-

Paper Information

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

Frontiers in Science

p-ISSN: 2166-6083 e-ISSN: 2166-6113

2015; 5(1): 1-8

doi:10.5923/j.fs.20150501.01

Characterizing Beef Cattle Value Chains in Agro-Pastoral Communities of Uganda’s Lake Victoria Basin

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLDenis Mpairwe1, Emmanuel Zziwa2, Samuel K. Mugasi3, Germana H. Laswai4

1Department of Agricultural Production, Faculty of Agriculture, Makerere University, Kampala, Uganda

2Association for Strengthening Agricultural Research in Eastern and Central Africa, Entebbe, Uganda

3National Agricultural Advisory Services, Kampala, Uganda

4Sokoine University of Agriculture, Morogoro, Tanzania

Correspondence to: Emmanuel Zziwa, Association for Strengthening Agricultural Research in Eastern and Central Africa, Entebbe, Uganda.

| Email: |  |

Copyright © 2015 Scientific & Academic Publishing. All Rights Reserved.

A study was conducted to characterize the existing beef value chains in the agro-pastoral communities around Lake Victoria Basin of Uganda and examine their potential for improvement. 100 beef cattle producers and 32 traders were interviewed in Rakai, Isingiro and Lyantonde Districts to understand their marketing channels and attributes. Majority of producers were small scale owning 1 – 50 cattle in Rakai (69.5%) and Lyantonde (54.6%) while Isingiro was dominated by large scale farmers owning more than 100 cattle (39.3%). 75% of producers sold cattle at farm gate, 13% in formal and 6% in informal livestock markets, while 6% to abattoirs. Cattle size and weight were reported by 67% and 24.8% respectively by respondents as major factors used in setting cattle prices followed by breed (7.1%) and production costs (1.1%). Four existing beef cattle value chains were identified ending with export of live cattle, consumption in cities and towns, consumption in production areas, and niche African markets. One potential value chain identified is the niche non African markets. Long beef cattle value chains exist in agro-pastoral communities which reduce the profit margins for producers. Identified strategies to improve the existing value chains include establishment of feedlots, buying of animals from smallholders for fattening in feedlots by commercial ranchers, and exploiting niche non African markets. Since animal size and weight are major factors determining cattle prices, cattle fattening using low cost crop residues could provide producers with more income.

Keywords: Agro-pastoral, Beef value chain, Cattle marketing, Production system

Cite this paper: Denis Mpairwe, Emmanuel Zziwa, Samuel K. Mugasi, Germana H. Laswai, Characterizing Beef Cattle Value Chains in Agro-Pastoral Communities of Uganda’s Lake Victoria Basin, Frontiers in Science, Vol. 5 No. 1, 2015, pp. 1-8. doi: 10.5923/j.fs.20150501.01.

Article Outline

1. Introduction

- Pastoral and agro-pastoral production systems supply more than 85% of milk and 95% of beef consumed in Uganda [1]. Historically, land was communally owned under pastoral systems and cattle production largely depended on mobility of pastoralists to search for pasture and water [2]. Mobility would enable the restoration of depleted grazing areas and maximize herd sizes without further degradation of land [3, 4]. However, the individualization of land ownership undermined pastoral mobility in Uganda’s rangelands and paved the way for sedentary and agro-pastoral systems [5]. Under agro-pastoral systems, cattle production requires more investment in pasture, water and feeding practices if sustainable production is to be achieved without degrading natural resources [6]. However, the unfavorable marketing systems and the less returns gained by cattle producers renders it more difficult to invest in production resources hence leading to critical degradation of grazing areas under the settled production systems [7, 8]. The pastoral and agro-pastoral production systems have peculiar characteristics relative to climatic conditions, cultural connotations, location and resource ownership which influence the marketing systems and the profit margin obtained by the different value chain actors [9, 10]. Climatic variability and fragile soils are major characteristic features of Uganda’s rangelands and major determinants of cattle production systems [11]. In addition, limited participation of pastoralists in livestock markets due to lack of incentives [12-14] and poor infrastructure [15, 16] greatly contribute to low market off-take. This hinders Uganda’s need to meet the country’s demand for meat and subsequently resulting into increasing trade deficit for meat [17]. Although poor breeds, inadequate feeds and diseases are the major factors limiting livestock production in Uganda and developing countries at large [18-20], poor market systems characterized by a long marketing chains also provide a disincentive to farmers not to produce more because of the limited profit margins they obtain. In addition, the majority of smallholder cattle producers in pastoral and agro-pastoral communities only sell their animals in response to short term demands for cash and dry season water and forage scarcity rather than market demands [21-23]. Because of this, profits in the existing marketing system are more skewed to traders [24], since the farmers intention of selling is driven towards problem solving than business. This further de-motivates livestock producers. Fixing livestock marketing problems in agro-pastoral communities leading to profitable gains to producers is envisaged to increase their investment in production resources and reduce resource degradation. This will also lead to increased off take rates and increased meat supply to meet the country’s demand. The objective of this study was therefore to characterize the existing beef value chains in the agro-pastoral communities around Lake Victoria Basin of Uganda and examine their potential for improvement.

2. Materials and Methods

- Study areaThe study was conducted in Isingiro, Lyantonde and Rakai Districts, which are located in the rangelands of Lake Victoria Basin. Rakai District is located in south-western Uganda between 31°04’ and 32°00’E, and 0°01’ and 1°00’S and receives annual rainfall of 1000 – 1200 mm. It borders Lyantonde District to the northwest, Lwengo District to the north, Masaka District to the northeast, Kalangala District to the east, the Kagera Region in the Republic of Tanzania to the south, Isingiro District to the southwest and Kiruhura District to the northwest. Lyantonde District lies 00°25’S 31°10’E, receives annual rainfall of about 750 - 1000 mm and is bordered by Sembabule District to the north and northeast, Lwengo District to the east, Rakai District to the south, and Kiruhura District to the west. Isingiro District is located 00° 50’S, 30° 50’E, receives annual rainfall of between 800 - 1040 mm and is bordered by Kiruhura District to the north, Rakai District to the east, the Republic of Tanzania to the south, Ntungamo District to the west, and Mbarara District to the northwest. The three districts are geographically located in Uganda’s cattle corridor (rangelands) with characteristic savannah grass lands and thorny acacia shrubs. The rainfall is bimodally distributed with long rains between March and June and short rains between September and November with characteristic dry spells between December and February and July to September. The districts are dominated with rain-fed smallholder farming systems and agro-pastoralism. Rakia District is known for increasing climatic variability, while Isingiro and Lyantonde for vulnerable dryland agro-pastoralism.Data CollectionSurveys were conducted in Rakai, Isingiro and Lyantonde targeting livestock producers and traders. A total of 100 producers and 32 traders were interviewed. 37 producers and 16 traders in Isingiro, 30 producers and eight traders in Lyantonde and 33 producers and eight traders in Rakai were interviewed. Cattle farming households were categorized into three groups basing on the number of cattle owned. These were small, medium and large scale producers owning 1 – 50, 51 – 100 and more than 100 heads of cattle respectively. Pre tested questionnaires with structured and semi- structured questions were used and data was coded and subjected to statistical analysis using SPSS-19.

3. Results

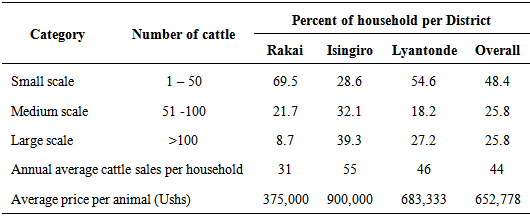

- Cattle production and salesThe majority of households in Rakai (69.5%) and Lyantonde (54.6%) were small scale producers while the majority in Isingiro (39.3%) were large scale producers (Table 1). The average number of cattle sold annually per household was highest in Isingiro (55) followed by Lyantonde (46) and lowest in Rakai (31). The average price per animal also followed a similar trend with the highest recorded in Isingiro (Ushs 900,000) followed by Lyantonde (Ushs 683,333) and lowest in Rakai (Ushs 375,000).

|

|

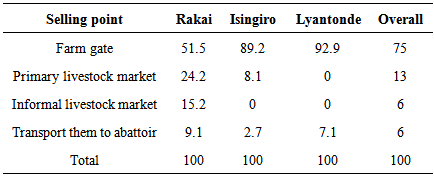

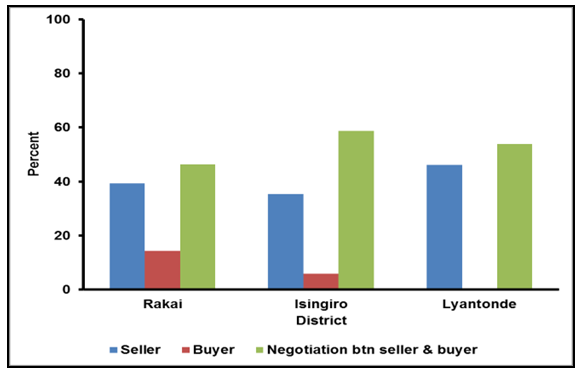

| Figure 1. Proportion of farmers selling cattle to different buyers |

|

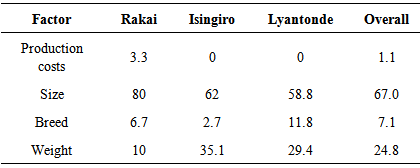

| Figure 2. Determinants of cattle prices |

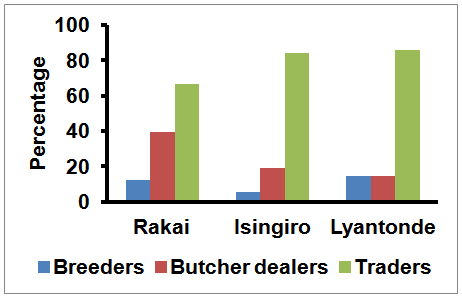

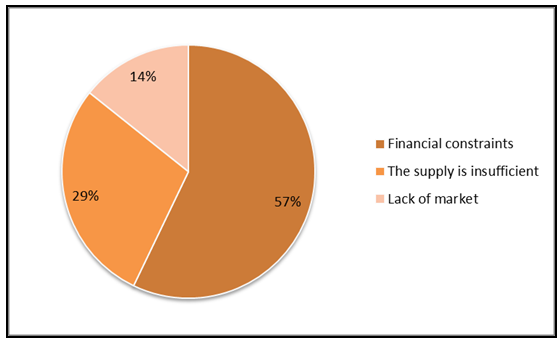

| Figure 3. Factors limiting the traders scale of operation |

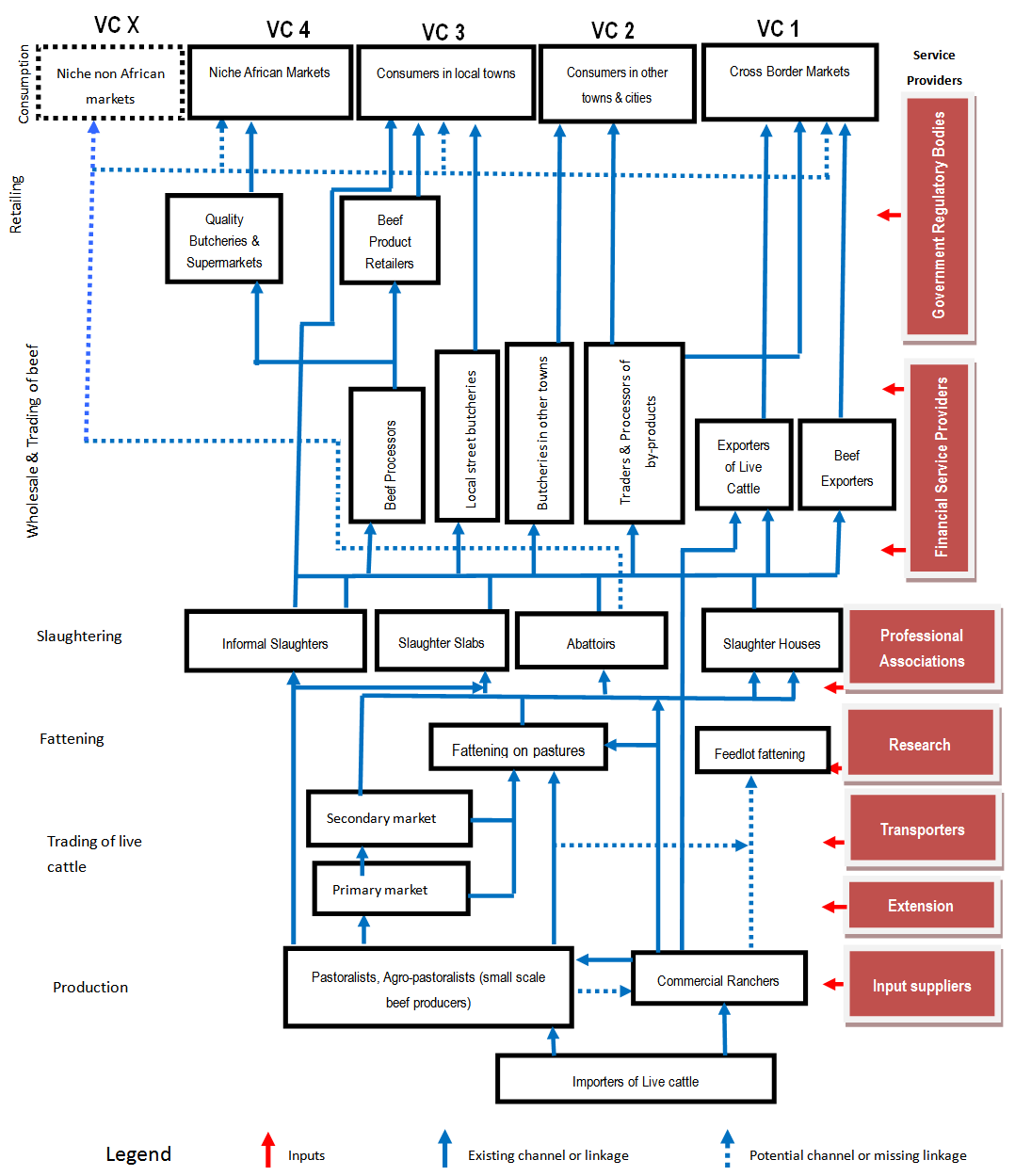

| Figure 4. Beef cattle value chains in the Lake Victoria Basin of Uganda |

4. Discussions

- The major differences among cattle producers in the study area was scale of production (small, medium or large scale) and this influenced the production and marketing practices of beef cattle. Differences in scale of production could be attributed to access and ownership of land [25] with majority of farmers having full land ownership rights in Isingiro and Lyantonde under large and medium scale while farmers without land ownership rights especially in Rakai under small scale production. These findings were consistent with several studies [26-30] which reported that farm size, access and ownership of land are major factors influencing adoption of agricultural technologies. As such, farmers under large and medium scale (especially in Isingiro and Lyantonde) practiced modern beef production and marketing practices which included introduction of improved breeds of cattle, cattle weighing systems and reduced actors in the beef value chains compared to small scale producers mostly found in Rakai.The selling of animals at farm gate and higher prices in Isingiro and Lyantonde were attributed to the fact that majority of producers in these areas were operating at large scale and with improved beef breeds and their crosses (Bonsmara, Boran, American Brahman and Chalolais). The exotic breeds have a big body size and weight hence high prices compared to the indigenous breeds owned by small scale beef producers in Rakai. Also, large and medium scale producers sell off a high number of cattle at a time to load a truck. As such, these producers do not need to go through primary and secondary markets as small scale producers. Also, proximity to main markets and road networks affect cattle prices as reported in earlier studies [12, 16]. This may explain why cattle prices in Lyantonde are higher than Rakai because of the easy access to Lyantonde and proximity to big towns and the city.Cattle markets and marketing channelsFarmers in Rakai still access communal grazing areas especially in the Sango bay estates. This often exposes their animals to contagious diseases (especially Foot and Mouth Disease) leading to the imposition of quarantines. As such, farmers often resort to informal markets if they are to sale their animals. Rakai has the highest percentage of farmers selling animals in livestock markets for both primary and informal markets. Because of poor grading systems and lack of facilities in existing livestock markets [22] it may be another reason contributing to lower cattle prices in Rakai District where many farmers sell animals in markets. Inadequate infrastructure was also noted to impose a serious constraint on the marketing of livestock [24]. As such, cattle keepers located in areas remote from the major markets where there is lack of physical infrastructure have poor access to markets and get lower prices for their animals.Traders and middlemen often believe that once animals are brought to these markets, farmers have no option but to sell at any price, hence the lower prices for animals sold in markets than at farm gate. Because of the long distance from Rakai and Isingiro to Kampala city (the major market for beef) and bad roads, farmers in these districts access longer marketing systems that include primary markets which are lacking in Lyantonde because of its close proximity to the city. Factors considers in determining the prices of cattleCattle size and weight were the major factors influencing the price of cattle. The ultimate goal of beef cattle producers as well as traders is having more meat on the animal. Traders preference for animals above 100 kgs is to minimize on costs incurred since movement permits, market dues and transportation are charged per animal regardless of its size. Therefore, money is saved when big animals are bought compared to small animals. Breed is not an important consideration in determining the price for traders, though a good attribute when selling breeding stock. Improved breeds such as Boran, American Brahman, Friesians and Charolais have thus been introduced because of their fast growth rates and quick returns to investment compared to indigenous breeds which take long to attain market weight.Existing beef cattle value chainsThe existing value chains were dependent on scale of production, proximity to main markets and town centers as well as prevalence of contagious diseases. The use of primary traders who buy cattle from farms and sell them to secondary traders in markets as well as the selling of animals in markets was common under small scale pastoral and agro-pastoral production systems and were more pronounced in Rakai District. The main reason behind this is that commercial ranchers sell off many animals at a time and can individually load a truck for delivery to city abattoirs or export. Some ranchers also have framework contracts for regular supply of animals to processors in the city. On the contrary, pastoralists and agro-pastoralists sell off their animals when there is a family need and thus sell fewer animals at a time. This means that traders have to move farm to farm until they collect enough animals to load trucks to the city or for export. Fattening of animals in the two systems was done on pasture. There are no commercial feedlot systems and this provides an avenue for improvement of the beef value chain in agro-pastoral communities. Feedlots were noted to increase animal weights and beef quality better than pasture finishing and thus high prices for animals [31].

5. Conclusions

- Beef cattle value chains in the agro-pastoral communities of Uganda were greatly influenced by scale of production with cattle from large scale producers going through shorter value chains and with fewer actors than cattle from small scale producers. Although beef producers have a high bargaining power in setting up cattle prices; the lack of enabling structures like weighing equipment limits their profits. Because size and weight are major determinants of cattle prices, interventions like animal supplementation and feedlot management can increase the price of animals and profit margin of producers if low cost feedstuffs are used. With the majority of beef producers in Uganda being smallholders, it was concluded that the current beef value chains are long, with many actors and lack enabling infrastructure.

6. Recommendations

- The existing beef cattle value in the agro-pastoral communities are long and with many actors involved. As such, potential improvements in the value chains should focus on reducing the number of actors, and provision of enabling infrastructure in livestock markets that will enable farmers and traders to sell animals by weight rather than visual estimation of their sizes and weight. Participatory feedlot trialing with communities should be conducted to assess the profitability of animal fattening.

ACKNOWLEDGEMENTS

- The authors are grateful to the beef value actors interviewed for their collaboration during the study. District production and agriculture officers in the study districts are also appreciated. The supportive role provided by Makerere University, Department of Agricultural Production staff and students is greatly acknowledged. This study was funded by Lake Victoria Research Initiative (VicRes), through the Inter-University Council for East Africa (IUCEA).