-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Construction Engineering and Management

p-ISSN: 2326-1080 e-ISSN: 2326-1102

2015; 4(5): 180-190

doi:10.5923/j.ijcem.20150405.03

Application of Hedging Principles to Materials Price Risk Mitigation in Construction Projects

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLGary P. Moynihan , Mohammad Ammar Al-Zarrad

Department of Civil, Construction & Environmental Engineering, The University of Alabama, Tuscaloosa, U.S.A.

Correspondence to: Gary P. Moynihan , Department of Civil, Construction & Environmental Engineering, The University of Alabama, Tuscaloosa, U.S.A..

| Email: |  |

Copyright © 2015 Scientific & Academic Publishing. All Rights Reserved.

Construction projects are exposed to many forms and degrees of uncertainty and risk, such as price materials volatility and shocks. Materials price uncertainties are pervasive throughout the project lifecycle, occurring at project initiation and continuing through execution. This research addresses the problem of material price volatility by presenting a step-by-step guidance to applying material hedging to mitigate the risk of material price fluctuation. Material hedging was investigated via the fuel hedging application utilized by airlines. The weather hedging process was subsequently used as a precedent for application to the construction industry. The resulting model provides a step by step guidance to apply material hedging in the construction industry. Further, this model is integrated to predecessor work, and provides an improved level of detail intended to support actual implementation of the material hedging technique.

Keywords: Cost Estimation, Construction Materials, Price Risk, Hedging

Cite this paper: Gary P. Moynihan , Mohammad Ammar Al-Zarrad , Application of Hedging Principles to Materials Price Risk Mitigation in Construction Projects, International Journal of Construction Engineering and Management , Vol. 4 No. 5, 2015, pp. 180-190. doi: 10.5923/j.ijcem.20150405.03.

Article Outline

1. Introduction

- Cost estimation is considered to be a critical component in the budget development for any construction project. Materials price uncertainties are extensive throughout the project life cycle, occurring at project initiation and continuing until termination. As a result, further investigation is recommended to evaluate new techniques to reduce the risk of construction material price fluctuations.

1.1. Risk Aspects of Construction Estimation

- Construction material suppliers faces serious financial risks due to their high debt to equity ratio structure and the nature of the material import trade [2]. Construction projects are exposed to many forms and degrees of risk, such as price volatility and shocks. Within a project context, risk may be defined as the probability of an undesired outcome that has the potential to reduce the possibility of meeting the project objectives [1]. Managing these risks has been recognized as a critical management process. Highly volatile raw material prices and ineffective price management can jeopardize a company’s success greatly. Major construction projects may involve multiple years of work which further increase the risk of material price change over time. Volatility in construction material price leads to financial risk and could potentially result in corporate failures.The engineering, procurement and construction (EPC) industry has tried to address this risk through numerous approaches. Most current approaches for material risk assessment are deterministic, i.e. that they treat variables such as price as if they were fixed. However, in reality material price frequently fluctuates both up and down [3]. Probabilistic approaches quantify this variation by using distributions instead of fixed values in the risk assessment. A distribution defines the range of possible cost values, and shows which values within the range are most likely. Taking into consideration the full range of possible cost outcomes can improve decision making about material risks [3].Simulation optimization is another way to manage risk. Optimization in general is maximizing the desired outcome for a specific level of risk or minimizing risk for a specific outcome [4]. A probability distribution describes the outcome of a decision under certain risk. Decision making under risk can be optimized using the expected value criterion in which alternatives are compared to identify the alternative that maximize expected profit or minimize cost [4]. Currently, indemnification and insurance provisions are the primary risk mitigation devices in any construction contract. These provisions obligate the party with less bargaining power to insure the other against certain risks. These contractual provisions could help the two parties allocate materials risk and other risks contractually [5, 6]. However, they cannot address unforeseen circumstances that can affect materials pricing (e.g. disruption of oil supplies due to Middle Eastern conflicts).Another major limitation is that these current approaches for material risk assessment do not reflect price volatility issues. Cost escalation of construction projects can be defined as the deviation of final project costs from the initial cost estimates [7]. Materials price fluctuation is one of the main factors that causes cost escalation in construction projects. By identifying and controlling cost escalation drivers construction companies can improve their cost estimates [7].

1.2. Materials Price Fluctuation

- According to Spillane [8], construction materials may encompass 50-60% of the total cost of a project if combined with other services such as equipment. When left unmanaged, materials may have even greater impact on project cost. Materials price uncertainties are extensive throughout the project lifecycle. Fluctuations of materials’ prices are a driver of project costs. Volatility is a measure of the amount and rapidity of these price changes, regardless of whether it indicates a financial increase or decrease. Consideration of volatility is important, not only because price escalations may occur, but because price adjustments also potentially impact resources allocation and project selection decisions [1]. Contractors are highly affected by the radical increases in the cost of raw materials, especially when they take on projects utilizing fixed price contracts. When material prices increase significantly during the course of a project, both the contractors and the clients are negatively affected. Contractors can find themselves facing major losses, while clients face the risks of contractors either going out of business at the middle of the contract, or trying to source low quality materials to overcome pressures. Historically, raw materials' prices typically only moved up (in one direction). A manager was tasked with estimating the rate of the increase and timing his orders to get ahead of the price hikes. Prices for key raw materials frequently fluctuate up and down, and it can be a critical mistake to take delivery just before prices fall. Further investigation, to evaluate alternate techniques to reduce the risk of construction material price fluctuations, is needed.

2. Literature Review

- A hedge is a type of investment that is projected to offset any potential losses that may be incurred by an associated investment. Hedges are normally established in the financial industry, through the use of derivatives. These derivatives, in general, are contracts whose value is derived from one or more variables called underlying assets (e.g. fuel). Both forward and future contracts are types of derivatives established to buy or sell something at a future date at a fix price. In contrast to forward contracts, futures contracts trade on specific central exchanges, called future markets [9]. Another category of derivative is referred to as an option. Options are of two types: calls and puts. Options give the buyer the right, but not the obligation, to buy or sell a certain quantity of the underlying asset, at an agreed price on or before a certain future date [9]. The last type of derivative is called a swap. Swaps are private arrangements to exchange cash flows in the future according to an agreed formula [9]. Companies choose the hedging tool according to their specific needs and plans. The formerly mentioned derivatives utilize different time periods, as suggested by Long [10]. Forward contracts’ time period is up to one year, which is considered to be a short-term contract. Future contracts’ time period is up to 5 years, and it is considered to be a medium-term contract. Finally, swaps and options that are up to 10 years are considered to be long-term contracts. Regardless of the derivative type, there are four general hedging strategies that a company could use [9]:1.” No hedge at all;2. Optimal hedge ratio - this strategy determines the number of contracts to purchase at the beginning of the hedging period based on the ratio of the covariance and the variance of the future contract price;3. Dynamic hedge ratio - this is the dynamic version of the previous strategy in which at each trading opportunity, covariance and variance will be updated.” It has been established that although derivative use can be effective in terms of managing financial risks, it may be expensive [11]. The literature also suggests that risk avoidance via derivatives is not limited to financial-related institutes, but may also be applied to other industries [12]. Although, some mention of the use of hedging has appeared in the literature regarding the transportation industry, in general, the most detailed information has been found to pertain to the airline industry.

2.1. Application of Hedging in the Airline Industry

- Fuel hedging has been used by the airline industry for many years, since fuel prices have been viewed as more unstable than their other operating costs and expenses. Jet-fuel expenses represent a significant cost factor for airlines, comprising 10% to 20% of the firm's total operating expenses [13]. Price volatility further leverages this impact. For example, for every $1 increase in fuel price, U.S. airlines face an additional annual cost of $425 million [14]. Moreover, these levels of instability themselves are extremely variable [13]. Thus, passing fuel costs to passengers is difficult when fuel prices peak quickly. Since air tickets are purchased at varying times in advance of the actual fuel cost increases, the time lag between airfares and input prices effectively reduces the airlines’ ability to shift the cost increase entirely to passengers when the air travel service is delivered and the jet fuel is consumed [15]. As part of a corporate risk management strategy, hedging generates both benefits and risks to firms [16]. Past studies have examined hedging behavior of U.S. airlines, but the impact of fuel hedging on airlines is empirically an unsettled issue. Sturm [17] found that hedging is positively correlated with the airlines’ value. Rampini et al. [18] found a strong positive correlation between hedging and operating income. However, an earlier study by Rao [19] suggested that the quarterly pre-tax income of an average U.S. airline company in the late 1980s and 1990s would be less unpredictable with hedging. For example, Southwest Airlines is considered to be a relatively “successful” hedger in the airline industry. It recorded impressive net gains of $1.3 billion from fuel derivative contracts’ settlements in 2008 (while other airlines experienced losses), owing to higher and volatile fuel costs. However, Southwest paid out $245 million to derivative counterparties in 2009 [20]. In 2011, the company experienced nearly a 30 percent decline in both its net income and operating income, primarily due to higher fuel costs [20]. Among the less successful hedgers in the industry, Delta, in 2009, incurred $1.4 billion fuel hedge losses from contracts purchased in 2008, when fuel prices unexpectedly dropped after a record high [15]. In summary, by not hedging, airlines may expose themselves to the risk of fuel spot price increases. Conversely, by hedging, airlines may face the risk of falling fuel prices in the near term and incurring financial losses in fuel hedging contracts.

2.2. Application of Hedging in the Construction Industry

- Although the use of derivatives as a risk management is well-documented in the literature [e.g. 21], the weather derivative is the only hedging application currently identified as being used by construction-related companies [22]. Construction companies may use free or paid weather prediction services to monitor the weather, but the accuracy of these services may do little to reduce the financial impact of the weather. By using a weather derivative, construction companies can manage and mitigate the financial risk of extreme rain during construction [22]. The purpose of weather derivatives is to allow companies to insure themselves against any delays or disruptions associated with bad weather. The first such trade was recorded in 1997. According to the Weather Risk Management Association (WRMA), the value of weather derivative trades in 2011 totaled $11.8 billion, a 20% increase from the previous year [23]. There are many ways to trade weather derivatives. Primary market trades are usually conducted Over-The-Counter (OTC), meaning that they are traded directly between the construction companies and banks [24].There are several components that determine the weather derivative [25]. The first element is the source weather station which is used as the reference location for the weather hedge. Second, is the weather index which defines the degree of weather which determines when and how payouts on the contract will happen. Third, is the term over which the underlying index is calculated. The next element is the structure of weather derivative, e.g. puts, calls, and swaps. The final component is the premium, which is an amount of money that is paid by the buyer of a weather option. The premium is normally between 10% and 20% of the amount of the contract [25].

2.3. Previous Work in Construction Materials Hedging

- Macdonald [1] first proposed the use of hedging as a tool for material price risk hedging. She argued that despite the negative reputation of financial hedging, following the 2008 financial crisis, construction companies could use this approach as a strategy to protect against cost escalation. Macdonald [1] then developed a conceptual model to mitigate materials price risks. The first stage of this model is the guidance phase. Here, the construction company identifies its hedging philosophy (i.e., avoiding loss or making profit) and delegates authority to personnel. In the second phase, the construction company identifies which phase of the project life cycle bears the materials risk. The assessment phase subsequently determines the amount, quality, and delivery location of the materials needed. Macdonald [1] refers to the fourth stage as the determination phase. In this phase the construction company determines when and how much to hedge. Further, they need to decide whether to hedge all at once or periodically over the project life cycle. The implementation phase is the fifth stage. In this phase the construction company places orders through a clearing house and monitors their hedge position. In settlement phase the construction company decides if they want to close the hedge, move out of the hedge early, or maintain the hedging position until the end of the hedging period. The final stage of Macdonald’s [1] model is the evaluation phase. Here, the construction company evaluates their hedging process to determine if the hedge was successful or if they need to change their hedging policy and procedures. Macdonald’s conceptual model is very summary in nature, and does not provide any guidance on how hedging could actually be implemented in the construction industry.

3. Methodology

- The term “best practice” refers to a method that has constantly shown results superior to those achieved with other means, and that is used as a benchmark for organizations [26]. Identifying best practices in the area of airline fuel hedging, then applying it in the construction industry, was envisioned as a reasonable approach that could provide a set of detailed guidelines for implementation, and thus save time and eliminate trial and error process improvements. This research conducted a detailed investigation of the process that airlines have conducted for hedging fuel costs, then identified their best practices in this area. Similarly, knowledge on the application of weather hedging in the construction industry was collected via literature search. This research matched construction material hedging with the fuel hedging process, and utilized the weather hedging process as a precedent for determining application to the construction industry. A step-by-step guideline was then developed to apply material hedging and integrate it with Macdonald’s [1] conceptual model.

4. Best Hedging Practices in the Airline Industry

- As cited by Carter et al. [27], according to Southwest Airlines, “the majority of airlines depend on plain vanilla instruments to hedge their fuel costs, including swaps, call options and collars”. Westbrooks [28] supports this statement, and further notes that most airlines use hedging to some extent to limit their fuel risk. This has been done mostly by utilizing swaps, call options, and collar options. Carter et al. [13] conducted a more detailed follow-up study of the airline industry, and note that the call option is the primary hedging tool used by airlines, since it protect them from any fuel price increase. Options were the next choice, since they were viewed as being more flexible than futures, yet allowing the holders to protect themselves against undesired price movements. At the same time, options provide the holder with the chance to participate in favorable movements. In order to better hedge their exposure to fuel price risk, airlines have moved to use a blend of a call and a put option referred to as a collar [13]. The call option protects the holder from price rising higher than its strike price (i.e. the price at which the contract can be exercised). The holder of this call option also writes a put option to limit any possible gain if price decreases below its strike price [13]. The total cost of taking the two options is the difference between the call option premium paid and the put option premium received. This is popular with airlines because it fixes the price for fuel between two identified values.Carter et al. [13] further state that swap is often considered the preferred hedging strategy for the airline industry. The airline would buy a swap for a period of one year at a fixed strike price for a stated amount of jet fuel per month. The average price, for that specified month, is then compared with the strike price. If the average price is greater than the strike price, the counter-party (which is generally a bank) would pay the difference times the amount of fuel to the airline [13]. However, if the average price were lower than the strike price, then the airline would pay the difference. Mercatus [29] conducted a subsequent survey of executives at 24 international airlines. The survey participants indicted that they are currently and/or have previously utilized various hedging instruments and structures. The survey confirmed that the majority of these airlines are utilizing fixed price swaps, call options, and collar options, as their favored hedging instruments. According to Mercatus [29], only 3% of the companies use futures while 39% use swaps. Further, 29% of the companies use call options, 26% utilize collar options, and 3% use forwards. A third relevant study was conducted by Gerner and Ronn [30], which further confirmed the results of both of the previous indicated studies [i.e. 13, 29]. The authors state that most airline companies use call options to provide insurance against sudden upward price shocks. Further, by purchasing a jet fuel swap, airlines can hedge their exposure to jet fuel price fluctuation. If the price of fuel goes up, the gain on the fuel swap offsets the increase in fuel cost [30]. Conversely, if the price of fuel declines, the loss on the fuel swap offsets the decrease in fuel cost. In either case, once the swap is executed, the airline has established their fuel cost [30]. Subsequent studies reaffirm the earlier cited research. Cobbs and Wolf [31] state that “the most frequently used hedging contracts by airlines: swap contracts (including plain vanilla, differential, and basis swaps), call options (including caps), collars (including zero-cost and premium collars)”. Further, Lim and Hong [14] state that futures are used by some airlines, but most airlines today use primarily swaps and call options to hedge their jet fuel price risk.

4.1. Responsibility for the Hedging Decision

- The responsibility for deciding on the type and specifics of the hedging instrument varies based on many factors (e.g. the company size and the company involvement in hedging). Twenty-two percent of the participants in the Mercatus [29] survey stated that the board of directors is responsible for making the hedging decisions. Thirty-nine percent of these companies have a special hedging committee. Eleven percent of the companies made the CEO or the president responsible about making the hedging decisions while 22% of the companies make CFO or VP of finance responsible for those decisions. Six percent of the companies did not reveal who is responsible for making the hedging decision. In order to make the correct hedging decision, the majority of the airlines rely on financial institutions and fuel suppliers, frequently their counter-parties, to provide them with hedging advice, data and information [29]. Sixty-eight percent of the companies that participated in the study rely on financial institutions for hedging advice. These financial institutions include both banks and brokerage firms which have hedging expert personnel. Sixteen percent of the companies rely on information from their fuel supplier. Eleven percent of the companies hire external consultants to provide input toward the hedging decision. Only 5% of the companies rely solely on their internal resources to gather hedging data and information. Jet fuel is usually traded Over-The-Counter (OTC), rather than on any exchange market. OTC trades involve counter-party risk for both sides, and thus small airlines would find it hard to find banks that are willing to take the risk of selling fuel derivatives to them [9]. OTC derivatives are traded directly between the airlines and banks, and most airlines choose to trade with more than one bank to reduce the counter-party risk [30]. In order to trade in OTC securities, the first step is to open a hedging account with the financial institution. The bank will then contact the fuel supplier to identify the selling price of the security. If the airline company accepts the price quoted, the bank will transfer the necessary funds to the fuel supplier account [30].

5. Construction Materials Hedging

- The development of the expanded construction material hedging process is based on the integration of weather hedging process in the construction industry, with the fuel hedging process in the airline industry.

5.1. Weather Hedging Process

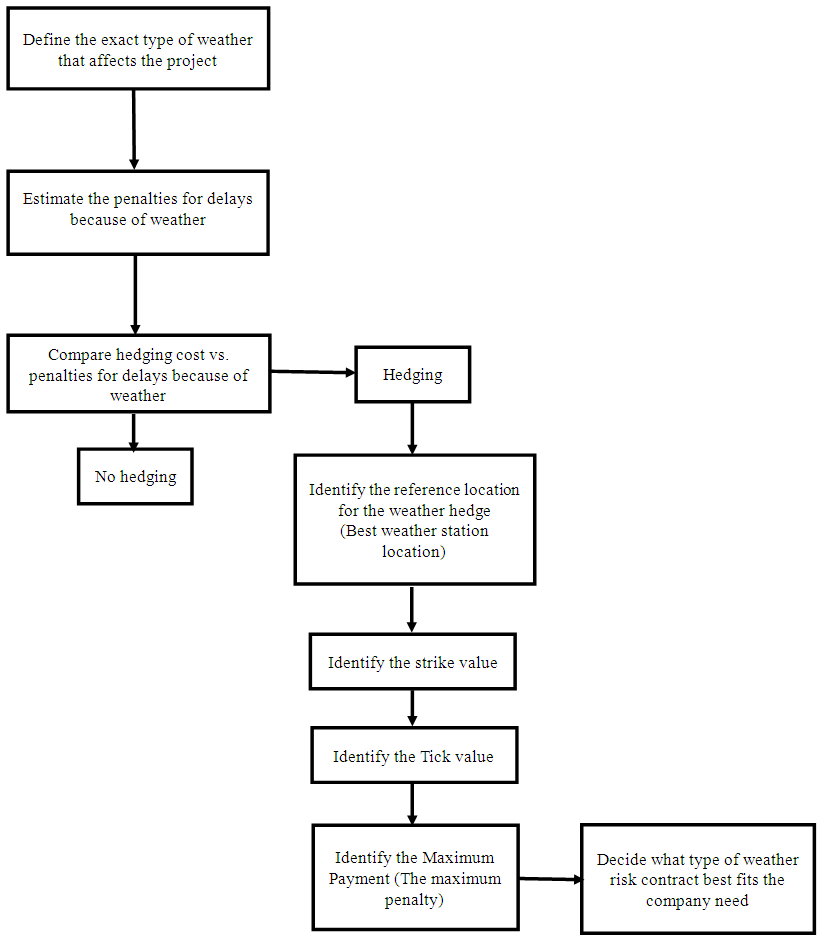

- According to the literature, the first step in the weather hedging process is to identify the type of weather (e.g., rain, wind, or temperature) that affects the project [32]. Once the relevant weather variables have been recognized, weather volatility can be linked to construction delays by obtaining historical data from the nearest National Weather Service location [32]. Based on this data, the contractor can estimate the number of days that need to be added to a project duration to cover the weather impact. This enables the contractor to estimate the penalties for weather-based delays, as well as to quantify the benefits of hedging to mitigate that impact [32]. To establish a reference line for the identified weather risk, construction companies should identify the following points as suggested by Holmes [32]: 1. The point where project delays become intolerable (the strike value);2. The gradual cost increase for each increment of precipitation (the tick value);3. The maximum penalties for delays because of weather (the maximum payment).The weather station locations used in the analysis are used for the hedge locations. The period of coverage is equal to the project period. The weather type was defined in the analysis, as were the strike value (the value at which the contract starts to pay out), tick value (the payout amount for a one increment change beyond the strike value.), and maximum payment levels [32]. Next, construction companies should decide what type of weather risk contract best fits their need (e.g. swap or option). An example of a call option, used as a weather hedge for a construction project, may have the following specifications: 1. Coverage Period: From April 1 to October 31 2. Weather Type: Sum of Daily Rain 3. D Strike Value: 20 inches 4. Tick Value: $50,000 per tenth-inch 5. Maximum Payment: $3,500,000 In this example, the option seller would pay the construction company $50,000 per tenth-inch in excess of 20 inches of rain, up to a maximum payment of $3,500,000. If there were 24 inches, the construction company would receive $2,000,000 from the option seller [32]. Figure 1 depicts the general weather hedging process steps.

| Figure 1. Weather hedging process steps |

5.2. Airline Fuel Hedging Process

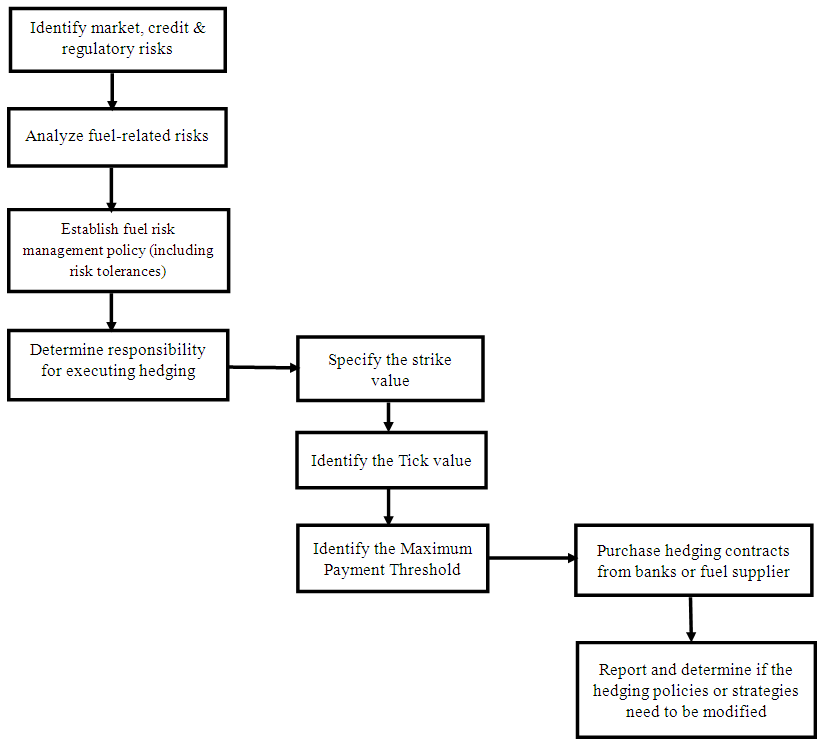

- As an initial step, the airline identifies all energy-related risks including market, credit and regulatory risks that will necessitate fuel hedging. These risks can be investigated using quantitative or qualitative analysis. An energy risk management policy is then established in order to formalize the goals, objectives and risk tolerance, as well as to determine who executes the hedging policy. A hedging committee, board of directors, or Chief Financial Officer are the preferred options for hedging responsibility in the airline industry [29]. The responsible party then determines the strike value, tick value and maximum payout value for the hedge. In this case, the strike value indicates the price of the jet-fuel at which the contract starts to pay out. Similarly, the tick value identifies the payout amount for a specified increment monetary change in a gallon of jet fuel price beyond the strike value. The cumulative payout will not exceed the specified contractual maximum financial payout. Once these steps have been initiated, the actual execution of hedging and trading strategies can commence. Airlines request their financial institutions and fuel suppliers to provide them with hedging advice, data, and information. The airline then purchases hedging contracts that fit their specific need. The preferred types of contract (i.e. options and swaps) are traded directly between the airlines and banks, and as such have counter-party risk that must be taking into account [30]. These contracts are examined to determine if they fit within the company's hedging policy. As the company’s risk exposure changes, the hedging policies may need to be modified. An example of a call option (to protect the airline from any aviation fuel price increase) would be analogous to the weather hedge noted previously. 1. Coverage Period: From Jan 1 to December 30 2. Fuel Type: Jet A3. Strike: $5 per gallon 4. Tick: $1,000,000 per 15 cent increase per gallon 5. Maximum Payment: $6,000,000In this example, the option seller would pay the airline company $1,000,000 per each 15 cents above the $5 per gallon threshold of Jet A fuel, up to a maximum payment of $6,000,000. Figure 2 depicts these steps.

| Figure 2. The airline fuel hedging process |

5.3. Construction Materials Hedging Process

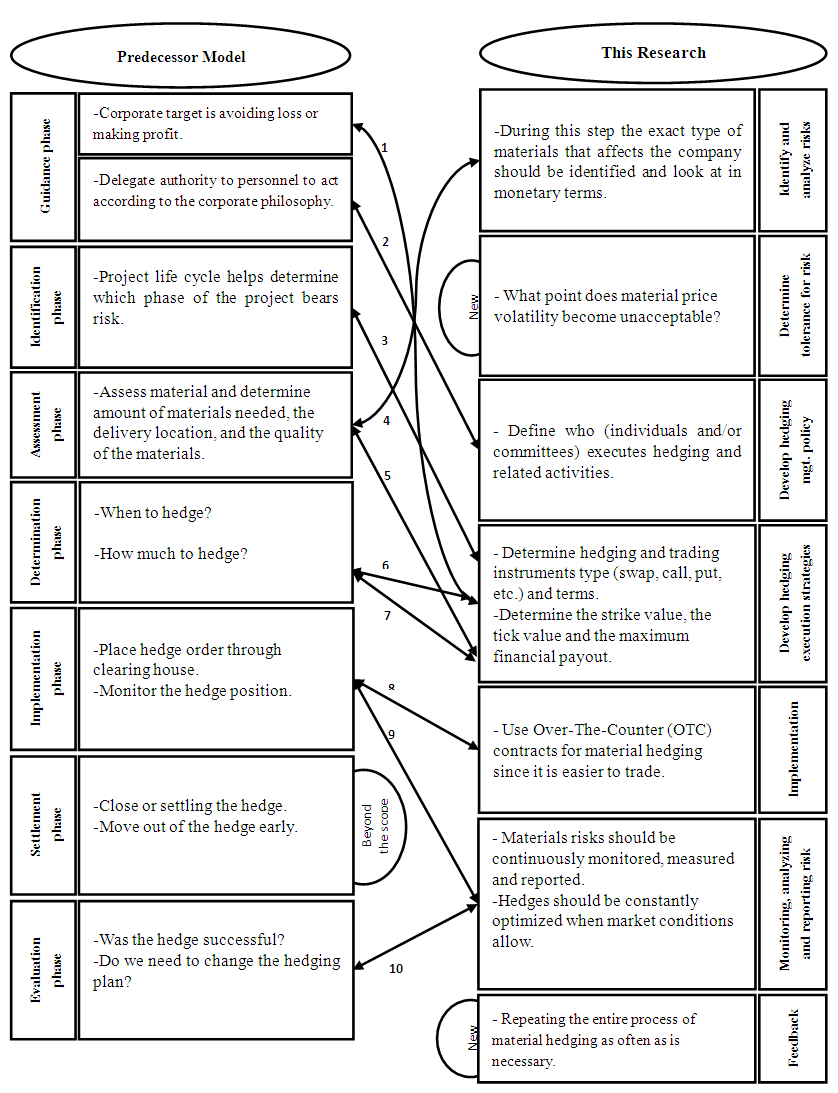

- Utilizing the knowledge collected from weather hedging application in the construction industry and the fuel hedging application in the airline industry, a step-by-step procedure was established in order to apply material price hedging in the construction industry. As depicted in Figure 3, these procedural steps include: identify and analyze risks; determine tolerance for risk; develop hedging management policy; develop hedging execution strategies; implementation, monitoring, analyzing and reporting risk; and repeat the process via feedback loop.

| Figure 3. Relation of predecessor model to this research |

5.4. Integration with Previous Research

- The model developed in this research provides a greater level of detail, intended support actual implementation within the overall context of Macdonald’s [1] summary concept, As noted by arrow 1, in Figure 3, both models note that construction companies should identify the type of hedging instrument (put option, call option, or swaps) that fits their hedging plan. Macdonald’s model infers this indirectly by indicating avoiding loss or making profit as a corporate target. In order to avoid loss, construction companies should utilize the call option, since it protects them from any material price increases. A put option can help construction companies making profit. Construction companies should determine the hedging instrument type as part of the hedging execution strategy development, as noted in this research. Both models stated that construction companies should identify the party that is responsible about making the hedging decision. Macdonald’s [1] model mentioned that authority should be delegated to personnel to apply the company hedging philosophy. Similarly, this research noted that the construction companies should define who executes hedging and related activities as part of the hedging management policy development, and provided specific recommendations. In Figure 3, arrow 3 indicates that the predecessor summary model references the timing of hedging contracts in the identification phase. In this phase, Macdonald (2013) stated that construction companies should determine which phase of the project bears the material risk. This implies that the hedging instrument duration could be only for one phase of the project (short term) or for the duration of the project (long term). Further, arrow 6 shows that Macdonald’s model directly mentioned hedging contract timing again in the determination phase. This research discussed hedging contracts terms identified as part of the company hedging execution strategy development. Arrow 4 reflects that both models noted that construction companies should assess their material requirements. The exact type of materials that affects the company should be identified at this point. Arrow 5 shows that the predecessor summary model mentioned determining the total amount of materials needed as part of the assessment phase. Also, this research mentioned determining the maximum financial payout of the hedging contract as part of the company hedging execution strategy development. Both are related since the construction company needs to understand the total amount of materials needed in order to be able to calculate the maximum financial payout of the hedging contract. Arrow 7 also indicates another shared linkage. The predecessor summary model asked construction companies to determine how much to hedge as part of the determination phase. To know how much to hedge, construction companies should identify the maximum financial payout of the hedge contract which is mentioned in the hedging execution strategies development stage of the model formulated in this research.Arrow 8 shows that both models discussed the implementation phase of construction material hedging. The predecessor model mentioned that the implementation phase starts by placing the hedge order through a clearing house. This research gave further guidance that construction companies should use OTC contracts for material hedging. Arrow 9 shows that predecessor model mentioned monitoring the hedge position as part of the implementation phase. This research notes that material risks should be continuously monitored, and that the model presented a completion phase called monitoring, analyzing, and reporting. Also, arrow 10 indicates that in the predecessor model, the hedge policy should be evaluated to determine if the hedge plan needs to be changed. This research also discussed that hedges should be analyzed and modified when market conditions warrant. Macdonald’s [1] model presented a settlement phase. This aspect was considered beyond the scope of this research, but should be considered for further investigation at a later date. Also, this research presented two steps that were not suggested in the earlier model: risk tolerance determination and the feedback loop.

6. Conclusions

- Construction materials cost estimation is considered one of the most important tasks in the development of project budget. However, material price fluctuation injects an aspect of uncertainty to the cost estimation process. The use of hedging to mitigate the risk of material price volatility is a new concept for construction companies. This research provides a framework to apply construction material hedging by using weather hedging and fuel hedging as precedents. This research provided a detailed investigation of how the airlines have conducted hedging for fuel costs, and identified best practices in the area. The identification of fuel hedging best practices provided the general framework for construction material hedging. Investigation of weather hedging provided insight to best integrate the fuel hedging practice in the construction industry. This resulted in development of a construction material hedging model with step-by-step guidance for its application. The developed model expands and extends predecessor work conducted by Macdonald [1], and provides a greater level of detail in tended to support actual implementation of material hedging within the overall context.

6.1. Further Research

- The next logical step in the development of this construction materials hedging approach is to test the validity of the extended model developed in this research. There are a number of validation techniques suggested in the literature. The first type is face validity which is defined as “the degree to which a test appears to measure what it claims to measure” [33]. It refers to the transparency or significance of a test as they appear to test participants. A limited face validation was accomplished by asking a small sample of construction companies to rate the validity of the model as it appears to them. Initial feedback was positive. More substantive would be a predictive validation [33] via actual implementation. This could be done by taking completed projects, with their original estimates for materials cost and their actual materials cost, then consider if a particular hedge had been applied what would have been the outcome for the contractor. Future work in this area could include investigation of material hedging cost to decide if the hedging application is economically feasible. This is could be added to the tolerance phase of this the model. Similarly, further investigation on the best way to settle the hedging contract is recommended. This could be done by simulating different scenarios of hedging situation. This would generate different settlement options for consideration, such as moving out from the hedge early or keep the hedge contract until its due date.