E. C. Merem1, Y. A. Twumasi2, J. Wesley1, D. Olagbegi1, M. Crisler1, C. Romorno1, M. Alsarari1, P. Isokpehi1, A. Hines3, G. S. Ochai4, E. Nwagboso5, S. Fageir6, S. Leggett7

1Department of Urban and Regional Planning, Jackson State University, 101 Capitol Center, Jackson, MS, USA

2Department of Urban Forestry and Natural Resources, Southern University, Baton Rouge, LA, USA

3Department of Public Policy and Administration, Jackson State University, 101 Capitol Center, Jackson, MS, USA

4African Development Bank, AfDB, 101 BP 1387 Avenue Joseph Anoma, Abidjan, AB 1, Ivory Coast

5Department of Political Science, Jackson State University, 1400 John R. Lynch Street, Jackson, MS, USA

6Department of Criminal Justice and Sociology, Jackson State University, 1400 John R. Lynch Street, Jackson, MS, USA

7Department of Behavioral and Environmental Health, Jackson State University, 350 Woodrow Wilson, Jackson, MS, USA

Correspondence to: E. C. Merem, Department of Urban and Regional Planning, Jackson State University, 101 Capitol Center, Jackson, MS, USA.

| Email: |  |

Copyright © 2020 The Author(s). Published by Scientific & Academic Publishing.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Abstract

In the last several decades, many nations of the sub Saharan Africa region of West Africa, have remained in the forefront of cocoa production far higher than other areas of the globe. With that has come larger export earnings due to rising demands and the reliance on cocoa in the manufacture of various products driving consumer demands in markets at local, regional and international levels. In as much as current cocoa production practices are shaped partly by pressures from transactions in the marketplace and regulatory frameworks in the West African region and beyond. The growing activities of cocoa farming has in the past several years, left in its wake negative environmental liabilities that are now over stretching the capacity of natural areas in the zone. While there exists widespread use of agrochemicals to boost production along with the associated impacts of water pollution, in some places. The situation is now so critical that the expansion of cocoa plantations into vast forest landscapes known for their services as emission sinks, are now leading to ecosystem disturbances. Other risks from cocoa land use activities in West Africa involves the exposures to soil erosion, the flow of sediment loads onto local streams and the spreading of cocoa plant diseases which has emerged as a major issue to the detriment of communities and the surrounding ecology. Even at that, very little has been done in the literature to assess the environmental impacts of cocoa land use. Considering the economic relevance of cocoa produce in the West African region and the prevailing fiscal, policy, demographic, ecological and global factors shaping production, together with the negation in mainstream analysis. This paper will fill that void by analyzing cocoa land use in selected countries in the study area. Emphasis are on the issues, trends, factors, impacts and the role of institutions. In terms of methods, the paper uses secondary data analyzed with mix scale tools of GIS and descriptive statistics. Besides the preliminary results showing rising changes in land use indicators and degradation of the ecosystem from cocoa farming operations, the GIS mapping reveals the gradual spreading of risks along the cocoa producing areas of the West African region due to several socio-economic and environmental factors located within the larger farming structure. To mitigate the problems, the study proffered solutions ranging from education, ecosystem monitoring, conservation initiatives, the strengthening of policy and the design of a comprehensive regional land use index.

Keywords:

Cocoa farming, Land use change, Environmental degradation, GIS, West Africa, Impacts, and factors

Cite this paper: E. C. Merem, Y. A. Twumasi, J. Wesley, D. Olagbegi, M. Crisler, C. Romorno, M. Alsarari, P. Isokpehi, A. Hines, G. S. Ochai, E. Nwagboso, S. Fageir, S. Leggett, Exploring Cocoa Farm Land Use in the West African Region, International Journal of Agriculture and Forestry, Vol. 10 No. 1, 2020, pp. 19-39. doi: 10.5923/j.ijaf.20201001.03.

1. Introduction

In the last several years, cocoa output rose to significant levels in the producer nations around the world. Beginning in 1960, world cocoa production has surged notably between 1.2 to 3.6 million tonnes. This increment occurred amidst many shocks triggered by fiscal restructuring programs, proliferation of crop infestations, plant viruses and price market manipulation, much of which have impacted yield. The key producers in the equator where cocoa beans are grown with dominance of global output consists of West African nations of Ivory coast (39%) and Ghana (21%) [1,2]. West Africa being a prominent production area stretches from Guinea to Cameroun where most cocoa plants thrive [3]. The other marginal producing nations in the continent of Africa with lesser profile and output are concentrated throughout the Sub-Saharan region. All in all, the cocoa marketplace transactions are categorized particularly by substantial presence of production activities flourishing in areas where yearly global output hinges on variabilities and attributes of the West African climate [4]. In the process, over the past many decades, many West African nations, have remained in the forefront of cocoa production far higher than other areas of the globe with the growth of 2-3 million tons since the 2000s [5]. With Europe and the US, the two prime markets accounting for 40% to 20% of global consumption individually [6]. Cocoa farming therefore epitomizes the center of key economic activities in several areas of West Africa, engaging millions of small-scale farmers. Still, they encounter challenges of falling output, degraded land and old pest-infected cocoa trees. In all these, global cocoa production now faces mounting environmental and economic challenges [7]. Considering all that, despite the surge in world demand, cocoa exporters face multiplicity of issues stemming from rising output on inadequate landbase, ways of minimizing the threats to forests and the environment, and the growing response to climatic variability [7]. Because the surge in cocoa farming came with its own portion of downsides including the exploitation of child labor involving over 2.2 million children in most cocoa plantations, and the incidence of deforestation [8,9,10,11]. From 1988 and 2007, West Africa lost 2.3 million hectares of its forests to cocoa tilling [12]. In all these, cocoa farming has been a major driver of deforestation in West Africa, particularly in Ivory coast, the globe’s chief cocoa producer. In that nation, cocoa as major produce often planted in the aftermath of forest cutting, left a dismal legacy of limited or no engagement in the restoration of mature farmsteads, in which greedy farmers typically drifted towards the forest borderlines to begin new cocoa plantations [13]. From that, in the middle of the 1900s, the cocoa borderline shifted from the arid eastern zone to the moist southwest portion of the nation, prompted by huge migration of potential cocoa growers from the grassland [14]. This has triggered grave soil degradation, flooding, erosion and crop declines and hydrological stress. These elements threaten the livelihoods and capacity to embrace novel forest-smart practices and sustainable farming. Based on the appraised annual full market worth of the cocoa sector of US $100 billion dollars [15], just around $6 billion dollars accrues to the 5 million growers who cultivate cocoa plants and those harvesting the beans in the West African region [16]. This level of socio-economic inequity together with the perceived ecological consequences of cocoa harvests in the producing nations of West Africa indicates that most consumption habits elsewhere usually leave in their wake grave problems which can no longer be ignored [17,18,19,20,21]. Even at that, very little has been done in the literature to assess the environmental impacts of cocoa land use [22]. Considering the economic relevance of cocoa produce in the West African region [23] and the prevailing fiscal, policy, demographic, ecological and global factors shaping production, and the little consideration in mainstream literature, this paper will fill that void by analyzing cocoa land use trends and the environmental impacts in selected countries in the study area of West Africa. Emphasis are on the issues, trends, factors, impacts and the role of institutions. In terms of methods, the paper uses secondary data analyzed by mix scale tools of GIS and descriptive statistics [24,25,26,27,28,29]. The paper has five objectives. The initial aim consists of the use of geo-spatial tech to analyze status of cocoa land use and changes, while the second objective is to provide a support tool for policy makers. The third goal stresses the design of a new approach for standardizing land use index. The fourth objective is to design a framework for regional agro-environmental impact analysis with mix scale techniques. The fifth objective is to appraise cocoa farmland trends. In terms of organization, the paper is divided into five sections. The first part covers the introduction, while the second part highlights the methods and materials. Section three presents the results of data analysis made up of descriptive statistics, spatial analysis of GIS mapping, impacts, factors and efforts. Section four deals with discussions while section five presents the conclusions and recommendation.

2. Methods and Materials

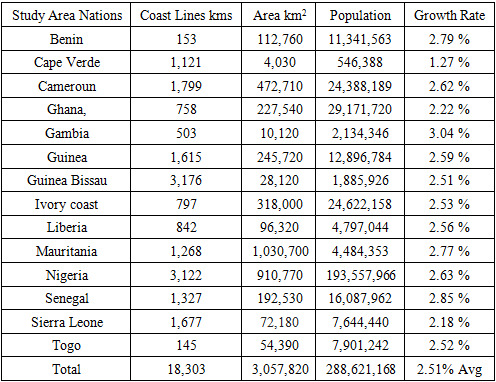

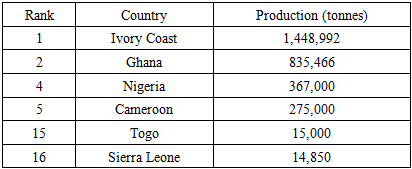

The study area West Africa in Figure 1 as a major cocoa hub in the equator stretches through 15 nations across diverse ecosystems. With a population of more than 288 million in 2016 (Table 1), the greater region has 1/3 of sub-Saharan Africa’s population on a land area of 5,112,903 km2 [30]. Seeing the increasing pace of cocoa farm operations as evidenced in the continent of Asia and Central and South America. Sizable proportion of the globe’s cocoa stock emanates from the neighbouring nations of Ivory Coast and Ghana alone, in the study area. Essentially, most of the cocoa output comes from the two West African nations. Collectively, the two countries produce over 60 percent of the world’s annual requirements of the beans [31,15]. Certainly, cocoa thrives exclusively mostly along equatorial environments upon which the crop in the region depends on for elevated temperatures and rainwater to flourish, alongside rainforest vegetation to usher cover and shield from intense sunlight and destruction triggered by storms. In the actual global ranking of the 20 major cocoa producing nations, the West African region occupied the top 5 spots as well as the 15th and 16th positions. The countries of Ivory Coast and Ghana emerged as the first two with 1,448,992 to 835,466 tonnes while Nigeria and Cameroun finished at number 4 and 5 with 367,000-275,000 tonnes in cocoa output. Behind them are the nations of Togo and Sierra Leone in the 15th and 16 spots, responsible for 15,000 to 14,850 tonnes in world production [32] as indicated in Table 1.1. | Figure 1. The Study Area, West Africa |

Table 1. The Population and Size of the Study Area

|

| |

|

Table 1.1. Top Cocoa Producing Countries In The World

|

| |

|

Since cocoa farm produce are sensitive to climatic variability, they are harvested in quite a few nations like those in the study area located around 20 degrees north and south of the equator [33,34,3]. The crop stands as the key component in chocolate products consumed throughout the globe [35]. Thus, being in the tropics where cocoa is grown and harvested, West Africa accounts for more than 70% of world cocoa production [36,37]. As such, cocoa farming has, therefore, become a major economic activity in many parts of West Africa, employing millions of small-scale farmers [33]. From the scale of production activities in the cocoa industry, it is worthy to note that the crop is also produced in Togo, Sierra Leone and Liberia in much smaller quantities. Given the pressures involved in meeting the rising demands among the consumer nations [38]. The West African region now faces far reaching environmental and socio-economic challenges that are detrimental to the local ecosystems and the citizens [39]. In that way, cocoa growing communities, especially in the study area are burdened by the threats of poverty [40], the issue of child labor in the industry [41] and deforestation which is often compounded by the decreases in cocoa prices in the international marketplace [15,42]. Even the broadly publicized initiatives in the sector to advance the welfare of planters, the other vulnerable groups affected and the ecosystem in the last ten years have done little to reverse the situation. Seeing the inaction, these concerns are now receiving the attention of various groups connected to the issues including the chocolate industry, human rights groups, and the authorities in West Africa and policy makers in Europe and the advocates of fair trade [43]. With the picking of cocoa beans from farms much more dominant in West Africa, the actual making of chocolate items are centered in Western Europe [43]. Besides that, the two largest markets are Europe and the US, accounting for 40-20% of global consumption respectively. In 2014 when the EU and US imported 2.3 to 0.7 million tonnes of cocoa estimated at $7.4 to $2.6 billion, cocoa operations in Ivory Coast and Ghana left the biggest land-use footprint of every crop output therein at a rate of 25%. Consequently, the expansion of cocoa farming is also driving deforestation in the zone.

2.1. Method Used

The research adopts a mix scale method comprising of descriptive statistics and secondary data connected to GIS to assess the environmental impacts of cocoa land use activities among the producing countries in the West African region along the Sub Saharan Africa zone. The spatial information for the study was obtained through numerous organizations consisting of NASA, the USGS, World Bank group, the Economic Community of West African States (ECOWAS) and the organization for Economic Cooperation and Development (OECD), the Hershey Company and Candy Industry and Alliance of Cocoa Producing Nations. Additional sources of geo-spatial information originated from the United States Agency for International Development (USAID), the United Nations Food and Agricultural Organization (FAO), the International centre for tropical agriculture, and the International Cocoa organization (ICCO). In addition to that, the United States Department of Agriculture (USDA), World Agroforestry Centre, The African Development Bank (ADB), also offered other information required in the research. Generally, most raw cocoa land use indicators germane to the region and separate countries were acquired from the Nigerian Bureau of Statistics, FAO’s FAOSTAT, The European Cocoa Association, the International Cocoa organization (ICCO), The national archives from Ivory Coast to Nigeria, The Federal ministry of agriculture and rural development and the USDA Economic Research Service provided info for some of the periods. At the same time, crucial insights on the relevant data also came from the Cocoa Research Institute of Ghana, the Ecole Nationale de Statistique et d’Economie Appliquée (ENSEA) in Ivory Coast and the Institute of Statistical, Social and Economic Research (ISSER) in Ghana.On the one hand, the USDA, the World Bank, FAO Statistics Data Base, USDA Foreign Agricultural Service (FAS), The Economic Commission for West African States (ECOWAS) and the US Congress provided the secondary data on the total production, quantity and export and the exposure of minors to child labour on cocoa farms. On the other, the Government of Nigeria, the United Nations Food and Agricultural Organization (FAO) offered the time series data and the monetary data on exports of cocoa crops stressing the trends in the region. For additional data needs, The International Fund for Agricultural Development (IFAD) and World Food Program (WFP) Climate Focus, Program on Forests were respectively critical in the procurement of information on the ecological risks of climate change and deforestation and econometric data indicating shortfalls and the variations. In a similar vein, the Ghana Cocoa Board, CRS Report for Congress, International Trade Commission Trade Data, Conseil du Café-Cacao or CCC, in Côte d’Ivôire, the Chatham House, University of Maryland Global Land Analysis and Discovery (GLAD) Lab, Gro-Intelligence, National Bureau of Technical Studies (BNETD), and NASA Landsat data, remained instrumental in the provision of other relevant information pertaining to spatial mapping and econometric information. The other key sources encompasses the United Nations Educational and Cultural Foundation (UNICEF), the International Cocoa Initiative, CILSS, IFC, Hershey company, Kraft Foods, Barry Callebaut, Blommer Chocolate, Cargill, ADM, ECOM, and Armagaro Trading, Tulane University, Tulane University School of Public Health and Tropical Medicine, National Bureau of Technical Studies (BNETD and the Prince of Wales’s International Sustainability Unit. Given that the regional and federal geographic identifier codes of the nations were used to geo-code the info contained in the data sets. This information was processed and analyzed with basic descriptive statistics, and GIS with attention paid to the temporal-spatial trends at the national, state and regional levels in the coastal West African region. The relevant procedures consist of two stages listed below.

2.2. Stage 1: Identification of Variables, Data Gathering and Study Design

The initial step in this research involved the identification of variables required to analyze the extent of harvest or production and changes at the national level from 1984 to 2018. The variables consist of socio-economic and environmental information of production volume of cocoa beans, ranking of top cocoa producing nations, production or output of the top producers, deforestation levels, land areas affected by deforestation, cocoa pest disease, distribution and size of cocoa pest diseases and the percentage of land areas devoted to cocoa farming, or as a percent of country total in harvested area. The others consist of area harvested, cocoa production volume and land size, cocoa production totals and change, percent share of world production, cocoa derived export earnings as percentage of total exports by value and the producer prices in local currency per kg. Notable among the variables are the cocoa production and areas under cultivation in the major producing nations, cocoa production average, estimated number of cocoa farmers, estimated areas under cocoa, cocoa bean production, projections in cocoa production, national populations and percentages of population change, the cocoa child labour population total and the cocoa child labour distribution among the countries. These variables as mentioned earlier were derived from secondary sources made up of government documents, newsletters and other documents from NGOs. This process was followed by the design of data matrices for socio-economic and land use (environmental) variables covering the census periods from 1984, 1990, 2000, 2002 to 2007, 2010 to 2018. The design of spatial data for the GIS analysis required the delineation of county, national and regional boundary lines within the study area as well. Given that the official boundary lines between the 10 nations remained the same, a common geographic identifier code was assigned to each of the area units for analytical coherency.

2.3. Stage 2: Data Analysis and GIS Mapping

In the second stage, descriptive statistics and spatial analysis were employed to transform the original socio-economic and ecological data into relative measures (percentages, ratios and rates). This process generated the parameters for establishing, the extent of cocoa farm land use, deforested land areas, and production and areas cultivated and those undergoing changes in harvests and their volumes, number of under aged children used in child labour by the industry and the situation throughout the region among each of the 10 nations using measurement and comparisons across time. While the spatial units of analysis consist of countries, region and the boundary and locations where cocoa harvests, export and cultivation operations and the percentage and size of child labour flourished. This approach allows the detection of change, while the tables highlight the actual frequency and averages, impacts, share of the population in child labour victims, and regional distribution of the number of minors by country, the concentration of activities and the trends as well as the price of cocoa exports in local currencies. The remaining steps involve spatial analysis and output (maps-tables-text) covering the study period, using Arc GIS 10.4 and SPSS 10.4. With spatial units of analysis covered in 10 nations (Figure 1), the study area map indicates boundary limits of the units and their geographic locations. The outputs for each country were not only mapped and compared across time, but the geographic data for the units which covered boundaries, also includes ecological data of land cover files and paper and digital maps from early 1975-2017. This process helped show the spatial evolution of location of various activities and the trends, the ensuing environmental and economic effects, ecological degradation as well as changes in other variables and factors fuelling the incidence of cocoa farmland use changes and impacts in the study area.

3. The Results

This section of the paper focuses on temporal and spatial analysis of cocoa land use trends in the study area. There is an initial focus on the analysis of harvested areas, cocoa beans production. Additional segments highlight production and cultivated areas, output totals and change using descriptive statistics. Consistent with the section are the emphasis on GIS mappings, impact assessment, the identification of the factors driving variations in land use in West Africa and the present initiatives. For more on the abbreviated info on the tables see the acronyms.

3.1. Size of Cocoa Harvested Areas

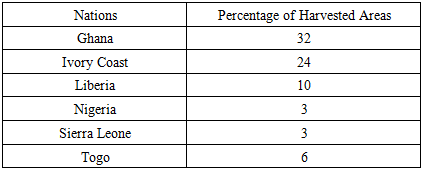

The distribution of harvested cocoa areas per nation as percentage of total agricultural land harvest based on the 2010-2013 average in the West African region, puts Ivory coast and Ghana ahead of the others with 32 to 24% of the crop accounting for the total in the respective countries. In the neighboring nations of Liberia and Togo, cocoa produce covered 10 to 6% of harvested farmland area compared to Nigeria and Sierra Leone where just only 3% cocoa areas represent total harvested agricultural land (Table 2). Based on the data, this comes at an average percentage rate of 13 points all through the fiscal years with the bulk of the region’s cocoa harvested areas concentrated in a trio of nations made up of Ivory coast, Ghana as well as Liberia with the remaining group of countries most notably Togo, Sierra Leone and Nigeria (Table 2).Table 2. Harvested Cocoa Areas Per Country in West Africa (as a % of Country Total Harvested Area, Based on 2010–2013 Average)

|

| |

|

3.1.1. Cocoa Beans Production 1984-2014

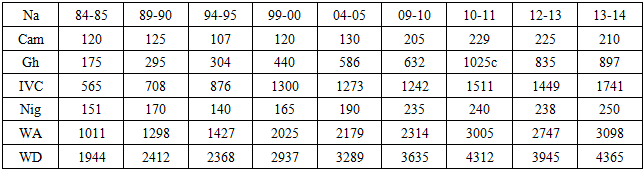

From the info on the table, the profile of the overall trends in the study area indicates that cocoa beans production did rise in each of the countries listed from Cameroun to Nigeria all through the 20 year span from 1984 through 2014, aside from insignificant fluctuations which did not override the soaring output. Of great significance during that period is the dominance of Ivory Coast, Ghana and Nigeria and Cameroun. Even at that, West Africa’s cocoa beans total output opened at 1,011 tonnes in 1984 to 1985, only to jump to 3,098 thousand tons in 2013 to 2014, representing 52 to 71% of the world totals. In terms of cocoa beans production in the West African region in 1984 to 2014 and the world, Ivory coast and Ghana not only held the top spots as the leading producers over the years, but cocoa beans output surged enormously from 1984-1985 to 1999-2000 until a slight slowdown in 2004-2005 to 2009-2010. From there on, Ivory coast saw huge rebounds of 1,511 to 1,741 thousand tonnes. In Ghana on the other hand, cocoa beans production grew much of the time on a back to back basis, until it reached an all-time high of 1,025 to 897 thousand tonnes in the periods 2010-2011 and 2013-2014. Among the two remaining nations classified under the medium tier of producers, both Cameroun and Nigeria’s initial outputs of 120-125 to 150-170 thousand tonnes in cocoa beans in 1984 through 1990 fluctuated over time. By 2004 to 2010, the volume of cocoa beans in the two countries superseded the levels in the previous decades by 130-205 and 190-235 thousand tonnes. Aside from the individual group of nations, the West African region’s cocoa bean production remains quite strong in each period beginning with 1,011to1,298 thousand tonnes and 1,427 to 2,025 thousand tons by 1984-1985 to 1999-2000. This surge continued with notable increases of 2,179 to 2314 thousand tons in 2004-2005, 2009-2010 alongside the huge production volumes of 3005 thousand tonnes in 2010-2011 that cooled off slightly by 2,747 thousand tonnes in 2012-2013, only to rebound by 3098 thousand tonnes in the fiscal year 2013-2014 (Table 3).Table 3. West Africa /World Production of Cocoa Beans (thousand tons)

|

| |

|

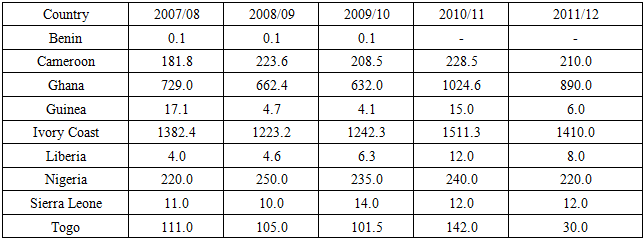

Cocoa production beans by country points to big gaps between the group of major producers known in the global stage and the nations in the region where output is at meagre levels. Of the bigger sources of cocoa beans, Ivory coast with 1382.4 to 1223.2 thousand tonnes from 2007/08 to 2008/09 held the top spot. The production pattern for cocoa beans in the country during 2009 /10 to 2011/2012 grew further to 1,242.3, 1,511.3 to 1,410.0 Thousand tonnes. The next country (Ghana) in the list of major regional producers in cocoa beans harvested about 729.0-662.4 and 632.0 Thousand tonnes in the three opening periods 2007/08 to 2009/10. In 2010 to 2012, Ghana’s cocoa bean output topped 1,024.6 to 890.0 Thousand tonnes. The duo of other nations (Nigeria and Cameroun) listed on the 3rd and 4th position among producers in the region rolled out somewhat similar volumes of cocoa beans in the marketplace estimated at 220.0-250.0 and 250.0 to 181.8, 223.6 and 208.5 Thousand tonnes between 2007/08 through 2009/10 /08. In the last periods (2010/11-2011/12), both nations saw changes in their cocoa production estimates beginning from 240.0 -220.0 to 228.5 and 210.0 Thousand tonnes. Among the quintet of third group of producers (Togo, Sierra Leone, Liberia, Guinea and Benin), Togo stands out in cocoa beans output with over 100,000 tonnes in the entire five years except for 2011/2012 when production in the country fell by 30.0 Thousand tonnes. Next comes the small country of Sierra Leone, where cocoa bean production stayed mostly in the low tens of thousand tonnes (11.0-10.0 and 12-14) throughout the years. While cocoa bean production in Liberia and Guinea were predominantly in the low thousand tones much of the time, the activities in Benin republic remained at less significant levels compared to the rest of the producers in the West African region all through 2007/08 to 2011/12 (Table 4).Table 4. Production of Cocoa Beans by Country (Thousand tonnes) Estimates Forecasts

|

| |

|

3.1.2. Regional Cocoa Production and Cultivated Areas

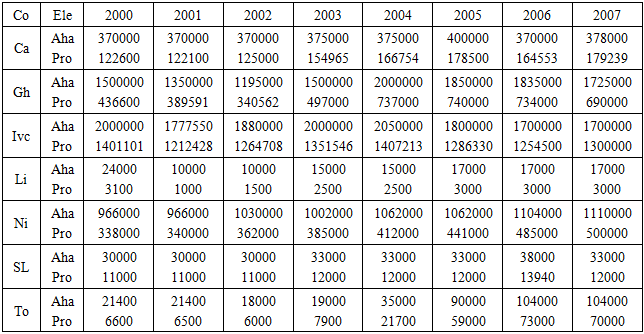

The extent of cocoa production volume and size in the West African region again shows Cameroun’s initial output of 122,600MT in 2000 fluctuated by122,100 to 125,000 -MT in the years 2001 and 2002. By 2003 to 2005, cocoa production surged (154,965 MT, 166,754 MT and 178,500 MT). The production figures for the country in 2006 and 2007 rose from 164553 MT to 179239 MT. In the case of Ghana as the 2nd largest producer in the region, note that its opening cocoa production volume of 436600 MT in 2000 dropped by 389591 to 340562 MT followed by an increase of 497000 MT in 2003. During 2004 to 2006 Ghana saw more increments of 737000-740000 MT at identical levels followed by a sudden drop of 690000 MT. Elsewhere, the Ivory Coast accounted for the largest output in cocoa production worth 1,401101 to 1.2 MT and above in the first three years from 2000 to 2002. Just as cocoa production in Ivory coast jumped from 1351546 MT to 1407213 MT in 2003 to 2004. Over time, the output of the produce reached 1286330 MT, 1254500 MT and 1300000 MT in 2005 to 2007. The nation held a firm grip on the same size of land (370000 acres) all through 2000 to 2007. Among the major cocoa producers in the region, Nigeria’s production capacity of over 300,000 MT (338000 – 340000 MT) in 2000 to 2001 rose by 362000 to 385000 MT during the two-year span that extended onto 2002 to 2003. By 2004 through 2006, the country averaged over 400,000 plus MT in production until it reached 500,000 MT in 2007.In terms of the other remaining group of producers on the lower scale as the table shows, Togo’s soft output (6000 plus MT and 7900 MT) between 2000 through 2003, grew notably by 21700 to 59000 MT and over 70000 in 2006 to 2007. At the same time, the production levels of Sierra in the tens of thousands MT (11,000 to 12,000, 13,940 MT) during the 7 years span of 2000 through 2007 exceeded the production capacity for Liberia where cocoa output stood at marginal levels below the rest of the producers in the West African region. Having said that, note also that harvested areas in the cocoa producing nations of West Africa were stable in some areas and fluctuated in others between 2000 through 2007 (Table 5). Regarding changes, the totals for cocoa harvested areas over those years not only grew among the individual nations much of the time from 4,911,400 to 5,067,000 hectares, but it also shows the predominance of the leading producing countries of Ivory coast and Ghana under regional average of over 4,996,293.5 hectares between the periods 2000 to 2007. Table 5. Cocoa Production Volume and Size 2000-2007 (Area Harvested and Size In Ha and MT)

|

| |

|

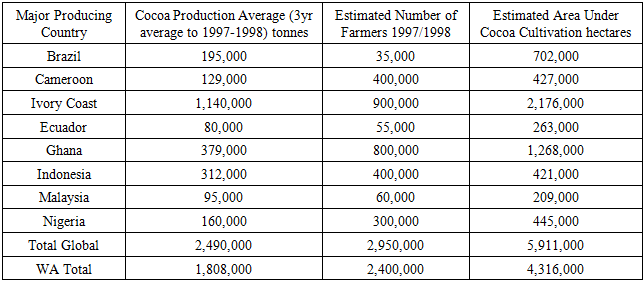

The size of cocoa production and areas under the major producing nations from 1997 to 1998 among those in the study area of West Africa indicates that while Ivory coast and Ghana led the region during those years. With cocoa production average estimated at 1,140,000 to 379,000 tonnes under a 3-year span extended onto 1997-1998, areas devoted to cocoa production on both countries in the millions of hectares (2,176,000-1,268,000 hectares) superseded other major producers in and outside of the West African region. Also, at the same time, the number of cocoa farmers in Ivory Coast and Ghana in the high hundreds of thousands (900,000 to 800,000 stood out as the highest numbers among the major producers. In the neighboring nations of Nigeria and Cameroun, indicators of production in a span of 3-year average levels, ranged from 160,000 to 129,000 tonnes on cultivated areas of 445,000 to 427,000 hectares managed by 400,000 to 300,000 farmers (Table 6). In summing up the raw figures on the listings, the study area, showed its dominance as the cocoa hub of the globe with a total of 2,400,000 active farmers and 4,316,000 hectares in cultivated area at record levels over the other producers in the sector. For that, of the world’s estimated number of farmers and areas cultivated, the West African region accounted for 81.35% to 73% of these cocoa farm indicators (Table 6).Table 6. Cocoa Production and Area Under Cultivation In The Major Producing Countries For 1997-1998

|

| |

|

3.1.3. Cocoa Production Totals and Changes 2007-2012

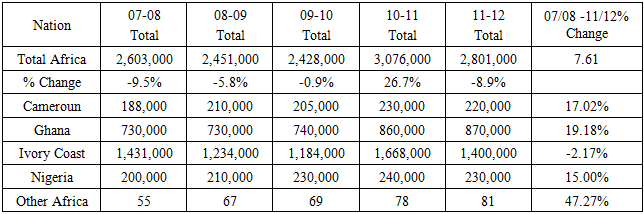

When it comes to cocoa production totals and changes from 2007-2008 to 2008-2009, the activities in Cameroun led to the production of 188 to 210 thousand tonnes of cocoa. In the other years 2009-2012, cocoa output in the country went from 205,000, 230,000 to 220,000 tonnes. In the case of Ghana, production held firm at 700,000 tonnes all through 2007 to 2010, and by 2010-2012 cocoa output moved from 860,000 to 870,000 tonnes. For Ivory Coast, cocoa production capacity over the years remained relatively similar, except for 2010-2011 when production jumped to all time high of 1,668,000 tonnes. The temporal breakdown indicates that cocoa production began in the leading nation at 1,431,000-1,234,000 tonnes and continued at 1,184,000 to 1,400,000 tonnes during 2009 to 2012. In Nigeria, the overall volume of cocoa production which exceeded 200,000 tonnes in each of the five periods went from 210,000 tonnes to 230,000 tonnes in 2008 to 2010 and continued at 240,000 tonnes in 2010-2011. Another thing to glean from the table in the context of total production throughout Africa, is that Ivory coast alone accounts for over half of the cocoa output in Africa more than the other countries. In terms of the percentages of change among the four West African nations from 2007/2008 to 2011-2012, three of them made up of Cameroun, Ghana and Nigeria posted double digit gains of 17.02 to 19.18% and 15% while Ivory coast the leading country finished with a decline of -2.17% despite dominating in absolute totals in the region all those years. The most fascinating thing about that, stems from Ivory Coast’s total (6,917,000 tonnes) at an average of 1,383,400 tonnes compared to 3,930,000 million to 786,000 for Ghana in the same categories. Elsewhere, both the neighbouring nations of Cameroun and Nigeria also maintained identical values of over 1 million to 200,000 plus tonnes in their totals and averages from 2007 to 2012 (Table 7). Table 7. Cocoa Production Totals and Change (in 000 tons)

|

| |

|

3.2. GIS Mapping and Spatial Analysis

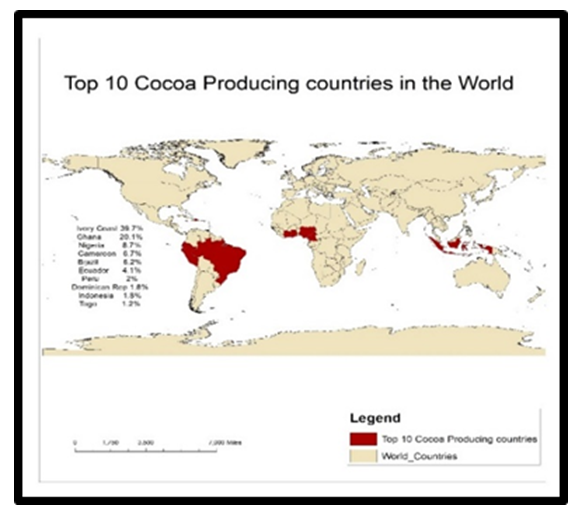

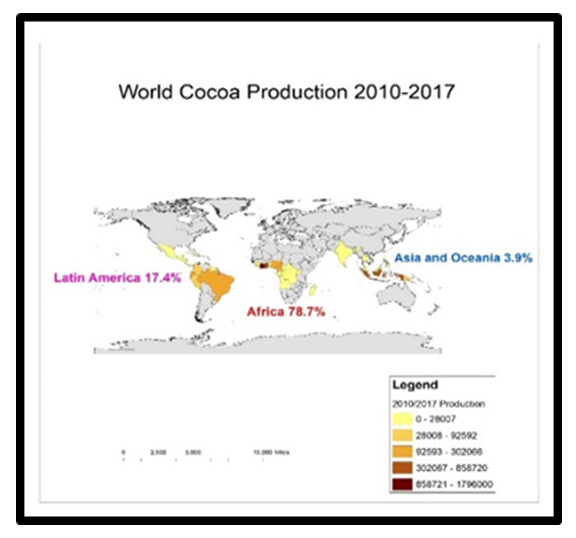

In the context of cocoa output among the top10 producing nations in the globe represented in red, much of them seem located in the tropical nations in South America and the African side of the map along the West coast on the right-hand side. Beginning with the group of 4 West African nations most notably Ivory Coast, Ghana, Nigeria and Cameroon. Note that the first two in the South west that accounted for the higher percentage points of 39.7 to 20.1 outpaced the other group of neighboring nations (Nigeria and Cameroun) in the Southern portion of the zone. In that part, cocoa production rankings mostly in single digits stood at 8.7 to 6.7% as Togo finished at only 1.2%. Among the quartet of countries (Brazil, Ecuador, Peru and the Dominican Republic) on the South American side listed below the west African zone. Their percentage rankings of 6.2-4.1 to 2-1.8 surpassed the levels in Indonesia estimated at 1.2% (Figure 2). In terms of the total percentage values at the continental level in 2010-2017, the group of international cocoa producers in Africa and Latin America held on to 78.7% to 17.8% of the output, followed by Asia and Oceania at 3.9% (Figure 3).  | Figure 2. Major Cocoa Producers |

| Figure 3. World Cocoa Output |

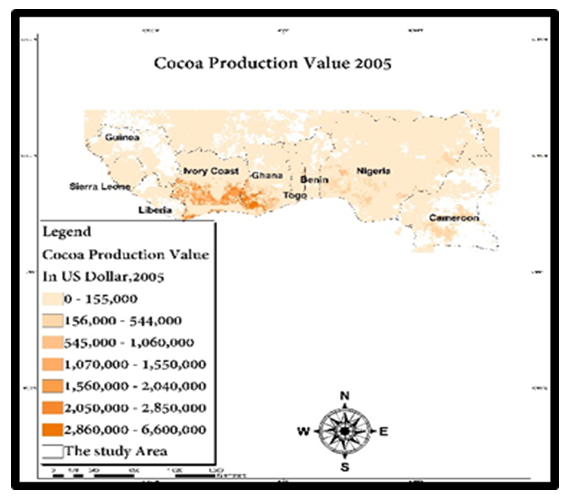

As part of the spatial analysis, the dispersion of monetary equivalence of cocoa production in 2005 under the pink and orange, captures multiplicity of dimensions germane to the trends in the producing nations in the region. Again, based on the information gleaned from the map legend and its entirety. The largest economic values stemming from the procurement of cocoa after production, points to a strong concentration of the highest dollar value accumulation estimated at $2,860,000-$6,600,000 to $2,050,000-2,850,000 and the next category of money value ($1,560,000-2,040,000) overly firm in the two leading producing cocoa areas of Ivory coast and Ghana. Just as the areas highlighted, coincide with the production patterns during the same period in 2005. The other production value scales ($1,070,000-1,550,000 and $54,000-1,060,000) even though somewhat slight, stayed fully visible in the southern side of Nigeria and Cameroon. Within that time, the dollar value levels in the low producing nations in both the Central zone (Benin, Togo) and the far South West areas of the study area (Liberia, Sierra Leone, and Guinea) faded gradually. This occurred in the lowest classes (0-155,000 to 156,000-1,060,000) of dollar equivalence stretched over various parts of the quartet of cocoa producing countries in the region in 2005 (Figure 4).  | Figure 4. Cocoa Production, West Africa 2005 |

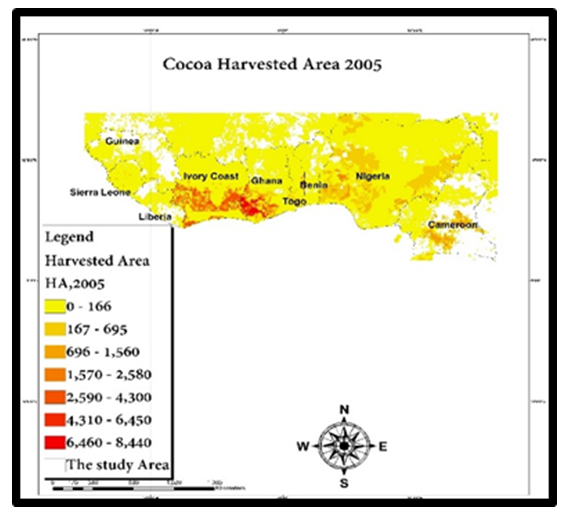

Having seen the global dimension of cocoa output distribution patterns, the geography of the size of cocoa harvested area among the countries in the study area of west Africa provides an interesting perspective that transpired in the fiscal year 2005 throughout the areas. With the configuration highlighted in red orange and yellow colors spread across the areas along the cocoa belt in the region, where large tracts of land devoted to production are harvested annually for the produce. The two major producers, Ivory coast and Ghana in light red in the lower south west, took out more produce. From the map, the network of large cocoa harvested area activities was concentrated in the South west, east central, and south east of Ivory coast, and the lower side of Ghana. In these places, the scale of harvested areas in light red as the legends indicate, were quite sizable (6,460-8,440 to 4310-6450 and 2590-4300 hectares). This was the case compared to nearby areas where lower level cocoa harvested areas (0-166 to 167-697 ha) mostly in yellow appeared in parts of the two countries. Aside from insignificant levels in cocoa harvested areas in the central zone West African nations of Benin and Togo. During the same period, there emerged a gradual pattern in the spread of the cocoa harvested areas mostly in lower categories clustered on varying scales (167-695 to 0-166 ha) over lower south nations of Nigeria and Cameroun with greater prominence in the South west, south East and North West Nigeria and the adjoining areas in Nigeria. The same can be said of the remaining countries such as Guinea, Sierra Leone and Liberia represented on the far South west corner of the map (Figure 5). | Figure 5. Cocoa Harvested Area, West Africa 2005 |

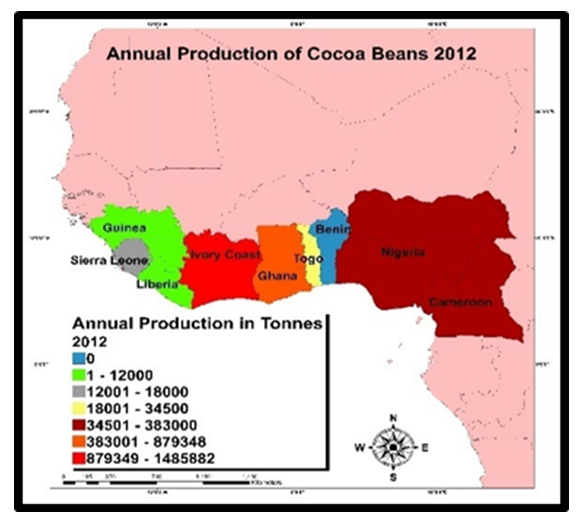

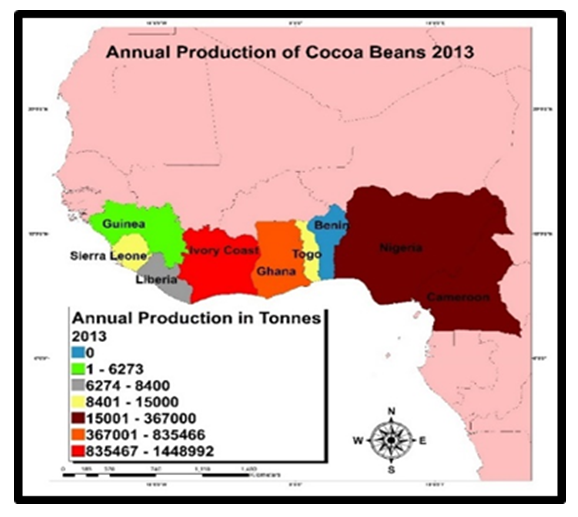

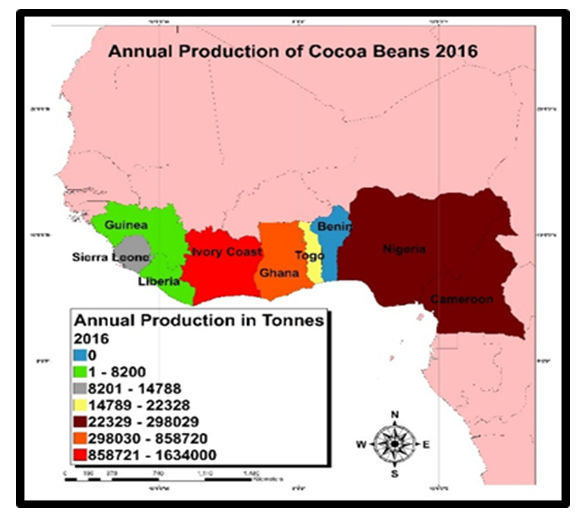

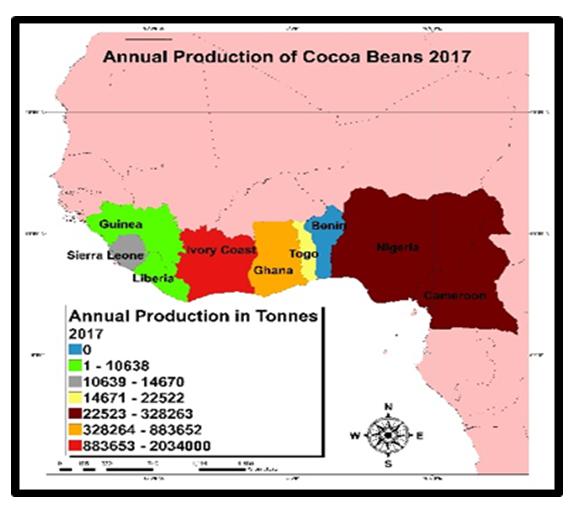

On the picture painted so far from the maps, between the periods of 2012-2013 and 2016-2017, the yearly production of raw cocoa beans in the West African zone were distinguished by various colors (beige, green, light red, orange yellow, blue and dark red). With the actual production volumes under high, medium and low numbers in the legend box, symbolizing the scales in cocoa bean output in the study area. The production activities in the first two leading nations Ghana and Ivory Coast appeared in light red and orange while the second tier group of producers (Nigeria and Cameroun) under the dark red color in the South east zone maintained their presence ahead of the low producing nations in colors of green to yellow concentrated in the South west and central part of the region. In that way, in the period 2012, the overall tonnage of cocoa bean (879349-148582 to 383001-879348 TN) produced in the near southern countries of Ivory coast and Ghana being in the top spot, surpassed those of their neighbors (Figure 6). This was followed by the gradual shift towards the south east zone of the region where annual beans production (34501-383000 TN) in the medium category remained visible in Nigeria and Cameroun. Under the third-tier areas (Liberia, Sierra Leone, Guinea and Togo) cocoa bean production faded to low values of 1-12000-18000 TN (Figure 6). Aside from the slight spatial variability between 2012-2013 in cocoa beans production as manifested in Southwest areas of Sierra Leone and Liberia. In the following years of 2016-2017, the emergent geographic patterns in the distribution of cocoa beans output among the different producer nations under the three tiers stayed consistent much of the time (Figures 7-9).  | Figure 6. Cocoa Beans Production West Africa 2012 |

| Figure 7. Cocoa Beans Production West Africa 2013 |

| Figure 8. Cocoa Beans Production West Africa 2016 |

| Figure 9. Cocoa Beans Production West Africa 2017 |

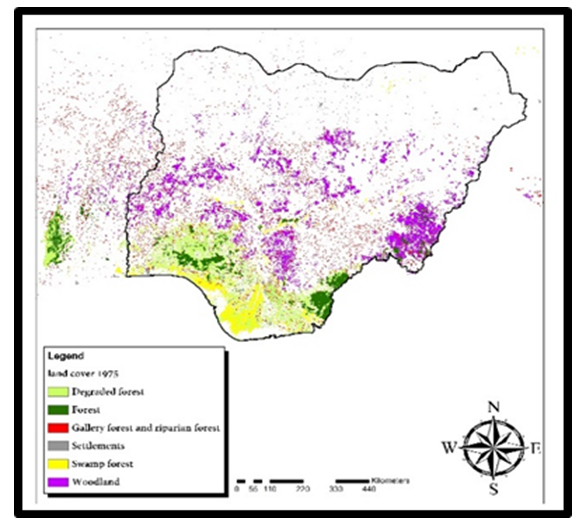

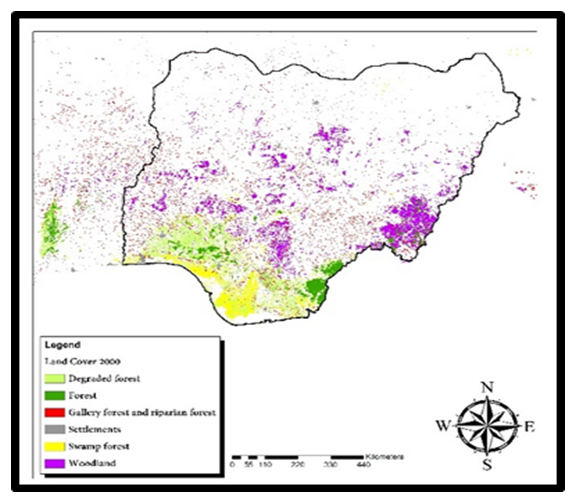

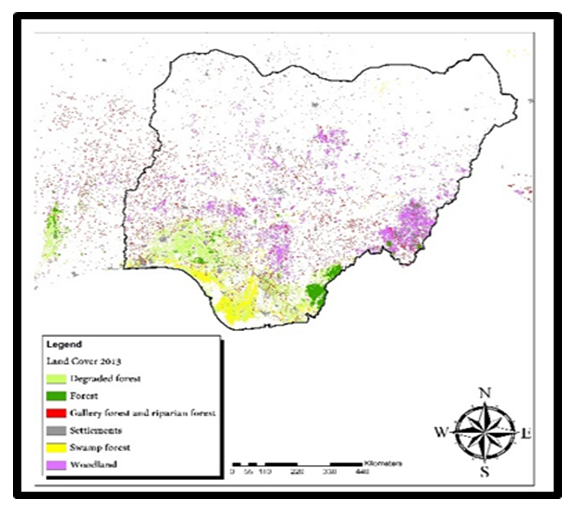

The interactions between forests/wood lands and cocoa farms and human activities in a trio of cocoa producing areas come under different patterns beginning in 1975, 2000, through 2013. The identified forms highlight the incursions of plantations onto forest cover areas with damaging consequences in the respective nations such as Nigeria, Ghana and Ivory coast. The spatial mapping of the encroachments of cocoa farming onto ecologically sensitive areas delineates forest and degradation of forest land cover areas from the activities of cocoa plantations in three of the countries in the study area from 1975-2013. The mappings revealed the common problem of forest clearance and degradation as manifested in Nigeria and neighboring nations of Ivory coast and the republic of Ghana. With the land cover indicators from degraded forest to wood land listed from the periods 1975-2013 in the three countries. The situation in Nigeria during the 1975 period especially along the cocoa belt of the area in the South West region, shows notable patches of degraded forest land adjacent to spots already designated as forested. Over the years in 2000, emerged the gradual expansion of degraded forest as forest land loss grew further in size. By 2013, the areas once covered by forests in cocoa producing areas in South West Nigeria appeared to have vanished in minute clusters, in the face of intense encroachment by cocoa farming operations (Figures 10-12).  | Figure 10. Land Cover Change Nigeria, 1975 |

| Figure 11. Land Cover Change Nigeria, 2000 |

| Figure 12. Land Cover Change Nigeria, 2013 |

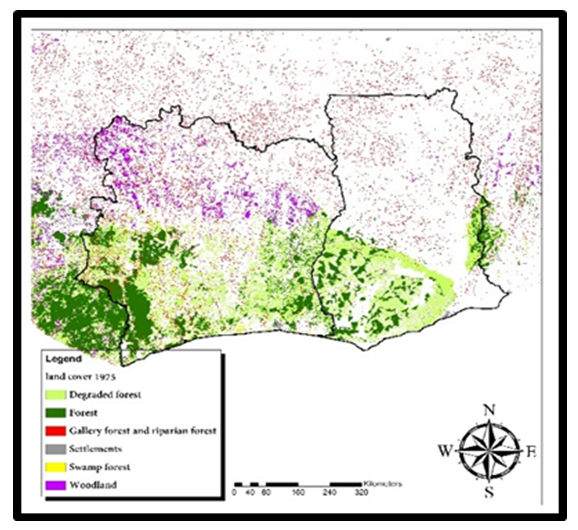

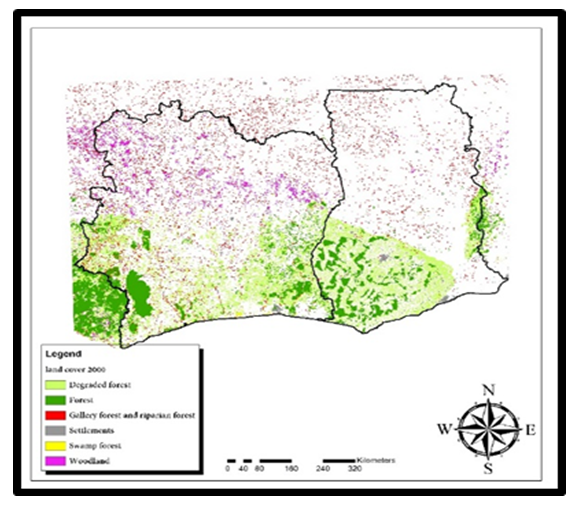

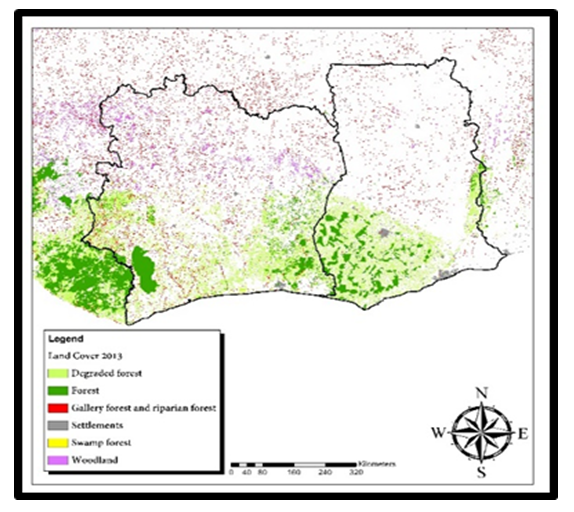

Regarding the neighboring nations of Ivory Coast and Ghana, the incidence of cocoa induced deforestation run deep in the cocoa producing areas in the Southern zone of both nations as the maps indicate. Beginning with the initial presence of vast tapestry of forest land in South west Ivory Coast, coupled with extension onto the South East corner amidst clusters of degraded forests in the middle of the country in 1975. Unsurprisingly, similar spatial patterns over forest cover also surfaced in Ghana’s southern region during the same period in 1975. While by the period 2000, both nations saw the recurrence of cocoa plantation induced deforestation manifested with the sudden loss of forest habitats and surge in degraded forest in cocoa planting areas of Southern Ivory Coast and Ghana. In 2013, the evolving geographic patterns did spread further into both neighboring nations to the extent that, the once heavily forested areas in Southwest and Southeast Ivory Coast and Southern Ghana plummeted heavily with most of the spots classified as degraded forests deemed completely faded (Figures 13-15). | Figure 13. Land Cover Change Ivory Coast & Ghana 1975 |

| Figure 14. Land Cover Change Ivory Coast & Ghana 2000 |

| Figure 15. Land Cover Change Ivory Coast & Ghana 2013 |

3.3. The Impacts of Cocoa Production

The impact assessment of cocoa farm activities in the study comprises of the environmental and social components. There is a coverage of deforestation, cocoa diseases and land degradation as well as the economic and social implications. The complete analysis under the different headings now follows.

3.3.1. Large Scale Deforestation in the Region

Widespread deforestation and degradation of West Africa’s tropical forest habitats came partly from the encroachment of small-scale cocoa operations which thrive on ecologically damaging activities such as slash-and-burn and landscape clearance. In the process, much of the ecological treasures especially the Guinean Rainforest (GRF) of West Africa, branded in the past two decades ago as a mega worldwide biodiversity epicenter or hot bed, had dropped to 18% of the original size at the beginning of the 21st of century. Having mentioned it earlier, the zone is renowned for its high cocoa output with a quartet of nations in West Africa, Ivory Coast, Ghana, Nigeria, and Cameroun responsible for 70% of international cocoa production in the past two decades [45,36]. Based on the rising levels of demands in the export markets, present estimates indicate that West Africa’s cocoa output surged by 50% all through 1987 and 2007 with much of the increment triggered by far deeper encroachments on forested habitats, amounting to huge disappearances in biodiversity and elevated carbon discharges. Over the years, the devastation of forests for cocoa farming in both Ivory Coast and Ghana has been fully recognized in the region. With cocoa seen as the purveyor of current deforestation in West Africa, the assessment of the trends among cocoa-producing zones therein revealed mounting dangers of deforestation in these places. Furthermore, from their rising production levels, cocoa farming is the leading cause of deforestation in the region especially in Ivory coast and Ghana where the rates rank among the highest in the globe. Just as Ivory coast and Ghana experienced the loss of 14% and 11% of their forest cover since 2000. From 1998 and 2007, 2.3 million hectares of the rainforest in both nations have been converted to cocoa farms especially in the Upper Guinean rainforest [12]. Added to that, cocoa is as well fast emerging as a source of deforestation along the Congo Basin ecozone, the most specie rich among the globe’s major tropical forests [12]. According to cocoa beans trade data, the nation of Cameroun saw increases of 131,075 to 263,746 tons in export in 2016. This entailed a doubling of cocoa trees planting with harvests under 3-5 years in mostly forested areas. Against that background, in 2012, the government of Cameroun announced its intentions to increase output from around 225,000 tonnes yearly to 600,000 tonnes during 2020 – an initiative likely to expose forests to further dangers [46]. Previously in the 2014 fiscal year, more than 11% of the land footprint of crop output in Cameroun was devoted to cocoa. The deforestation trends in the country, reveals the South-West region/province and two of its divisions as places with the largest cocoa output. Elsewhere, in nearby Nigeria, where cocoa has strong roots in the south west region, between 1990-2008, 8% of countrywide deforestation has been attributed to the crop [46]. The logging industry also adds to deforestation and land degradation with the rights to cut timber trees not controlled often by cocoa farmers on whose land these trees stand. On the positive side, Ivory coast intends to turn cocoa wastes into biomass energy by utilizing thousands of tonnes of cocoa pods to generate electricity power.

3.3.2. The Spreading of Cocoa Diseases and Degradation

While this is compounded by the exposure to climate change risks prompted by shrinking land base for cocoa estates, farming in both Ghana and Ivory Coast contain many old and pest-infested cocoa plants. About 23% (368,000 hectares) of Ghana’s cocoa area is more than 30 years, and 17% (272,000 hectares) is infected with cocoa swollen shoot virus disease (CSSVD. In Ivory coast, also 12% (240,000 hectares) of the cocoa land remains exposed. In the cocoa producing areas with gold deposits, farmers in need of cash, let artisanal miners use their land for mining, in return for money. This results in more land loss and degradation for cocoa farming [12,11,7,22]. In that way, artisanal and small-scale gold mining now constitutes a major problem in the cocoa producing zones in Ghana. In recent years, the number of miners and the intensity of their operations and damage they inflict has grown. Since the increasing numerical size of miners and the struggle to earn a living from farming has led to the huge expansion in informal and marginal mining operations globally. The use of mercury to extract gold is leading to serious environmental degradation. This makes contaminated fresh water unsafe for usage or in irrigation. In such settings, contaminated mud run off from the mines, creates further devastation to downstream aquatic systems like rivers and lakes. Until recently, this meant working with shovels and simple pans, but some of that now come with bulldozers, huge pumps and workers [11]. Ivory coast is increasingly confronted with these issues as well. Not only is the number of small-scale miners rising there too, but also some of the runoffs from rivers in Ghana end up in the neighboring country [47].

3.3.3. Economic and Social Effects

Knowing that cocoa may be produced essentially in developing countries, the by-products are consumed mainly in industrialized countries, with the main purchasers being the chocolate processing and confectionary industry. Some producing countries also process part of their cocoa bean output themselves. The by-products obtained (cocoa mass, powder and butter, are exported or used domestically to supply the chocolate industry. Over the years, the producing countries’ share of processing has grown steadily. In West Africa, most of the grinding entities operating in Ivory coast and Ghana, account for 14% of the world’s total volume [48,39]. Despite that, cocoa is mainly traded on the London and New York stock markets and it is highly sensitive to rumours or anticipation of stock depletions, bad harvests and weather related or political events. In those settings, the market is extremely unstable and speculative price variations can be considerable [49,1,4]. However, market prices have shown a downward trend since the early 1980s due to the dual impact of supply and the substantial reserves held by consuming countries. In the 1980s, consumer countries took advantage of the falling prices to build up considerable reserves, which they used to regulate the market to their advantage. However, producing nations are not able to build reserves in their own interest, which is why they remain subject to world market behaviour [38,50]. Under the social sphere, where the chief problem is poverty, chocolates cannot exist without farmers, yet most of them are under compensated. In the region, farmers in Ivory Coast earned an estimated 568 franc, or $1 per day. In the same nation, farmers selling cocoa within fair trade certification are living on the margins. Such certifications require that producers adhere to certain processes and management practices that confer a range of social and environmental benefits. Even with that, poverty brings a host of other problems, among them child labor and vast deforestation. Despite global awareness and industry commitments, child labor is still widespread [37]. In 2001, companies including Mars, Ferrero, the Hershey company, Kraft Foods and Nestel expressed their collective commitment to combat child labor in cocoa growing areas of West Africa. They showed their support through the Harkin-Engel protocol, an international agreement aimed at reducing the worst forms of child labor in the cocoa sector in Ivory Coast and Ghana by 70% in 2020.

3.4. Factors and Efforts

The emergent changes in cocoa land use trends in the West Africa did not materialize in a vacuum. They are associated with a variety of economic forces that are mostly market and price related coupled with the prevailing physical factors (conditions) in the zone. At the same time, a wide range of initiatives have also been put into place by stakeholders in response to ongoing concerns about the activities of the sector in the cocoa producing areas of West Africa. This phase of the paper provides a synopsis of these themes, one after the other.

3.4.1. Economic: Market and Export Earnings

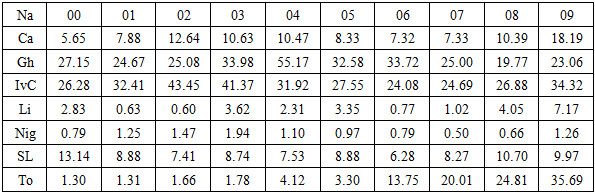

The volumes and variability in export earnings from the sale of cocoa crops in the region are key predictors of land use activities in the zone. To buttress the potentials of cocoa derived export earnings in the use of land, consider the percentage of total exports by value between 2000 through 2009 in the zone. At that time, the proceeds in Ghana and Ivory Coast mostly in double digits percentage levels accounted for the highest levels starting with 27.15%% to 25.08% for Ghana from 2000 to 2002 and 26.28% to 43.45% in earnings for Ivory Coast during the same period. In 2003 to 2006 when the value of cocoa earnings in Ivory Coast varied (by 41.37% to 31.92% and 27.55% to 24.08%) Ghana saw notable increments (of 33.98% to 55.17%) by 2003 through 2004 and additional uptick in values at over 32% from 2005 to 2006. This represents over ¼ to 1/3 and over half of the revenues in some of the years in both Ghana and Ivory Coast compared to Nigeria where the percentage of cocoa revenues from 2000 to 2009 hovered between 0.79% to 1.26% or below 2.00%. Liberia’s cocoa derived export proceeds though higher than Nigeria in some periods, stayed in lower levels as well. Despite the low single digit percentage earnings in cocoa as percentage of total export values for Togo and Cameroun, both nations posted double digit revenues over time. Togo’s value of export earnings comprised of 13.75% to 20.01% and 24.81% to 35.69% by 2006 to 2007 and 2008 through 2009, while Cameroun averaged over 10% in 2003-2004 and 2008, coupled with 12.64% to 18.19% in 2002 and 2009. Sierra Leone on its part, posted 13.14% to 10.70% in 2000 and 2008 with the remaining years (2000 to 2009) in high single digits in export earnings (Table 8). Another way to look at the significance of the earning levels is that, in as much as those revenues constituted essential components of the total exports of the principal producers like Ghana and Ivory coast all those years at average levels of 30% to 31% from 2000 to 2009. Among the lower tier nations such as Togo where cocoa as proportion of export earning averaged over 26.84% in the last fiscal years 2007 to 2009. Cocoa is central to the lives of many citizens in these nations. The same applies to Cameroun and Sierra Leone as well, even though oil rich Nigeria averaged just only under 1.07% (Table 8). Therefore, these proportions of cash flow into the economies through cocoa export exemplifies its role as the life blood of these nations since these transactions emanate from activities predicated on land use at the farm level. Table 8. Cocoa Derived Export Earnings as Percentage of Total Exports By Value

|

| |

|

Despite all these, producers in West Africa continue to be at the receiving end given the little improvement in the lives of millions of small-scale farmers who often see their fortunes diminish. In fact, in the Ivory Coast, income for cocoa farmers has dropped extensively by 30-40% over the years. With the deck stacked against the cocoa producing nations in West Africa. The variabilities in export earnings as dictated by events in the global marketplace, has not in any way translated into wealth for the citizens of the countries. This occurs under a setting dominated by unfair trade practices prevalent in the importing nations in the west. Since the GDP of the two largest producers (Ghana and Ivory coast) are heavily dependent on cocoa earnings from abroad, the only options left to them and other producers under those circumstances’ rests on continual production, hence the variations in land use indicators over the years. This seems built on the volume of export market earnings in the zone.

3.4.2. Producer Prices

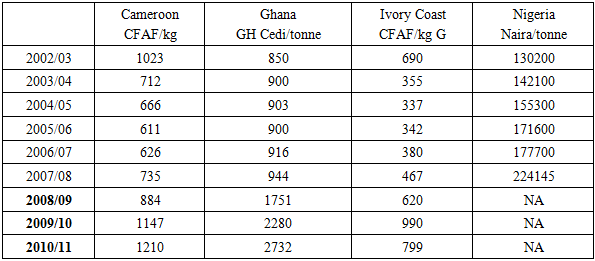

Looking at the info on the table generally, market forces operating through producer prices have the capacity to influence cocoa land use indicators in the study area. The producer prices among the nations in the zone showed a mix of increments and slides over time. Despite these fluctuations, producer prices heavily based on activities in the farms, rose in 2002/2003 to 2011 in a quartet of countries with notable rally in Nigeria and Ghana. Taking into consideration the level of volatilities in the marketplace over the years, the producer prices in various currencies saw some fluctuations. In the two French speaking areas (Cameroun and Ivory Coast) with common currency, see the major disparities in the producer prices with the world’s largest producer, having lower prices than Cameroun from 2002 to 2011. Aside from different averages of 849 to 553.3 CFAF/kg among the two nations, in 2002/03 and 2008/09 when producer prices reached 1023 to 712 CFAF/kg in Cameroun, the fees in Ivory Coast stood at only 690-355 CFAF/kg. In the proceeding years (2006 to 2008), the producer fees pattern held firm at 626-735 CFAF/kg in Cameroun followed by 380-467 CFAF/kg for Ivory Coast and during the later years of 2009 to 2011. In those periods, producer costs hovered around 1147 to 1210 CFAF/kg to 990-799 CFAF/kg. In the case of Ghana, producer costs grew yearly from 850 to 900 GH Cedi/tonne and 916 -944 GH Cedi/tonne by 2002 to 2008 followed by the highest producer price levels of 1751, 2280, to 2732 GH Cedi/tonne between 2009 through 2011. In Nigeria, also cocoa prices increased all the time by 130200-142100 Naira/tonne to 177700-224145. The consistency held firm during the early and the later years in 2002 to 2004 to 2007 to 2008 (Table 9). Notwithstanding the price movements over the years brought by the uptick in global demand, the cocoa exporting nations in West Africa do not always operate from a position of strength hence the spill over to the activities on the ground. Still, the gross disparity comes with the unequal distribution of only 6% of the $100 billion in total market value of cocoa revenues to millions of farmers directly involved in the actual cultivation of the crop in West Africa. Besides that, the common practice among importers in the West to buy and hoard cocoa arbitrarily at their will which producers cannot, affects prices and weakens the right of farmers to decent earnings. Under such uncertainties with their fate in the hands of greedy importers elsewhere, the business as usual syndrome in the sector results in more cocoa products flooding markets in ways that influence output and the land use changes witnessed in the zone from 1975-2017. Table 9. Producer Prices In Selected Cocoa Exporting Countries Producer Prices in Local Currency

|

| |

|

3.4.3. Physical Environment

The role of the physical environment in driving the activities leading to changing cocoa land use and the production capacity over the years in study area cannot be overstated here. Principally, West Africa as a major global cocoa frontier within the equatorial environment, consists of over a dozen countries with favourable climates across diverse ecosystems. Despite the rising levels of cocoa farming activities among other competitors worldwide from the continents of Asia and the Americas. Large amounts of the world’s cocoa produce do originate solely from the leading West African countries of Ivory Coast and Ghana in Sub-Saharan Africa. From the combined values of 60% of world cocoa beans in both nations. Essentially, cocoa crop cultivation flourishes entirely in and around equatorial climates similar to the West African region where tilling relies on increased heat or temperatures and heavy rainfall to thrive under the moist tapestry of gigantic rainforest plants needed to furnish shade, and protection to the crop from the bombardment of sun rays, and devastation from eventual storms in the wet season. With overall population of hundreds of millions of people. The West African region remains the area with unused potentials and untested markets waiting to explode in ways that could one day unlock unfair trade practices impeding access to wealth through the production, export and consumption of the produce, despite the current reliance on revenues from markets outside the zone. With these attributes in place and the climatic advantage of being in the equator, the size of cultivated areas has surged remarkably as production rose yearly by millions of tons under the sustained stewardship of millions of small scale farmers since the opening decades of the 21st century. Thus, the various transactions pertaining to cocoa land use variables as witnessed over the years in the sector and the ensuing changes in the region would not have occurred in the absence of the physical environment. Clearly, the environmental factor partly played a role in influencing the land use changes in cocoa farming in the study area.

3.5. The Efforts of Stakeholders

Chocolate companies, cocoa processors and governments have come together under the cocoa and forests initiative. On July 4, Ghana launched its national implementation process, and Ivory coast pledged to begin reforestation, but reclaiming what has been lost will take time because replanting will be extensive. Anything less than that will not save Ghana and Ivory Coast from an environmental tragedy in 20 years. These issues are not limited to a handful of countries and not the fault of farmers but are illustrative of a system buoyed by inequity and corruption. Furthermore, the official regulator in Ivory Coast in a ruling demanded that cocoa farmers reduce output in October of 2019 by 2.2 million tonnes to 2 million tons for the fiscal year 2020 in an attempt to prevent farmers from over producing as Ghana and Ivory Coast put forward a plan to boost farmers revenues. In the process, both top producing countries introduced a fixed $400 per tonne in cost of living differences on every contract in 2020/2021. They also committed to using raised funds to assure planters 70% of the $2600 per ton price goal [50]. At the same time, a corporate entity, Cargil has set aside about $12.3 million for the next 36 months to advance sustainable chain traceability schemes in both nations. This involves the dual disbursement of $7.7 to $3.4million in the nations of Ivory Coast and Ghana to ensure the safety and welfare of kids and households residing in cocoa producing communities in a way that enhances an open cocoa distribution network for clients and traders. While this initiative entails the increases in child labor monitoring system together with International Cocoa Initiative from 53-46,800 to 130-120,00 cooperatives and farmers. To rehabilitate child labor victims, 6 new schools are now under initial stages of construction to serve affected areas in Ghana [43].

4. Discussion

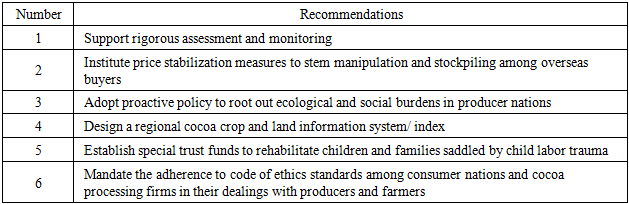

This segment of the study discusses the major points that emerged. Essentially, this research has assessed the rising issues in cocoa land use activities and the environmental impacts in some nations within the Sub Saharan Africa zone in West Africa using mix scale model of GIS and descriptive statistics. The research as well centred on the fundamental concerns through a profile of the study area anchored in material and methods component and ecological impact assessment. From there, the study highlighted factors influencing cocoa farming land use, the impacts and the initiatives of the core stockholders and actors at the local and global scene. Despite the widespread issues inherent in the cultivation of cocoa among West Africa’s exporting nations. The land use activities have been blurred by the widespread concerns over child labour, market volatility, price manipulation in the processing markets in the west, production variability, and the visible dangers of environmental degradation, the spreading of cocoa diseases, and deforestation. The present level of cocoa farming activities stands bolstered by distribution of harvested cocoa areas, cocoa beans production, the ranking of major cocoa producers, coupled with export earnings and producer prices of the commodity over the years. This is manifested given the changes amongst land use indicators such as production, cocoa areas harvested, cocoa beans production, cocoa production totals, the exploitation of cocoa farmers and their propensity to poverty and unfair practices perpetrated by the buyers in consumer nations with mounting environmental costs. To assess these problems, the paper applied mix-scale method of temporal-spatial analysis connected to descriptive statistics and GIS. From the analysis, the planters in West Africa under a major cocoa hub with large stocks of cocoa produce, harvested vast areas in multiple countries of the region. These where areas the production hovered at robust levels, notwithstanding pressing concerns of price volatility, child labor [51], and the risks posed to the surrounding ecology. In as much as cocoa farming and land use indicators from production to import remained quite substantial amidst changes in the study area from 1984 to 2017. Of the major variables in the West African region’s cocoa industry, the percentage levels of harvested areas in 2010-2013, were much higher in a trio of nations most notably Ghana, Ivory Coast and Liberia. Within the same periods in the entire West African region, cocoa production rose significantly by 1011-3098 thousand tons from 1984-1985 through 2013-2014. While several countries in the region have been quite dominant globally in cocoa production ahead of their competitors given the increase of 2-3 million tons in output beginning in the 2000s. By 1988 and 2007, the study area saw the disappearance of millions of hectares of forested areas to cocoa farming. This came at the expense of marginal operators who regularly face the threats of degradation and diminishing production and crop destruction by pests. While this is compounded by the exposure to land use change risks, prompted by shrinking land base for cocoa estates, cocoa farming in both Ghana and Ivory Coast contain many old and pest-infested cocoa plants.Seeing the relevance of cocoa farming in both the economies of the nations and welfare of the producing localities involved in it. The inherent challenges like unfair trade practices unleashed by the importing nations towards the sector are of great importance to planners, since inaction drives their recurrences. Yet, despite the billions of dollars in imported cocoa in 2014 in the west, cocoa farmers in leading producing nations like Ghana and Ivory endured the biggest land use footprint estimated at 25% out of each crop production. Accordingly, the factors and the impacts of cocoa land use farming activities left unwanted footprints in the farm hub of the zone with the loss of large parcels of natural areas to the cultivation of the crop coupled with the exposure of many farmers to poverty. These issues have been made worse by other socio-economic factors like prices and the inequities tied to the exploitation of minors through child labour during harvests, as well as the latest threats to the region’s biodiversity from cocoa production.Aside from the changes in land use indicators and related parameters, coupled with huge potentials and ecosystem degradation from cocoa farming. The geographic diffusion of the tendencies, using GIS visualization reveals huge harvest potentials, and heavy concentration of clusters of areas with enormous production capacity, a steady spreading of deforestation in cocoa producing areas of the region due to socio-economic and ecological factors. Thus, the variations in cocoa output and land use indicators in the zone never happened on their own. The investigations as carried in the study showed they are linked to socio-economic and physical factors of pricing, penchant for export earnings and the physical/ecological conditions conducive to the cultivation and the abundance of the resource in an equatorial area like West Africa. In that way, the upsides from the enquiry and the inference drawn from it is so informative, that it offers fresh hopes for the nations, managers and stakeholders involved in building further on the current production capacity in the years ahead. This would put them in better positions in combating the roadblocks to fair practices and equitable distribution of cocoa revenues vital to improving the welfare of farmers and their communities as well as the victims of child labour in the sector. More so, the enquiry offers a feasible template for managers in assessing the propensity to various risk exposures on the part of producers in fragile ecosystems in the zone. While regional analysis of cocoa land use activities in the study area and the effects ushers in the pathways for quick interventions during critical situations for managers, stakeholders and producers. Opportunities exists for regulators and scholars in the zone to use the findings as appropriate tools for appraising events in susceptible communities and protecting them from the bad practices fueling land degradation, deforestation, child labour and poverty. To address the issues that emerged in the study, the paper proffered suggestions starting with the need for ecosystem monitoring and assessment, to the adherence to ethical standards among consumer nations and the processing firms therein and the design of a regional land use index. See Table 11 in the Appendix for a brief summary of the recommendations.

5. Conclusions