.

3.4.1. Validation of the Framework through the Use of Economic Analysis Methods

- The framework was validated by using the economic measures of PV and AEV of LCC. They are the two most common measures of LCC [38] and it’s why they were used for validation. The framework was validated to check if its application would yield a building maintenance database sufficient for LCC at the item, elemental and building level.

3.4.2. Validation of the Framework by Experts

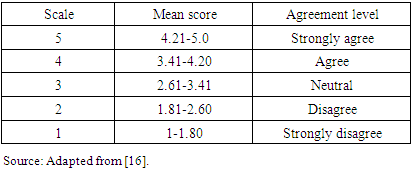

- The framework was also validated by experts. The experts selected were those who did not participate in the multi-case study so as to avoid member biasness. The experts selected for validation were from three public institutions namely Ardhi University, National Housing Corporation (NHC) and Muhimbili National Hospital (MNH). Ardhi University was selected as it is a university with similar characteristics as the cases studied. Whereas, MNH is the largest public hospital in Tanzania, therefore their experts offered an opinion on the adaptability and applicability of the framework in public hospitals. In the case of NHC, it is one of the public institutions with the largest number of public buildings in Tanzania hence opinions of their experts were valuable for validation of the framework. There were two criteria for selecting experts to be included for validation from those institutions. The first criterion was that the experts had to be maintenance practitioners working within the estate or facility management departments of those institution. The second criterion was that they had to have a professional background in either Architecture, Quantity Surveying or Engineering. A total of 9 experts were identified in the respective public institutions and questionnaires were delivered to them, 6 by hand and 3 using Google Forms. On each aspect as proposed in the framework the experts were asked to rank how they agree with such aspect using a 5-point Likert scale agree level (5: Strongly Agree, 4: Agree, 3: Neutral, 2: Diagree, 1: Strongly Disagree). A scale of interpretation as shown in table 3.1 that follows adopted from [16] was used.

|

4. Results and Discussion

- Data collected from both cases was analysed and the emergent themes for each case were the system of collecting and reporting maintenance data, surveying of the building condition and decentralization of maintenance data. The following were the findings for each theme.

4.1. Results from the Multi-Case study

4.1.1. System of Collecting and Reporting Maintenance Data

- Case A: It was revealed that the system of collecting and reporting maintenance data is mainly based on the manual filling system with some adoption of computerized system in reporting defects and tracking materials used for maintenance. Collection and reporting of data, is based on the type of maintenance work. Under planned maintenance work maintenance data is acquired through condition survey reports, bills of quantities, payment certificates and final accounts. Under unplanned maintenance the main means of collecting and reporting data is through the use of maintenance forms which are referred to as the work orders. A review of the work orders showed that they contained information regarding the location, the building, the description of the defect, the materials, labour hours and costs for each maintenance work requested. Regarding the collection and reporting maintenance data, the respondent pointed out the following challenge;“In the past we used to have a computerized system whereby through the system we could track the maintenance needs of the building and its element. Through the system we could predict when a certain element of the building needed maintenance, the costs to be incurred and the cost impact of delayed maintenance. However, the implementation of the system needed personnel to collect data in order to feed information into the system and as time went on, some of our staff got outsourced and some retired as a result the system collapsed.”It was revealed that apart from the current system used in case A for collection and reporting of maintenance data, there was a planned maintenance management system (PMMS) which was used in the past that could predict the optimum schedule and costs of future maintenance works. The system included the collection of building information regarding the building condition rating the defective scale of a building’s elements and using those scales as variables for predicting the optimum schedule and future costs of maintenance. However due lack of adequate personnel, the system had to be stopped because the personnel were not enough to collect data for all university buildings. Case B: The system of collecting and reporting maintenance data at case B is dependent on the type of maintenance work. In case of planned maintenance, the means by which information is collected and reported is through the use of condition surveys, bills of quantities, payments certificates and final accounts. Collection and reporting of data for unplanned maintenance is done through the use of maintenance requisition forms. A review of the maintenance requisition forms showed that the forms contained information concerning the location, building, section of work, description of the defect and materials used for each maintenance work. There is also a computerized system of reporting building defects whereby the user can access the system and report the defect to the estate department. Reliance on manual collection methods was pointed out to be the main challenge leading to difficulties in tracking building maintenance data. Despite the ongoing maintenance activities, the estate does not have the records on the frequency of maintenance, history on maintenance costs and materials used for the university buildings. Responding to the difficulty in keeping track of maintenance data, the respondent recommended;“If we had a computerized system for the whole institution or for the estate, we would be able to track materials and frequency of maintenance. It would be good to have a system of tracking each building we would know why this particular building undergoes frequent maintenance. It would help us to know a large proportion of the cost goes to which part and help even in the design of the new buildings.”

4.1.2. Surveying of the Building Condition

- Case A: It was revealed that during the condition surveys the defects are identified and their extent measured in order to determine the quantity of work and materials required for maintenance. It also was revealed that under planned maintenance bills of quantities are prepared through the information derived from detailed condition surveys of the building and its elements. Furthermore, it was also revealed that for unplanned maintenance, condition survey is done through the day-to-day inspection of the building condition to identify defects and report them to the estate. In order to regularly inspect the building condition, the estate in case A has categorized buildings into zone whereby for each zone there is an assigned estate officer who is responsible for assessing the building condition. Apart from the estate officers, there are building users’ representatives involved in the inspection of the building condition and reporting defects to the estate. It was revealed that the inclusion of building user’s representative had caused some challenges in reporting of building defects. The respondent pointed out the challenge by saying;“Many times, we get misleading information concerning building defects once they are reported. We receive reports whereby the building defect has not been properly described. As a result, we have to depend mostly on our own estate officers to identify and report building defects.”It was revealed despite the inclusion of building user’s representatives the work load of the estate officers had not been significantly decreased because of the limited skills the user’s lacked knowledge in construction to accurately identify and report defects. Case B: It was revealed that there is a team of experts comprising of architects, quantity surveyors, civil engineers and technicians who perform a detailed survey as a means of determining the quantity of work and materials used for planned maintenance. The primary method of surveying the building condition is through the visual inspection method whereby the respondent said the following:“In order to survey the building condition, we have to physically see something for example if there are cracks and leaking pipes, we have to see them in order to identify. On the part of electrical services, we use some equipment but mostly we rely on the visual method of identifying building defects especially for the building’s structural parts.”Under unplanned maintenance it was also revealed that it is through the day-to-day survey of building condition that building defects are identified. the regular inspection of the building condition is done by estate officers who are assigned specific zones of buildings to inspect.

4.1.3. Decentralization of Maintenance Data

- Case A: It was revealed that despite the system of collecting and reporting maintenance data through the use of condition surveys, bills of quantities and maintenance work order forms, building maintenance data is decentralized. The estate in case A, does not have databases that keep track of changes in building characteristics and records of maintenance history of its buildings. It was revealed that building characteristics information is not centralized whereby the means of storing building information is solely on the use of as-built drawings therefore information concerning the age, frequency of repairs and changes in building materials is not tracked. Also, there is decentralization in reporting maintenance costs whereby the respondent pointed out:“In the current system we do not track maintenance data for an individual building rather we have records of the maintenance costs as a whole and if there is a need for an audit the accountant can then use the records to ascertain the expenditures. We do not track the materials or cost used to repair specifically to a given building.”The estate does not centralize maintenance data at the building level whereby at the end of the year it does not produce annual cost reports specifying in details the maintenance cost spent for each building. Case B: It was revealed that maintenance data at Case B is decentralized. There is no central point upon which building maintenance history concerning the changes in building characteristics and maintenance costs can be accessed. It was revealed that there is decentralization of maintenance because data concerning the building information and maintenance cost data is not reported to the building level. It was revealed that, there are no database that centralize building information such the age, materials, use and building’s occupational details. Also, it was revealed most buildings were old and do not have their as-built drawings and as a result the estate lacks readily available information on the floor areas, heights and layouts of their building services such as plumbing and electrical systems. The respondent also pointed out decentralization in reporting maintenance costs by saying:“We report according to the plans we made for example if we planned to use a certain amount, we report the general amount that we used this much but we don’t go in details since we have the BOQ and if one wants to check he or she can trace it in the BOQ.”Hence due to decentralization in reporting maintenance costs, it was revealed that even though data was initially collected and reported in various documents such as the bills of quantities, the data collected is not centralized to produce building maintenance databases.

4.1.4. Cross Case Analysis

- Both cases have similar systems of collecting and reporting maintenance data. In both cases maintenance data is collected and reported through condition surveys, BOQs and maintenance requisition forms. Despite using similar means of collecting and reporting maintenance data, there is a difference in the forms of BOQs used in the quantification, description and costing of planned maintenance and differences in the contents of the maintenance requisition forms. Case A uses an elemental form of a BOQ while the estate office in case B uses a trades of work format of BOQ for measurement of planned maintenance works. Also, in relation to the contents of the maintenance forms used for collecting data for unplanned maintenance. It was revealed that Case A contains details on the duration of maintenance works and the costs of labour while the contents of the maintenance forms used in Case B do not contain such details. Another point of difference between the two cases is in the level of integration of computerized. Case A has a much more integrated computerized system in reporting of maintenance data whereby through the computerized system materials used for maintenance are tracked and the balance of materials remaining in the store is determined. While, Case B does not a computerized system for tracking maintenance materials, the materials used for maintenance are tracked manually. Regarding condition surveys it was revealed that both cases employ condition surveys as a means for identification and measurement of extent of defects in order to estimate the quantity of work and resources needed for maintenance in both planned and unplanned maintenance. It was also revealed that in both cases, maintenance data is decentralized and there are no building maintenance databases that can be used for LCC.

4.2. Discussion of Results from the Multi-Case Study

- Findings revealed that in both cases maintenance data concerning the quantity of work done, costs of maintenance, materials and equipment used which is crucial for LCC [9] is collected in both cases. However, in both cases details concerning the cause of defect is not reported in the maintenance work orders. Details on the extent and cause of defects are useful for LCC whereby through such information one could establish the relationship between the occurrence of defects and the factors that caused their occurrence. Through such relationship one could predict the frequency of maintenance and repairs based on the factors that caused their occurrence. Findings also revealed that the predominant system of collecting and reporting maintenance data is the traditional manual filling system. The results are consistent with [29] who also found out that most public institutions in Tanzania rely on manual methods in collecting maintenance data. The manual methods of collecting data leads to data that is dispersed [33] and this was evident in both cases studied whereby the reliance on manual methods of collecting and managing data such as filling of work order forms manually without the use of computerized systems has led to decentralization of maintenance data.Centralization of maintenance data is critical for LCC of building maintenance. LCC is data intensive [13] and there needs to be a centralized source of information for the process to be accurate. As revealed from the literature for accurate LCC, there needs to be data on the building’s characteristics and maintenance history concerning its; number of floors [19], condition [5], details on the frequency of maintenance [4], cost of materials, equipment [9]. However, this was not the status in both cases, whereby in both institutions, maintenance data is decentralized. There are no databases for individual buildings showing their maintenance history and building characteristics upon which the records on the life cycle costs of maintenance can be accessed.

4.3. Development of the Framework

4.3.1. Findings Considered in the Development of the Framework

- The framework was developed based on findings from the literature, previous frameworks and key findings from the multi-case study. Findings from the literature identified the maintenance data required for LCC. The framework developed addressed how maintenance data required for LCC can be collected and reported in order to establish and continuously update a building maintenance database for LCC. The framework also considered the details and structure of reporting maintenance data as given in the frameworks by [4] and [9]. [9], developed a framework for collecting whole life cost (WLC) data whereby the framework included the structure of presenting WLC from the project level to the component level. The framework categorized maintenance costs into reactive, preventive and replacement costs and broke down the costs of each maintenance work into indirect costs and direct costs of labour, equipment and materials. The framework developed also considered the means by which details on the equipment, materials, hours of work and labour used for each maintenance work can be collected and reported during the execution of maintenance works. The framework by [4] included the data structure containing details of maintenance data required for LCC of a building’s function part. The framework categorized maintenance work into repair, replacement and regular maintenance work and the details for LCC each maintenance work included the quantity, cost, timing, unit cost and the description of the maintenance activity. The developed framework also considered how the details provided in [4] can be collected and reported in order to establish and continuously update a database that could be used for LCC of each building’s item. The key findings from the multi-case study revealed that there are mainly two types of maintenance work carried in both cases which were planned and unplanned maintenance. Hence, the framework developed provided stages of collecting and reporting maintenance data which were categorized into planned and unplanned maintenance. Findings also revealed that the contents of the maintenance forms used for reporting data in unplanned maintenance were not consistent with the data required for LCC as revealed in the literature. As identified in [37] maintenance data regarding the cost of labour, duration of maintenance works and the factors affecting the frequency of repairs and maintenance are vital for LCC. Details on the cause of defects are not reported in both cases and details on the duration and labour are not contained in Case B maintenance forms. It was also revealed that although there is a use of BOQs, there are no forms in both cases that track details on the materials, labour and time used for planned maintenance work. Therefore, the framework developed as provided a means by which details on the causes of defects, duration of work and labour can be reported during the execution of both planned and unplanned maintenance works. It was also revealed that maintenance data is decentralized in both cases. Decentralization of maintenance data was revealed as to be the main issue which hinders the development of a building maintenance database for LCC. The framework developed provided a means by which a building maintenance database can be established. In addition to that the framework outlined a systematic and detailed means by which maintenance data required for LCC can be collected and reported in order to continuously update the database.

4.3.2. Main Parts of the Framework

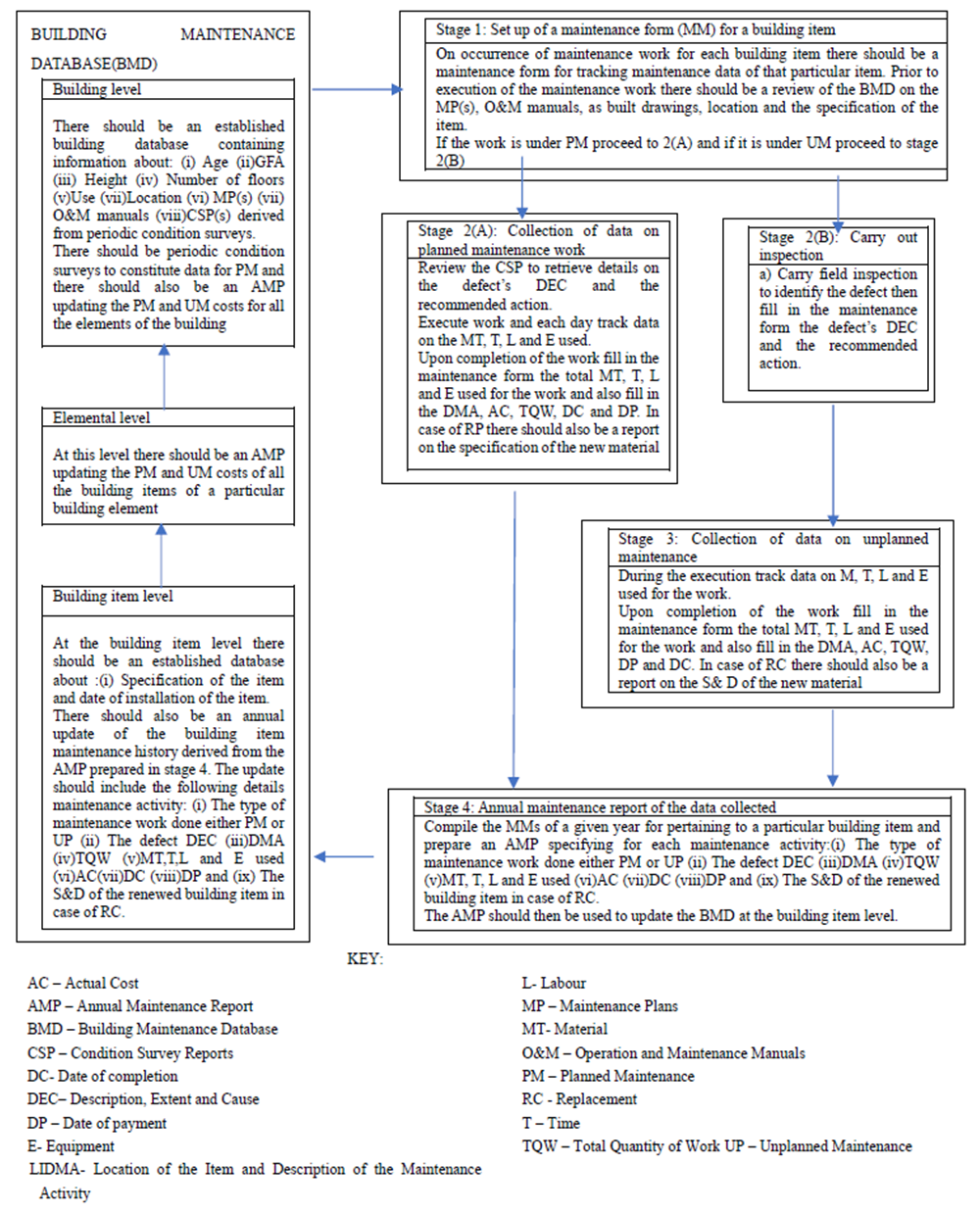

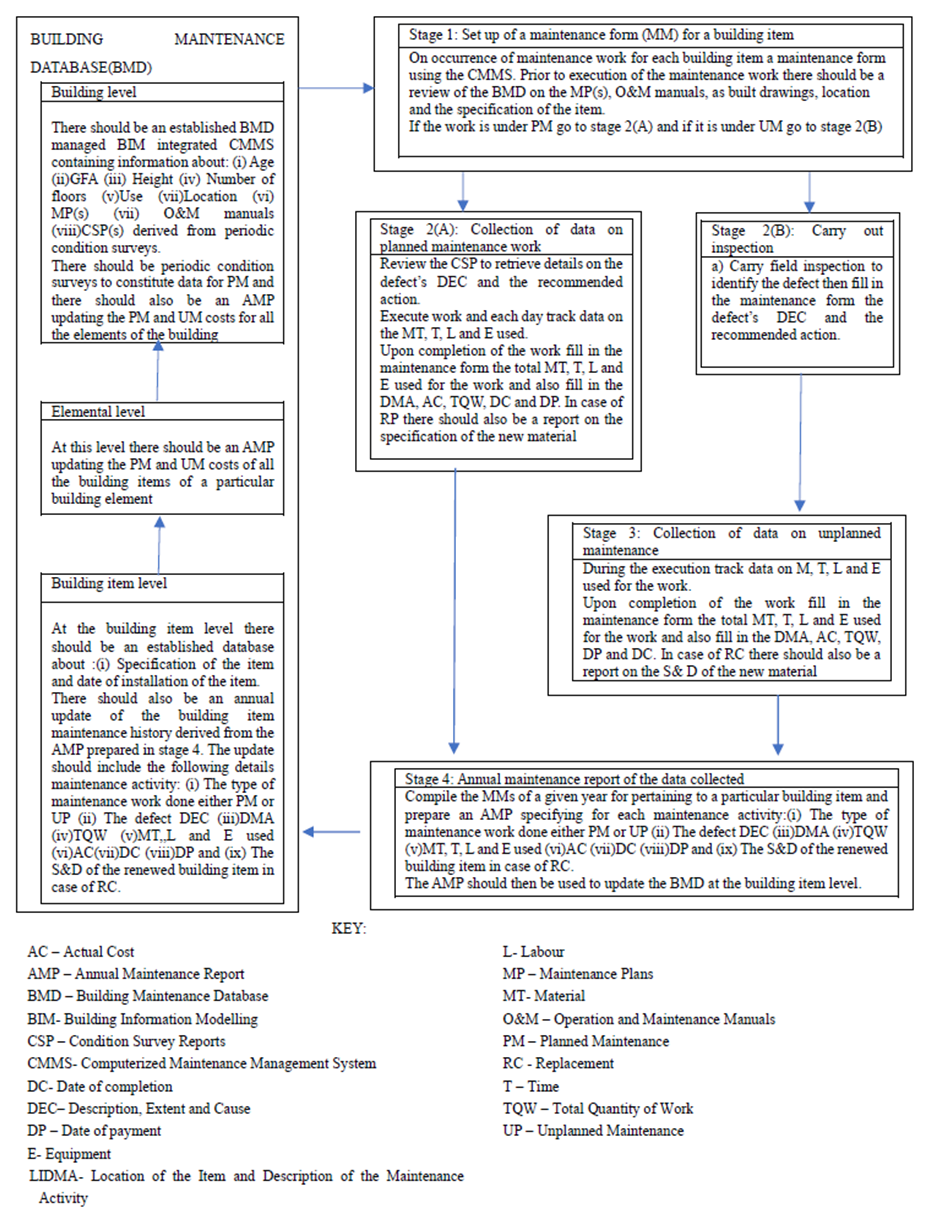

- The proposed framework consisted of two main parts which were the Building Maintenance Database (BMD) and the stages for updating the BMD. The BMD is aimed to be the means by which maintenance data required for LCC can be centralized. The BMD is structured into three levels which are the building level, elemental level and item level. The building’s level contains information on the condition surveys, maintenance plans, operation and maintenance manuals and building characteristics such as its location, age, gross floor area, height, number of floors, materials and use. The contents of the database at the elemental level include history on the costs of planned and unplanned maintenance for each building element derived from the annual maintenance reports from the item level. The item level contains information on the specification and date of installation of each building item and annual update on the annual costs of maintenance cost categorized into planned and unplanned maintenance. The annual report updating the database at the item level contains details on the description of each maintenance work, the type of maintenance action whether repair or replacement, costs, quantity, materials, labour and time used for each maintenance work done for that building’s item. The second part of the framework are the stages proposed for updating the established BMD. The stages are aimed to provide a detailed means of collecting and reporting maintenance data prior, during and after execution of planned and unplanned maintenance work in order to continuously update the BMD. The framework proposed stages 1 up to 4 for collection and reporting of maintenance data executed for each building’s item during the year. Stage 1 addresses how a maintenance form can be opened and the data that needs to be assessed prior to execution of maintenance work. Stage 2A addresses collection and reporting of data for planned maintenance. Stage 2B addresses the collection of data prior to execution of unplanned maintenance whereby since unplanned maintenance works are reactive, the framework provides a means by which data regarding the building’s defect and the recommended maintenance action can be collected. Stage 3 of the framework addresses the details of maintenance data to be collected and reported during and after execution of each unplanned maintenance work. Stage 4 of the framework outlines the details of the annual maintenance reports derived from data compiled from all the maintenance forms collected during the year for a given building’s item. The framework which was developed for validation is as shown in figure 1.

| Figure 1. A proposed framework for collecting and reporting maintenance data for LCC of public buildings in Tanzania |

4.4. Validation of the Framework

- The framework was validated using two approaches which were validation by using the economic methods of LCC and the other approach was by using experts. The following was the validation.

4.4.1. Validation of the Framework Using Economic Methods of Analyzing Life Cycle Costs of Building Maintenance

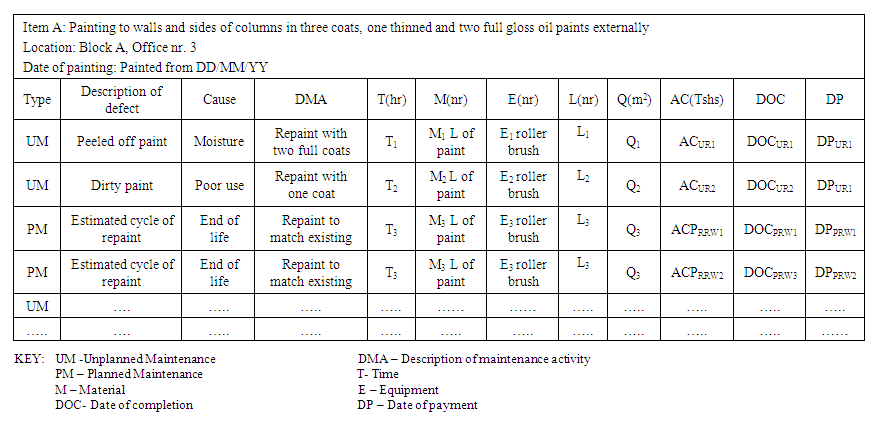

- The framework was validated such that considering a BMD that is established and updated as guided in the framework at the item, building and item level would yield sufficient data for LCC using the economic measures of PV and AEV.The following table 4.1 shows a typical database at the building’s item level as adopted and modified from [4].

| Table 4.1. An illustration of a typical database at the building item level as adopted and modified from [4] |

| (1) |

| (2) |

| (3) |

| (4) |

4.4.2. Validation of the Framework by Experts

- A total of 9 Questionnaires were sent to experts from Ardhi, NHC and MNH. 6 of the questionnaires were delivered by hand and 3 of them through google forms. Out of the 6 questionnaires delivered by hand 5 of them were returned and 3 out 3 questionnaires sent via google forms received responses. The questionnaires for validation consisted mainly of three parts which werei) Demographic profile of the respondentsii) Specific validation questionsiii) General validation questions

4.4.3. Demographic Profile of the Respondents

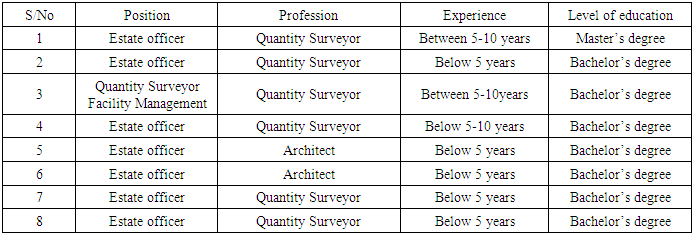

- The respondents were asked about their position in the estate or facility management department, working experience, professional background and their highest level of education. The following table 4.2 shows the profile of the respondents.

|

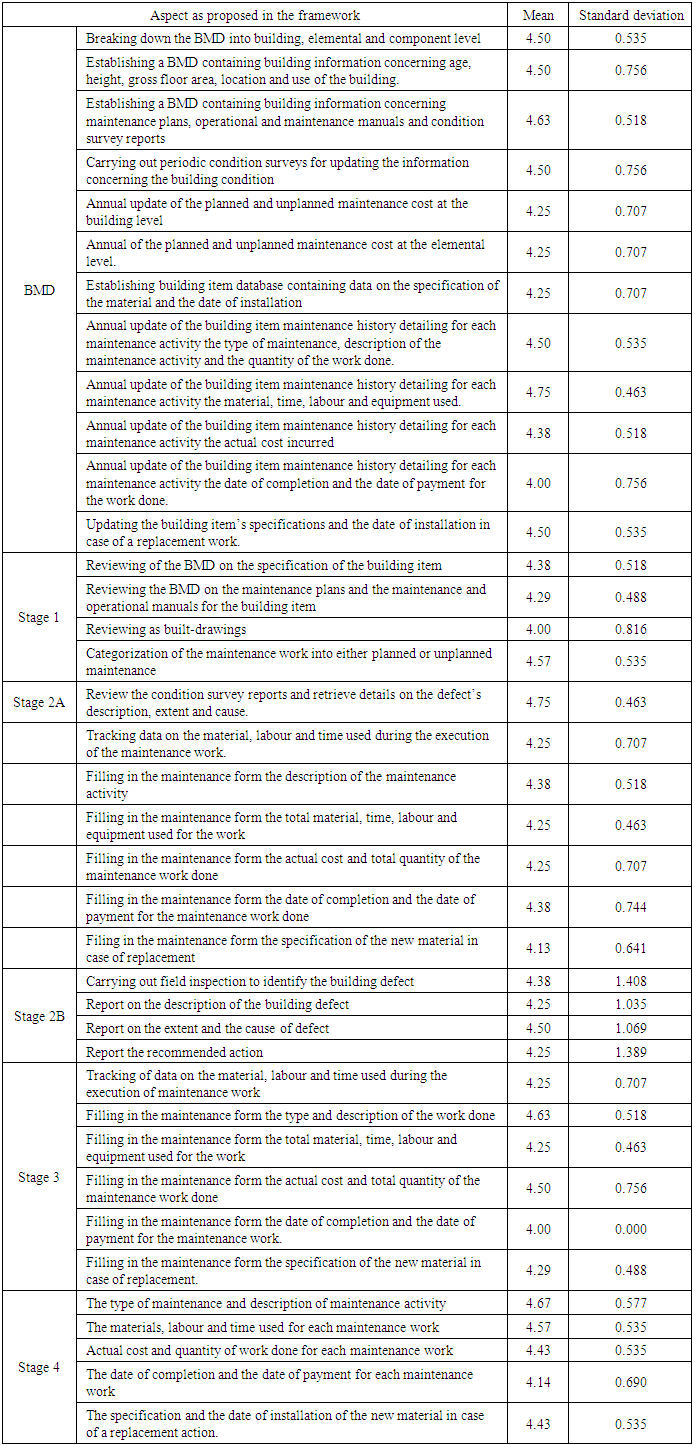

4.4.4. Specific Validation Results

- On the part of specific validations questions, respondents were asked how they agree with each aspect of the BMD and the four stages as proposed in the framework. Results are as shown in table 4.3 that follows.

|

4.4.5. General Validation Questions

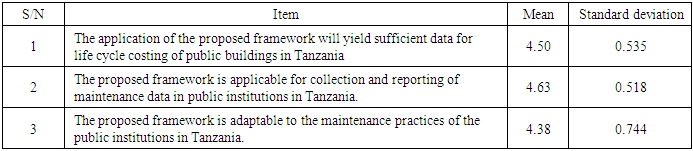

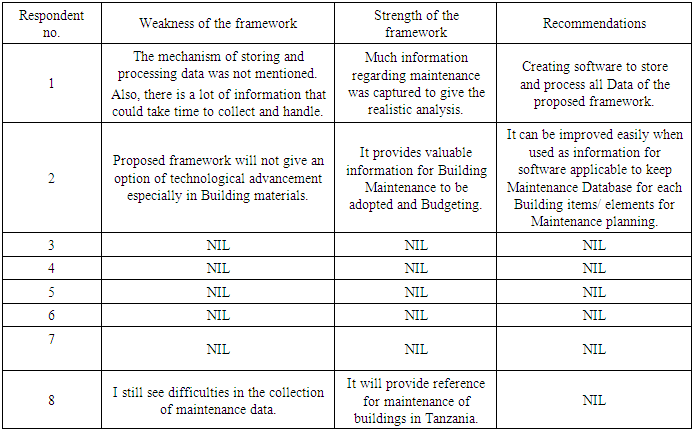

- Experts were asked on their opinions regarding the applicability and adaptability of the framework. There were also asked concerning the weaknesses and strengths of the framework and their recommendations on how the framework could be improved. Tables 4.4 and 4.5 show the results.

|

|

| Figure 2. Validated framework for collecting and reporting maintenance data for LCC of public buildings in Tanzania |

5. Conclusions

- The practice of LCC is dependent on the data available [4]. Lack of detailed information greatly affects the accuracy of its results. Tanzania lacks a centralized source of building information upon which operational and maintenance data for LCC can be accessed [26]. A study of the cases UDSM and MUHAS revealed that the main factor that hinders availability of maintenance data for LCC is decentralization of data in the estates. Despite, there being efforts to collect and report data as maintenance activities are carried out, the data collected and reported is dispersed and as a result the estates lacked maintenance databases for LCC.Due to this, a framework was developed addressing decentralization of data by providing a means by which a building maintenance database for LCC can be established and outlining stages through which maintenance data can be collected and reported in order to continuously update the database to constitute a reliable source of data for LCC of public buildings in Tanzania. The framework was validated by experts from NHC, MNH and Ardhi university whereby experts strongly agreed that the framework is adaptable to public institutions in Tanzania and that its application would yield sufficient maintenance data for LCC. Therefore, the study recommends the adoption of the framework in public institutions in Tanzania for collection and reporting of maintenance data. Furthermore, the study recommends there to be an adoption of CMMS among public institutions in Tanzania.