-

Paper Information

- Next Paper

- Previous Paper

- Paper Submission

-

Journal Information

- About This Journal

- Editorial Board

- Current Issue

- Archive

- Author Guidelines

- Contact Us

American Journal of Economics

p-ISSN: 2166-4951 e-ISSN: 2166-496X

2015; 5(2): 119-127

doi:10.5923/c.economics.201501.12

Exports as a Driving Factor of Structural Changes in the BRICS Economies: 1995 – 2012

Abstract

Abstract Reference

Reference Full-Text PDF

Full-Text PDF Full-text HTML

Full-text HTMLAleš Kocourek

Department of Economics, Faculty of Economics, Technical University of Liberec, Czech Republic

Correspondence to: Aleš Kocourek, Department of Economics, Faculty of Economics, Technical University of Liberec, Czech Republic.

| Email: |  |

Copyright © 2015 Scientific & Academic Publishing. All Rights Reserved.

The aim of this article is to shed some light on the structural changes that have taken place during the last two decades in the five emerging markets forming the BRICS grouping. Author also tends to discuss the consequences of these changes for the grouping as a whole and for its individual members. Individual shares of nine major industries on the value added and on exports of each of the BRICS countries were calculated for each year of the period 1995 – 2012, so that then the methods of time series analysis could be applied. The results show a shift from primary manufacturing and from production of merchandise with low added value, to more sophisticated goods. In agriculture, hunting, forestry, fishing, electricity, gas, and water supplies, transport, storage, communication, public administration, education, health, and other service activities, the driving force of the restructuring is formed by the domestic customers of the five BRICS emerging markets. In the sectors of mining, quarrying, and manufacturing the foreign demand for exports plays a crucial role affecting the output of these industries. Weaker impact of exports was identified also in construction, financial intermediation, real estate, renting, and other business activities.

Keywords: BRICS, Export, Gross value added, Industry, Restructuring

Cite this paper: Aleš Kocourek, Exports as a Driving Factor of Structural Changes in the BRICS Economies: 1995 – 2012, American Journal of Economics, Vol. 5 No. 2, 2015, pp. 119-127. doi: 10.5923/c.economics.201501.12.

Article Outline

1. Introduction

- Since 2001, when economic expert of the investment bank Goldman Sachs, Jim O’Neill [12] coined the acronym BRIC for the first time, the rapidly growing countries of the world, Brazil, Russia, India, China, and since 2011 also South Africa, have experienced a dramatic development which can be hardly described as stable or fluent [7]. From more or less a journalistic label with indistinctive common economic content of the potentially world’s most successful emerging markets, the BRICS grouping has been continuously transforming itself into one of the most important players in the global policy and economy. Together the five countries represent a quarter of the world area, 40% of the world population, 20% of global GDP, and 16% of the world international trade in goods and services. All the BRICS members are connected by the disappointment from being permanently marginalized within the system of international relations and by their endeavor to transform it (especially the UN Security Council, but also the World Bank Group and the International Monetary Fund) or to rebuild it from the ground (founding a joint development bank, creating a reserve fund for mutual support of the national currencies,planning a monetary union).Nevertheless, the BRICS countries represent quite divergent opinions on a number of issues (be it the civil war in Syria, the global climate change, the territorial ruptures between China and India, the fear of South Africa from growing impact of China in the “Black Continent”, Chinese economic expansion to Middle East and eastern Russia, Russian political intentions in Ukraine, or growing competition on the global commodity markets).The aim of this article is to shed some light on the structural changes that have taken place in these five emerging markets during the last two decades and to discuss the consequences of these changes for the grouping as a whole and for its individual members. The focus of this article concentrates on the structure of production and structure of exports. According to Cui and Syed [4], Kojima [8] or Kocourek [5], the BRICS are continuously changing their export orientation from primary manufacturing and from production of merchandise with low added value, to more sophisticated goods. The whole group of the BRICS is gaining new competitive advantages mainly in the sector of machinery and transport equipment, but also in some others. The position of individual countries has been transforming significantly as well: China is gaining and consolidating the export positions mainly in the chemical industry (together with Russia), manufacturing, consumer goods, and of course machinery and transport equipment (together with India). de Vries et al. [19] shows that for China, India and Russia reallocation of labor across sectors is contributing to aggregate productivity growth, whereas in Brazil it is not.The rudimentary issue for this paper is the question of the driving forces leading to these changes. Is the development in the BRICS countries determined by the demand from abroad, the demand for their exports? Or are these transformations induced by the growing domestic demand from the establishing numerous middle class? The relevance of technological spill-over effects (discussed e.g. by Puškárová [13] or Montobbio and Rampa [10]) for the BRICS remains a subject of future research and will not be discussed here.The fundamental idea is following: If the share of a particular industry on exports of a country developes over time at a higher pace than the share of the industry on the gross value added, the structural change is predominantly driven by exports. If the pace of development of export share is lower or even of an opposite direction, then it must be the domestic demand inducing the structural shift. The influence of taxes and subsidies on individual shares of gross value added are not taken into account here.The analysis itself is rather straightforward: The shares of each individual industrial sector on the total gross value added were calculated from the national accounts data published by United Nations Statistics Division [16] and the shares of each individual industrial sector on the total value of exports were calculated from the ComTrade statistics of the United Nations Conference on Trade and Development [15]. Since panel data analysis does not seem to provide the proper instruments for reaching the aim of this paper, the calculated shares were in the following steps analyzed using the statistical methods of time series regression analysis.The results show a significant positive linkage between the structure of gross value added (GVA) and the structure of exports (X). Especially in the sectors of mining, quarrying, and manufacturing the foreign demand for exports plays a crucial role affecting the output of these industries. Weaker relationships were identified also in construction, financial intermediation, real estate, renting, and other business activities. In agriculture, hunting, forestry, fishing, electricity, gas, and water supplies, transport, storage, communication, public administration, education, health, and other service activities, the domestic customers of the five BRICS emerging markets represent more powerful and important driving factor than the foreign demand for the BRICS exports.

2. Research Methods

- There were two major problems identified to be solved before performing the structural analysis of the BRICS itself. First of them was the problem with compatibility of the data, the second one was the question of the best indicator showing the structural relations between the gross value added and the value of exports.

2.1. Data

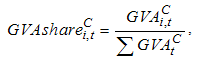

- The data on the gross value added in the sector composition were provided by the United Nations Statistics Division [16]. They are recorded and published following the International Standard Industrial Classification of All Economic Activities (ISIC, rev. 3). The data are available for the period 1980 – 2012 aggregated on the level of seventeen tabulation categories (from A to Q).For each BRICS country, each year and each of the tabulation categories (or a group of the categories) the share of the gross value added on the total gross value added of the whole economy was calculated using simple formula:

| (1) |

| (2) |

2.2. Correlation Analysis

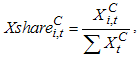

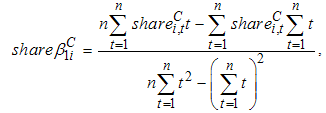

- The GVAshares and Xshares were calculated in every year of the period 1995 – 2012, which made it possible to investigate further their time series using the methods of regression analysis. The linear mean annual paces of change over the 18-year-long period have been estimated using ordinary least square correlation analysis:

| (3) |

|

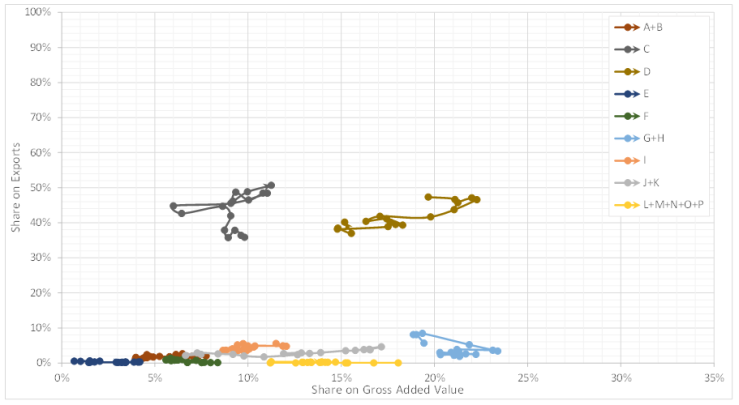

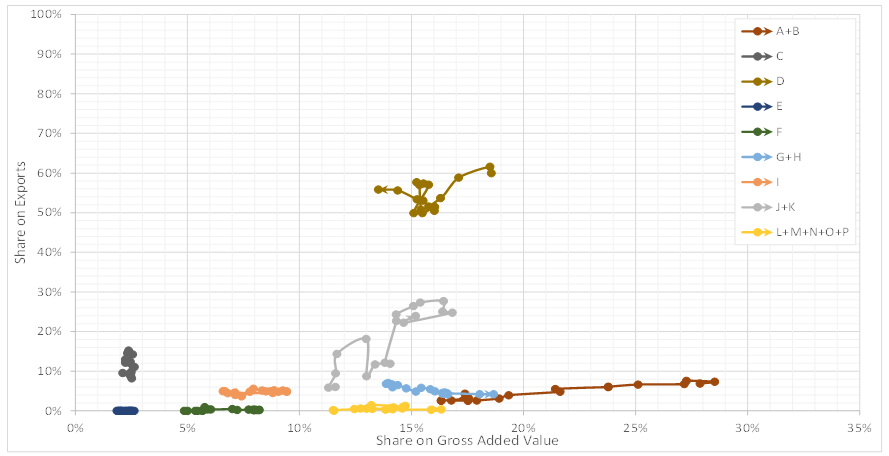

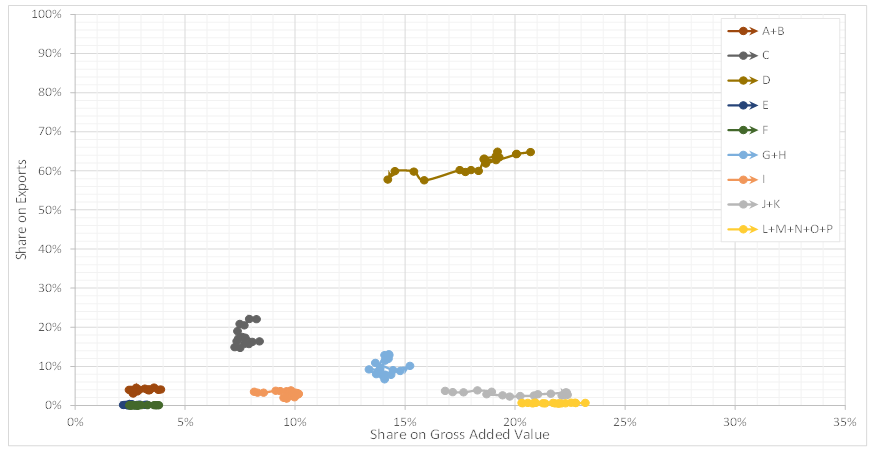

3. Results of the Analysis

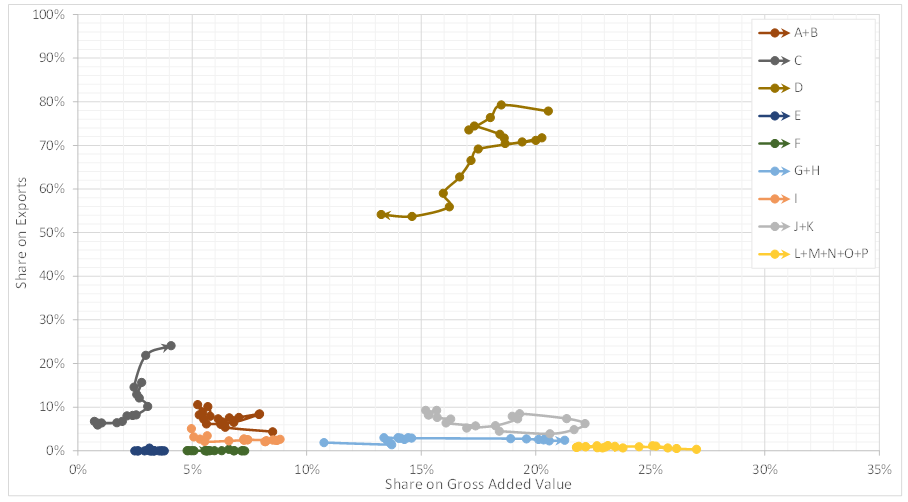

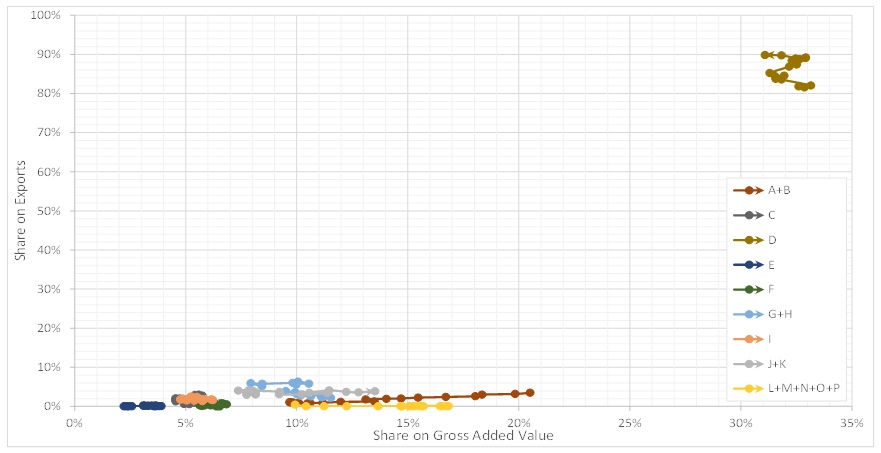

- The findings of the research for the five BRICS economies are first illustrated on a set of figures (Figure 1. – Figure 5.), where the dynamic paths of the computed GVAshares and Xshares are simply shown over the period 1995 – 2012 (for explanation of sectors see e.g. Tab. 2). The most interesting findings resulting from these five figures are following:For Brazil, the Fig. 1 highlights the dropping importance of manufacturing (sector D in ISIC rev. 3) for exports as well as for gross value added. On the other hand, the rise of exports and to a lesser extent also of GVA generated in mining and quarrying (industry C in ISIC) was recorded as well as an increasing share of wholesale and retail trade and of hotels and restaurants (industry G+H in ISIC) on Brazilian GVA with basically no reflection in their share of exports.

| Figure 1. Brazil |

| Figure 2. Russian Federation |

| Figure 3. India |

| Figure 4. China |

| Figure 5. South Africa |

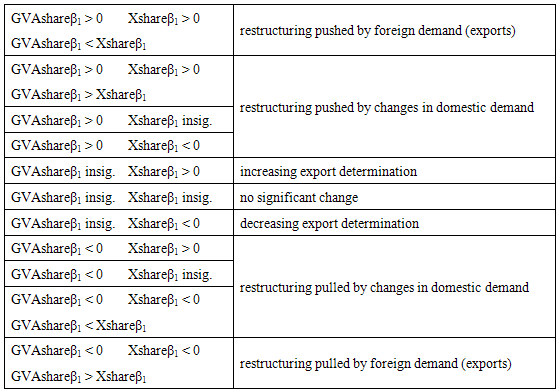

3.1. Driving Factors of the Structural Changes

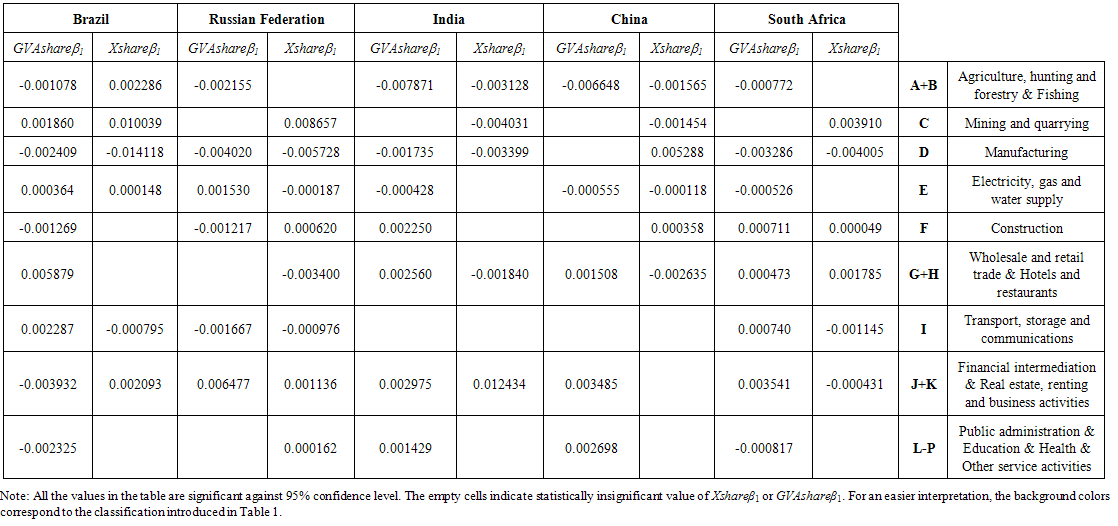

- The following Table 2 reveals the factors driving the changes in structure of gross value added in all the five BRICS economies following the proposed methodology summed up in the Tab. 1.

| Table 2. Driving Factors of Structural Changes in the BRICS |

4. Conclusions

- The results of this paper proved a long-run export reorientation of the BRICS from elementary raw materials processing and from low added value production, to more sophisticated merchandise. With some exceptions in Russian Federation and Brazil, the analysis generally confirms the Akamatsu’s flying geese paradigm [2]. Unfortunately, the level of aggregation of the data (enforced by using the United Nations statistical databases) does not allow for a more detailed research of structural changes within the main sectors of the BRICS national economies. This issue represents an attractive field for further research when more detailed data were available or by applying the Input-Output analyses on data collected in the World Input-Output Database.Even the findings achieved in this paper highlight some important issues: The success of Chinese export-oriented policy bears fruits for its economy and society, but also intensifies the competition, especially in the manufacturing sector. Chinese dominance as well as its size and ambitions have been already causing some fear and tensions on the Indian, Russian, as well as African side of the BRICS, challenging the very basics of the concept of the grouping as a sustainable economic entity [9].The fact, the BRICS countries are turning more and more to the production of high value added merchandise is a consequence of their previous rapid economic growth and development. Arising middle class in their societies magnifies the domestic demand for consumer goods and services, which consequently boosts the domestic demand for investment units, business equipment, raw materials, and semi-products. This strong stabilizing factor for economic performance of these giant markets was identified especially in the sectors of agriculture, electricity, gas and water supply, construction, transport, storage, communication, wholesale & retail trade (with an exception of South Africa, where exports from this sector play a crucial role), financial services, real estate, renting and other business activities (with an exception of India, where – again – exports from this sector play the leading role).A side effect of this continuous process can be identified in the growing dependence of Chinese and Indian economies on import of raw materials. Exports of raw materials and ores from these two Asian mega-markets are on a decline. In fact, they are absorbing the growing exports from Brazil, Russian Federation, and South Africa. In this context, a further deepening of mutual relations of the BRICS countries and strengthening the integration processes within this grouping seem sensible and advantageous for all the member states.An important role in the complex processes of restructuring has been probably played by the foreign direct investment (although Sharma [14] shows on example of India, the influence of foreign direct investment on exports is not as significant as one would expect) and also by the changing situation in the developed market economies. Analysis of these factors and their importance for restructuring the BRICS economies open a space for further research as it has the potential to provide new arguments to the debate on the future of the BRICS.

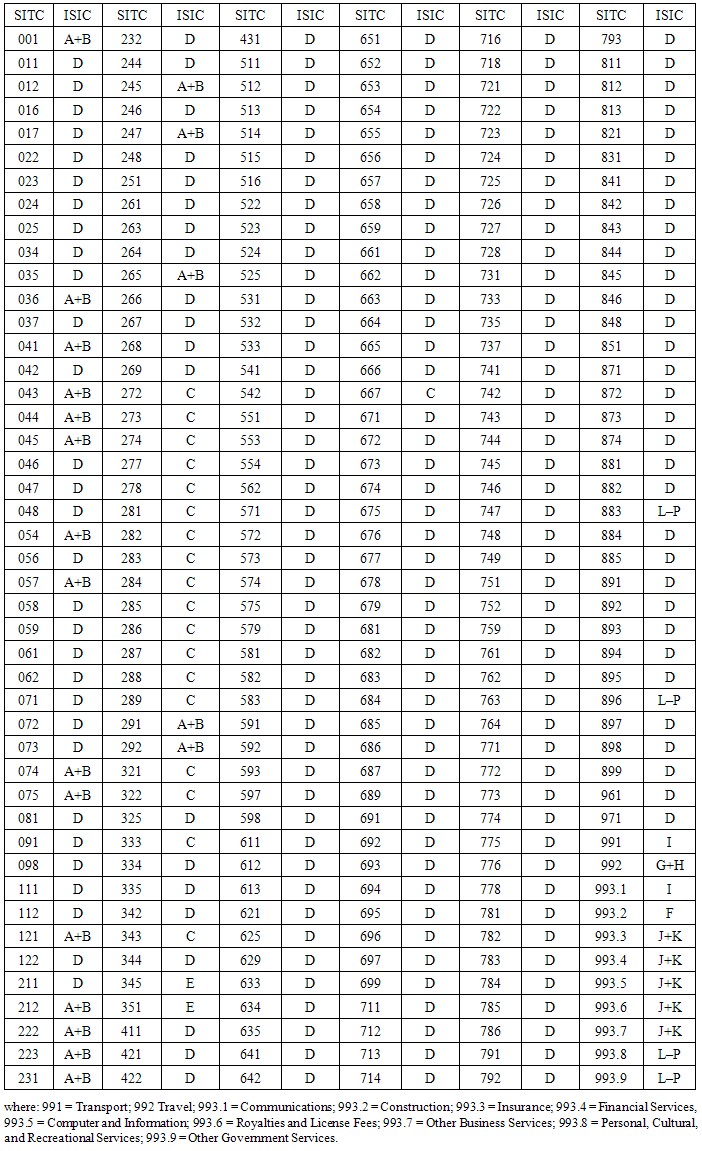

Appendix – ISIC, rev. 3 – SITC, rev. 3 Correspondence Table