-

Paper Information

- Next Paper

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

American Journal of Economics

p-ISSN: 2166-4951 e-ISSN: 2166-496X

2015; 5(2): 278-284

doi:10.5923/c.economics.201501.36

Past Performance Evaluation is the First Step toward the Future: A Case Study of a Performance Management System in a Malaysian Multi-National Company

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLRaemah Abdullah Hashim1, Zahidah Akmal binti Ghazali2, Azahari Jamaludin3

1OUM Business School, Open University Malaysia

2Business School, University Utara Malaysia

3Faculty of Business and Finance, Twintech International University College of Technology

Correspondence to: Raemah Abdullah Hashim, OUM Business School, Open University Malaysia.

| Email: |  |

Copyright © 2015 Scientific & Academic Publishing. All Rights Reserved.

Many studies have shown that performance management systems (PMS) have positive impact if it is properly organized and implemented in the organization. Basically, the PMS is designed to address the needs of an organization to measure and monitor employees’ performance on continuous basis, and to make the system work well the involvement from all major stakeholders especially the future users of the system is a must. In addition, the PMS will become more effective when tying rewards to the results of a performance review. But, caution there could be resistance at the early stage of the adoption however the significance benefits gained from the PMS in long run will be translated into better rewards for its overall population and can act as a catalyst to behavior change within the organization. The sole purpose of this research is to discuss the institutionalisation of the Performance Management System (PMS), specifically the appraisal process in a Malaysian multinational corporation (MNC). The research approach used an exploratory case study method via document review, informal conversations and observation. In addition, the study will also address the issues faced by the MNC and its subsidiaries in this regard as well.

Keywords: Performance management system, Employee performance, Appraisal process, Key performance indicators

Cite this paper: Raemah Abdullah Hashim, Zahidah Akmal binti Ghazali, Azahari Jamaludin, Past Performance Evaluation is the First Step toward the Future: A Case Study of a Performance Management System in a Malaysian Multi-National Company, American Journal of Economics, Vol. 5 No. 2, 2015, pp. 278-284. doi: 10.5923/c.economics.201501.36.

Article Outline

1. Introduction

- What is a Performance Management System (PMS)? Performance management is a continuous process of identifying, measuring and developing the performance of individuals and teams and aligning their performance to organization goals [1]. As such, employee’s identified objectives are perfectly linked to organization main goals. If PMS is properly organized and implemented its will provide a systematic way of analysing and measuring the employees current performance. Even though there is no specific model of performance management but a review of literature suggests that there are several elements normally present such as Objective-setting; Performing and evaluating; and Performance review [2]. And the process is typically cyclical and in an ongoing manner [3]; [4]. Typically in big organizations, the achievement of goals is dependent on the employees achieving their individual goals. As such, PMS is a suitable tool to be linked with the organization’s business strategies [5].In order to ensure the effectiveness of PMS, several steps are best observed when planning and implementing the system including: (i) Prerequisite Stage: knowledge of the organization’s mission, strategic goals and the job in question [6]; (ii) Performance Planning Stage: joint discussion between manager and employee in setting individual goals; (iii) Performance Execution: tracking of employee’s performance through work observation and provide appropriate ongoing feedback. [7]; (iv) Performance Assessment: evaluating behavior or performance displayed throughout the appraisal period; (v) Performance Review: summarizing the employee’s contributions over the entire appraisal period; and (vi) Performance Renewal and Re-contracting. The research approach for this study was an exploratory case study method via document review, informal conversations and observation. In addition, this study focused on the performance management system adopted by the MNC, the implementation in its subsidiaries, the issues faced by the MNC and its subsidiaries.

2. The Company Background

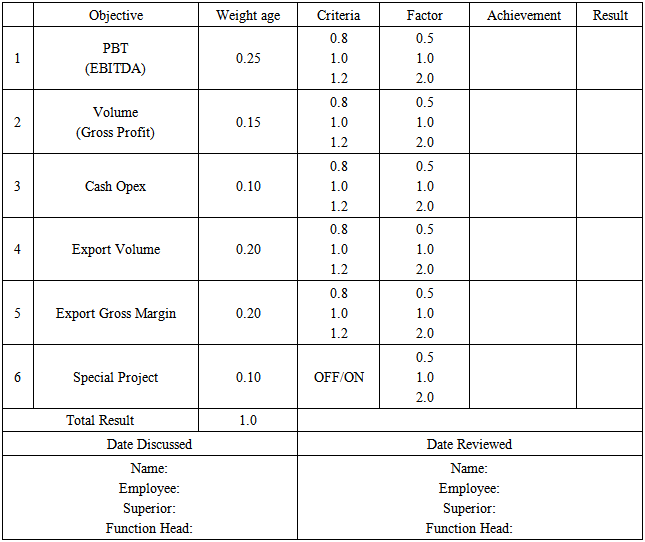

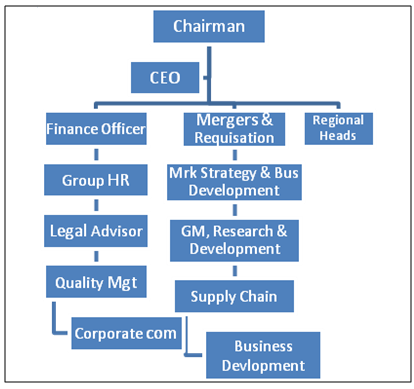

- Phoenix’s (not a real company name) is a multinational corporation (MNC) which was established in 2008. The company headquarters is in Kuala Lumpur, Malaysia. The company has been actively in operations in 20 countries with employees of more than 25 nationalities. The business structure is as in Figure 1. Currently, the company has several manufacturing plants scattered across five continents. As a result, the company has adopted different human resource management (HRM) practices including different PMS. Therefore, there were no uniformed policies on how annual increment and bonuses were rewarded. In 2009, the company Human Resource Department introduced the Short Term Incentive Plan (YIP) as a tool to identify work objectives and to measure the performance of its managerial level employees (see Table 1). However, YIP only measures the company overall financial performances and hard targets.

|

| Figure 1. Business Reporting Structure |

|

3. Implementation Problem

- Firstly, the problem that occurs in 2012 with regard to the credibility of the appraisal process and it result. Amidst protests from employees who have been receiving uniformed salary increment tied only to company’s performance and not individual performance. Therefore, the Human Resources (HR) department has requested all employees to complete the YIP form which defines their key performance indicators (KPI) and also their attributes appraisal form. All the forms were submitted on time to the HR department for discussion in the calibration meeting and to deliberate the top 30% and bottom 10% of the population in finalizing ratings for each employee. Among the critics was on top-down setting targets such as the company financial performances. For example, the earnings before interest, tax, amortization and depreciation (EBITDA) and net operating profit were too high and at the same time the employees do not have full control of its performance. On the other hand, employees may have some influence on operational expenses (OPEX) and operating cash flow by spending prudently but probably had little or no control on capital expenditure (CAPEX) plans. In addition, some support functions such as finance, human resources and administration also struggle to define objective targets as their work performance was difficult to be quantified or measured. Further, the feedback from for example from the Latin America operation’s protested against individualistic rating and insisted that whatever success achieved was always because of teamwork. There were also complaints from the Asia region operations’ that since their employee population had gone through dismissals and replacement hiring, there were no poor performers to fit into the bottom 10%.There are also some questions on how Phoenix’s regional functional heads and employees were being evaluated when their role were essentially providing service and consultation. Whilst YIP may be able to identify their specific achievement and the performance appraisal evaluated their leadership competencies and behaviors, both tools did not provide an indication on whether they brought any value to the country’s operations.When the system continued in the following year in 2013, it was the top management’s turn to question the anomaly found in actual rewards paid. There were some employees who had received the Yearly Incentive Plan (YIP) bonus payment higher than company-average but scored not as good in their final rating, hence receiving average increment. Conversely, there were employees whom the managers unanimously rated ‘1’ as excellent on behavioral attributes but did not receive good YIP bonus payment because he failed to achieve some hard targets. Basically, the strongest criticism against the system, however, was more on the use of forced ranking. There were heated arguments when manager started pushing down employees rating and telling their staffs that they had proposed for a higher grade but the staff’s rating was relegate after the calibration meeting which caused unhappiness to those who were promised higher rating by their manager. The top management came back with the explanation that even in the Olympics sporting event where the best of the best converges, there would still be the gold medalist and the one that came last. It is also illogical to say that each and every person would put equal amount of effort in a team project – there would always be someone who has done more than the next person. However, the HR department noted that the forced ranking did not seem to apply. But, the system continued for another year. Secondly, in the same year, 2013, the HR department introduced the Balanced Scorecard (BSC) for management committee members i.e. direct reports of Group Chief Executive Officer (CEO) such as the Group Chief Financial Officer, Head of Group HRM and all Regional Business Unit Heads. Once the corporate BSC was finalized at the business planning stage, these objectives were then further cascaded to function heads and business unit heads who then set the individual key performance indicators (KPIs) with the respective staff using the YIP tool at the beginning of the financial year. This is done at all levels from non-executive up to top management. The performance appraisal process was initiated through a session referred to as the ‘mid-year performance review’. The managers were required to review the progress of YIP, KPI achievements with their respective employees and also to provide feedback and coaching to keep the employees’ performance on track. The full-year performance appraisal will take place at the end of the financial year. Employees will perform self-appraisal using a performance appraisal form to evaluate their achievement. They then need to submit the appraisal form to their superior for further discussion and agreed upon the final evaluation. They will also discuss any intervention plans to close the performance gaps, if any. At the end of the session, the manager will propose an overall rating to the employee such as Rating ‘1’ (Excellent), ‘2’ (Very Good), ‘3’ (Good) and ‘4’ (Poor). Most of the time, managers had wanted to differentiate those rated ‘3’ as this will form the larger group, there were some who were performing well but not good enough will to be rated “2” and those who just meet expectations but not performing poor enough will be rated “4”. For those group that falls in Rating 3, the company introduced options for managers to rate employees into categories: 3H=High, 3S=Solid, 3L=Low. The proposed rating for each employee will then be compiled by Human Resource department and brought for discussion at the ‘People Development Committee Meeting’. The ‘People Development Committee Meeting’ so called Forum will discuss the rating distribution amongst a class of employees and performance ratings were challenged or calibrated. Several Forums were held at different levels to discuss the different groups of employee. For example, the performance ratings for managers were discussed in a separate Forum held by senior managers where the performance of one manager was benchmarked against the others. The Forum seek to moderate any halo/horn effect or other elements of bias that inherent in performance appraisal and calibrate the performance rating distribution for the whole company. The distribution was typically as follows: Rating 1 = 10%; Rating 2 = 20%, Rating 3 = 60% and Rating 4 = 10% of the population in each group of employees. The final eventual rating will determine the rewards, namely the salary increment to be awarded to the respective employee.The input obtained on any intervention plan to close the performance gaps of individual employees will be used by the HR department to determine the training and development needs for respective employee. The major criticism of the system had been that the cascaded BSC targets such as financial performances were too high and employees did not have full control of its performance. Only 60% of the KPIs total weight was allocated to individual targets. There was also strong criticism that YIP did not stimulate better sales growth due to the way it rewards sales personnel. The stretched target required a sales employee to reach 120% of his target before being eligible of increased reward (multiplying factor of 2) but does not pro-rate the multiplier if they achieved results in between. The effect was that once a sales person reaches his 100% target, he will not do anything more especially if the stretch target is too challenging as he will still receive the reward for meeting 100% if his achievement just falls short of 120%.Finally, from its pilot implementation in Asia and later globally, often there were cries from various regions and country subsidiaries on the PMS that “one size does not fit all’. A single performance appraisal format may not be suitable to be used in some countries for various reasons such as difference in business approach and emphasis, union agreement or local labor legislations or even cultural belief on performance and reward peculiar to each country.

4. Solutions for PMS Improvement

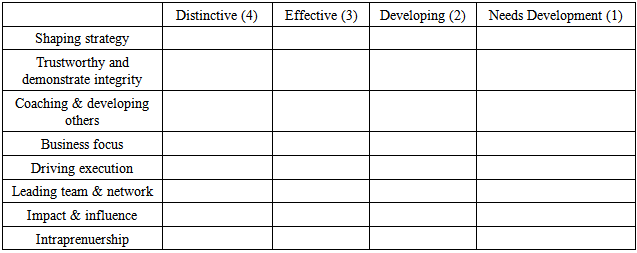

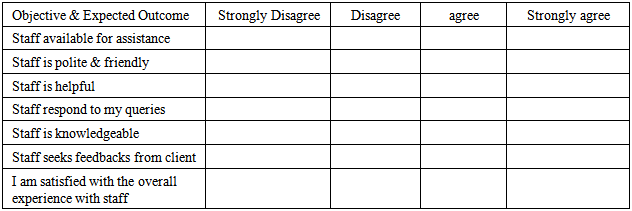

- Performance management system is an ongoing process that includes setting and aligning goals, coaching and developing employees, providing informal and formal feedback to performance linked to recognition and rewards [6]. Further, the PMS tools and process must be valid, reliable, and acceptable. As such, the PMS may benefit from the following improvements:Management by Objectives (MBO) Currently, the company set the objectives, evaluated and rewarded using the YIP framework which was essentially a method of management by objectives (MBO). MBO only works effectively if managers and employees commit to the process in setting employees objectives. However, more often than not, the top-down approach in Phoenix alienates the achievement of these objectives. Employees could not relate and do not have enough influence especially to the financial numbers however, it was recognized that the overall performance of the company should be ‘shared’ by all employees. Therefore, it is acceptable for the company to apportion 40% weight of the total bonus payment based on company performance. The remaining 60% KPI should be set according to the individual’s expected contribution towards achieving the corporate goals. In order to overcome the issue of ‘freeloaders’ that is employees who rides on the performance of others, it is better to emphasis on individual KPI in order to specify what is expected from that particular employee. With clear objectives, employee will know how he will be measured and what he needs to do in order to contribute to the achievement of the bigger corporate objectives. A clear job analysis which defines the roles and responsibilities of each employee is a prerequisite for this. Therefore, the company has to ensure that each and every employee has a definitive job description.To address the deficiency of YIP in managing the performance of sales personnel, the YIP framework must be modified slightly for this group and those who depends on incremental performance, for example the plant personnel who works on volume and productivity. The YIP result calculation should allow for results in between minimum 80% achievement and the 120% stretched target to be recognized on pro-rata basis. This would drive the employees to still push as best as they can even after achieving 100% target as they will be rewarded proportionately to their achievement. This modification, however slight, may make the difference required for the company to nurture the high-performing culture.360° Evaluation for Headquarters and Regional PersonnelPerformance should be measured accurately so that the employees know where they have to improve. In the case of regional managers who provide support and direction to the country personnel, it is perhaps best to implement a simple 360o evaluation to supplement their performance evaluation. This method had been implemented by the Asia regional function heads in Phoenix but is not applied elsewhere in the organization. This team used a simple feedback tool which requires feedback from country CEOs and employees who deal with the regional managers on their responsiveness and knowledge (see Table 3). It is suggested that this should also be used for managers in the headquarters who deal with regional managers and sometimes, directly with country personnel in order to determine their effectiveness.

|

5. Case Study Evaluation

- The above case study suggests that performance management is a continuous process of identifying, measuring and developing the performance of individuals and teams and aligning their performance with the organization’s goals. There are several issues identified pertaining the following:a) Objective-setting: employees have no real control or influence over cascaded corporate targets and also difficult to set targets for service functions;b) There were issues in the use of forced ranking method. Where good-performing employees miss out on good rating when the ‘quota’ has been exhausted. c) Anomaly of bonus payment against performance appraisal rating as bonus is paid against achievement of hard targets (YIP);d) Claim by certain country subsidiaries that reward differentiation promotes individualistic target achievements rather than teamwork;e) Contention that the rigid YIP mechanism and behavioral appraisal do not stimulate sales growth and value creation in the business;f) The tools used do not reflect the effectiveness of services and consultancy provided by regional managers to the country subsidiaries;g) Use of standard YIP and performance appraisal form is unrealistic because ‘one size does not fit all’.In order to address the above PMS issues the company may consider making the following enhancements to its current system:a) To ensure that the balance 60% of KPIs are focused on individual KPIs to avoid ‘freeloaders’;b) To modify the performance tools to fit the job. For example, sales and plant personnel to be rewarded proportionately when they exceed 100% achievement;c) In continuing the use of ranking distribution, the allocation for each level of performance should be relaxed to reflect actual performance level within the organization;d) Consider the use of 360o evaluation to supplement the performance evaluation of regional managers on their work effectiveness;e) Top management’s must make time and seriously discuss employee’s performance during the calibration meeting. f) Managers must be trained as evaluators and encouraged to use the coaching form as critical incident records;g) Use performance matrix for rewards i.e. bonus and increment and ensure significant difference in reward between different performance ratings;h) Allow the subsidiaries to determine their operational objectives as long as they are in line with the organizational goals.

6. Conclusions

- The PMS must be designed and aligned with the needs of an organization. This can be done thorough consultation with the company major stakeholders. In addition, feedback from all parties is an important element that should be incorporated in the PMS. Furthermore, PMS is an important management tools that can have positive outcome for the organization when done properly [15]. Tying rewards to the results of a performance review would make an organization more efficient and effective. New rules and routines will not be institutionalized if the new system challenges the prevailing one. There could be resistance to the initial coercive adoption of proper PMS process and structure. However, the benefits of increased in business performance can be a catalyst to behavioral change within the organization. As with many PMS which has many weaknesses, Phoenix continues to enhance and tailor its PMS from time to time to drive the desired behavior necessary to support its business objectives.