-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Construction Engineering and Management

p-ISSN: 2326-1080 e-ISSN: 2326-1102

2018; 7(3): 101-112

doi:10.5923/j.ijcem.20180703.02

Assessment of the Performance of Value for Money for Building Projects in Local Government Authorities in Tanzania

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLHappy Simaya, Godwin Maro

Department Architectural Construction Economics and Management (SACEM), Ardhi University, Dar es Salaam, Tanzania

Correspondence to: Godwin Maro, Department Architectural Construction Economics and Management (SACEM), Ardhi University, Dar es Salaam, Tanzania.

| Email: |  |

Copyright © 2018 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

This study is focused on assessing the performance of the building projects in Local Government Authorities in Tanzania in meeting value for money. The study intended to address the declined performance of the Local Government Authorities (LGAs) that brings inefficient, ineffective, lack of transparent and accountable to most of their building projects procured. The aim was to assess the performance of building projects done at LGAs to determine the extent of compliance with Value of Money (Vfm). The methodology used was the documentary review for 30 completed audited projects by Public Procurement Regulatory Authority (PPRA) and unstructured interview to 5 LGAs official. The study revealed that there was the unsatisfactory performance of time, quality and cost as key performance indicators Vfm. Also, the findings the projects faced with the challenges of excessive delays, in adequate BOQs, lack of proper progress reports, improper preparation of the documents, inefficient supervision and absence of approval from Procurement Entities (PEs) Tender Board (TBs). The study concludes that time, quality and cost are important aspects which should be taken into consideration during the project execution. The challenges that have faced the LGAs in achieving value for money are like poor management, payments not done on time, poor preparation of tender documents and also lack of skilled contractors. It was recommended that there must be effective project management techniques, proper preparation of various documents and effective follow up of audit recommendations by the PPRA.

Keywords: Value for money, Local Government Authorities, Building Projects

Cite this paper: Happy Simaya, Godwin Maro, Assessment of the Performance of Value for Money for Building Projects in Local Government Authorities in Tanzania, International Journal of Construction Engineering and Management , Vol. 7 No. 3, 2018, pp. 101-112. doi: 10.5923/j.ijcem.20180703.02.

Article Outline

1. Introduction

- The construction industry is very important for the development of any nation. In many ways, economic growth of any nation can be measured by the development of physical infrastructures such as building, roads and bridges.In construction projects, value for money relates to functionality and cost of the built facilities. Cost is how the money is given is been spent for the projects which should be effective, On the time we consider the completion time of the project which should be within the given time without any delay and on quality this is what the final results are looked at after the use of resources, it should have the best quality of the work. Factors for ensuring value for money are like transparency, accountability, competitiveness, fairness and efficiency (Nsiah-Asare and Prempeh, 2016). Value for money is used to describe a clear assurance to ensuring that best results possible have been obtained from the money spent. In the UK Government, use of this term reflects a concern for more transparency and accountability in spending public funds, and for obtaining the maximum benefit from the resources available (Barnett, et al; 2010).There has been a dream of having LGA’s which are efficient, effective, transparent and accountable for their building projects implemented in their areas. However, periodical Vfm audits and other procurement audits done by PPRA, revealed that there are still several challenges that continue to exist even after PPRA has directed corrective measures to be employed by particular entities (PPRA, 2012). Moreover, there has been the unsatisfactory performance of completed projects as measured by Vfm indicators, which are time, costs and quality (PPRA, 2017). Regardless of a persistent decline in performance of the LGA’s, various actors believe that effective LGA’s could be achieved if the internal actors in LGA’s played their parts effectively and efficiently (Tulli, 2014). Therefore, the study explores the concept on Vfm based on key performance indicators of time, quality and cost of building projects, challenges which the LGAs are facing and the ways which could be used in solving those challenges which hinder the achievement of Vfm. The areas of the study were government funded building projects which had been audited by the PPRA from 2013-2017. This paper comprises six sections introduction, literature review, methodology, findings, conclusion and recommendations.

1.1. Literature Review

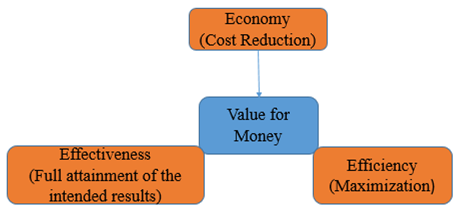

- Jackson (2012) explained that Value for money is striking the balance between the three E’s; economy (cost minimization), efficiency (output maximization) and effectiveness (full attainment of the intended results). It’s a way of thinking about using resources well. Is a measure of quality that assesses the monetary of the produced good or service (NAO, 2017). Value for money; Good value for money is the optimal use of resources to achieve the intended outcomes (NAO, 2017). VFM does not mean a tender must be awarded to the lowest tenderer thus not about achieving the lowest initial price but the optimum combination of whole life costing and quality (Nsiah-Asare and Prempeh, 2016).

| Figure 1. Defining Value for Money. (Source: Adopted from Barnett et al; (2010)) |

1.2. Key Definitions of Concepts

1.2.1. Economy

- Is the price paid, thus the actual money spent on providing services at best value taking price and quality into account (Gateshed, 2017)? Thus, it’s the minimizing of the cost of resources used for an activity. Achieving more output in terms of quantity of the input (Kasendi, 2013).

1.2.2. Effectiveness

- It measures the impact of obtaining a value for money. It can be quantitative (amount of effectiveness) or qualitative (the value of effectiveness) (Gateshed, 2017). This can be intended impacts actually achieved (Kasendi, 2013).

1.2.3. Efficiency

- Is a measure of yield on how much you get out in relation to what you put in converting resources (inputs) into the results (outputs) (Gateshed, 2017). It can be the resources spent on outputs that produce the most outcome (Kasendi, 2013).

1.2.4. Value for Money Audit

- Value for money audit is an independent investigation which gives objectives and a constructive assessment on the extent to which audited bodies used resources in carrying out the responsibilities with due regard to economy, efficiency and effectiveness (Opiyo, 2015).

1.3. The objective of Value for Money Audit

- It provides the assembly with independent information and advice about how economically, efficiently and effectively departments, agencies and other government bodies have used their resources. It is also encouraging audited bodies to improve their performance in achieving value for money and implementing policy and identify good practices and suggest ways in which public services could be achieved (Chezue, 2014).

1.3.1. The importance of Value for Money Audit

- It promotes the wise use of funds by pinpointing opportunities for the organization to spend less without interfering the extent and impact of their programmes and services or lowering their quality (Opiyo, 2015). Determine whether activities funded from resources attain their objectives are fair and if the value is created when resources are used. Also increases transparency and accountability by keeping the legislature well informed about the organization actions and the outcome of its own decision.

1.3.2. Types of Audits

- There are two types of audit: internal audit and external audit. An external audit has three types: financial audit, compliance audit and performance audit. i. A financial audit is carried in accordance with the provision of the Act. It’s to ensure a sound accounting and financial system so that all accounting transactions are under proper control and authorization. Its objective is to report on true and fair view of the financial statements and their compliance with all the legal and regulatory requirements (Loke et al; 2016). ii. A compliance audit is used to verify that all incurred expenditure has been approved and is in accordance with policies, laws and regulations (Loke et al; 2016).iii. A performance audit is in ensuring public funds were managed economically, efficiently and effectively. It determines that the government is not paying extra public money for any spending on goods or services but to achieve the established goals or objectives of at public organization. Also, it’s unique compared to financial audit and compliance audits because of its capability (Loke et al; 2016).The main goal of an audit is to inspect and evaluate the current state of the project awareness, find out to what extent it complied with defined criteria for project success and identify opportunities for improving the project awareness and supervision. The inspection can be performed after the project completion or after the end of one project recognition stage, or it can be performed during the project recognition (USAID, 2007).

1.3.3. Audit Process

- The Authority responsible for audit PPRA in particular case in order to carry out efficiently the audit exercise request selected procuring entity to make available all relevant documents listed in the audit intention letter in a timely manner.

1.3.4. Selection of the PE’s to be Audited

- According to PPA 2011 and its regulations of 2013, the selection criteria involve the volume of procurement; PEs with the volume of procurements of above 20 billion during the audited financial year; The frequency of complaints or mis-procurement allegations leveled against the procuring entity. Those with a high frequency of complaints were allocated more points and those procuring entities with cases which warranted investigation were included in the list. Results of previous audits; procuring entities which had low compliance levels in the previous audits are allocated more points; Time lapse since the last audit; procuring entities with longer time interval since they were audited are allocated more points. Geographical location; is used to adjust the number of procuring entities to be audited depending on the route in order to maximize resources utilization and Internal auditor’s reports; quarterly reports from the head of the internal audit unit of each procuring entity submitted to the Accounting Officer and later to the Authority as required by PPA 2011 (PPRA, 2014).

1.3.5. Key Performance Indicators for Compliance with VFM

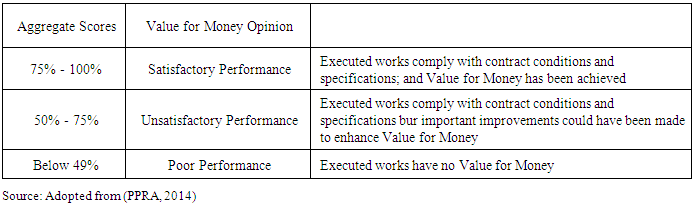

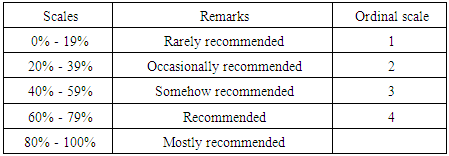

- Loke et al; (2016) and Takim and Akintoye (2007) discussed that the building industry is considered to have underperformed compared to other industry. The key performance is construction time, cost, quality and client satisfaction with the outcome. 1) Time Refers to the actual time required to produce a deliverable thus the end results of the project. Naturally, the amount of time required to produce the deliverable will be directly related to the number of requirements that are part of the end user along with the number of resources to the project (Tomtsongas, 2011).2) Quality Represents the fit for the purpose that the project must achieve to be a success. The amount of time put into individual tasks determine the overall quality of the project. Over the course of a large project, quality can have a significant influence on time and cost. When concentrating upon the project processes and the successful achievement of cost and time objectives, product success deals with the quality of the project, final project and the quality objectives of the project (Tomtsongas, 2011). 3) CostMeans amount of money or resources available. Each activity in the project has a duration and corresponding cost attributes. Activity cost increases with the shortening of the duration and the duration increases if we decrease the activity cost. In construction, the need to estimate the cost of quality in the project is a vigorous task realized as the objective of attaining a product with a good quality is not only to meet the client’s requirements but also to do it with the lowest cost (Anuar and Poh kiat Ng, 2014).4) Value for Money Audit Opinion In this case, value for money assessment criteria, scores for every audited project were collected and the overall performance of the project was evaluated depending on the computed collected score. Three different VFM views relating to three (3) ranges of collected scores for individual projects were shown as on the table below.

|

1.4. Challenges Faced Adhering to Value for Money in Building Construction Projects

- i. Insufficient Tender DocumentsIn this case, it shows that tender documents are not well and sufficiently prepared hence bringing confusion and changes during the execution of the project. Mostly the incompleteness and insufficient information are seen on the BOQs, drawings and and specifications. Some PEs fail to clearly articulate the goods or services to meet their requirements thus making it difficult at a later date to implement the contract (Chimwaso, 2013; Semen, 2014; Jatarona et al; 2016). ii. Unethical behavior among PEs Officials This is unacceptable behaviors like awarding contracts to companies belonging to themselves or their relatives without undergoing the tendering process, obtaining tenders through quotations from a single supplier, soliciting bribes in order to influence tender award decision, approval of variations to suppliers and acceptance of low quality goods or services (Semen, 2014; Chirchir, and Gachunga, 2015).iii. Poor contract administration Include failure to give the necessary approvals, acceptance of poor quality goods or services and delayed payment to suppliers or services providers. Others include poor workmanship resulted from poor supervision and Late approval in giving the extension of time (Semen, 2014; Jatarona et al; 2016). iv. Incomplete or non-completion of projects On this, the buildings were not completed within the given time on the contract and thus there were liquidated damages which were supposed to be imposed but they were not (Jatarona et al; 2016).

1.5. Research Gap

- Aspect of Vfm have addressed by Staples and Dalrymple (2012); Jackson (2012); Chezue (2014); Ademan, (2014); Osei Owusu, et.al (2014); Opiyo (2015); Nsiah-Asare, and Prempeh (2016) who did studies on the benefits, techniques and audit practices for vfm. Challenges in complying with public procurement regulations have been studied by Chigudu (2014) in Zimbabwe; Biramata (2014) at Tanzania Ports Authority and Ivambi, (2016) for Public organizations in Tanzania; Adusei, and Awunyo-Vitor (2015) in Ghana. Also, Ngogo (2014); Abere, and Muturi (2015) conducted studies on the factors affecting compliance with the Public Procurement Regulations in Tanzania and Kenya respectively.Jha, and Iyer, (2007); Takim and Akintoye (2007); Saraf (2015); Jatarona et al. (2016); loke et al. (2016) did studies on public construction projects performance and factors affecting Quality performance in construction projects in Malaysia.Therefore, based on the analysis on the body of knowledge from the previous studies with regards to Vfm the research identified a limited knowledge on the performance of vfm in building construction projects which need to be addressed.

2. Methodology

2.1. Introduction

- In this study, the data are classified based on the objectives. The data collected and information are processed by using the required techniques of data processing which are tabulating, editing, and classification for easy interpretation. Data analysis is conducted and interpreted according to their corresponding with specific objectives. To achieve the objectives of the research, data were presented by using tables for the analysis to be clear and easy to understand by readers but also one to be interested in the topic for further studies. Conclusion, recommendations and suggestions are drawn from the analyzed data since data analysis helped to get the main idea from the research findings.

2.2. Research Design

- The type of research design to be used was descriptive research design whereby the researcher interested in describing a particular situation or phenomena under (Farooq, 2013). The study was qualitative in nature with regards to collection, analysis and presentation of the collected data.

2.3. Sampling Technique

- The population of the study is based on audited VFM PPRA reports for building construction projects executed by Municipal Councils and City Councils within Tanzania in five financial years 2011/12, 2012/13, 2013/14, 2014/15 and 2015/16.The section of the population based on the fact that they have a larger number of building projects. Therefore, the population of 90 building projects 75 for Municipal and 15 for City councils which have been audited for the period of five years were identified. Systematic random selection technique was employed to select a sample size of 30 out of 90 projects for review. The chosen sample size represents 1/3 of the populations for which the researcher looks adequate and it is representing the population. Convenient sampling techniques were used to obtain information from five (5) Heads of Procurement Unit (HPMUs) from Ilala, Kinondoni and Temeke municipals councils in Dar es Salaam, Dodoma and Morogoro municipals councils.

2.4. Data Collection

- Is the systematic approach to gathering and measuring information from a variety of information from a variety of sources to get a complete and accurate picture of an area of interest. It enables a person to answer the relevant question, evaluate outcomes and make predictions about future probabilities and trends (Rouse, 2016).

2.4.1. Document Review

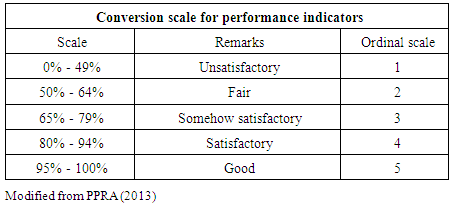

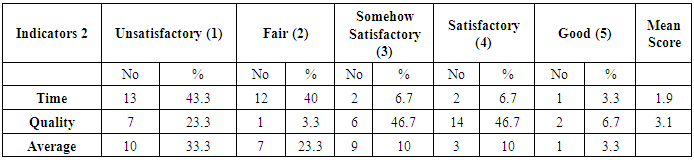

- The audited reports for the said period were reviewed mainly to determine project performance indicators of quality, cost and time. The indicator was assigned a scale of five (5) having Unsatisfactory (1), Fair (2), Somehow satisfactory (3), Satisfactory (4) and Good (5) for performance in quality, cost and time indicators.

2.4.2. Interviews

- The researcher had an interview with HPMUs discussing various issues related to challenges in achieving Vfm in their procurement. Interview Method involves the presentation of oral verbal and replies in terms of oral-verbal responses. The type of interview to be used by the researcher is the unstructured interview. The interview session took an average time of 20 minutes.

2.5. Data Processing and Analysis

- Data processing is concerned with editing, coding, classifying, charting and tabulating research data (Francis, 2015). On this study data processing and analysis involved tabulation, classification basis on ranking scale used on data collected and literature review. Tables 2, 3 and 4 displays the ranking scales for data analysis for the findings from all the specific objectives. The objective ranging was from 1 to 5.The table below illustrates the scale which is used for analysis of key performance indicators which is from the documentary review. It has a scale of five (5) having Unsatisfactory (1), Fair (2), Somehow satisfactory (3), Satisfactory (4) and Good (5).

|

|

|

3. Results and Discussion

3.1. Performance Indicators for Value for Money in Building Projects

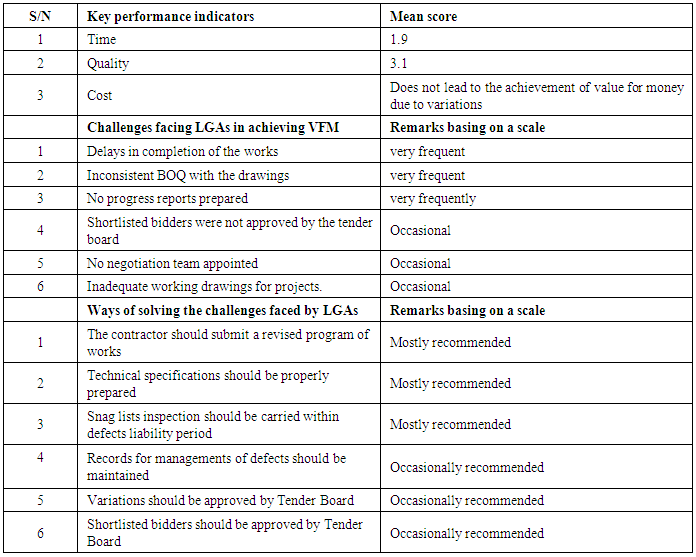

- The key performance indicators have been used in evaluating Vfm whether it has been achieved or not. For this study, there has been the use of time and quality parameters to measure the Vfm as analyzed from the table below.

|

3.2. Challenges Facing LGAs in adhering to Vfm in Building Projects

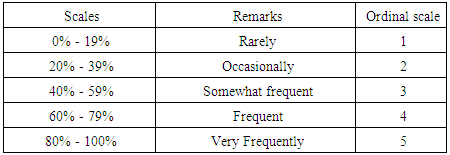

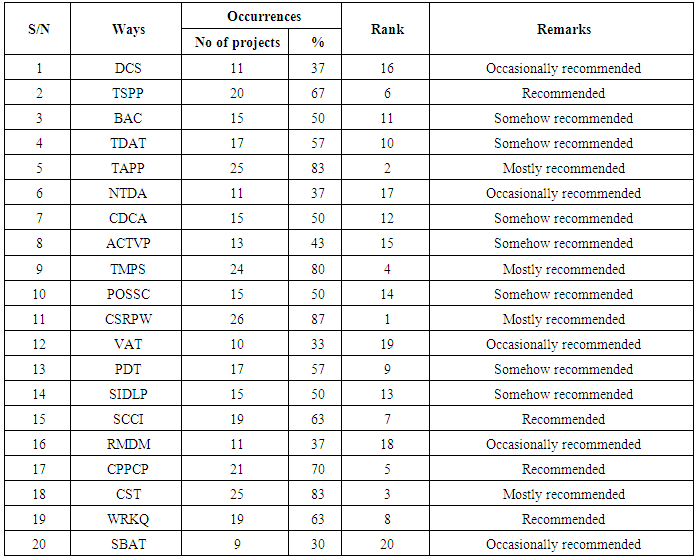

- There are challenges which are facing the Local Government Authorities which have made them not to achieve value for money. These challenges have been extracted from the documentary reviews and also interview has been made to the members of the LGAs. The extracted data is analyzed in form of table 6. Table 6 illustrates the challenges faced by Local Government Authorities whereby the challenges are in a coded form which is 20 in number and the building projects are 30 in number. Also, there are letters used which are, V represents that there is a challenge and X represents that there is no challenge. From the table, we can see that there is a challenge having the highest score of 80% implying very frequently meaning that this challenge on delays for completion of the works (DCW) has been faced by a large number of projects which are 24. There is another challenge which has a frequent result which means that it is also a problem to this PEs for the achievement of Value for Money (Vfm) and their score is 70% for 21 projects for the challenge on inconsistent BOQ with drawings (IBQD), 63% for19 projects for the challenge on no progress reports prepared (NPR) and 60% for 18 projects for the challenge on no approval for tender documents (NATD). Furthermore another challenge which has somehow frequent result which means that it is also a problem to this procuring entity (PEs) and their score is 53% for 16 projects for the challenge on inadequate specifications (ISPE), 53% for16 projects on the challenge, poor management of contract securities (PMCS), 47% for 14 projects on the challenge, poor management of the defects liability period (PMDLP), 43% for 13 projects o the challenge, no material testing records (NMTR), 40% for 12 projects for the challenge on delays for award of contract beyond tender validity period (DAC), 40% for 12 projects for the challenge on no snag list prepared (NSL), 40% for 12 projects for the challenge on improper issuance of the practical completion certificate (IIPCC) and 43% for 13 projects for the challenge on no submission of contract award to PPRA for publication (NSCA). Additionally, another challenge is having an occasional result which means that it is also a problem to this procuring entity (PEs) for their achievement of Value for money (Vfm) and their score is 37% for 11 projects with a challenge on Inaccurate contract document and irrelevant Special Conditions of Contract (ICDSC), 37% for 11 projects with the challenge of Poor management of the extension of the contract period was not properly handled (PMET), 37% for 11 projects with the challenge on shortlisted bidders were not approved by the tender board (NASB). 30% for 9 projects with the challenge on no negotiation team appointed (NGT) and 23% for 7 projects with the challenge on inadequate working drawings for projects (IWDP). There was no challenge that had a rare score meaning that all the above lead to this LGAs does not achieve value for money.On the interview part, respondents from the local government authorities addressed the challenges faced that lead to the building projects not to achieve value for money as follows;

3.2.1. Local Government do not Pay on Time

- One of the respondents said that; “When it happens that the authority is to construct a building by using its own fund, there has been a problem because they depend on internal raising of the fund which may take a long time hence when the project has started their times they have no more to continue with the execution hence delays in time and quality” Another respondent said that, “The funding of the projects comes on phase meaning that their times when the execution of the project has to stop to wait for the payment whereby during that phase there can be delays in receiving the money hence leading to delays on the project thus affecting quality and time”.

3.2.2. Poor Management

- One of the respondents reported that “The number of staffs has been a problem whereby there can be many projects but few staffs who could do the supervision” Another respondent said that “Within the organization the number of staffs which includes the quantity surveyors, architects and engineers are few. Therefore, some of the projects like supervision due to the fact that there are few numbers of workers who could supervise these projects hence leading to poor quality”.

3.2.3. Political Interference

- One of the respondent address this that “The councilors are not familiar with the tendering process thus they tend to bring about politics even in acquiring the contractor who will execute the work and there after the tenderer who win the tender is no competent and there after brings problem during the execution of the contract”. Another one said that “The politicians have been a barrier in achieving value for money because on the specifications part they do not approve on the specifications which have been made by the engineer saying that they are spending unwisely their money. So these local government authorities tend to follow the politician's needs because they are the users hence at the end quality is been affected”.

3.2.4. Poor Preparation of Tender Documents

- One of the respondents said that “Some of the staffs are not competent in preparing these tender documents, for example, the BOQ, drawing and even specification which at the end leads to variations which also leads to the delay of the project” Another one said that “Poor preparation of this tender documents have led to a restructuring of the tender document when the project is being executed hence leading to dragging behind of the time completion date and also affecting the quality of the project when the process has to take a long time to its updating”.

3.2.5. Lack of Competitive Contractors

- One respondent said that “There times when the Local Government Authorities have small assignments to be undertaken thus they do not follow the bidding procedure in acquiring those contractors hence the contractors who are given that assignment are unqualified contractors” Another respondent said that “There has been cheating during the tendering process whereby the person who wins the tender is not qualified hence becomes a burden during the contract execution”.

3.3. Appropriate Ways of Achieving Vfm in Building Projects

- There are ways which are used in solving the challenges that are been faced by the Local Government Authorities which have made them not to achieve value for money. These ways have been extracted from the secondary reviews and also interview has been made to the members of the Local Government Authorities. The extracted data were analyzed in form of table 6.

|

3.4. Payments should be Made on Time

- One of the respondents said that “The LGAs should have enough money on their own so as in case of any emergency needed in the construction process they can be able to solve it easily and undertake the process smoothly.

3.5. Avoid Political Interference

- It is the right of councilors to be involved in the decision making because they are the end users but their rights should be minimized in the case that when they present an idea, they should wait for implementation or outcomes but be involved indirectly. One of the respondents said that“The politician’s rights should be minimized by not participating in tendering process because they have no knowledge about it. So, in case of any problem during the implementation process they should be told but otherwise, they should wait for the outcomes”

3.6. Proper Preparation of tender Documents

- Tender documents should be prepared by skilled workers because it is the one that carries the whole process of how the project will be executed. Thus messing with it will lead to poor result at the end. One of the respondents said that “If skilled workers prepare these tender documents it will be well prepared and reduce ambiguities during the execution of the projects and thus problems caused due to poor preparation of the tender documents will not happen”.

3.7. Skilled Contractors

- Contractors that are chosen to undertake the tender by following the procedures should be skilled and those who are capable of undertaking the project till its completion. One of the respondents said that “Contractors selected should have all the criteria needed for the execution of the work so that when given a project, assurance for the achievement of value for money is automatically”.

3.8. Operational Issues

- The government should set a certain money that will be able to run this local government whenever they need to undertake a certain project it can be easily done from commencement until its completion. One of the respondents said that “The government should have enough budget for the LGA and avoid giving us the money in phases because this affects the execution of the project when the money does not reach on time and thus affecting the achievement of value for money”.

3.9. Summary of Key Findings

4. Conclusions and Recommendations

- This section presents the summary of the major outcomes based on the specific objectives of the study and drawing conclusion on what was to be done on assessment on the value for money audit for building projects in local government authority (The case of PPRA) so as to provide solutions to problems that lead to the procuring entities not to achieve Vfm in the building projects.

4.1. Conclusions

- On the key performance indicators, which are time, quality and cost, it is noted that there was unsatisfactory performance. It has been concluded that time parameter unsatisfactory performance had scored high percentage. On the quality parameter, the high percentage of was covered by satisfactory performance. This was supported by interview results that show that said that quality and time parameters are not satisfactory achieved. On the cost aspect, it was concluded that there has been cost over runs which have affected the achievement of Vfm. That brings achievement of Vfm for the projects to be poor with the late completion of the projects, poor quality and workmanship and the cost has been affected due to variations. Challenges facing LGAs in adhering to Vfm in building projects noted were LGAs do not pay on time, Poor management, Political interference, Poor preparation of tender documents and Lack of competitive contractors.

4.2. Recommendations

- The AOs of the audited entities should be required to implement the specific audit recommendations provided in the audit reports and submit a report of implementation status. In this it will be easy to notice what was recommended is not repeated on another project by the same entity. There should be a special unit which is concerned with quality assurance so as it can be able to enable the entities to know how to overcome the weakness on the next project execution. This recommendation is made on the basis of the fact that in most of the audited projects, the responsible contractors, consultants and project managers are not at the site when measurements are made. They are supposed to be there so as respond to the issues observed before making further decisions.Measure quality of the works and at the end achieve value for money. This is important because the works will be of a good quality because of other supervision on the project execution. The PEs should prepare and submit to the Authority an action plan on how the entity is going to address the weakness observed for future improvement of the procurement process.