-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

International Journal of Construction Engineering and Management

p-ISSN: 2326-1080 e-ISSN: 2326-1102

2014; 3(1): 24-41

doi:10.5923/j.ijcem.20140301.03

Identifying and Classifying Effective Factors Affecting Overhead Costs in Constructing Projects in Iran

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLS. Hesami 1, S. Amin Lavasani 2

1Assistant Professor, Department of Civil Engineering, Babol Noshirvani University of Technology, Dr Shariati, Bābol, Iran

2M.SC student in Construction Engineering and Management of Tabari Institute of Higher Education, Babol, Iran

Correspondence to: S. Amin Lavasani , M.SC student in Construction Engineering and Management of Tabari Institute of Higher Education, Babol, Iran.

| Email: |  |

Copyright © 2014 Scientific & Academic Publishing. All Rights Reserved.

Nowadays, construction industry is one of the most important sectors in the competitive markets. The increasing of the competitiveness of the active companies in the field of construction is one of the most important strategic purposes in the construction industry. Construction companies must search continuously for finding ways of reducing their costs and offering high quality services if they want to stay in the competition. Overhead costs, the major sectors of the project costs, is one of the important cost stations which can have better control and management which leads to the increasing of the winning chance in the bids’ companies and have a considerable effect on the financial condition of the company. This paper reviews the key papers published in the time period from 1999 to 2013 and extracted the effective factors on overhead costs of the literature further by sending questionnaire to 49 authoritative contractor companies in Iran and collecting 25 valid responses. This research also provides a list consist of 30 effective factors on overhead costs in construction projects in Iran in four fields: (a) project, (b) client, (c) Government regulations, and (d) environmental factors.

Keywords: Overhead costs, Contractor companies, Competition in project

Cite this paper: S. Hesami , S. Amin Lavasani , Identifying and Classifying Effective Factors Affecting Overhead Costs in Constructing Projects in Iran, International Journal of Construction Engineering and Management , Vol. 3 No. 1, 2014, pp. 24-41. doi: 10.5923/j.ijcem.20140301.03.

Article Outline

1. Introduction and Background

- Nowadays, companies consider different factors for achieving better performance and success on a project. One of these factors is decreasing costs while maintaining or improving quality, because in the current competitive environment, they should be aware of how well they compare with other companies if they want to survive the competition.The construction industry is a very competitive market which is fundamentally controlled by the price (Chan, 2012). The most important factor in the competitiveness of construction companies is the price of bids, especially when it became the main criterion used to select contractors (Plebankiewicz, 2013; Zavadskas, 2008). The first step in reducing costs is to recognize them. Overhead costs, an important part of project costs, is one of the most important cost centers which can provide better controllability and management of price and, consequently, increase the chance of winning a contract and directly affects the company's financial condition (Plebankiewics, 2013).Siskina et al., (2009) also showed that overhead cost is a good starting point for decreasing overall costs. There are many different definitions of overhead costs. According to Tipper (1996), overhead costs are those costs which could not be considered to be attributed with a specific product or service.Cilensek (1991; as cited in Dagostino, 2003) gave one of the most useful definitions of overhead costs for the construction industry: those costs which are not a part of actual costs of construction, but is imposed to the contractor for supporting the project. Overhead costs have also been defined as cases which show the costs of a job and are almost considered as constant costs that must be paid by the contractor.Filicetti (2007) defined overhead costs as costs which are imposed during business but are not directly attributed to a specific product. Therefore, overhead costs are basically independent of project type and product, including general overhead costs. Generaloverhead costs and company overhead costs are those costs which could not be linked to specific jobs, like head office, including staff wages and office rental. Overhead costs of a job or project are those costs which can be associated with a specific subject like, supporting project costs, profit, tax, and … (Adrian, 1982; Assaf et a1., 1999; Holand et al., 1999; Plebankiewicz et a1., 2013; Peurifoy, 2002). Although it is very well understood that the overhead costs are not the major station of costs, it is an important point in winning contract bids. Solomon claimed that contractors must consider overhead costs if they want to catch the margins of competition in one bid. However, overhead costs are very important for cost estimation and lack of accuracy in the estimation causes some companies to lose their competitive edge (Chen et al., 2008; Assaf et al., 1999; and Lew, 1987). Apanaviciene et al., (2011), stated that overhead costs are introduced as a major portion in indirect costs, company costs management, competitiveness of bids price, the improvement of management system operating efficiency and its substructures and gaining success in an open and competitive market. However, company survival is directly associated with a competitive price, winning bids, gaining projects, cash flow, profitability, and, consequently, reaching an optimum overhead costs (Chan et al., 2002). According to Assaf (1999), optimum overhead level is a level which provides the chance of attending strategic purposes of company with minimum cost possible. This point crosses the way of knowing overhead costs and quantifying factors and consequently decreases the possibility of failure in project. The result of Enshassi et al., (2008) also showed that 35% of contractors who studied the overhead costs carefully from bids documents, have won in 20-30 percent of the projects, they took part in the basic purpose. The aim of paper is to identify and classify the effective factors on overhead costs in construction project to control and decrease these types of costs and therefore, it is possible to support contractors in order to increase their competitiveness so they can offer more competitive price in bids.In this present research, the researcher made an attempt to reach these targets:Ø Identification and studying the factors on overhead costs in construction projects.Ø Categorization of identifiable overhead costs in order of priority.As there has not been a general list of overhead costs in any books or research, this article aims to identify and classify these costs generally.

2. Factors which Affect Overhead Costs

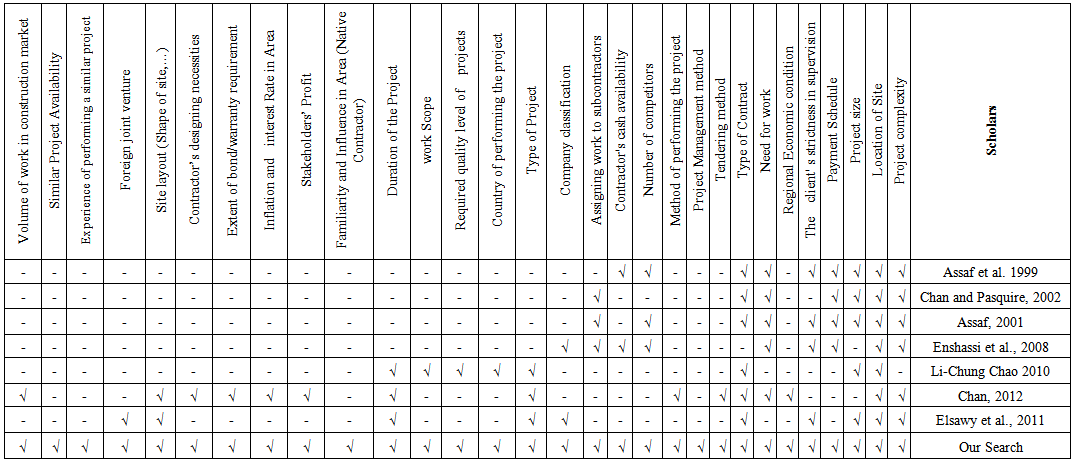

- The author of this document reviewed 13 key articles published between 1999 and 2013, with the goal of extracting a comprehensive list of factors which affect overhead costs. Afterward, the author sent the list, which included 26 factors, to 49 contractor companies in Iran. Management at these companies was; asked to suggest factors which should be add to the list. Nine new factors were suggested by 25 people. Then the author sent a questionnaire which included the nine suggested factors to the original49 companies in Iran, all of whom agreed on four of the nine factors, so those four factors were added to the list of factors which affect overhead costs. Therefore, 30 factors were identified as affecting overhead costs of construction company projects in Iran.

2.1. Methodology for Extracting Factors which Affect Overhead Costs

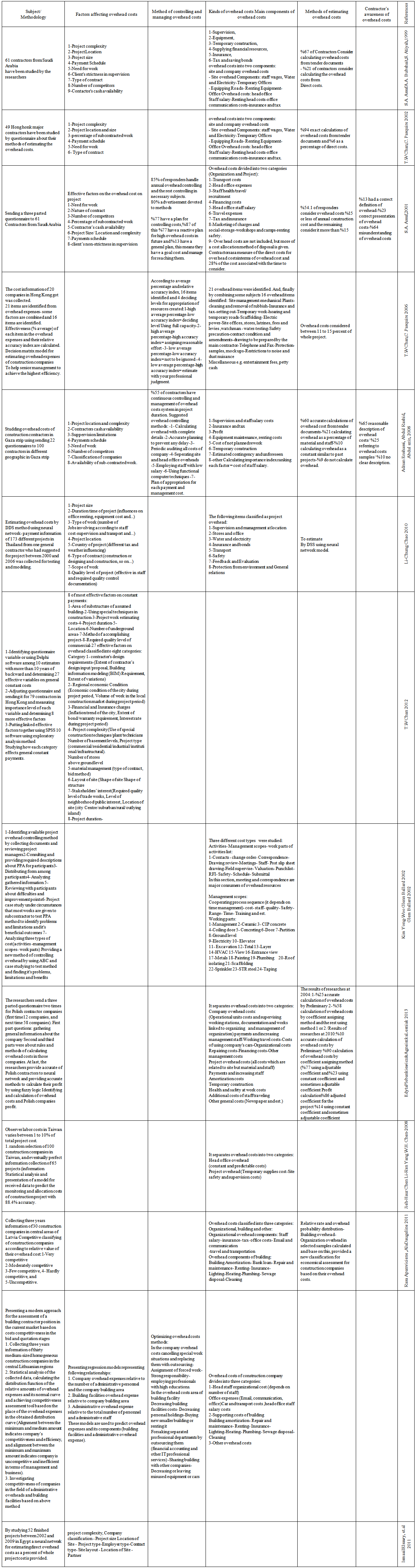

- The author placed the reviewed papers on overhead costs into the following six categories:1. The company perception about overhead costs: In this section, the author examines the companies' levels of awareness, amount of recognition, and ability to correctly define overhead costs.2. The method of estimating overhead costs: In this section, the author explains the companies’ methods of estimating overhead costs in the process of extracting prices in bids.3. The overhead cost: In this section, the author identifies and introduces the main components of the extracted overhead costs in each reviewed study.4. Controlling and management of the overhead costs: In this section, the author introduce the methods of controlling and managing overhead costs that were used in the reviewed studies.5. Factors which affect overhead costs: In this section, the author introduces those factors identified in the reviewed studies as affecting overhead costs.6. Research methods and results: In this section, the author explains the research method that was used and the results obtained in each reviewed study. Table 1 presents the classification of the results of the investigated key articles in this study.

| Table 1. Classification of results of key articles published between 1999 and 2013 about overhead cost |

| Table 2. Identifying factors influencing overhead costs in the present study and studied articles |

3. Explaining the Factors which Affect Overhead Costs

3.1. Project Complexity

- Project complexity is a function of organizational complexity, resources’ complexity, and technical complexity (Maylor, 2008). Regarding lack of quantitative and objective assessment of the project complexity level, different interpretations of the above agent leads to wrong assessment and, finally, increases costs (Chan, 2012). Chan’s (2012) noted that, special techniques and tools in the construction were introduced as an agent linked with the project complexity, especially technical and organizational complexity, since this sensitivity increases the requirement formore professional experts and better support. Akintoy (2000) noted that, the construction and design complexity take first place in impacting overhead costs.

3.2. Project Location

- Choosing the project location can affect some components of the project overhead costs including traveling costs, transportation, access, the amount of importation, security of the public properties, launching and conserving offices, and other temporary facilities (Chan, 2010;Cooke, 1981).In addition, whatever the project location has better conditions in terms of weather conditions, access to the professional experts, the existence of the available ways, and security, controlling and management of the overhead costs are simpler and prevents from the appropriation of additional or more expensive resources. Enshassi et al., (2008) show that the most important effective factor on overhead costs is the complexity and the project location.

3.3. Project Size

- The requirement for resources and staff are increased by increasing the size of the project. Hence, it affects the amount of the overhead costs. In the study of Shash and Abdul-Hadi (1992), the project size is the most important factor in the bids. Besides, Akintoye (2000) states that the size and the complexity of the project affect the organizational structure of the contractor, the cost breakdown structure, and the project period as well.

3.4. Payment Schedule

- Although there are some policies and necessities in the contracts about delays that may influence the in completion of duties such as payments, these cases do not affect the performance of the project but the interaction between the subcontractors and salespersons in meeting the project schedule. Finally, it results in the imposition of additional costs and the increase of the overhead costs.In the research of Enshassi et al., (2008), the payment delay is the fifth effective factor on increasing the overhead costs. They state that many contractors depend on these payments for performing the project faster, and any delay in confirming these payments with the employers make pause in performing the contractors’ work. The results of the research of Memon et al., (2011) showed that the cash flow and the contractors’ financial problems that the contractors are involved in are the most important effective factors on the construction costs.

3.5. The Client’s Strictness and Exactness in Supervision

- In the study of Enshassiet al., (2008), the client’s strictness and exactness in the supervision is the forth effective factor on increasing overhead costs. Where there is an increase in bureaucracy and strictness, an employer’s supervision in obtaining a desired quality and their interaction with the contractor, there will be an affect on overhead costs. Kim et al., (2002) showed that meetings and bureaucracy are the two major activities that consume the most overhead resources.

3.6. Regional Economic Condition

- In bad economic periods, companies have fewer projects and there is a need to decrease overhead costs to improve the chance of survival (Chan, 2012).The economic condition of the region has an impact on staff salaries, the price of services, rental of machines, etc, and consequently it affects the amount of the overhead costs as well.

3.7. Need for the Contractor’s Work

- Maintaining staff and financial earnings are the most fundamental reasons required for the organizational work and the contract work companies. The staff is usually trained by spending the cost for the company and the contract work companies as an economic real-estate are normally desired to keep the experienced staff. However, without the existence of this project, keeping this capital is difficult for the organizations. The amount of need for work in the study of Assafetal., (1999)is introduced as the most important effective factor on indirect overhead costs and in the research of Enshassi et al., (2008) takes the third place.

3.8. Type of Contract

- Standardizing the format of the contract or ratifying it with the inner format based on the employers’ conditions affects the amount of the overhead costs in terms of the possibility of occurring the claims and performing additional commitments (if exists), and the magistrate costs. Whatever the commitments that are out of the contract are few and the contract is termed a win-win contract, the possibility of occurring the claims are decreased, and controlling and management of the overhead costs are improved. The inside form of the contract often has a non-standard necessities and inner organization that leads to the increase of the project overhead costs (Chan, 2012). In addition, the type of the contract in terms of the construction, the design and the construction, and the relation of the under-contracts have an impact on overhead costs as well (Chan, 2010). In the study of Assaf et.al (1999), the contract type, with a little difference from the factor of needing the work, takes the second place in effective factors of indirect costs.

3.9. Tendering Method

- The tendering method like the contract type and the size of the contract necessities affects the amount of the project overhead costs (Chan, 2012). In Iran, there are several methods for choosing the contractors in the tenders, except leaving the tender that the employers are simply allowed to choose the contractors by providing special cases; other methods have an impact on the overhead costs depending on the form, the type, and the location of the tender. Regarding the tenders in that the technical suggestion is inevitable in addition to the requirement for the financial suggestion, spending resources for designing, explaining concept, and side costs are the factors that affect the amount of the overhead costs.

3.10. Project Management Method

- The contract work organizations in Iran are usually managed based on duty, matrix (including weak or strong) or project-directed. The amount of the power of the project manager is different in each of the above methods. The project manager has the least and the most authorities in the duty structure and the project-directed structure, respectively. In the project-directed organizations that make a specific team for each project, the overhead costs are lower than the organizations in that use the organizational staff in the matrix or duty ways.

3.11. Method of Performing the Project

- The method of performing the project shows the main contractor’s ability and commitment (Chan, 2012).The method of performing the project affect overhead costs and must be considered in terms of engineering, providing and supplying goods, construction, financial support, maintenance and exploitation, up to what level, under the commitment of which side of the contract is put, and the project is done in the form of two-sided or three-sided factors.

3.12. Number of Competitors

- In the study of Assaf etal., (1999), the number of competitors takes the third place of effective factors on indirect costs after the needing for the work and the type of the contract. However, in the research of Enshassi et al., (2008), this factor takes the seventh place and has less effect. The number and quality level of the competitors is effective on the amount of the overhead costs because of its effect on the profit level, the contingency reserves, and some other cases due to the requirement for more accuracy.

3.13. Contractor’s Cash Availability

- In the research of Enshassi et al., (2008), the contractor's cash availability takes the second place in effective factors on the overhead costs with a little difference after the project location and the complexity. However, in the study of Assaf, et al., (1999), this factor is at the fifth rank in effective factors. The contractors with good financial conditions do not very much influence by the overhead costs, whereas the contractors with low financial capacities influence more (Enshassi, 2008).The contractor's cash availability with the effect on providing and supplying goods and machines, etcprovides the possibility of economizing and performing the project more economical, and is very effective on the amount of the overhead costs.

3.14. Assigning Work to Subcontractors

- Although assigning the spending work to the subcontractors and the experts saves the organizations from the over spread, it causes some costs including the costs to create coordination and integration between them, suitable support, etc, and puts the amount of the spending work packages among the effective factors on the overhead costs. Eksteen et al., (2002) express that the spending work does not seem to have a considerable effect on the overhead costs. In addition, in the study of Enshassi et al., (2008), this factor is identified to be the lowest rank of the list of effective factors.

3.15. Companies’ Classification

- In Iran, the contract work companies are classified to 5 grades from 1 to 5 in view of their relative work class, and after passing levels including the amount of yearly projects, etc. They promote and reach at the grade 1 in the relative category (construction, road, installations …). It is obvious that the companies with higher grades need more work space, machines and repository as well as better and more expert staff; hence, they have more overhead costs. In the study of Enshassi et al., (2008), this factor is identified after the factor of assigning the work to the subcontractors in preceding the last grade of effective factors of the list in the study. The classification of the companies in the study of Elsawy et al., (2011) is identified as the tenth effective factor on overhead costs in Egypt.

3.16. Type of Project

- The type of project like road, dam, construction and, etch as an impact on the number of involved jobs, coordinating the supervision and the transportation, and also affects overhead costs (Chan, 2010). In other words, considering sullying and requirements hazards based on the type of the project including road, dam, tunnel, construction, the amount of the required resources, the overhead costs may be different, regardless of its simplicity or complexity. Elsawy et al., (2011) examined 52 construction projects in Egypt since 2002-2009 and showed that type of the project is the third effective factor on the direct overhead costs.

3.17. Country of Performing the Project

- The country in which the project is performed affects the amount of the overhead costs in aspect of culture, governmental laws, taxes, safety of war, sanction by other countries, etc. For example, in some countries, different taxes are belonged to the construction projects by different employers. As a result, the overhead costs are increased (Shen et al., 2001). According to Chao (2010), the country of performing the project has importance on the amount of the overhead costs in terms of weather, culture, and laws.

3.18. Required Quality Level of the Projects

- Although the required quality level of projects is sometimes determined by the type of work for example, a fast transportation project tends to have higher quality than the normal road projects; this considerably affects the staff and the required documentations for the quality control and consequently affects the overhead costs (Chao, 2010). In other words, access to better quality depends on existing better tools and resources, and suitable management that have an impact on the overhead costs. Since reaching at the optimum level of the overhead directly faces the quality of services with challenges, it is a complex and difficult issue for the organizations.

3.19. Work Scope

- Work scope affects number of middles, communication necessities, distribution of resources, and engineering costs and as a result it affects the overhead costs (Choa, 2010). In addition, the work scope decreases the performance of the additional activities that are ineffective on the achievement of the projectvia better and more correct identification of the employers’ requirements and better understanding of the work limit. Consequently, it is effective on the decrease of the overhead costs.

3.20. Duration of the Project

- Most of the researches emphasize on the project duration as an important factor that affects the overhead costs and the parts related to the duration include more than 45% of the overhead costs of the project. In addition, the high potential risk of the project delay increases the importance of this factor to affect overhead costs (Chan, 2012).Although increasing the contract duration enhances the overhead costs, the contractors are not allowed for the restoration of their overhead costs in the delay period in most of the standard contract forms (Chan, 2012). Elsway et al., (2011) show that the project duration is the most important effective factors on overhead costs.

3.21. Familiarity with and Influence in Area (Native contractor)

- Better familiarity with the area is effective on supplying and providing materials and goods, using professional staff, and simpler and less expensive solution of the created crises as well as affects the overhead costs. This issue has lately been given special attention in Iran and is considered as a particular privilege for the native contractors to balance the suggested prices in the bids. In addition to the mentioned cases, the native contractors can perform more economical in traveling costs, residing, staff salary, and telecommunications, etc, and have higher chance to win the bids.

3.22. Stakeholders’ Profits

- Maintaining the stakeholders’ profits is a wide spread factor. In fact, maintaining public profits and observing neighbors’ rights, solving and gaining basic information, and cooperating with the deciders’ organs in the urban management (water and sewage office, and gas office) are among the most fundamental cases that are effective on the amount of the overhead costs and must be considered. Chan (2012) believes that if a project causes to riot even the claims are successful, the contractor must bear the project overhead costs due to the extension or stop working.

3.23. Inflation and Interestrate in the Area

- In Warsame’s research (2006), inflation and interest rate are the most important factors affecting the construction cost. There is no doubt that increasing the inflation causes an intense fluctuation in the insurance right because of the increase of the financial claims of the insurance companies. Besides, changes in the interest rate leads to the high insurance right and the above cases put on a heavy responsibility for the contractors about the project overhead costs (Chan, 2012).In the study of Enshassi et al., (2008), the inflation is the most important reason for increasing the overhead costs.

3.24. Extent of Bond and Warranty Requirement

- In Iran, the extent of bond is usually started from 6 months and may be increased in the consideration of the project type and conditions. Taking into consideration the conditions of the resources’ amount, the extent of bond and the warranty requirement are effective on increasing overhead cost. According to the study of Chan et al., (2006), the insurance and the warranty form nearly 10% of the overhead costs, and this issue turns into a main concern for the contractors in the case of increasing the insurance right and the warranty amount.

3.25. Contractor’s Designing Necessities

- The requirement for using special software, further experiments or the requirement of making a model for explaining the primary design, and such instances are the most fundamental constituents of this part that are effective on the amount of the overhead costs. If the project design is complex or unknown and has many variables, the contractor will need more staff to coordinate the design and provide the plans; failure in performing this work can simply lead to delay or performing inconclusive works and additional uncoverable costs (Chan, 2012).

3.26. Site Layout (Infrastructure, Site shape, Site coverage, Etc …)

- Infrastructure, shape, site coverage, possibility of providing suitable support for the project, materials and storage limitation, and such instances affect overhead costs. For example, the level of the infrastructure is directly linked with the bulk of work, the amount of the required resources, and the amount of the overhead costs. In addition, whatever the level of the infrastructure is wider and the area of site is fewer, storing the construction materials and other construction facilities are difficult. There are solutions to solve the above problem including delivering the materials at the consuming time or renting the storage near the site that lead to the increase of the overhead costs (Chan, 2012).

3.27. Foreign Joint Venture

- In view of the fact that the cost of engineering services in Iran is very lower than the European countries or even the Asian countries and neighbors, the presence of the foreign joint ventures with increasing the transportation cost, the residence cost, and the staff salary cause to increase the amount of the overhead costs. In recent years, this issue has become more important with intense sanctions and decreasing the Rial value in Iran.

3.28. Experience of Performing a Similar Project

- The experience of performing a similar project decreases the amount of trial and error and makes it possible for the project team to provide a more accurate explanation of the project framework. As a result it has an impact on decreasing overhead costs. The contractor’s experience helps them achieve a high quality of work standard and the overall project success (Memon, 2011). In addition, Akintoye et al., (2000) show that the main reason for incorrect estimation is due to the lack of knowledge and practical experience of the construction process. Lack of experience to perform a project and lack of technical knowledge leads to delay and increases the costs (Kaming et al., 2010).

3.29. Similar Project Availability

- Although similar projects availability causes limitations in resource appropriation, recognizing supplies, optimum accomplishing method, the amount of required resources and finally better management leading to economizing in overhead resources and makes suggesting competitive price possible.

3.30. The Volume of Work in the Construction Market

- It is sometimes difficult to obtain project resources and reduce costs in a thriving market, and vice versa, so the market capacity and project size also influence overhead costs. When there is a downturn of business and when companies have fewer projects, they may have no option but to adjust overhead costs (Chan, 2012).

4. Classification of Effective Factors on Overhead Costs

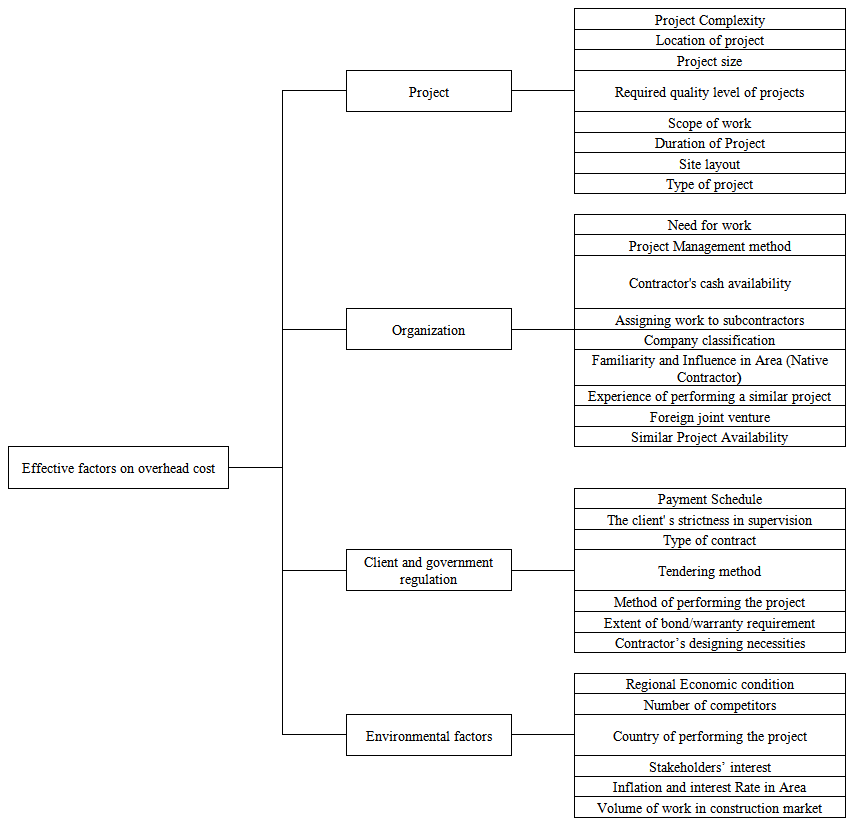

- This section includes how to classify thirty factors on overhead costs and the introduction of the structure of the suggested hierarchy processes. As seen in Figure 1, the first level is the structure of the hierarchy processes of factors on overhead costs. The second level includes the project criterion, organization, employers, governmental laws, and environmental factors; this structure was formed after interviews with experts. Each of the second level criterions includes several sub-criteria; the second level and its criterion are explained as follows:

| Figure 1. Distributed framework of effective factors on overhead costs |

4.1. Project

- This standard emphasizes that some of the key factors in overhead cost management requires knowledge and attention to the complexity, location, size, quality, scope, duration, and type and project site design.

4.2. Organization

- The criteria and sub-criteria of organization contains “contractor’s needed job, project management method, contractor’s cash availability, percent sub-contracted work, company grade, familiarity and influence in area, similar projects availability, foreign partner and the experience of accomplishing similar availability” reflects the impact of organ size on overhead costs.

4.3. Client and Government Regulations

- Third standard of second level of the hierarchy model are the regulations of the client’s profession and of the government. It includes the subjects below:ü Payment scheduleü Client’s strictness in supervisionü Type of contractü Tendering methodü Extent of bond/ warranty requirementü Contractor’s design requirements

4.4. Environmental Factors

- The last standard of second level introduced by client’s experts is environmental factors which includes six factors on overhead costs identified in previous levels. These factors included economical condition of area, the number of competitors, the country of project, stakeholder’s profits, inflation and the amount of work at market.

5. Conclusions

- The overhead costs must be considered as one of the fundamental elements in the management of the company’s costs, competitive tendering price, improving the operational product of the management system in the company. With knowledge and controlling the overhead costs, the contract work companies are able to achieve an optimum level of the overhead, and making a balance between quality and cost to compete better, decrease risk, and survive the market. One of the most important steps in controlling these costs is recognizing and assessing factors on overhead costs. Therefore, this study is concentrated on the two stages of this process that are recognition and the classification of factors on overhead costs. The literature of the overhead costs in the construction projects collects various and factors in different countries in which are effective on overhead costs. These factors play an important role in increasing the contractors’ understanding, and increasing their competitiveness in the suggested price process. Lack of a comprehensive list of such factors on overhead costs was obvious. The present study is a fundamental step in this area. In addition, other related articles were reviewed and studied. The results of factors on extracted overhead costs from questionnaire included thirty factors that were collected into four groups. Unlike other articles, the present study continually used a combination of the literature study and the experts’ judgments in this area are to extract factors on overhead costs, and presented a comprehensive framework. The results of this framework can help the contractors increase the competitiveness and better control over the overhead costs.