-

Paper Information

- Next Paper

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

American Journal of Economics

p-ISSN: 2166-4951 e-ISSN: 2166-496X

2013; 3(1): 12-17

doi:10.5923/j.economics.20130301.03

Host Country Restrictions, Choice of Entry Mode and Japanese Subsidiaries Performance in Developing Countries

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLNorhidayah Mohamad 1, 2, Yasuo Hoshino 1, 3, 4

1Graduate School of Business Administration, Aichi University, 461-8641, Japan

2Faculty of Technology Management & Technopreneurship, Universiti Teknikal Malaysia Melaka, 76100, Malaysia

3Graduate School of Accounting, Aichi University, 461-8641, Japan

4Institutes of Policy and Planning Sciences, University of Tsukuba, 305-0006, Japan

Correspondence to: Norhidayah Mohamad , Graduate School of Business Administration, Aichi University, 461-8641, Japan.

| Email: |  |

Copyright © 2012 Scientific & Academic Publishing. All Rights Reserved.

This paper empirically examines the effects of a host government’s local ownership restrictions, the choice of entry mode and Japanese subsidiaries performance in two selected developing countries namely Malaysia and Thailand that received among the highest Japanese FDI for fiscal years 2003 through 2009. The purpose of this paper is to investigate the influence of host government restriction by using subsidiary’s financial data as the performance indicator from ORBIS database. Our sample consists of 1267 cases. The results reveal that local host government restriction significantly influence the choice of entry mode and subsidiaries performance in the two developing countries.

Keywords: Entry Mode, Japanese Subsidiaries, Financial Performance, Malaysia, Thailand

Cite this paper: Norhidayah Mohamad , Yasuo Hoshino , Host Country Restrictions, Choice of Entry Mode and Japanese Subsidiaries Performance in Developing Countries, American Journal of Economics, Vol. 3 No. 1, 2013, pp. 12-17. doi: 10.5923/j.economics.20130301.03.

Article Outline

1. Introduction

- Foreign Direct Investment (FDI) enable Multinational Corporations (MNCs) get access to larger markets, reducing production cost with cheap labor and other advantages that can provide them with higher profitability and business growth. On the other hands, Foreign Direct Investment (FDI) also provide advantages to the host country on the economy and technology through technology transfer, diffusion of management skills and the exploitation of the international market. Entry mode is one of the important parts in order to go abroad through FDI. There were two familiar type of entry mode known as joint ventures (JVs) and wholly owned subsidiaries (WOS) depend on host countries’ restrictive. Local government restrictions on entry mode were different between countries. Research by[1] on local ownership restriction in Japanese subsidiaries in Asia found that the extent of local ownership restrictions is negatively and significantly associated with the financial performance of WOS and does not directly influence the JVs entry mode. There is still insufficient research on the impact of host governments’ restriction on the performance of foreign subsidiaries. It is very important for MNCs to understand how the host country restrictions affect their subsidiary performance. Clear understanding on the effect of local government restriction may assist the MNCs to make decision on selecting the best host country for their subsidiaries. Therefore, the main purpose of this study is to examine the relationship between the local ownership restrictions towards choice of entry mode and subsidiary performance in two selected developing countries.

2. Literature Review

- In past literature, researchers have mention that host government’s local ownership restriction have influence the choice of entry mode[1],[2],[3]. For developing countries, Reference[2] in his research on ownership patterns of U.S joint venture abroad found that government mandates and political risk perception are crucial than market size. Beamish[4] also state that the developing nation’s more than half percentage cites government restrictions as important factor and only one third indicate the need for local skills workers. Whilst for developed countries, most of the MNCs select the joint venture as entry mode as the need for local partner skills. Only small percentage said that government restrictions were the factor that influences the ownership structures for subsidiaries.Other research by[3] mentions about two type of ownership structure. Firstly was the structure that can minimize the transaction costs of doing business abroad and secondly, the ownership structure are determined by negotiations with host governments, where the outcomes depend on the bargaining power of the firm. In his research results, his found that attractive domestic markets increase the power of host governments.Reference[1] had mention about three argument regarding local ownership restrictions and subsidiary performance. The first argument postulates that local ownership restriction has negative impact on subsidiary performance. Thus, this perspective suggests that a host government’s local ownership policy leads to lower performance. The second argument suggests that host government facilitates a foreign firm’s resource access opportunities by providing a wide range of subsidies and fiscal incentives and protection from competitor within and outside the host country. The last argument suggests that local ownership restriction itself does not affect JVs performance. The assumption is that since most foreign firms have many options of overseas investment opportunities, a decision to invest takes a very careful consideration of the costs and benefits of a particular investment project. Moreover, they also found that local ownership restrictions was differ among countries where Thailand use the general ownership criterion, while Malaysia use combination of general ownership criterion and industry-or project-based restrictions. In short, local ownership restriction can either hinder, facilitate, or do nothing for subsidiary operations in host country can be negative, positive or neutral factor that influence on subsidiary performance. Seems that Thailand implemented the general ownership restriction,[5] found that there is significant difference between Japanese subsidiaries ownership and it performance at the local host country On the other hand, parent financial performance also may influence the performance of their subsidiaries in local host country. The six primary measures of operating performance are the rate of return on shareholder fund (RSHF) or known normally as return on equity (ROE), return on capital employed (ROC), return on assets (ROA), profit margin (PRMA), R&D per operating value (RDOP) and solvency ratio (SOLR). These profitability ratios were used to assess the business ability to generate earnings and at the same time investigate the financial health of companies during a specific period of time.Despite local ownership restriction and parent financial performance, parent characteristic such as international experience and number of local workers also contribute to the success of the subsidiaries. Based on all previous arguments, we propose the following three specific hypotheses:Hypothesis 1a: There is a significant difference in performance between local ownership restriction and choice of entry mode.Hypothesis 1b: In the case of developing countries, JVs entry mode performs better than wholly owned subsidiaryHypothesis 2: Parent financial ratios has significant impact on subsidiary performance in developing countriesHypothesis 3: Parent characteristics are negatively correlated to subsidiary’s performance in developing countries.

3. Methodology

- This study examines the relationship between entry modes, domestic variables, and parent characteristics of Japanese companies, and the attained performance of their subsidiaries. The principal focus of this study is the operating performance of Japanese companies. We applied multiple regression models in this research and the suggested focus was on the performance of the selected MNC subsidiaries.The classification of entry modes was based on the percentage of share ownership of the major shareholders as reported in this database. Firms with over 95% ownership were considered as wholly owned subsidiaries and those below than 95% ownership were considered as majority owned subsidiaries. Therefore, 95% ownership has been used in this research as well to distinguish between wholly owned firms and partnerships.The data for the entry mode and the performance of the subsidiaries was derived from the ORBIS database for fiscal years 2003 through 2009. The criteria for inclusion of firms in the sample were as follows:1. We selected only firms that show all the financial data that we use in this research. The companies that have 80% of missing data were eliminated from the sample.2. We only selected the industry type of business and excluded all the others types of business such as banking and insurance firms. Our final samples include 609 cases for Malaysia and 1085 cases for Thailand. It appears that the financial statement ratios of Japanese subsidiaries in Malaysia and Thailand come from a single database, thus we were able to directly compare these two countries because they use the same accounting principles.

3.1. Dependent and Independent Variables

- Various variables have been used in previous studies dealing with a firm’s performance. According to[6] in their research on determinants of financial performance, they found that financial performance variables include widely used measures embracing levels, growth and variability in profit (typically related to assets, investments or owner’s equity) as well as such measures as market value, assets, equity, cash flow, research & development (R&D), sales and market/book value. Some variables serve as performance characteristics; for example, some studies use sales growth as a performance measure. In addition, all financial return variables were measured in percentage or fraction form such as concentration ratios, market share (%), growth rate (%), advertising/sales ratios, R&D/sales ratios, and ratios of capital investment to a size measure. Reference[7] in their research about strategic performance measurement approaches to explain a firm’s performance found that strategic performance measurement practices are associated with accounting measures such as sales growth. However, in this research, the financial ratios were used to measure the performance of Japanese MNC subsidiaries in Malaysia and Thailand. The measurements consisted of three profitability ratios (ROE, ROA, and PRMA) and one structure ratio (SOLR). For the analysis, a simultaneous analysis of several groups was used using SPSS 18.0 for Windows software. This research consists of nine independent variables, which come from the data of parent companies. The parent company’s data takes into account the parent company’s ROE, ROC, ROA, PRMA, RDOP, SOLR, age and number of workers.

4. Empirical Result

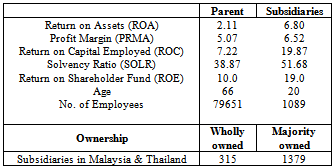

4.1. A Descriptive Comparison of the Samples

|

4.2. Testing for Differences between Local Government Restriction, Entry Mode and a Firm’s Performance

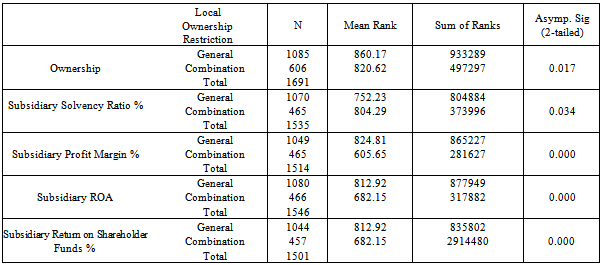

- In this research, the classification of performance was measured by using subsidiary financial data comprised of profitability ratios and structure ratios. Whilst local ownership restrictions were grouped into two categories based on the past research finding by[1]. They found that Thailand use general ownership criterion (General) and Malaysia use industry and project-based restriction (Combination). Therefore, we used these two types of local ownership restriction and group it into “General” and “Combination”. Non-parametric tests were employed to determine if a statistically significant difference existed between ownership and performance in these two countries. The Mann-Whitney test is used to see whether variances exist in different groups. Therefore, if the Mann-Whitney test is significant at p ≤ 0.05, confidence can be gained in the hypothesis that the variances are significantly different and that the assumption of homogeneity of variances has been violated. In the case of developing countries, there were differences between local ownership restriction with entry mode and firm’s performance as shown in Table 2.

|

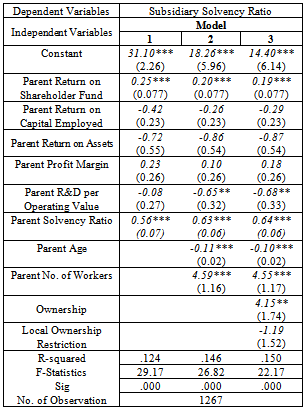

4.3. Multiple Regressions

- Multiple linear regression models with one dependent Y variable:

| (1) |

|

5. Conclusions

- The choice of entry mode and subsidiaries performance has long been a concern of international business scholar. Local ownership restriction in Malaysia and Thailand was vary where Thailand use the general ownership criterion, while Malaysia use combination of general ownership criterion and industry-or project-based restrictions. Analysis from ORBIS database reveals that local ownership restriction has significant influence towards choice of entry mode and subsidiary financial performance in both developing countries. The relationship between ownership and a firm’s performance is an important issue. In the current study, we found that JVs with majority ownership subsidiaries has a better performance than the wholly owned entry mode. The significant ownership results for Japanese subsidiaries in Malaysia and Thailand show that, the form of business will reflect the subsidiary SOLR performance. The significant result for both countries also consistent with[11],[12],[13] that found a significant relationship between ownership and firm’s performance. Therefore, we support the hypothesis 1a and 1b where ownership had significant difference in performance and joint venture entry mode performs better than wholly owned subsidiaries in Malaysia and Thailand. Moreover, the results also reveal that Japanese parent company’s financial performances are significantly influenced the subsidiaries financial performance in Malaysia and Thailand. As mentioned by[14], the contribution of the parent company’s resources, information, adaptation, and flexibility enable the subsidiary to gain more from the parent company and at the same time increase their performance. Moreover, based on the OLI theory, possession of superior intangible and tangible assets from parents to subsidiaries in developing product differentiation to satisfy local market need with R&D activities is a part of the ownership advantages that may enhance the performance of the subsidiary in the host country.In addition, in this paper we have also considered the effect of parent characteristics on the performance of their subsidiaries. For Malaysia and Thailand, parent age indicates a negative significant relationship with a subsidiary’s solvency ratio performance. As the descriptive analysis shows that the age of parent companies was more than half century. At the age, probably the parent companies already passed the mature stage where firms face a slow decline in profitability[9]. This is because competitiveness pressure from new entrants leads to profitability decline for mature firms. It also supports the empirical findings on industry lifecycle, the theoretical model of industry lifecycle and dynamics, and empirical patterns of firm and industry dynamics collectively suggest that the shape of the size distribution should change as an industry ages[10]. Thus, we partially accept the third hypothesis. This study contributes significantly to the development of a general FDI theory by using new financial variables for performance measurement in the case of Japanese subsidiaries in two ASEAN countries from the year 2003 until 2009. However, this study was limited by data reliability and the lack of available data. Even though we tried to consider many variables from the data of parent companies in measuring the performance of subsidiaries, this does not mean that we were able to capture all the data variables. This implies that it is still necessary to use other variables such as investment objectives, and other profitability ratios of parent companies that may affect the success of subsidiaries in foreign countries. Furthermore, only Japanese companies took part in this research. Thus, with the data available to us, our general findings were confined to Japanese firms only. Future research should look into this aspect.

ACKNOWLEDGEMENTS

- This study supported by JSPS KAKENHI Grant Number 21530410, 24530500 and Malaysia Ministry of Higher Education (MOHE).