-

Paper Information

- Next Paper

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

American Journal of Economics

p-ISSN: 2166-4951 e-ISSN: 2166-496X

2012; 2(7): 164-170

doi: 10.5923/j.economics.20120207.02

The Methodology of Economic Costs Influential on Automation of Component Production

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-Text HTML

Full-Text HTMLDarina Matisková

Technical University in Kosice, Faculty of Manufacturing Technologies with seat in Presov, Department of Manufacturing Management, Bayerova, 1, 080 01, Presov, Europa , Slovakia

Correspondence to: Darina Matisková , Technical University in Kosice, Faculty of Manufacturing Technologies with seat in Presov, Department of Manufacturing Management, Bayerova, 1, 080 01, Presov, Europa , Slovakia.

| Email: |  |

Copyright © 2012 Scientific & Academic Publishing. All Rights Reserved.

This article is about determine the optimalization and minimalization of costs from automation production for small and middle enterprices of mathematical methods. The transition from current engineering to the complex automated and highly machanical production is inevitable. The economic aspects on optimalization of components production are nowadays very current issue. At the time of ongoing world economic crisis the most discussed topic in this area as well is the decreasing of the production costs. When cutting conditions and tool durability optimizing, it is necessary to apply certain optimizing criterion within certain restraining conditions. The restrictions are given by technical parameters of a machine, tool, machined material, required quality of machined surface etc. The essential economic criterion is the amount of production cost.

Keywords: Economic Reasons, Production of Costs, Minimalization of Costs, Optimizing, Machine Serviceability

Cite this paper: Darina Matisková , "The Methodology of Economic Costs Influential on Automation of Component Production", American Journal of Economics, Vol. 2 No. 7, 2012, pp. 164-170. doi: 10.5923/j.economics.20120207.02.

1. Introduction

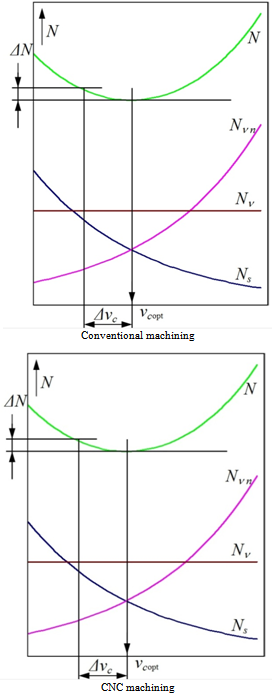

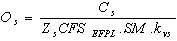

- When considering machining process from the point of efficiency (productivity) production costs are oblivious. Yet, It is applicable exceptionally.In market mechanism it is required to produce a product in such economic conditions so that its sale price be acceptable and attractive. To start thinking about a production process it is necessary to get an idea about its cost structure.When machining, it is important to consider engaging movement of particular machines. At more difficult optimization it is possible to source from single-machine optimization.Optimization of cutting conditions is convenient to realize by a complex calculation whose outputs are optimal values of cutting conditions and durability of a cutting wedge. According to complexity it is necessary to use a computer with appropriate software.Using more expensive production installation the costs raise more rapidly. They reach minimum at higher cutting speed than when utilizing usual machines. Disobedience to this relation leads to sharp rise of production costs when machining using the CNC machines. The basic cost development scheme is in the fig. 1. .(1)When considering machining process from the point of efficiency (productivity) production costs are oblivious. Yet, It is applicable exceptionally.In market mechanism it is required to produce a product in such economic conditions so that its sale price be acceptable and attractive. To start thinking about a production process it is necessary to get an idea about its cost structure.When machining, it is important to consider engaging movement of particular machines. At more difficult optimization it is possible to source from single-machine optimization.

2. Explanation of Methods

- Optimization of cutting conditions is convenient to realize by a complex calculation whose outputs are optimal values of cutting conditions and durability of a cutting wedge. According to complexity it is necessary to use a computer with appropriate software.It is worth to comment that if „universal“ software for optimization usable without an input of a particular company data are commercially offered it is not possible to speak about optimization. The optimization is dependent on particular conditions of every company. The software represents only basic recommendation what cutting conditions to determine. Real optimal values can markedly differ from these cutting conditions.(2), (3), (6)In present, the cutting conditions are mainly chosen from norms that is not optimal. The nature of cutting conditions optimization is to determine optimal values of given conditions (cutting depth –

, underthrust depth – f, cutting speed –

, underthrust depth – f, cutting speed – ) and the optimization of a machine durability.The criterion for minimum costs is the basic optimization criterion in engineering technology. It should be applied on principle.We attempt to describe the criteria for minimum production costs. We shall consider only the costs items that are dependent on cutting conditions. Consequently, total costs may be given by the relation:

) and the optimization of a machine durability.The criterion for minimum costs is the basic optimization criterion in engineering technology. It should be applied on principle.We attempt to describe the criteria for minimum production costs. We shall consider only the costs items that are dependent on cutting conditions. Consequently, total costs may be given by the relation: | Figure 1. Dependence of N production costs and their components on cutting speed . . – costs on machine work, – costs on machine work,  – secondary work costs, – secondary work costs,  – costs to device exchange – costs to device exchange |

| (1) |

- costs to machine labor per an operational section,[€],

- costs to machine labor per an operational section,[€], – costs to machines related to the operational section,[€],

– costs to machines related to the operational section,[€], – costs to exchange or offset of a worn-out device related to the operational section,[€],Individual cost units may be formulated as follows:For labor costs of a machine holds:

– costs to exchange or offset of a worn-out device related to the operational section,[€],Individual cost units may be formulated as follows:For labor costs of a machine holds: | (2) |

are costs to one minute machine labor,[€.

are costs to one minute machine labor,[€.  ],

], – hourly costs to machine operation,[€.

– hourly costs to machine operation,[€.  ],

], – operator´s wages including social and health insurance,[ €.

– operator´s wages including social and health insurance,[ €. ],

], – planned operational costs of a department,[%]

– planned operational costs of a department,[%] - increment shift time, (usually 1, 11-1,15),

- increment shift time, (usually 1, 11-1,15), – machine time,[min.]Hourly costs to machine operation may be formulated:

– machine time,[min.]Hourly costs to machine operation may be formulated: | (3) |

| (4) |

– is the write-off of a machine,[€.

– is the write-off of a machine,[€.  ],

], – a machine price,[€],

– a machine price,[€], – electricity price (middle value of long-term average or educated guess),[

– electricity price (middle value of long-term average or educated guess),[ ],

], – machine operational life in years,

– machine operational life in years, – machine time fund planned in hours per year and shift,SM – shift,

– machine time fund planned in hours per year and shift,SM – shift, – reparation index and machine maintenance index,

– reparation index and machine maintenance index, - index of time-utilization of a machine,

- index of time-utilization of a machine,

| (5) |

are machine operational costs related to one device serviceability,[€],

are machine operational costs related to one device serviceability,[€], – number of the machine exchange related to one operational section (it usually is a number lower than 1).The number of exchanges

– number of the machine exchange related to one operational section (it usually is a number lower than 1).The number of exchanges  can be given by:

can be given by: | (6) |

– the relation of real time or more precisely the working time (when the machine deterioration is obvious) and machine time or the lenght of power run of a machine.Costs to a machine related to a device serviceability can be given for various types of devices as follows:For overall re-sharpening:

– the relation of real time or more precisely the working time (when the machine deterioration is obvious) and machine time or the lenght of power run of a machine.Costs to a machine related to a device serviceability can be given for various types of devices as follows:For overall re-sharpening: | (7) |

is the price of a machine,[€],

is the price of a machine,[€], – depreciated price of a machine,[€],

– depreciated price of a machine,[€], – sharpener´s wages including social and health insurance,[€

– sharpener´s wages including social and health insurance,[€  ],

], – planned annual operational costs of sharpening service,

– planned annual operational costs of sharpening service, – the number of possible machine re-sharpening,

– the number of possible machine re-sharpening, – time of machine sharpening, min,For a machine with replaceable cutting plates that are not possible to be re-sharpened applies:

– time of machine sharpening, min,For a machine with replaceable cutting plates that are not possible to be re-sharpened applies: | (8) |

is the price of a plate,[€],

is the price of a plate,[€], – the price of tool body,[€],

– the price of tool body,[€], – the number of cutting plates on a device,

– the number of cutting plates on a device, – number of cutting edges on a plate,

– number of cutting edges on a plate, – assumed number of plate clamping work whilst machine body serviceability,

– assumed number of plate clamping work whilst machine body serviceability, – index of cutting plates utilization,

– index of cutting plates utilization, - index of machine body maintenance,Approximated values of empirical constant factors of the relation are given in the table 2. Those are statistic data.

- index of machine body maintenance,Approximated values of empirical constant factors of the relation are given in the table 2. Those are statistic data.

|

| (9) |

is the number of possible re-sharpening of a plate.Costs to exchange of a device can be given by:

is the number of possible re-sharpening of a plate.Costs to exchange of a device can be given by: | (10) |

are costs to exchange of a device per,[min],

are costs to exchange of a device per,[min], – wages of a setup man including social and health insurance,[

– wages of a setup man including social and health insurance,[  ],

], – time to exchange a device,[ min],The criterion for minimal production costs can be given (production costs to operational department shall be minimum) by the relation (1).Having substituted the above-mentioned relations into this criterion the optimization criterion to be reached from the point of view of production costs as follows:

– time to exchange a device,[ min],The criterion for minimal production costs can be given (production costs to operational department shall be minimum) by the relation (1).Having substituted the above-mentioned relations into this criterion the optimization criterion to be reached from the point of view of production costs as follows: | (11) |

| (12) |

| (13) |

is the length of machine automatic operation run,[ mm],n- rotational frequency,f – displacement,[ mm]Substitution(13) in(12) results in the criterion equation:

is the length of machine automatic operation run,[ mm],n- rotational frequency,f – displacement,[ mm]Substitution(13) in(12) results in the criterion equation: | (14) |

| (15) |

| (16) |

| (17) |

| (18) |

are total production costs per a work-piece,[€],

are total production costs per a work-piece,[€], – production costs to i- operational section,[€],

– production costs to i- operational section,[€], - costs to a special device necessary for production of a given work-piece,[€],n – number of produced pieces,

- costs to a special device necessary for production of a given work-piece,[€],n – number of produced pieces, – number of operational sections within one work-piece,Costs to secondary work:

– number of operational sections within one work-piece,Costs to secondary work: | (19) |

– costs to secondary work,[€],

– costs to secondary work,[€], – unit secondary time,[ min.],Rate costs:

– unit secondary time,[ min.],Rate costs: | (20) |

are rate costs,[ €-1],

are rate costs,[ €-1], – rate time with shift time over plus,[ min]Criterion of minimum production costs can be also given by the method of hourly operational costs. (11), (12)Fixed costs whose share in total costs continually raises are just those unwelcome costs that burden production. This is one reason why it is success to produce with optimal capacity employment.For practical utilization it is appropriate to express the capacity utilization in time units (hours, norm hours). When formulating the cost model of a production workplace (of a machine) other advantageous properties of this method can be used.1. Possibility of division (decomposition) hourly overhead lump sum into two individual units as follows:- Into hourly overhead lump sum of joint expenses (

– rate time with shift time over plus,[ min]Criterion of minimum production costs can be also given by the method of hourly operational costs. (11), (12)Fixed costs whose share in total costs continually raises are just those unwelcome costs that burden production. This is one reason why it is success to produce with optimal capacity employment.For practical utilization it is appropriate to express the capacity utilization in time units (hours, norm hours). When formulating the cost model of a production workplace (of a machine) other advantageous properties of this method can be used.1. Possibility of division (decomposition) hourly overhead lump sum into two individual units as follows:- Into hourly overhead lump sum of joint expenses ( )- Into hourly overhead lump sum of a production workplace (a machine) (

)- Into hourly overhead lump sum of a production workplace (a machine) ( )2. Possibility to decompose each hourly overhead lump sum as the sole number into more partial generic cost items that enables to separately observe individual impacts on hourly overhead lump sum.(14), (15)The first property enables to present overhead costs to particular activities within the production process with the help of hourly overhead lump sum as the total of two separable components. Total value of hourly overhead lump sum is consequently given by the total of both components. While

)2. Possibility to decompose each hourly overhead lump sum as the sole number into more partial generic cost items that enables to separately observe individual impacts on hourly overhead lump sum.(14), (15)The first property enables to present overhead costs to particular activities within the production process with the help of hourly overhead lump sum as the total of two separable components. Total value of hourly overhead lump sum is consequently given by the total of both components. While  will be the same for all workplaces within a single organizational unit (center, operational department, etc.) to which joint expenses are related, the

will be the same for all workplaces within a single organizational unit (center, operational department, etc.) to which joint expenses are related, the  value will be unique for each workplace (machine, set of machines).The second property allows the distinction of general expenses from the point of generic e.g. for example to components of write-offs, rent (leasing), wages, energy costs, overhead material etc. It is crucial to choose such a classification in concrete application that would respond to the situation given. It is necessary to focus on main items sensible that the less important ones can possibly be joint together. It means for example that while the significant part of a production device will not be true but rented (leased) than that item has to appear in the HRP decomposition. While the production device is true it is useless to mention the item.The simple solution is not to divide general expenses into two parts i.e. joint expenses of a department and costs of a workplace but leave it as the average value of hourly overhead lump sum designed on the basis of share of total of all overhead costs within a department and total department capacity. It is a simple solution that can be appropriate as the first stage of transition from a calculation through an extra charge to a calculation with the usage of the hourly overhead lump sum method.By this simplification the influence of individual factors is covered and their impact is not clear in the total calculation.Essential matters for the working process optimization are a solid analysis of on what the value of expense units depends. It is determining just because the information enables to manage the working process effectively. From the point of preceding ideas, there is an alternative coming out to determine minute costs to machine work (relation 2):

value will be unique for each workplace (machine, set of machines).The second property allows the distinction of general expenses from the point of generic e.g. for example to components of write-offs, rent (leasing), wages, energy costs, overhead material etc. It is crucial to choose such a classification in concrete application that would respond to the situation given. It is necessary to focus on main items sensible that the less important ones can possibly be joint together. It means for example that while the significant part of a production device will not be true but rented (leased) than that item has to appear in the HRP decomposition. While the production device is true it is useless to mention the item.The simple solution is not to divide general expenses into two parts i.e. joint expenses of a department and costs of a workplace but leave it as the average value of hourly overhead lump sum designed on the basis of share of total of all overhead costs within a department and total department capacity. It is a simple solution that can be appropriate as the first stage of transition from a calculation through an extra charge to a calculation with the usage of the hourly overhead lump sum method.By this simplification the influence of individual factors is covered and their impact is not clear in the total calculation.Essential matters for the working process optimization are a solid analysis of on what the value of expense units depends. It is determining just because the information enables to manage the working process effectively. From the point of preceding ideas, there is an alternative coming out to determine minute costs to machine work (relation 2): | (21) |

hourly absorbed lump sum of joint expenses,[

hourly absorbed lump sum of joint expenses,[  ],

], – hourly overhead lump sum of a production department (a machine),[

– hourly overhead lump sum of a production department (a machine),[  ]By analogy for minute expenses to exchange of a machine (relation 10):

]By analogy for minute expenses to exchange of a machine (relation 10): | (22) |

| (23) |

is optimal serviceability of a machine from the point of production costs,[min]m- empiric constant from the Taylor´s relationDetermination of optimal serviceability does not depend on cutting conditions, but leads to simplification of cutting conditions optimization. After that, it relates usage of gradual way of optimal cutting conditions setting. The procedure does not lead to optimal values.Optimization of cutting conditions is always realized according to a optimization criterion within a restriction (restrictive conditions given by production conditions).Working process is always limited by a certain group of restrictive conditions. It is possible to formulate these conditions mathematically as in equations. The exception is the complex Taylor´s relation that is an equation.Restrictive conditions are given by a working machine (its performance, cut-off twisting moment of retentive unit, cut-off size of cutting power elements, range of twists and offsets), a device (cutting material, geometry, surface roughness), material of a work-piece, cutting environment, requested qualitative parameters. For complex optimization calculation of cutting conditions mostly linear parametric programming was used. The mathematical apparatus comes out of linear or linearized restricting conditions. In connection with the development of production technology the utilization of non-linearized restricting conditions arose. It related for example continuous, non-linearized restricting conditions from the point of twisting moment (twist of a work-piece in a chucking device) and a bending moment (extraction of a work-piece one-sidely attached in a chucking device) by machines with high rotational frequency. Apart from the continuous non-linearized restricting conditions more and more non-continuous restricting conditions occur. Before all, it relates different characteristic of working machines performance. Mathematical methods of cutting conditions optimization with these restricting conditions lead to interval optimization tasks. For example, two restricting non-linearized conditions are mentioned.For linear process of performance characteristic for performance holds the following line-equation:(14)

is optimal serviceability of a machine from the point of production costs,[min]m- empiric constant from the Taylor´s relationDetermination of optimal serviceability does not depend on cutting conditions, but leads to simplification of cutting conditions optimization. After that, it relates usage of gradual way of optimal cutting conditions setting. The procedure does not lead to optimal values.Optimization of cutting conditions is always realized according to a optimization criterion within a restriction (restrictive conditions given by production conditions).Working process is always limited by a certain group of restrictive conditions. It is possible to formulate these conditions mathematically as in equations. The exception is the complex Taylor´s relation that is an equation.Restrictive conditions are given by a working machine (its performance, cut-off twisting moment of retentive unit, cut-off size of cutting power elements, range of twists and offsets), a device (cutting material, geometry, surface roughness), material of a work-piece, cutting environment, requested qualitative parameters. For complex optimization calculation of cutting conditions mostly linear parametric programming was used. The mathematical apparatus comes out of linear or linearized restricting conditions. In connection with the development of production technology the utilization of non-linearized restricting conditions arose. It related for example continuous, non-linearized restricting conditions from the point of twisting moment (twist of a work-piece in a chucking device) and a bending moment (extraction of a work-piece one-sidely attached in a chucking device) by machines with high rotational frequency. Apart from the continuous non-linearized restricting conditions more and more non-continuous restricting conditions occur. Before all, it relates different characteristic of working machines performance. Mathematical methods of cutting conditions optimization with these restricting conditions lead to interval optimization tasks. For example, two restricting non-linearized conditions are mentioned.For linear process of performance characteristic for performance holds the following line-equation:(14) | (24) |

and q are constants.For the process of performance it is possible to derive for example for turning operation a restricting condition as follows:

and q are constants.For the process of performance it is possible to derive for example for turning operation a restricting condition as follows: | (25) |

| (26) |

is chucking power influencing the jaw,[N],

is chucking power influencing the jaw,[N], - chucking power influencing the jaw, yet: n=0,[N],

- chucking power influencing the jaw, yet: n=0,[N], - constantThe

- constantThe  constant can be drawn from the details of a manufacturer as the decrease of chucking power at maximum rotational frequency of a spindle.

constant can be drawn from the details of a manufacturer as the decrease of chucking power at maximum rotational frequency of a spindle.

|

| (27) |

– tightening average,[ mm],

– tightening average,[ mm], Rubbing index between a jaw and a work-piece,After substitution and modification there are restrictive conditions as follows:

Rubbing index between a jaw and a work-piece,After substitution and modification there are restrictive conditions as follows: | (28) |

is determined with high level of security. Next, it is possible to monitor total deterioration of a machine or of parts of a cutting edge as well. Monitoring of cutting process is realized by appropriate sensors whose outputs are processed using appropriate logic.

is determined with high level of security. Next, it is possible to monitor total deterioration of a machine or of parts of a cutting edge as well. Monitoring of cutting process is realized by appropriate sensors whose outputs are processed using appropriate logic.3. Conclusions

- Only automation of technological process,implementation of automated production machine allows to significantly increase the quality of production and its productivity and to decrease the number of service attendants and to minimalize of all costs. This article is about engeneering and economics tasks in the theory of reliability are connected with the choice of such constructional, technological and operating parameters of machines, that would provide their high technical economical indicators with considering their operational reliability. The first task is solved especially on the theoretical level and it results in working out mathematical dependancies of reliability indicatorsdepending on technological, constructional, structural and operating indicators of machines with regard to externalities. The process of working out such dependancies is dificult because until now the qualitative indicators of reliability have been evalueted by statistical methods.

References

| [1] | Akinwumiju, J.A. & Patwari, A.S. (1990) Statistical Analysis of population Data for Educational Planning in Nigeria. Faculty of Education, University of Ibadan, Nigeria 10-24. |

| [2] | BERGELIS, A.: Impact of collaborative manufacturing engineering on production variety and efficiency. 10th International Conference: New Ways in Manufacturing Technologies 2010, Prešov, pp. 95-102, ISBN 978-80-553- 0441-0 |

| [3] | Bonin, J. P., Putterman, L., Economics of Cooperation and the Labor-Managed Economy, Harwood Academic Publisher, USA, 1987. |

| [4] | GAŠPÁR, Š. – MAŠČENIK, J. – PAŠKO, J.: The effect of degassing pressure casting molds on the quality of pressure casting. In: Advanced Materials Research. Vol. 428 (2012), p. 43-46. - ISSN 1022-6680 |

| [5] | HIRANO, H. : 5 Pillars of the visual workplace. Productivity Press, Portland, Oregon, 1998. |

| [6] | HOSHI, T. : High productivity machining research in Japan. Journal of Applied Metal Working 4 (3), 1986, pp. 226-237 |

| [7] | HRICOVÁ, R.: Application of simulation means in computer aid of manufacturing systems control. In: TSO 2009 Proceedings - New Trends in Technical Systems Operation, 9. ročník, TU Košice, KPVP Prešov, 5. -6. novembra 2009, str. 114/117. ISBN 978-80-553-0312-3 |

| [8] | Ireland, N. J., Law, P. J., The Economics of Labor- Managed Enterprises, St. Martin’s Press, USA, 1982. |

| [9] | LUXHOJ, J, T., RISS, J, O., THORSTEINSSON, U. : Trends and perspectives in industrial Maitenance Management. Journal of Manufacturing Systems vol. 16, 6/1997 |

| [10] | MÁDL, J. : Computer – Aided determination of machining conditions. Science Report CEEPUS, Kielce 2010, pp.97-103. ISBN 978-83-88906-56-5 |

| [11] | MÁDL, J., KVASNIČKA,J. : Optimalizace obráběcího procesu. Praha, ČVUT, 1998, 168 |

| [12] | MODRÁK, V.: Functionalities and integration possibilities of manufacturing execution systems, 2009. In: Annals of Faculty of engineering Hunedoara - journal of engineering. Vol. 7, no. 1 (2009), p. 51-56. - ISSN 1584-2665 , http://annals.fih.upt.ro/ANNALS-2009-1.html.. |

| [13] | Moore, J. L. (1994) Research methods and data analysis Hull: Institute of Education, University of Hull UK. October; 9-11. |

| [14] | MURA, L. : The network approach of internationalization – study case of SME segment. In: Scientific Papers of the University of Pardubice – Series D, No. 19, Vol. XVI č. 1/2011, s. 155-161, ISSN1211-555Xhttp://www.upce.cz/fes/veda-vyzkum/fakultni-casopisy/scipap/posledni-obsah.pdf |

| [15] | Oppenheim, A N. (1992) Questionnaire design, interviewing and attitude measurement; London & New York: Pinter Publishers, 70 -72. |

| [16] | Pal, D., White, M. D., “Mixed Oligopoly, Privatization, and Strategic Trade Policy”, Southern Economic Association, Southern Economic Journal, vol. 65, no. 2, pp. 264-281, 1998. |

| [17] | Putterman, L., “Labour-Managed Firms”, In: Durlauf, S. N., Blume, L. E. (eds.), The New Palgrave Dictionary of Eco-nomics, Volume 4, Palgrave Macmillan, UK, pp. 791-795 |

| [18] | RAGAN, E., FEDÁK, M., OLEJÁR, T.: Analysis of the switchover point and die temperature influence on injection time with using Cad-cae systems 2011. In: Annals of Faculty of Engineering Hunedoara. Vol. 9, no. 2 (2011), p. 225-228. - ISSN 1584-2665 :http://annals.fih.upt.ro/pdf-full/2011/ANNALS-2011-2-45.pdf... |

| [19] | SEBEJ, P. : The resources exploitation non-parametric statistical tests on the evaluation tendency be accounted / Peter Šebej - 2005.In: Aplimat. Part 2. - Bratislava : STU, 2005 S. 537-543. - ISBN 809692642X |

| [20] | SEBEJ, P., HRUBINA, K., Wessely, E. : Creation of production planning using the mathematical model and multi-criterion optimalisation / P. Sebej, K. Hrubina, E. Wessely - 2004.In: Annals of DAAAM for 2004. - Vienna : DAAAM International, 2004 P. 413-414. – ISBN3901509429 |

| [21] | Stephan, F. H. (ed.), The Performance of Labour-Managed Firms, Macmillan Press, UK, 1982. |

| [22] | Vasilko, K., Bokučava, G.: Technológia automatizovanej strojárskej výroby.Bratislava, ALFA, 1991, 275 s., ISBN 80-05-00806-6 |

| [23] | VASILKO, K.: Analysis of the Impact of Cutting on Machining Process, Manufacturing Engineering, issue 1, year IX, 2010, pp 5-9 |

| [24] | World Bank, 2001. Global Economic prospects. Washington. D.C. |

| [25] | Wu, Y. and Zeng, L., 2008. The Impact of Trade Liberaliza-tion on the Trade balance in Developing Countries, IMF, Working Papers No.WP/08/14. |