-

Paper Information

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

American Journal of Economics

p-ISSN: 2166-4951 e-ISSN: 2166-496X

2013; 3(2): 127-131

doi:10.5923/j.economics.20130302.11

Drivers of Sustainable Environmental Manufacturing Practices and Financial Performance among Food and Beverages Companies in Malaysia

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLHameed Olusegun Adebambo 1, Rihanat Idowu Abdulkadir 2, Nik Kamariah Nik Mat 3, Alaa A jihad Alkafaagi 3, Anas Ghassan Jadou kanaan 3

1School of Technology Management & Logistics, Universiti Utara Malaysia, Kedah, 06010, Malaysia

2Department of Accounting and Finance, University of Ilorin, Nigeria

3Othman Yeop Abdullah Graduate School of Business, Universiti Utara Malaysia, Kedah, 06010, Malaysia

Correspondence to: Hameed Olusegun Adebambo , School of Technology Management & Logistics, Universiti Utara Malaysia, Kedah, 06010, Malaysia.

| Email: |  |

Copyright © 2012 Scientific & Academic Publishing. All Rights Reserved.

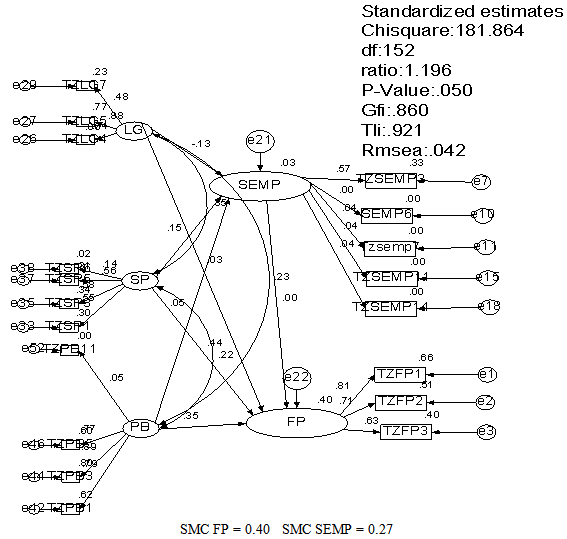

This study investigates the direct influence of the drivers of sustainable environmental manufacturing practices, sustainable environmental manufacturing and financial performance. Quantitative research design was employed in conducting this study. Primary data was collected through questionnaire which was delivered by hand to 257 respondents including the managers, executives/senior executives of food and beverages companies in Malaysia. 115 questionnaires were returned and used for the analysis. Structural equation modeling was employed to analyze the collected data using Amos 16. A fit model was achieved from the confirmatory factor analysis after eliminating few items recognized as errors by the modification indices verification showing the goodness of fit model (Ratio = 1.196; P-value = 0.05; GFI =0.860; TLI = 0.921; RMSEA = 0.042). Based on this, it was found that stakeholder pressure and perceived benefits are significantly related to financial performance.

Keywords: Sustainable Environmental Manufacturing Practices, Financial Performance, Stakeholder Pressure, Perceived Benefits

Cite this paper: Hameed Olusegun Adebambo , Rihanat Idowu Abdulkadir , Nik Kamariah Nik Mat , Alaa A jihad Alkafaagi , Anas Ghassan Jadou kanaan , Drivers of Sustainable Environmental Manufacturing Practices and Financial Performance among Food and Beverages Companies in Malaysia, American Journal of Economics, Vol. 3 No. 2, 2013, pp. 127-131. doi: 10.5923/j.economics.20130302.11.

Article Outline

1. Introduction

- The importance of the manufacturing sector cannot be over emphasized as a result of its contribution to the gross domestic product of the Malaysian economy. This has been witnessed in its contribution to the total products exports, employment generation. This also added to the improvement in the performance of the manufacturing industry of the nation[1]. Despite the contributions of the manufacturing sector on the economy, the operations have also impacted negatively on the environment.Among the negative impacts of the manufacturing companies on the environment include: huge consumption of resources, high consumption of energy for production processes, destruction to the green-house gas (GHG) as a result of the huge emission of carbon dioxide (CO2) into the environment[2]. Inspite of the negative impact of the manufacturing sector on environmental degradation and depletion, Reference[3] opined that the manufacturing industries have a high potential of becoming the driving force behind the implementation of sustainableenvironmental manufacturing practices.Recently, there has been an increasing demand from the stakeholders, requesting the manufacturing companies to be more environmentally responsible to their products and production processes (e.g[3],[4]) This demand is as a result of the factors that drive the implementation of sustainable environmental manufacturing practices which include: perceived benefits, stakeholder pressure and legislative compliance[3]. Hence, sustainable environmentalmanufacturing practices are regarded as a source of better firm performance in an organization ([5],[6]).Previous literatures on sustainable environmental manufacturing practices have indicated two different ways in which firms perceive environmental manufacturing services [27]. Firm investment in environmental manufacturing practices is regarded as a complete burden in firms, as more cost is incurred in the implementation of the practices[27]. Such cost may result from compliance with legislation and pressure from the stakeholders. However, according to[3], some of the benefits of manufacturing companies from the implementation of sustainable manufacturing practices are as follows: manufacturing cost reduction; improved image of the firm, increased product quality. As such, this study seeks to investigate the influence of the drivers of sustainable environmental manufacturing practices on firm performance. This study will be limited to only the financial performance, thus the non-financial performances are out of the scope of the study.

2. Review of Previous Literatures

- Previous literatures on sustainable environmental manufacturing practices have identified relationship between sustainable environmental practices and firm performance (e.g[7],[8],[9],[10]). Reference[7] investigated therelationship between environmental practices and firm performance. They therefore, concluded that environmental practice is significant to firm performance. Similarly,[8] studied green manufacturing practices and document a positive relationship between sustainable environmental practices and organizational performance.[10] reported that the improvement of practices ensures a reach super level of performance among manufacturing companies. Also,[11] investigated the impacts of environmental concern on firm performance between manufacturing and service companies and found a positive significant relationship between environmental concern and attributes of performance. However, the result shows that there is no significant difference between the environmental practices of manufacturing and services companies. Contrary to the findings reported above,[12] found a negative relationship between Environmental performance and Economic performance. Similarly,[13], on therelationship between emission reduction and firm performance where firm performance was defined as including both operating and financial performance reported that reducing emission is negatively significant to firm performance.[9] found environmental practices as negatively significant to economic performance but the study also indicated that environmental practices is positively related to environmental performance. It is apparent from the studies reviewed above that finding on the relationship between environmental practices and firm performances have been inconsistent. This inconsistence has been reported earlier by (e.g[3],[7],[14],[15]). Furthermore, past researchers have identified that relationship exist between the drivers, environmental practices in firms and performance (e.g[16],[17],[18],[19]). Reference[16] found a positive relationship betweenstakeholder pressure and corporate environmental management practices. Reference[19] found that perceived stakeholder environmental pressure is related to reverse environmental logistic practices. [18] Identified a relationship between perceived benefits and hotel performance in Malaysia. Thus, it was concluded that regulation is one of the factors that drive performance in an organization. As a result, this study hypothesized that: 1) stakeholder pressure, perceived benefit and legislation directly influence sustainable environmental manufacturing practices in firms and 2). Sustainable environmental manufacturing practices directly influence financial performance in firms.

3. Research Methodology

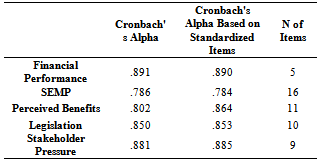

- This study employed the use of questionnaire for data collection in order to achieve the objectives of the study. This data was collected among the Malaysian food and beverages manufacturing companies. Two hundred and fifty seven (257) questionnaires was distributed to the respondents out of which one hundred and fifteen (115) usable questionnaire was collected. The list of the participated companies was obtained from the database of the Federation of Malaysian Manufacturers (FMM) directories. Firms involved in this study range from the medium to the large organization, with more than fifty (50) full-time employees. This exclusion criterion follows the assertion of[20] that companies with less than fifty (50) full-time employees are less feasible to implement sustainable environmental manufacturing practices due to some certain restrictions and barriers. The respondents of this study are the managing directors, manufacturing and/or production managers, quality managers\and the companies executives.The development of the questionnaire in this study is divided into four parts; (a) contains information about financial performance of the selected companies, (b) contains information about sustainable environmental manufacturing practices, (c) the drivers/motives for implementing sustainable environmental practices in organizations (perceived benefits of sustainable environmental manufacturing practices, stakeholder pressure and legislation), while (d) contains the background information of the selected companies (companies ownership, number of employees, ISO certification) and information about the respondents (job position and years of experience). The main issue considered in this instrument development is keeping the questionnaires short and concise to enhance adequate response.The financial performance in this study measures the profitability ratio (ROA, ROI, ROCE, rate of turnover) of the companies. Items of measuring sustainable environmental manufacturing practices were based on pollution prevention practices and product stewardship practices in the companies. Perceived benefits of the implementation of sustainable environmental practice were adapted from[21] Items were used for measuring the stakeholder pressure which was adapted from[16]. Also, the measurement for legislation was adapted from[21] and[20] The items of the instrument were measured on a 7-point likert scale ranging from 1 = strongly disagree, 2 = disagree, 3 = slightly disagree, 4 = neutral, 5 = slightly agree, 6 = agree and 7 – strongly agree. Pilot study was conducted during the development of the questionnaire which includes face and content validity. Experts both academicians and practitioners were consulted for face validity. Thus, the comments of these experts were used in modifying and improving the quality of the questionnaire. However, the only modification done on the questionnaire was only on the format and the rewording of the questionnaire. Hence, the second phase of the face validity received positive comments from the experts and thus, ratified for data collection.Also, reliability test was conducted to examine the internal consistency of the collected data.[22] regards the reliability test as the measurement of the internal consistency and stability of the instruments. This study employed Cronbach’s alpha to interpret the reliability value, thus any value of Cronbach’s alpha above 0.7 is accepted as reliable[23] However, according to[24] a low cronbach’s alpha of 0.6 is also acceptable in an exploratory research. The analysis of the reliability of each variable in this study was computed separately and the summary is shown in Table below. The result shows that all the items have high internal consistency (Cronbach’s alpha ≥ 0.7), and thus reliable. Structural equation modeling (SEM) was employed to analyze the collected data. This was achieved by using Amos 16 to present the results of the goodness of fit.

|

4. Findings

| Figure 1. Revised Model |

|

5. Discussion

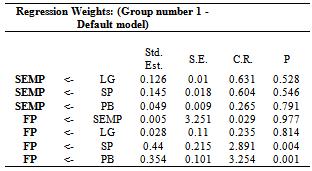

- The findings reveal that stakeholder pressure and perceived benefits are significantly related to financial performance. This reveals the influence of the different stakeholders (government agencies, local communities, trade associations, employees, consumers, customers, environmental organizations, competitors and press media) on the financial performance of the firms thereby supporting the findings of[25]. Also, the benefits expected by the companies from the implementation of sustainable environmental manufacturing practices significantly influence the financial performance of the firms. Such benefits include reduced operating/production costs, increase quality of products, increase in market share and company’s image. This result supports the findings of[18] and[26] which found significant relationship between perceived benefits, environmental management and corporate performance.Additionally, the findings of this study show that there is an insignificant relationship between perceived benefits, legislation, stakeholder pressure and sustainableenvironmental manufacturing practices. This result supports[16] and[17] which established a relationship between stakeholder pressures and environmental practices but differs from the findings of[17] which found a significant relationship.

6. Conclusions

- This study concludes that the factors: stakeholder pressure, legislation and perceived benefits directly influence the implementation of sustainable environmental manufacturing practices and firm performance. Thus, this implies that the pressure exerted by the stakeholders of firms, legislation and the benefits perceived by the company from environmental manufacturing practices drive the implementation of sustainable environmental manufacturing practices in firms and therefore improves the financial performance. This study hereby suggest that future researchers should endeavor to conduct similar research using larger sample size to enhance more generalizable result