-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Construction Engineering and Management

p-ISSN: 2326-1080 e-ISSN: 2326-1102

2022; 11(1): 1-7

doi:10.5923/j.ijcem.20221101.01

Received: Nov. 23, 2021; Accepted: Dec. 22, 2021; Published: Jan. 13, 2022

Hindrants to Value for Money Achievement in Force Account Projects

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLMartha D. Sayi1, Rehema J. Monko2

1School of Architecture Construction Economics and Management (SACEM), Department of Building Economics, ARDHI University (ARU), Dar-Es-Salaam, Tanzania

2School of Architecture Construction Economics and Management (SACEM), Department of Civil Engineering, ARDHI University (ARU), Dar-Es-Salaam, Tanzania

Correspondence to: Martha D. Sayi, School of Architecture Construction Economics and Management (SACEM), Department of Building Economics, ARDHI University (ARU), Dar-Es-Salaam, Tanzania.

| Email: |  |

Copyright © 2022 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Force Account is a procurement method whereby a procuring entity itself or through the use of public or semi-public agencies or departments concerned executes construction projects by its own personnel and equipment. The uses of Force Account may be justified where required works are small and scattered or in remote locations for which qualified construction firms are unlikely to tender at reasonable prices or work is required to be carried out without disrupting ongoing operations. Force Account payments are based on established quantities of labour, materials, and equipment that are used to complete the work. This study was grounded on survey that involved a comprehensive review on correlated studies on achievement of value for money in construction projects executed though force account in Tanzania. The targeted information was sought to answer the research objectives of assessing the critical challenges hindering the value for money achievement in Force Account projects. Results indicate three aspects of value for Money namely; Time, Cost and Quality are not well balanced for the best attainment of achievement of Value for Money in Force Account Projects. Most of these projects put more emphasis on Cost only without considering the aspects of time and quality control. Majorities of these projects are executed in a long period contrary to the required standard time of project period. Furthermore, quality control and achievement are not attained as much as required.

Keywords: Force account, Time, Quality and Cost management, Value for Money, Public Projects, Tanzania

Cite this paper: Martha D. Sayi, Rehema J. Monko, Hindrants to Value for Money Achievement in Force Account Projects, International Journal of Construction Engineering and Management , Vol. 11 No. 1, 2022, pp. 1-7. doi: 10.5923/j.ijcem.20221101.01.

Article Outline

1. Introduction

- Force account is a payment method used for extra work when the contractor and the State Transportation Agency cannot agree on a unit price or lump sum amount, or if either of those methods are impracticable [10]. Force account payments are based on established hourly rates and the quantities of labor, materials, and equipment that are used to complete the work. This method reimburses the contractor the actual costs of labor, equipment and materials incurred in the performance of the work including allowable overhead and mark up [11]. This provision can be included in the contract when the quantities and scope of work are unknown at the time of bid letting.According to [14], as per clause 167-(2), force account is construction using public or semi-public agencies or departments concerned, where the public or semi-public agency has its own personnel and equipment. As per clause 167-(1a) of PPRA regulation 2013, the use of force account may be justified where the force account required works are small and scattered or in remote locations for which qualified construction firms are unlikely to tender at reasonable prices, work is required to be carried out without disrupting ongoing operations.

1.1. Statement of the Problem

- Force account assures efficiency gains where the entity is able to execute works much faster, enhancement of internal capacity of the procuring entity since works are executed and supervised by the procuring entity staff and cost savings compared to other methods [13].Despite the good advantages, the force account approach exposes the government to the great of risk, since it cannot pass risk on to any other entity or organization besides itself [15]. Force account operations have fundamental inefficiencies including lack of financial discipline because they are not driven by profit motives. A procuring organization will often receive additional budget allocations when it generates cost overruns unlike a private firm that has a rigid budget constraint [16]. Henceforth, this study assessed the critical challenges hindering achievement of value for money in public projects using force account method.

2. Force Account Versus Value for Money

2.1. Historical Background

- According to [1], measurement of value for money for any given project or programme, taking into account available means (time, quality, money, human resources) in the most efficient, effective, economical and equitable way. The various ways by which project stakeholders help in achieving Value for Money was also expatiated on, URT and the potential of some construction management tools [12] such as follows;a) Detailed risk analysis and appropriate risk allocationThe risk in construction projects is of varying degree of impact and occurrence/likelihood. Risks involved in construction projects can be categorised into procedural risks (consent and licensing risk), design risks, construction risks (time and cost overrun) defective construction, financing risks (changing economic condition), maintenance risks operating risks (ineffective operation of an asset), revenue risks (disappointing performance of the asset) among others.b) Drive for faster project completion A purposeful collaboration among project stakeholders in conjunction with the efficient utilization of some project management tools can serve in the good stead of reducing the overall project duration. The knowledge of several project delivery methods such as design-build, a public-private partnership, single source system etc. and the correct understanding of which of them would be most suitable to fast-track the project would help to reduce the cost associated with the elongated project schedule, hence provide value for money invested by the client. Also, the use of project planning tools such as Gantt chart, Network Diagram, and Team Planner etc. will also be of help in the bid to plan and monitor the progress of work on the site.c) Curtailment in project cost escalation A failure of the final project cost to be within the limit of initial target cost/project budget that has a significant effect on the value derivable from such project. Take, for instance, an event hall project in which the cost overrun after the project completion amounts to about 15% of the initial target cost, coupled with interest paid on borrowed capital could ultimately reduce the initial inflow and profitability for the client/owner thereby presenting a project with below per value for money invested. Hence, the identification of likely factors or activities in a project that could result in overall cost escalation and the diligence in reducing the impact (or avoiding them) could help to ensure the final project cost does not offshoot the pre-determined project budget. d) Encouragement of innovation in project developmentThe introduction of innovating strategies and concept to the process of procuring a service and/or constructing a project can increase its value to the clients and end-users hence securing a greater measure of value and/or return on investment. Innovative strategies could come in the form of the introduction of better and more efficient plants and equipment, development of an innovative solution, better motivation strategies for workers, improved framework for communication and decision making, improved supply chain management, the introduction of hi-tech facilities, development of cost database, efficiency in tracking supplies among others. Meanwhile, [4] advocated for a more innovative way in assessing the value of projects. e) Maintenance cost being adequately accounted for The application of VFM tools such as value management and life cycle cost analysis will ensure the use of durable and maintainable building element and designs that will reduce the cost required to maintain such project in the long run. Accounting for the maintenance cost should be considered at the design stage (outline design) of a project, by identifying key components of the projects, objectively decide on alternative design items or components, estimate likely maintenance cost of each alternative design components, then finally choose the most cost-effective design component based on the lowest cost, provided it gives the required function and conforms to the required quality standard. f) Accurate assessment of the cost of the project The quantity surveyor/cost engineer on the project should endeavour to carry out an accurate assessment of the cost of the project, ensuring that the unit rate assigned to each item of the bill of quantities (BOQ) takes into its calculation, the various activities, materials, labour, plants and other variable costs that are needed to carry out the task. Also, the quantity surveyor should ensure that no item of work is erroneously excluded from the BOQ, as such error of omission though may win the contract can constitute claims and subsequent disputes, which if not well managed could affect the cost of the project and could in adverse situations lead to project abandonment hence loss of return on investment to the clients. [5] Noted that when calculating the costs and risks to the government and private sector it is imperative that all costs and risks included are comprehensive and realistic; failure to do so will result in biased estimates that may lead to a less-than-optimal procurement choice and subsequent loss in value. [2] Affirmed that establishing baseline cost estimates is critical in all VFM projects. g) Detailed specifications The importance and relevance of workable specification to any project cannot be overemphasised. More so, if such specification is well detailed, that is taking into consideration all the design components, materials, the standard of workmanships, day work schedules, rates etc. The more detailed a specification is, the greater the ease by which the quantity surveyor or estimators carry out the assessment of the cost of the project, hence the more accurate his cost estimate, and as before discussed the greater the client derives a value for his investment. An undetailed specification can give rise to dispute between the various consultants, if by chance the quantity surveyor does not notice that some specifications of a design component are missing it will result in cost overrun and subsequent reduction in value derivable by the client from the project.

2.2. Critical Challenges Hindering Using of Force Account Method

3. Methodology

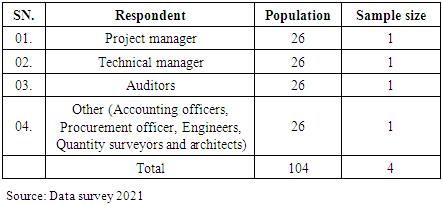

- Methodology and research design used in this study was surveying research design, which apart from literature review, questionnaires were used by approaching Accounting Officers who are the overall in charge of all Local Government activities, Procurement Managers who manage all tenders and contracts of construction works, Project Managers who closely supervise execution of construction activities on site and all related project matters, External Auditors from local Government Councils who control government expenditures including government fund spent in construction projects, and Local Labours (construction companies) that are employed to execute force account projects. The unit of analysis based on Tanzania regionals. Also, the study used both qualitative and quantitative method approach, which made it easier in determining the planned objectives, samples and design of the study.

3.1. Study Population and Sample

- Population is the entire mass of observations, which is the parent group from which a sample is to be formed [9]. Additionally, [7] confirms that; this is a group of individuals, objects or items from which the sample is taken for measurement, and it refers to an entire group of persons or elements which have one thing in common. In this study, the sample population includes Accounting Officers who are the overall in charge of all local government activities, Procurement managers who manages all tenders and contracts of construction works, Project managers who closely supervise execution of construction activities on site and all related project matters, External auditors from local Government Councils who controls government expenditures including government fund spent in construction projects, and local labours (construction company) that are employed to execute force account projects. The study employed both probability and non-probability sampling. Depending on the nature of respondents, different sampling techniques were used:i. Tanzania Mainland has twenty-six (26) regions. Each region has at least four (4) districts. Stratified probability sampling was used in this study. The rationale behind this technique is being the heterogeneity of the contractors’ population in Tanzania, in which it was categorized into strata of 4 districts each region. [9] Asserts that; this technique is precise and includes all important subpopulations; is free from bias and it ensures a sample that accurately reflects the population being studied.ii. Then, Purposive non-probability sampling was used to select the respondents within the districts. These Accounting Officers who are the overall in charge of all local government activities, Procurement managers who manages all tenders and contracts of construction works, Project managers who closely supervise execution of construction activities on site and all related project matters, External auditors from local Government Councils who controls government expenditures including government fund spent in construction projects, and local labours (construction company) that are employed to execute force account projects. These key informants were purposively sampled because they are believed to have the technical and specialised knowledge about the topic under investigation by virtue of the offices that they hold.Besides, the sample size proposed to determine what is termed by [7] as precision rate of and the confidence rate. Size of the sample should be optimum neither large nor small.To determine the sample size for small populations, the normal approximation has been used to the hyper-geometric distribution formula. It has ability to estimate sample sizes from small populations accurately (Yamane, 1967). The sample size formula is; -

| (1) |

|

3.2. Data Collection Methods

- Both primary and secondary data collection were done by using multiple sources of evidence. Questionnaire survey was used to collect primary data from contractors in which the respondents answered questions on their own, [17]. Also, secondary data regarding the critical challenges hindering achievement of value for money in public projects using force account method were collected from literature review via published and unpublished books, journals, articles and papers.

3.3. Questionnaire Design

- The Questionnaires were designed to reflect the current situation of Force Account method in public construction projects in order to answer the objective of the research [8]. “Self-administered semi structured questionnaire was used as the research instrument. A questionnaire consisted of a number of questions printed or typed in a definite order on a form or set of forms” [7]. The self-administered questionnaires cover the advantage of being flexible because they hold both open and closed-ended questions for gathering comprehensive information to ensure relevancy and consistency of information gathered as the responses are objective, standardised and comparable.The questionnaire of this study had two-parts. Part A and B. Part A carry Personal information questions and part B, each question developed to address a specific objective of the study respectively.

4. Results, Analysis and Discussion

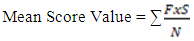

- The main objective of this research is to assess the critical challenges hindering achievement of value for money in public projects using force account method. Data were collected, analysed and presented using SPSS (20), Excel (Tables) and Microsoft Word in order to get more accurate computation that mapped out pattern or relationship between measured or comparable variables. The study adopted the use of quantitative analysis method by using syntax mathematical operation in determining the mean score,

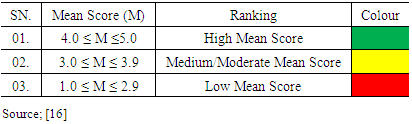

Where: F = Frequency of response for each scoreS = Score given to each causeN = The total number of respondents for each factorMean score value (M.S) comparisonThe value from mean score was categorised into three groups which the first one had the value from 4 to 5 ranked as the high mean score, from 3 to 3.9 ranked as medium/moderate mean score and 1 to 2.9 ranked as low mean score as presented in table 4.1 below.

Where: F = Frequency of response for each scoreS = Score given to each causeN = The total number of respondents for each factorMean score value (M.S) comparisonThe value from mean score was categorised into three groups which the first one had the value from 4 to 5 ranked as the high mean score, from 3 to 3.9 ranked as medium/moderate mean score and 1 to 2.9 ranked as low mean score as presented in table 4.1 below.

|

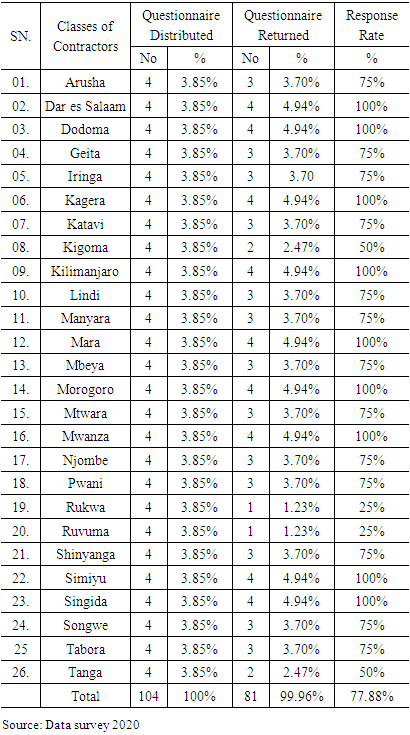

4.1. Response Rate

- The aim of this research was to assess critical challenges hindering achievement of value for money in public projects using force account method. These force account projects are the government projects that are executed by using own personnel. Government through its procuring entities, is the key decision maker of how the projects are going to be executed. The procuring entity is responsible for all the details and specifications of the force account project. In collecting data, the questionnaires were distributed to 26 regions in 104 districts where by 4 districts of each region of Tanzania Mainland were selected and requested to respond to the questionnaire. The researcher collected an overall of 97.59% of the distributed questionnaires as presented in Table 4.2.

|

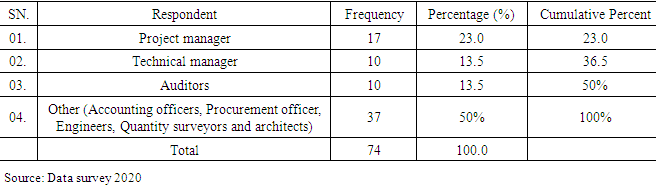

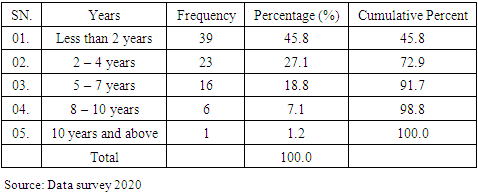

4.2. Population Characteristics

- This part mainly is comprised of general information about the respondents in terms of category of the organization, position and experience of the respondents.Position of respondents

|

|

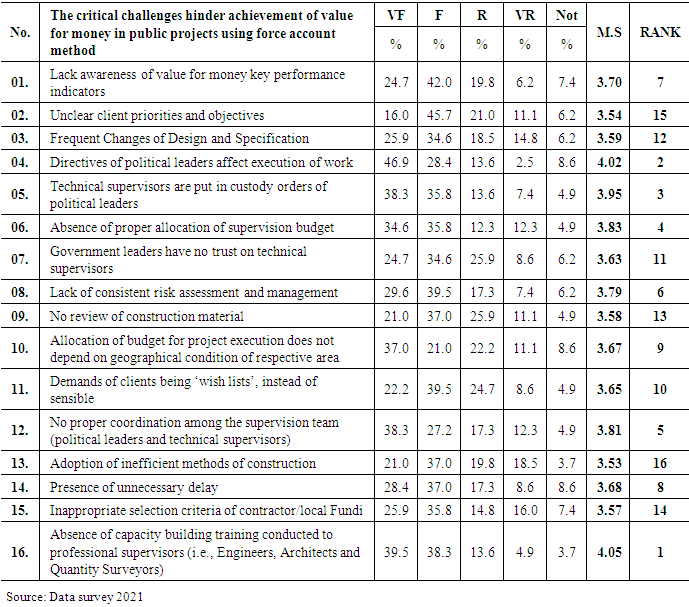

4.3. The Critical Challenges Hindering Achievement of Value for Money in Public Projects Using Force Account Method

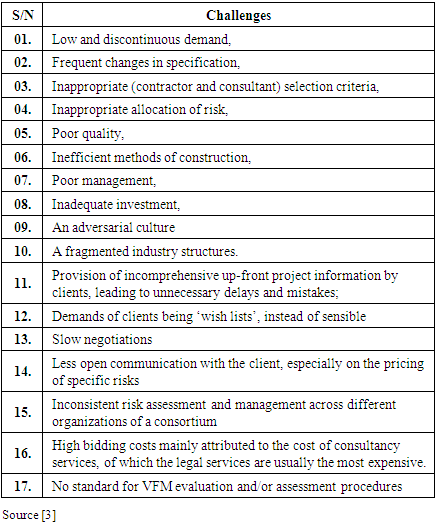

- This study is assessing the critical challenges hindering achievement of value for money in public projects using force account method, in which the following challenges were discovered; Frequent changes in specification, Inappropriate (contractor and consultant) selection criteria, Inappropriate allocation of risk, Poor quality, Inefficient methods of construction, Poor management, Inadequate investment, An adversarial culture, A fragmented industry structures, Provision of incomprehensive up-front project information by clients, leading to unnecessary delays and mistakes; Demands of clients being ‘wish lists’, instead of sensible, Slow negotiations, Less open communication with the client, especially on the pricing of specific risks, Inconsistent risk assessment and management across different organizations of a consortium, High bidding costs mainly attributed to the cost of consultancy services, of which the legal services are usually the most expensive, No standard for VFM evaluation and/or assessment procedures.Discussion of findingsTable 4.5 depicts the critical challenges hindering achievement of value for money in public projects using force account method. The obtained data on the challenges hindering achievement of value for money in Force Account project are presented in the following aspects below;

|

5. Conclusions

- This study was assessing the critical challenges hindering achievement of value for money in Force Account projects. The study revealed the critical challenges in implementation of force account projects such as Absence of capacity building training conducted to professional supervisors (i.e. Engineers, Architects and Quantity Surveyors), Directives of political leaders affect execution of work, Technical supervisors are put in custody orders of political leaders, Absence of proper allocation of supervision budget and No proper coordination among the supervision team (political leaders and technical supervisors)”.